How to Value ASX Bank Stocks Using the Dividend Discount Model

8 mins ago

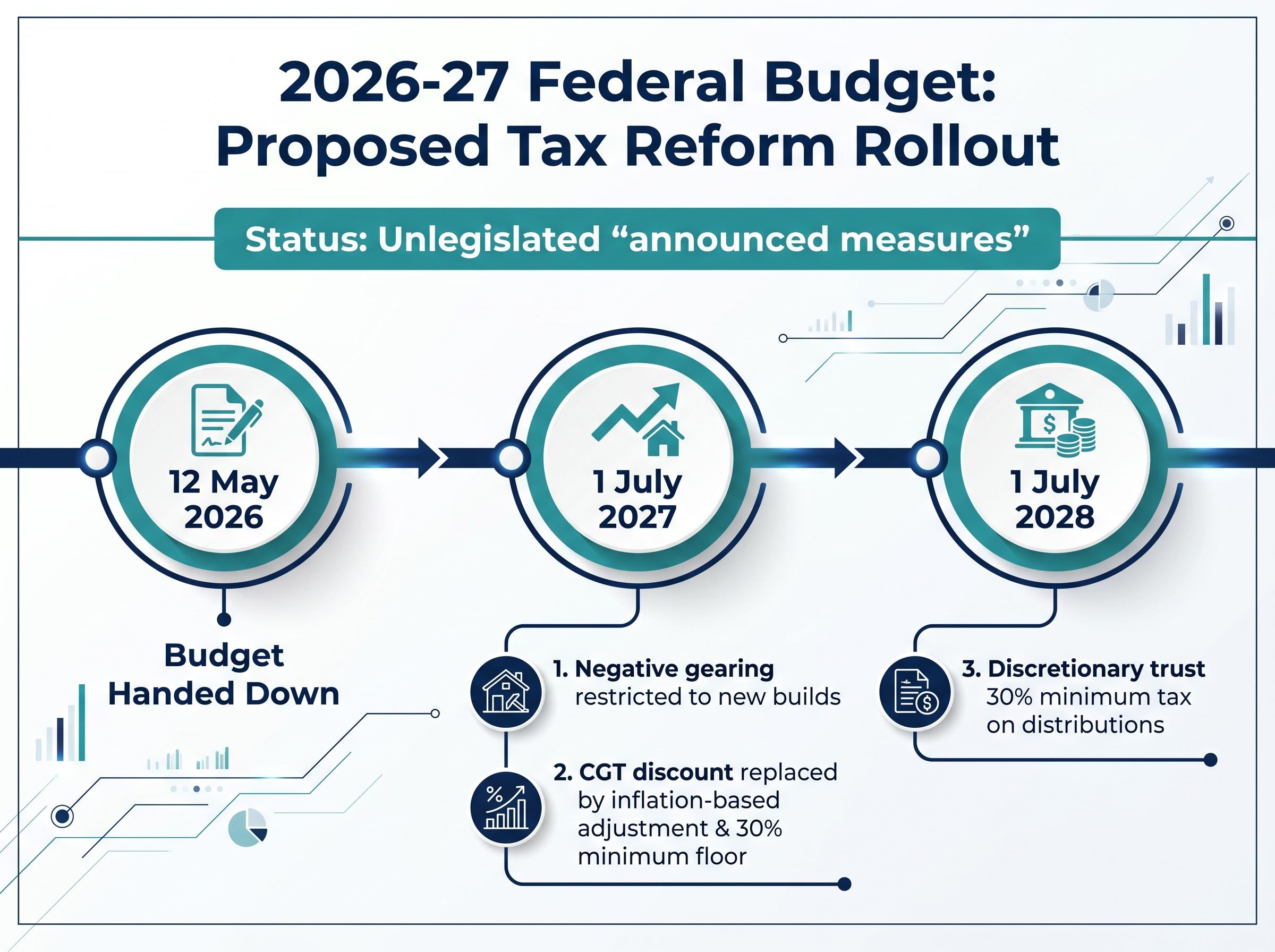

Australia’s 2026-27 Federal Budget, handed down on 12 May 2026, proposed the most significant overhaul of property and investment taxation in more than a decade. Three separate reforms target negative gearing, the capital gains tax discount, and discretionary trust distributions, each with its own implementation timeline and affected investor group.

With start dates set for 1 July 2027 and 1 July 2028, the planning window is already open. Yet none of the three measures has been legislated. No bills have been introduced, no parliamentary committee has considered them, and design details remain incomplete.

This explainer breaks down each proposed reform, distinguishes what is confirmed from what remains subject to legislation, and identifies which investor groups fall within scope, so readers can approach their advisers with informed questions rather than act on incomplete information.

The 2026-27 Budget did not announce a single tax reform. It announced three structurally separate changes that affect different, though overlapping, groups of investors. Negative gearing restrictions reshape the deduction landscape for residential property holders. A capital gains tax discount overhaul alters the after-tax outcome for anyone selling an appreciating asset. A discretionary trust minimum tax changes how family and business trusts distribute income.

Each measure carries a different implementation date, which means the urgency and planning horizon differ by reform.

Announced, not enacted. The Australian Taxation Office (ATO) lists the relevant personal income tax changes from the 2026-27 Budget as “announced measures” on its tax law and policy updates page, a designation that signals no legislation has been passed. This distinction matters for every section that follows.

| Reform | What changes | Who is affected | Implementation date |

|---|---|---|---|

| Negative gearing restricted to new builds | Deductions for losses on established residential properties removed | All residential property investors | 1 July 2027 |

| CGT discount replaced | Flat 50% discount replaced by inflation-based discount; 30% minimum tax floor on capital gains | All investors selling assets held longer than 12 months | 1 July 2027 |

| Discretionary trust minimum tax | 30% minimum tax rate applied to income distributions | Trustees and beneficiaries of discretionary trusts | 1 July 2028 |

Under the current framework, an investor who owns a residential property generating a rental loss can deduct that loss against other income, including salary and wages. This is negative gearing, and it applies regardless of whether the property is a newly constructed dwelling or an established home purchased on the secondary market.

The proposed change draws a hard line between the two.

From 1 July 2027, only new-build residential properties would qualify for negative gearing deductions. Investors holding established properties at the implementation date would lose the ability to offset rental losses against other income.

Key distinctions under the proposed rules:

No grandfathering provisions are indicated in the official Budget documentation, according to the Australian Government Budget 2026-27 tax reform measures published on 12 May 2026. This means existing property holders cannot assume their current arrangements will be protected.

The negative gearing changes also carry implications for the rental market and new construction pipeline: analyst forecasts point to modest national price softening of 3-5% and upward rental pressure, while new construction is projected to increase significantly from 2028 if state-level planning reforms accompany the federal measures.

The official Budget documentation does not define the precise criteria for new-build eligibility. Whether this covers off-the-plan purchases, substantial renovations, or only ground-up construction remains an open question. This detail will depend on the drafting of legislation, and investors should monitor its development closely.

For more than two decades, Australian investors selling an asset held longer than 12 months have applied a straightforward calculation: disregard 50% of the capital gain, then pay tax on the remainder at the individual’s marginal rate. The system is simple, and the benefit is identical whether the asset was held for 13 months or 13 years.

The proposed replacement introduces two changes that make the outcome less uniform.

First, the flat 50% discount would be replaced by an inflation-based discount. Rather than halving the gain automatically, the discount would adjust the gain for changes in the price level over the holding period. In a low-inflation environment, this produces a smaller discount than the current 50%; in a high-inflation environment, the adjustment could be more generous for long-held assets.

Second, a minimum 30% tax rate would apply to capital gains. Investors whose marginal rate currently sits below 30% would face a higher effective tax on gains than they do under the existing system.

| Feature | Current framework | Proposed framework |

|---|---|---|

| Discount type | Flat 50% | Inflation-based adjustment |

| Minimum tax rate on gains | None (taxed at marginal rate) | 30% floor |

| Small business CGT concessions | Available | Preserved, no alterations announced |

Small business carve-out. Small business CGT concessions are explicitly preserved under the announced measures. Eligible small business owners selling qualifying assets are not affected by the proposed discount replacement or the 30% floor.

The implementation date is 1 July 2027, the same as the negative gearing restrictions. The precise mechanics of the inflation-based calculation have not been published and will depend on forthcoming legislation.

The CGT discount abolition widens the structural tax advantage of superannuation over personal investment by approximately 20 percentage points on exit, because SMSFs are fully exempt from the new framework and maintain their existing 10% effective CGT rate while personal investors and trusts transition to the new inflation-indexed system with a 30% floor.

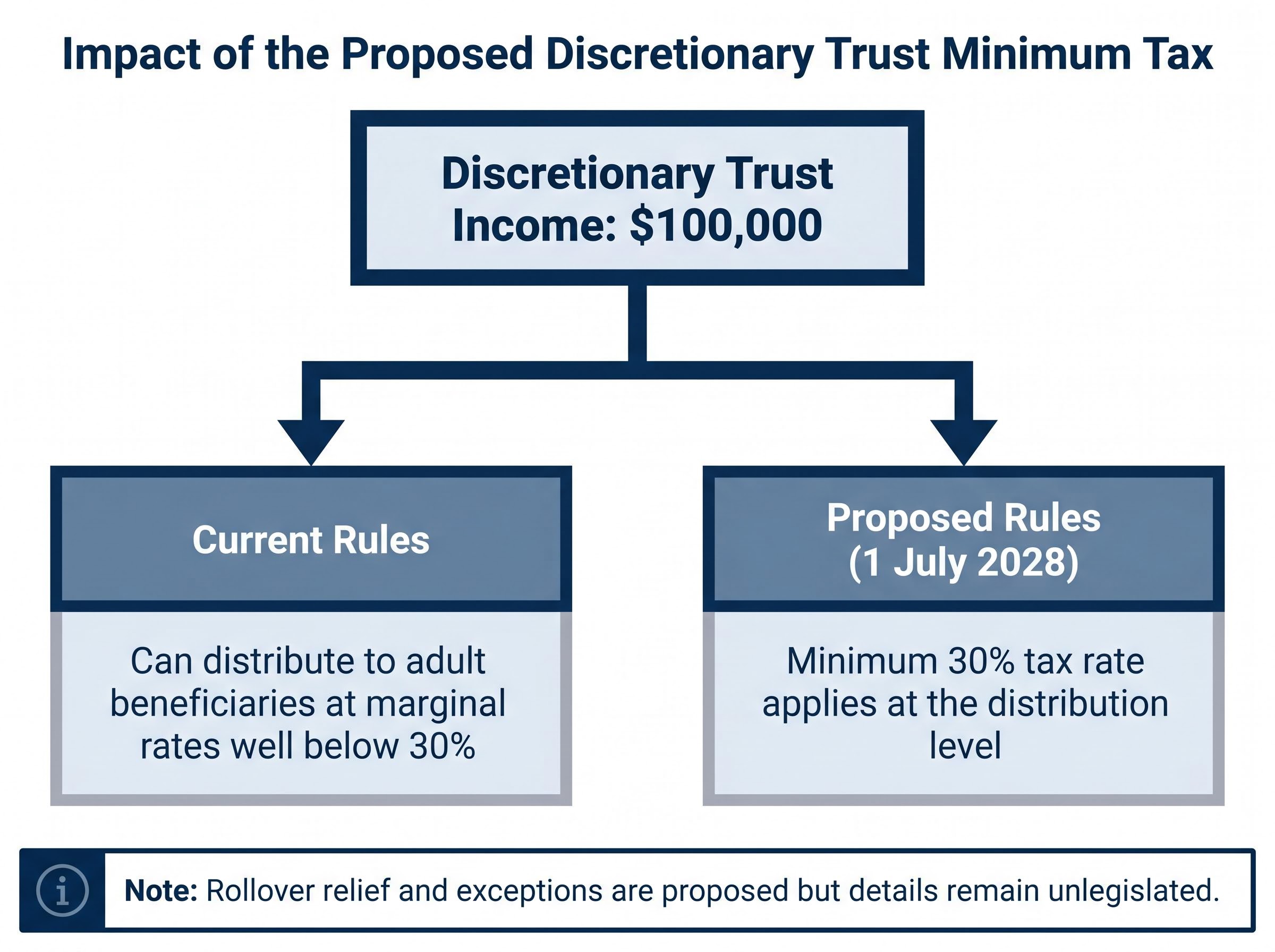

A discretionary trust is a legal structure in which a trustee holds assets on behalf of a group of beneficiaries. The trustee has the discretion to decide how much income to distribute to each beneficiary in a given year. This flexibility is the feature that has made discretionary trusts one of the most widely used tax planning structures in Australia.

Under existing rules, a trustee can distribute income to beneficiaries on lower marginal tax rates, reducing the overall tax paid by the family or business group. A trust earning $100,000 could, for example, distribute that income across several adult beneficiaries, each of whom may pay tax at rates well below 30%.

From 1 July 2028, a minimum 30% tax rate would apply to discretionary trust income distributions. The mechanics, based on the Budget announcement, work as follows:

This would reduce the effectiveness of distributing income to beneficiaries on lower marginal rates, which is the structural advantage that made income-splitting through trusts attractive in the first place.

The Budget announcement confirms that exceptions to the minimum tax will apply and that rollover relief provisions are included in the announced measures. However, the scope of both remains subject to draft legislation. Which categories of trusts or distributions may be exempted, and how rollover relief would operate in practice, are details that have not yet been published.

Investors and advisers should treat this as a known unknown. The 1 July 2028 implementation date provides a longer planning runway than the other two reforms, but it also extends the period of uncertainty about design.

The phrase “Budget announcement” carries less legal weight than readers may assume. A measure announced in the Budget is a statement of Government policy intent. It becomes law only after a bill is introduced to Parliament, debated, passed by both houses, and given Royal Assent.

As of late May 2026, none of the three tax reforms has reached even the first stage of that process. No bills have been introduced. No parliamentary committee consideration has been reported.

The ATO tax law and policy updates page designates both the negative gearing restrictions and the CGT discount replacement as announced measures that are not yet law, confirming that neither reform has passed Parliament as of the 2026-27 Budget announcement date.

What “announced measure” means on the ATO’s website. The ATO lists Budget measures separately from enacted law on its tax law and policy updates page. An “announced measure” is one the Government has committed to pursuing but that has not yet passed Parliament. It is not yet the law, and its design may change during the legislative process.

The gap between announcement and legislation matters because each reform carries open design questions that could materially affect the final rules:

Professional tax commentary from firms including KPMG and PwC, published between March and May 2026, consistently notes the unlegislated status of all three measures and advises clients to plan with flexibility rather than certainty.

For investors whose tax planning relies on retirement-timing strategies or testamentary trust structures, our dedicated guide to the proposed 30% CGT floor examines these specific scenarios in depth, including why testamentary trusts cannot be grandfathered by any living person today and the risks of restructuring portfolios before the measure is legislated.

The two implementation dates, 1 July 2027 and 1 July 2028, serve as planning anchors rather than action deadlines. Professional commentary from major tax advisory firms recommends a sequenced approach calibrated to specific circumstances.

For investors and early employees holding startup equity or low-cost-base shares, our deep-dive into CGT indexation for founders explains why the inflation adjustment provides negligible relief when the original outlay is minimal, with a $10,000 cost base on a $5 million exit generating an indexation benefit of only around $3,400 over a decade, and how Canada and the United Kingdom have addressed this with entrepreneur-specific CGT carve-outs that Australia’s reform does not replicate.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

These statements relate to announced Government policy that has not yet been legislated. The final design and implementation of these measures are subject to change based on the parliamentary process.

The 2026-27 Federal Budget proposed three distinct tax reforms: negative gearing restricted to new builds from 1 July 2027, the 50% CGT discount replaced by an inflation-based mechanism with a 30% minimum tax floor from the same date, and a 30% minimum tax on discretionary trust distributions from 1 July 2028. Each is significant in scope. None is yet law.

The distinction between announcement and legislation is not a technicality. It is the single most relevant fact for any investor deciding how to respond. The planning window is open, but it should be used for preparation, not premature action.

Readers affected by any of the three reforms should seek qualified tax advice tailored to their specific asset holdings, structures, and circumstances before the implementation dates arrive.

The 2026-27 Federal Budget proposed three reforms: negative gearing restricted to new-build residential properties from 1 July 2027, the 50% CGT discount replaced by an inflation-based mechanism with a 30% minimum tax floor from 1 July 2027, and a 30% minimum tax on discretionary trust distributions from 1 July 2028.

No. As of late May 2026, none of the three proposed tax reforms have been legislated. No bills have been introduced to Parliament, and the ATO lists the negative gearing and CGT discount changes as announced measures that are not yet law.

From 1 July 2027, the flat 50% CGT discount would be replaced by an inflation-based adjustment, and a 30% minimum tax floor would apply to capital gains, meaning investors on lower marginal rates could face higher effective tax on gains than under the current system.

From 1 July 2027, only new-build residential properties would qualify for negative gearing deductions. Investors holding established properties would lose the ability to offset rental losses against other income, and no grandfathering provisions are indicated in the Budget documentation.

The professional advice from major tax firms is to monitor legislative progress closely, seek personalised tax advice on distribution strategies, and plan methodically ahead of the 1 July 2028 start date rather than acting before the design details are confirmed through legislation.