Nuix Limited raised A$1.7 billion at its December 2020 IPO by pointing investors toward a metric that appears nowhere in its statutory accounts. ASIC later argued that very metric sat at the heart of whether the company met its legal obligations to the market.

Annual Contract Value is one of the most widely cited performance indicators for ASX-listed software and subscription companies, yet it is not defined by accounting standards, not audited in the same way as statutory revenue, and not calculated consistently across companies. For Australian retail investors evaluating technology stocks, understanding what ACV does and does not tell you has become a practical necessity rather than an academic exercise.

This piece explains what ACV measures, why it diverges from reported revenue, how Australian regulators treat it, and what a live enforcement case reveals about the risks of taking the metric at face value. By the end, readers will have a framework for evaluating ACV disclosures critically rather than accepting them as straightforward growth signals.

Understanding ACV from the ground up: the basics every investor needs

A software company with 100 customers each paying A$10,000 per year has contracted revenue of A$1 million. That contracted position, the total annualised value of all active agreements at a given date, is what Annual Contract Value captures. It does not matter whether those contracts were signed last week or three years ago; ACV reflects the current run-rate.

The metric exists because traditional revenue recognition rules were designed for product sales, not multi-year subscription contracts. When a company sells a perpetual licence, the transaction is relatively straightforward. When it sells a three-year subscription, accounting standards require the revenue to be spread across the life of the contract. ACV was developed to give investors a view of the total contracted scale of a subscription business at a point in time, separate from the portion that accounting rules permit to appear on the income statement.

ASX software business economics, particularly the 75-90% gross margins that characterise established SaaS platforms, explain why investors and analysts place such emphasis on contracted run-rate metrics: when direct delivery costs are near-zero per additional subscriber, contracted scale becomes a more meaningful predictor of future profitability than near-term reported revenue.

Nuix Limited describes ACV as measuring total contracted revenue on an annualised basis, captured at a specific date. This is representative of how most ASX subscription companies define it. ASIC’s MoneySmart guidance advises that non-statutory management metrics of this kind should always be read alongside statutory profit and revenue figures.

Three related metrics are worth distinguishing:

- ACV (Annual Contract Value): The annualised value of all active contracts at period-end; a snapshot of the current contracted run-rate

- ARR (Annual Recurring Revenue): Often used interchangeably with ACV but may include or exclude different contract types depending on the company’s definition

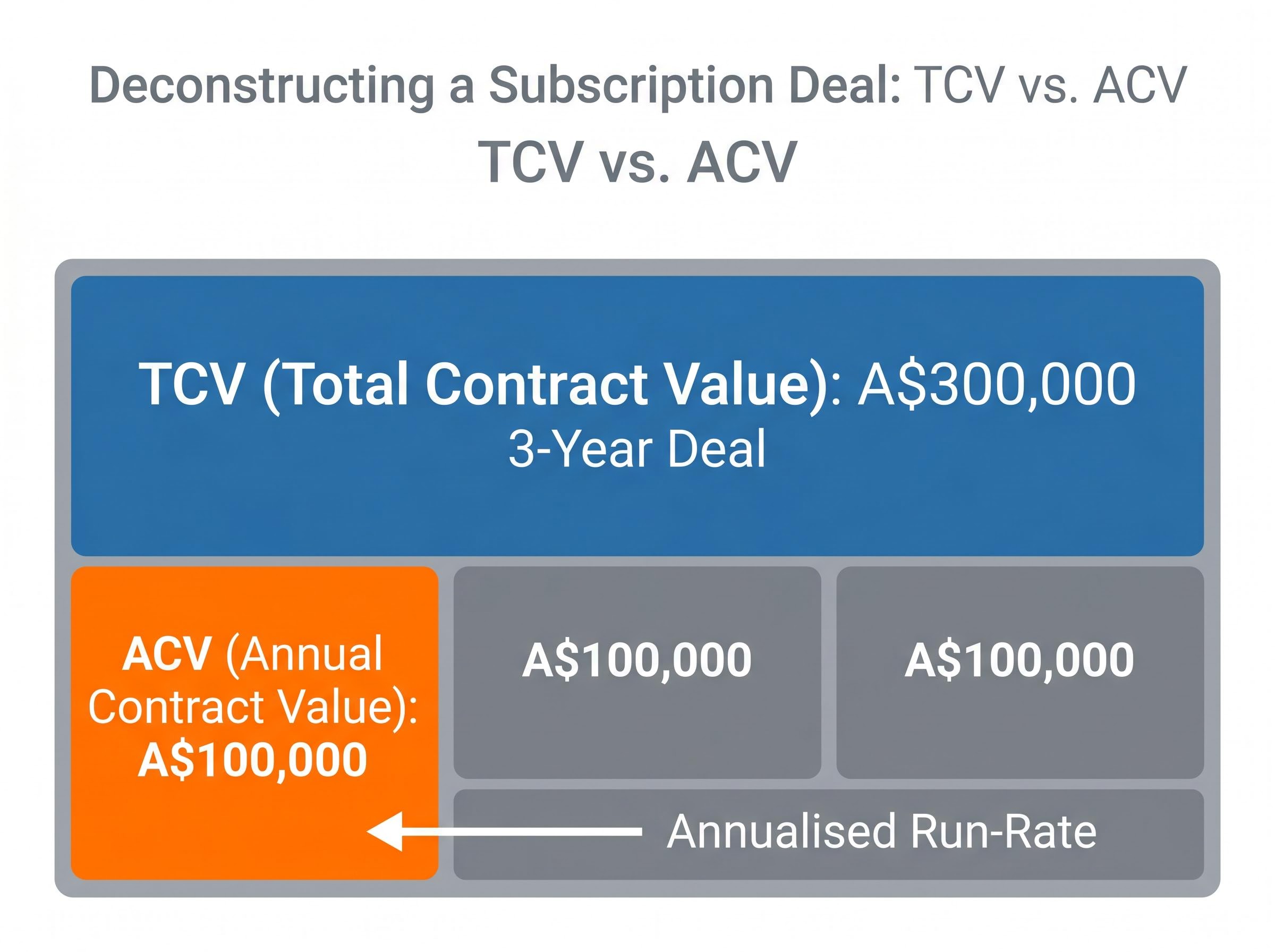

- TCV (Total Contract Value): The full value of a contract over its entire life, not annualised; a three-year deal worth A$300,000 has a TCV of A$300,000 but an ACV of A$100,000

When big ASX news breaks, our subscribers know first

What Annual Contract Value actually measures

ACV is a snapshot of the annualised value of all active subscription or licence contracts at a specific point in time. It is distinct from recognised revenue, distinct from cash received, and distinct from any measure defined by Australian Accounting Standards (AASB). It is a contracted run-rate metric: it reflects the full annualised value of current contracts regardless of where in the contract term the company currently sits.

That distinction is what makes ACV worth understanding. Two subscription businesses can report identical statutory revenue in a given half-year and have radically different contracted futures. The one with a higher ACV has more revenue locked in under active agreements; the one with a lower ACV may be relying on new sales to sustain the same revenue trajectory.

ACV is also a non-statutory metric. It is not required by ASX Listing Rules, not governed by a single standard definition, and not subject to the same audit rigour as income statement revenue. What each company includes in ACV, whether professional services, trial contracts, or contracts with uncertain enforceability, varies.

What ACV includes versus what it does not:

- Includes: The annualised value of active subscription and licence contracts at a specific date

- Does not include: Revenue already earned and recognised under AASB 15, cash received from customers, or any figure defined by statutory accounting standards

- May or may not include (varies by company): Professional services revenue, short-term trial agreements, contracts with uncertain renewal prospects

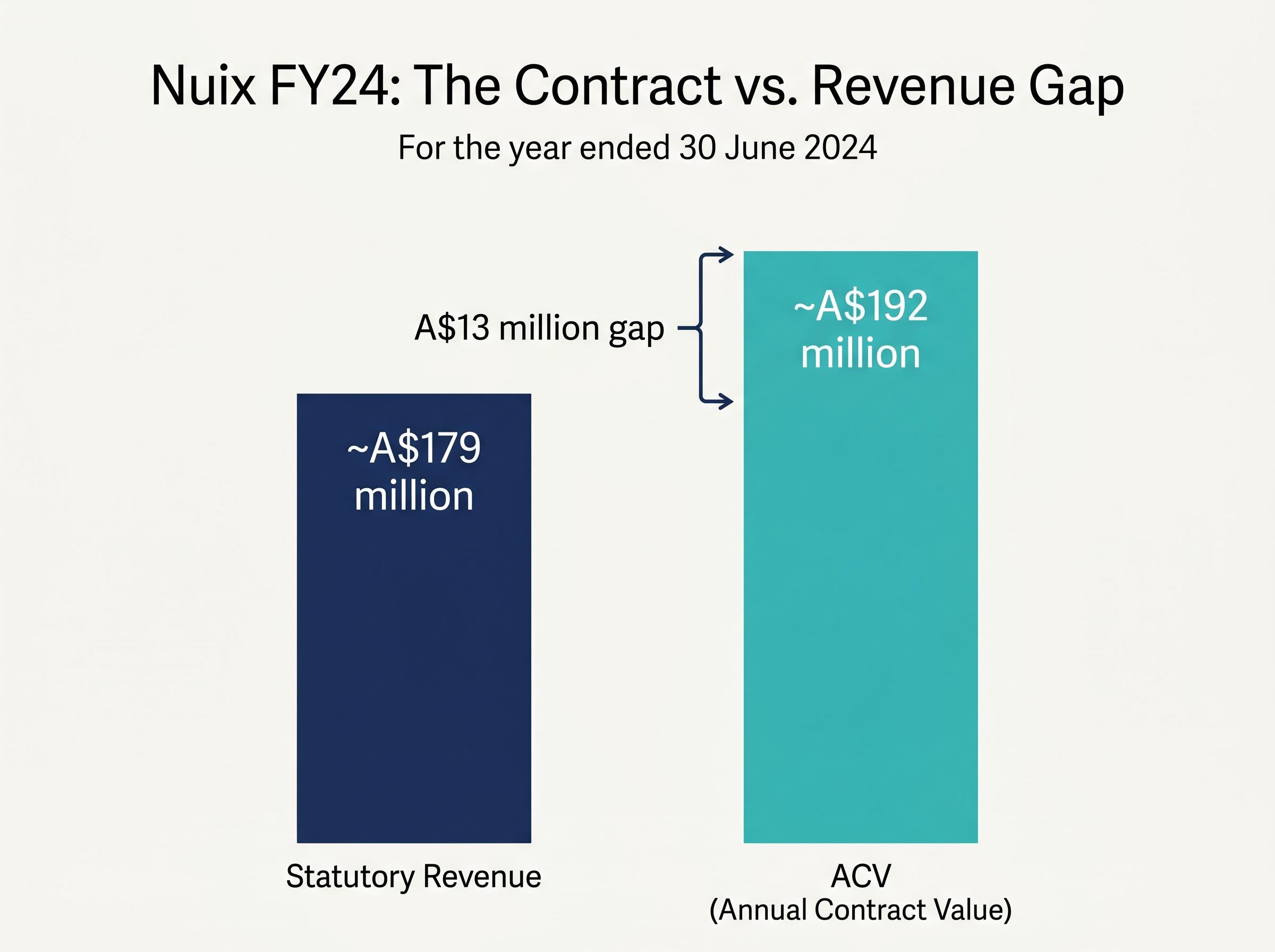

Nuix, FY24: ACV at 30 June 2024 was approximately A$192 million versus statutory revenue of approximately A$179 million for the same year. That A$13 million gap between contracted run-rate and reported revenue illustrates the timing divergence in concrete terms.

Why ACV and statutory revenue tell different stories

The gap between ACV and statutory revenue is not a quirk of presentation. It is an inevitable consequence of how accounting standards treat contract-based businesses.

| Period | ACV (A$m) | Statutory Revenue (A$m) |

|---|---|---|

| FY24 (year ended 30 June 2024) | ~192 | ~179 |

| 1H FY25 (half ended 31 December 2024) | ~198 | Not directly comparable (half-year) |

Nuix’s 1H FY25 ACV of approximately A$198 million (as at 31 December 2024) shows the contracted run-rate continuing to exceed prior-year statutory revenue. For a healthy subscription business, ACV growth preceding statutory revenue growth is the expected pattern. The question is whether contracted value converts into earned income at the anticipated rate.

The AASB 15 timing effect explained

Under AASB 15 (Revenue from Contracts with Customers), a three-year licence signed in July is not fully recognised as revenue in the first year. Only the proportional portion earned in that reporting period appears in the income statement. Revenue is recognised progressively over the life of the contract, matching the delivery of the service to the customer.

ACV, by contrast, counts the full annualised value of that same contract from the moment it is active. A A$300,000 three-year deal contributes A$100,000 to ACV immediately; the income statement recognises a fraction of that in the first reporting period based on the number of months elapsed.

This structural lag means ACV functions as a leading indicator of future statutory revenue, but only if contracts convert, renew, and do not churn. A widening gap between ACV and statutory revenue over multiple periods, rather than a closing one, can signal execution problems: contracted value that is not converting to earned income at the expected rate.

How Australia’s regulatory framework governs ACV disclosures

ACV may be a management metric, but getting it wrong carries legal consequences. Three interlocking regulatory instruments govern how ASX-listed companies present non-statutory measures of this kind.

ASIC Regulatory Guide 230 sets out the three-part framework that governs how listed companies must present non-statutory metrics: labelling them clearly as non-IFRS, reconciling them to the nearest comparable statutory measure, and ensuring they are not given prominence that overshadows audited results.

ASIC Regulatory Guide 230 (RG 230), the regulator’s primary guidance on non-IFRS financial information, imposes a three-part requirement:

- Label clearly: Non-IFRS financial information must be explicitly identified as non-statutory and distinguished from AASB-defined measures

- Reconcile: The metric must be reconciled to the most directly comparable statutory (IFRS) measure, so investors can see the bridge between the two

- Do not give undue prominence: Non-IFRS figures must not be presented in a way that overshadows or obscures statutory results

The core RG 230 principle in plain terms: Companies can report ACV, but they cannot present it in isolation, without reconciliation, or in a way that makes it appear more reliable than the audited statutory figures it sits alongside.

ASIC Information Sheet 247 extends these requirements to the operating and financial review section of annual reports, covering metrics including ACV and ARR. ASX Guidance Note 8 on continuous disclosure applies when ACV is used in ASX announcements or investor presentations, requiring that forward-looking metrics be supported by reasonable grounds and not be misleading.

ASIC’s treatment of ACV in the Nuix proceedings explicitly signals that contract-based performance indicators are not exempt from these obligations.

ASIC’s FY2026-27 reporting priorities extend the same disclosure-quality expectations into revenue recognition and fair value measurement, signalling that the regulator’s scrutiny of how companies present financial information to investors is broadening well beyond the ACV context.

The Nuix case: when ACV becomes a regulatory flashpoint

Nuix Limited listed on the ASX in December 2020 at A$5.31 per share, achieving a market capitalisation of approximately A$1.7 billion. ACV featured prominently in the prospectus as a growth signal, giving investors a view of contracted scale that statutory revenue alone could not provide.

What followed turned that prominence into a regulatory test case.

- December 2020: Nuix lists on the ASX at A$5.31 per share

- September 2022: ASIC commences civil penalty proceedings alleging continuous disclosure failures, misleading conduct, and directors’ duty breaches connected to representations about ACV and forward-looking metrics

- April 2026: The Federal Court dismisses ASIC’s allegations

- 3 May 2026: ASIC lodges an appeal to the Full Federal Court

- As at 25 May 2026: No hearing date has been publicly confirmed; ASIC is not appealing findings relating to Nuix’s board directors

The Nuix ASIC Federal Court appeal, filed on 22 May 2026, targets Nuix as a company only, with former directors explicitly excluded from the regulator’s grounds, a distinction that shapes how investors should read the residual legal risk attached to the stock.

ASIC’s original proceedings covered three broad grounds: continuous disclosure under s674 of the Corporations Act and ASX Listing Rule 3.1; misleading or deceptive conduct under s1041H of the Corporations Act and s12DA of the ASIC Act; and directors’ duties under ss180-183 of the Corporations Act. ASIC’s central argument is that ACV and related forecasts constituted material information requiring disclosure, not merely supplementary management metrics.

What ASIC is asking the Full Federal Court to find

ASIC’s appeal contends that the primary judge misapplied the continuous disclosure provisions in the context of forward-looking ACV representations. The regulator argues that statements and omissions about Nuix’s ACV and associated revenue forecasts should have triggered immediate disclosure obligations.

The appeal is ongoing and no outcome should be assumed. The purpose of referencing it here is to illustrate regulatory risk, not to adjudicate the merits. What matters for investors is the principle ASIC is testing: that for subscription businesses, non-statutory metrics like ACV can independently attract continuous disclosure and misleading conduct obligations under Australian law.

What investors should actually check when they see an ACV figure

ACV is not cash. Contracted value that has not converted to billings or cash receipts carries execution risk regardless of how prominently ACV growth features in reporting. ACV definitions are not standardised; each issuer determines what to include, and those definitions can shift between reporting periods.

Five practical cross-checks convert the metric from a headline number into a structured due diligence step:

- Compare ACV growth against statutory revenue growth trajectory. Material divergence that persists over multiple periods warrants scrutiny; the gap should narrow over time if contracts are converting as expected

- Reconcile ACV to invoiced billings and cash receipts from customers. If ACV is growing but cash from customers is not, the contracted value may not be converting to realised income

- Track net ACV additions, not just the headline figure. New ACV minus churned ACV reveals whether growth is coming from expansion or merely replacing lost contracts

- Read the issuer’s own definition of what is included in ACV. Determine whether professional services, trial contracts, or agreements with uncertain enforceability are captured in the figure

- Check whether ASIC-required reconciliations to IFRS measures are provided and consistent over time. The absence of a reconciliation is itself a signal worth noting

Management incentive structures tied to ACV targets can create presentation incentives that investors should factor into their assessment. Where executive remuneration is heavily weighted toward ACV milestones rather than cash flow or statutory earnings, the metric may receive disproportionate emphasis in investor materials.

The core principle: ACV is a forward-looking contracted value indicator. It is not revenue and it is not cash. Treating it as either understates the gap between what a company has promised on paper and what it has delivered to the bank account.

ACV as a metric with teeth: what the Nuix appeal means for ASX software investors

ASIC’s explicit treatment of ACV as potentially triggering continuous disclosure obligations signals something broader than one company’s legal proceedings. For subscription and SaaS businesses listed on the ASX, non-statutory metrics are not peripheral; in the regulator’s view, they can be independently material.

The Nuix case is not isolated. The iSignthis matter, in which ASIC challenged non-standard performance metrics in investor communications, established a prior reference point. Proxy adviser Ownership Matters has recommended that boards adopt explicit policies governing non-IFRS metric presentation under RG 230, a sign that governance expectations are moving in the same direction as regulatory enforcement.

The implication for investors is direct. If ACV is material enough to attract regulatory scrutiny, it is material enough to warrant systematic due diligence rather than acceptance as a given.

- ACV as a leading indicator: Useful when read alongside churn rates, net retention, and cash conversion; misleading when taken at face value in isolation

- Regulatory obligations attach: Companies presenting ACV face disclosure requirements under RG 230, INFO 247, and ASX Guidance Note 8; investors have a right to expect compliant presentation

- The five-step cross-check framework: Compare to statutory revenue, reconcile to cash, track net additions, read the definition, and verify reconciliations are present and consistent

Other ASX-listed subscription businesses, not just Nuix, present ACV or ARR as central performance indicators. The principles being tested in the Nuix appeal carry sector-wide relevance.

For investors wanting to see how these principles played out at the portfolio level across a recent market cycle, earnings quality in ASX tech stocks proved to be the primary determinant of recovery: companies with demonstrated profitability and positive cash flow before the 2025-2026 drawdown recovered materially faster than high-ACV, high-growth peers that had not converted contracted value into earnings.

Separating contracted promise from financial reality in ASX tech stocks

Annual Contract Value is a forward-looking contracted value indicator that carries regulatory weight in Australia. It is not a substitute for statutory revenue or cash flow analysis, and the regulatory framework governing its presentation, from RG 230 through to the continuous disclosure provisions ASIC is testing in the Nuix appeal, confirms that how companies present this metric matters legally.

Investors evaluating ASX technology or SaaS stocks can apply the five cross-checks outlined above to any company reporting ACV: read the issuer’s definition, compare ACV growth to statutory revenue, reconcile to cash, track net additions, and verify that RG 230-compliant reconciliations are provided. ASIC’s RG 230 and MoneySmart resources are freely available for further context on non-IFRS metrics.

The Nuix appeal remains a standing reminder that contracted revenue figures are not exempt from disclosure law. Investors who understand the mechanics and limitations of ACV are better positioned to evaluate these stocks on evidence rather than narrative.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.