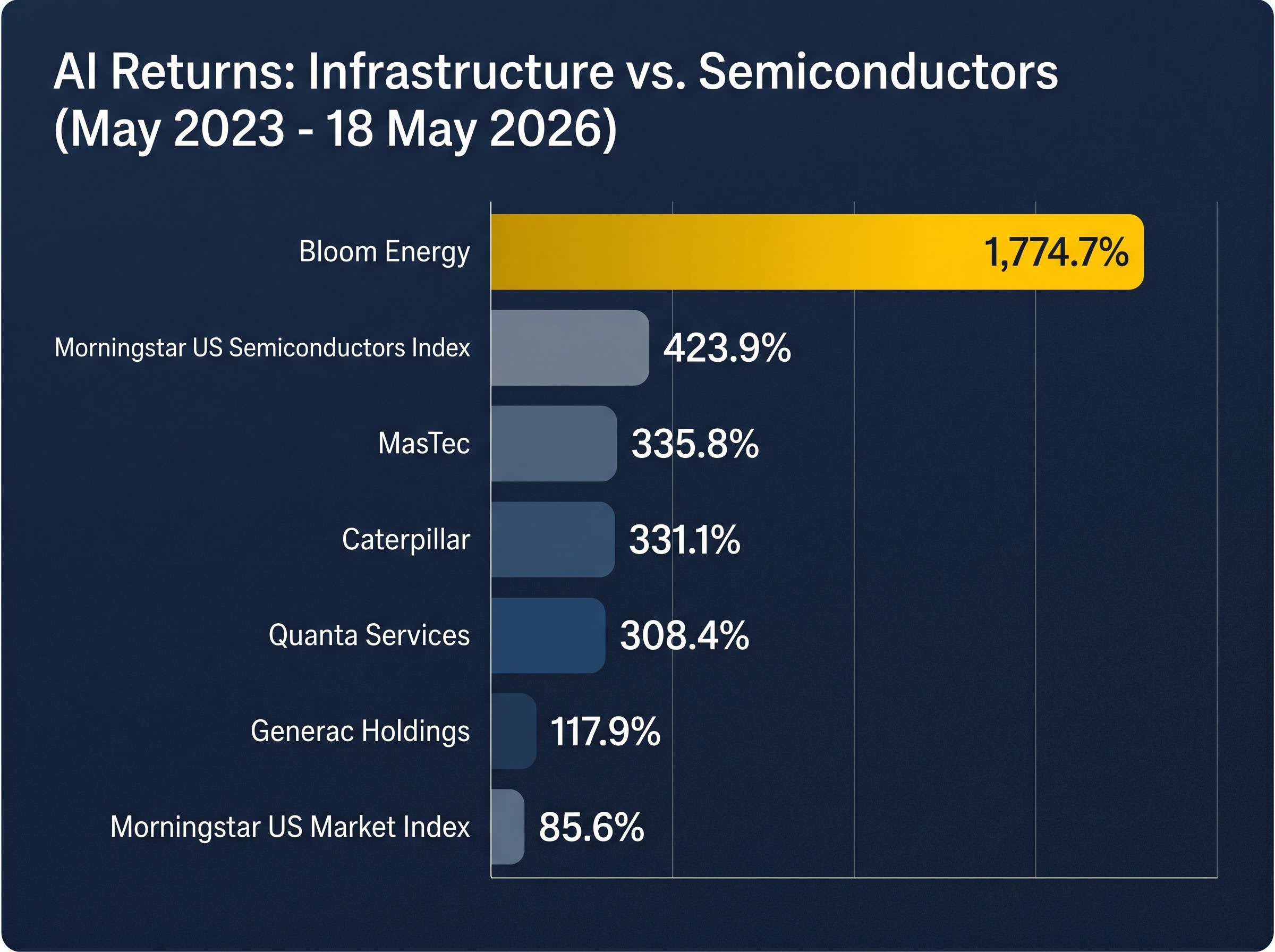

Bloom Energy shares returned 1,774.7% over three years. Caterpillar returned 331.1%. MasTec returned 335.8%. None of them make a single chip. Since Nvidia’s May 2023 earnings ignited the AI trade, most investor attention tracked semiconductor stocks, whose collective index returned 423.9% through May 2026. But a quieter, and in some cases more dramatic, rotation has been unfolding in industrial contractors, power generators, and energy infrastructure firms supplying the physical backbone AI actually runs on. This analysis identifies the specific industrial and power companies generating outsized AI infrastructure stock returns, explains the structural mechanics that make this trade durable, and surfaces the risks investors need to weigh before adding non-tech AI exposure to a US equity portfolio.

The returns that the semiconductor narrative buried

The numbers tell the story before the argument needs to. The Morningstar US Semiconductors Index delivered a cumulative 423.9% return from May 2023 through 18 May 2026, a stretch that made chipmakers the default AI trade. The Morningstar US Market Index returned 85.6% over the same window. Several industrial names beat them both.

Bloom Energy returned 1,774.7% over three years through 18 May 2026, more than quadrupling the semiconductor benchmark.

Caterpillar returned 331.1%. Quanta Services delivered 308.4%. MasTec posted 335.8%. Even Generac Holdings, the weakest performer in this group, returned 117.9%, still exceeding the broad market by a wide margin. Meanwhile, the Morningstar North America Software Application Index returned just 17.6% over the same period.

| Stock / Index | Three-Year Total Return (May 2023 to 18 May 2026) |

|---|---|

| Bloom Energy | 1,774.7% |

| MasTec | 335.8% |

| Caterpillar | 331.1% |

| Quanta Services | 308.4% |

| Generac Holdings | 117.9% |

| Morningstar US Semiconductors Index | 423.9% |

| Morningstar US Market Index | 85.6% |

This outperformance is not a recent catch-up trade. It compounded across the full three-year AI cycle, largely unnoticed while analyst coverage and media attention concentrated on semiconductors. Investors who anchored their AI thesis solely to chip stocks missed returns comparable to, or exceeding, the semiconductor index in companies they may not have considered AI plays at all.

The AI infrastructure investment shift from software-centric capital allocation to physical assets has been underway long enough to show up in Wall Street’s own projections: analysts anticipate $530-700 billion in global data-centre IT spending for 2026, with alternative energy providers and on-site generation solutions emerging as primary beneficiaries of capital that would previously have flowed toward enterprise software.

When big ASX news breaks, our subscribers know first

Why data centres became a power and construction crisis before they became a chip crisis

AI data centres are extraordinarily power-dense. A single large-language model training cluster can draw tens of megawatts, and as inference workloads scale, the electricity requirement is sustained rather than temporary. The result is that electricity delivery, not chip supply, is now the binding constraint on how fast AI infrastructure can be built.

The scale of projected demand growth makes the point concrete. DOE-affiliated analysis and independent research suggest US data-centre electricity demand could rise from roughly 4% of total US consumption in 2023-2024 to as much as 6.7-12% by 2028-2030. Approximately 20 GW of new data-centre load is projected by 2030. Wood Mackenzie, BloombergNEF, and S&P Global have all identified AI and data-centre demand as a defining 2026 power market driver.

The DOE data centre electricity demand projections, published in December 2024 by Lawrence Berkeley National Laboratory, confirm that data centres consumed 4.4% of total US electricity in 2023 and are expected to reach 6.7% to 12% of consumption by 2028, providing the official federal benchmark against which utility planners and infrastructure contractors are sizing their buildout commitments.

Meeting that demand requires buildout across five distinct infrastructure categories:

- Grid hookups and interconnection

- Substations and power distribution

- Transmission lines and upgrades

- Gas generation and backup power systems

- Cooling infrastructure

Where the grid falls short

The bottleneck is not a lack of willingness to build. Grid interconnection queues have swelled as data-centre operators apply for utility-scale power connections, and substation lead times now extend years into the future. Permitting delays compound the problem; physical construction timelines for transmission and distribution infrastructure mean that contracted work for firms like Quanta Services and MasTec extends well beyond the current fiscal year. This is what converts a demand surge into multi-year revenue visibility. The spending is not discretionary and cannot be accelerated past the physical constraints, which means the firms solving these constraints have durable, contracted backlogs rather than one-cycle order books.

Grid interconnection constraints are creating a two-speed buildout dynamic: firms with contracted backlog tied to physical transmission and substation work are accumulating multi-year revenue visibility, while data-centre operators that cannot secure grid hookups in time are accelerating adoption of on-site alternatives, a divergence that has distinct implications for how each part of the infrastructure trade performs through the cycle.

Understanding this power constraint reframes the AI infrastructure trade from a momentum story into a capacity story, which has direct implications for how investors should think about entry timing and holding period.

A field guide to the companies collecting the infrastructure dividend

The companies benefiting from the AI buildout fall into distinct functional categories, each addressing a different part of the physical constraint. The taxonomy matters because each category carries different revenue drivers, margin profiles, and risk exposures.

Quanta Services and MasTec sit in the engineering, procurement, and construction layer. Quanta reported a record backlog of $48.5 billion and raised its 2026 revenue guidance to $34.7-$35.2 billion, according to its 30 April 2026 Q1 earnings release. The demand is driven by electric transmission, grid modernisation, and data-centre interconnection. MasTec has reported continued strength in power delivery and communications infrastructure, with data-centre and AI-related demand supporting its backlog.

Vertiv and Eaton, as highlighted by Reuters and Bloomberg, occupy the electrical equipment and thermal management segment, supplying switchgear, power distribution units, and cooling hardware to data-centre operators.

| Company | Category | Primary AI Revenue Driver | Key Recent Data Point |

|---|---|---|---|

| Quanta Services | Contractor / EPC | Grid interconnection, transmission, substations | Record backlog of $48.5 billion |

| MasTec | Contractor / EPC | Power delivery, fibre, site infrastructure | Backlog supported by data-centre demand |

| Bloom Energy | Power generation | On-site fuel cells for grid-constrained data centres | Q1 2026 revenue $751.1 million (130% YoY growth) |

| Caterpillar | Power generation | Prime and backup generation at scale | Power generation sales anticipated to triple in 2026 vs. 2024 |

| GE Vernova | Power generation / Grid equipment | Gas turbines, large-scale baseload generation | Highlighted by Reuters, Bloomberg, S&P Global |

| Generac Holdings | Backup / Distributed power | Industrial standby and microgrid resilience | Rising data-centre backup demand |

The power generation layer

Bloom Energy reported $751.1 million in Q1 2026 revenue on 28 April 2026, reflecting 130% year-over-year growth and 208% product revenue growth. Its fuel cells are positioned as grid-independent, fast-to-deploy power for data centres that cannot wait years for grid interconnection.

The grid bypass mechanics underpinning Bloom Energy’s growth story reflect a broader pattern: hyperscalers facing multi-year interconnection queues are actively funding behind-the-meter generation capacity, creating a structurally separate demand channel from utility-scale grid investment that benefits on-site providers regardless of transmission buildout timelines.

Caterpillar is making a meaningful shift. Morningstar analyst George Maglares has noted that the company’s power generation segment is moving beyond backup into the primary power market, with sales anticipated to triple in 2026 versus 2024. GE Vernova addresses large-scale baseload needs through gas turbines and grid equipment, while Generac captures the standby and microgrid resilience layer.

The distinction between grid-tied generation (GE Vernova, utility-scale gas) and on-site generation (Bloom Energy, Caterpillar) represents two separate investor theses. Grid-tied plays benefit from long permitting and construction cycles; on-site plays benefit from urgency and interconnection queue constraints.

Hyperscaler capex as the demand floor under this entire trade

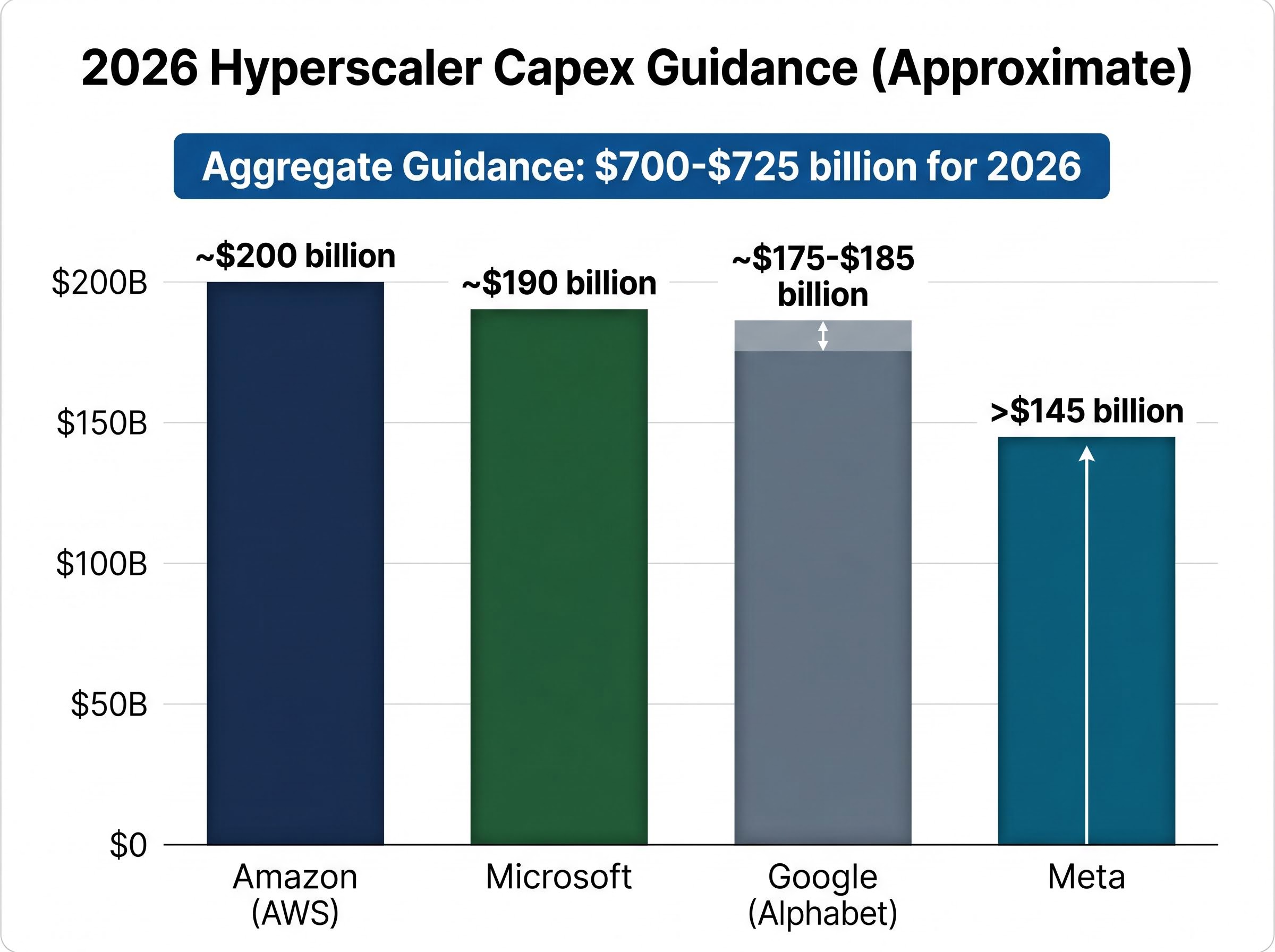

The company-level evidence is compelling, but the structural durability of the thesis rests on the spending commitments of the customers funding the buildout. Microsoft, Amazon, Google, and Meta have all issued upward capex revisions in 2026, with aggregate guidance trajectories pointing toward approximately $700-$725 billion for the year. No confirmed broad slowdown or downward revision to hyperscaler capex has emerged in 2026 reporting.

The hyperscaler capex trajectory for 2026 is tracking toward figures that make the multi-year infrastructure buildout case difficult to dismiss: Amazon, Microsoft, Alphabet, and Meta collectively spent $130 billion in Q1 2026 alone, with full-year combined guidance converging near $725 billion and a $1 trillion annual run rate projected for 2027.

- Microsoft: capex guidance tracking toward approximately $190 billion for 2026

- Amazon (AWS): approximately $200 billion for 2026

- Google (Alphabet): approximately $175-$185 billion for 2026

- Meta: guidance exceeding approximately $145 billion for 2026

(Note: individual per-company figures are approximate and drawn from guidance trajectory estimates that have not been independently verified at these specific levels.)

Private-market valuations corroborate the demand signal. According to PitchBook data, Anthropic’s estimated valuation reached $900 billion as of 15 May 2026, up from $21 billion in July 2024. OpenAI’s estimated valuation stood at approximately $852 billion as of late March 2026, compared to $86 billion in January 2024. The Morningstar PitchBook Global AI Unicorn Index gained 252.36% over three years through 18 May 2026.

Anthropic’s estimated private-market valuation rose from $21 billion in July 2024 to $900 billion by May 2026, a trajectory that reflects the scale of capital still flowing into AI and, by extension, into the physical infrastructure required to support it.

When private-market AI companies are approaching these valuations and hyperscalers are allocating hundreds of billions to infrastructure, the downstream demand for physical buildout companies is not speculative. It is contractually embedded in multi-year spending plans.

The risks that make this trade harder than the return table suggests

The structural case is strong. The risk case is specific.

- Overbuilding and capex pause risk. If hyperscalers slow or pause capital spending, contractor backlogs and power-company pipelines face meaningful revenue exposure. Reuters and Bloomberg have both reported analyst warnings about potential overbuilding risk if hyperscaler capex plateaus in 2026-2027. A multi-year buildout scenario does not eliminate the risk of a digestion period.

- Valuation after re-rating. After 300%+ returns, the easier phase of multiple expansion may be behind these names. Future returns depend more on sustained earnings delivery than on sentiment-driven re-rating. The semiconductor industry’s aggregate market cap grew from approximately $2.2 trillion in May 2023 to approximately $9.4 trillion by April 2026, according to Morningstar, illustrating how rapidly AI-adjacent valuations can stretch.

- Customer concentration. The thesis depends heavily on a small number of hyperscaler customers. Their spending decisions can shift quickly, as evidenced by the software application market cap contraction of 26% from October 2025 to April 2026 (Morningstar), a reminder that AI-adjacent trades can reprice on short notice. The ten largest US Market Index holdings represented more than one-third of total index value as of 20 May 2026.

What to watch as a leading indicator

Rather than predicting which risk materialises first, investors can track a specific set of signals:

- Quarterly hyperscaler capex guidance revisions (any downward revision is the single most important warning signal)

- Quanta Services and MasTec backlog trends (declining sequential backlogs would indicate softening demand)

- FERC interconnection queue data (queue withdrawals or slowdowns signal cooling demand for new capacity)

- Bloom Energy order momentum and guidance trajectory

These function as a practical monitoring checklist rather than a forecast.

The AI infrastructure trade is still broadening, not narrowing

The argument across this analysis points to a single reframing: the AI buildout is a physical construction and power challenge as much as a technology challenge, and the equity returns in industrial and energy infrastructure names reflect genuine earnings leverage rather than sentiment alone.

As AI model training gives way to inference at scale, power demand per query becomes a sustained rather than one-time load, extending the infrastructure buildout timeline beyond the initial construction cycle. Bloom Energy’s six-month return of more than 240% through approximately May 2026 suggests that new capital is still entering these names on recent catalysts, not only in retrospect. The AI unicorn index has more than doubled over the twelve-month period leading to May 2026, indicating private-market capital formation is still accelerating.

Morningstar analyst George Maglares has pointed to Caterpillar management’s confidence in near-term demand visibility as evidence that the power generation cycle is still in its early innings rather than approaching a peak.

The framework for investors is straightforward: track capex commitments, power demand growth, and backlog data rather than chip headlines as the primary signal for this part of the AI trade. The physical stack is where the next chapter of AI-driven returns may be written.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.