Warsh Strips Fed Statement to 130 Words, Drops All Guidance

12 mins ago

As major technology hyperscalers prepare to disclose their April 2026 earnings, a staggering statistic redefines the market environment. Aggregate artificial intelligence infrastructure spending now exceeds the entire United States energy sector’s capital expenditures by a factor of four. This projection from CreditSights signals a definitive shift in Wall Street focus. Analysts are systematically rotating their attention away from software capabilities and focusing directly on the physical infrastructure required to sustain them.

The sheer density of power required for modern computing creates an undeniable bottleneck. Constructing a viable AI energy stocks strategy requires understanding this specific tension. Investors need a clear roadmap connecting massive technology spending to the secondary beneficiaries poised to capture this unprecedented capital wave. The companies capable of providing immediate, scalable electricity outside the traditional utility framework are capturing premium valuations.

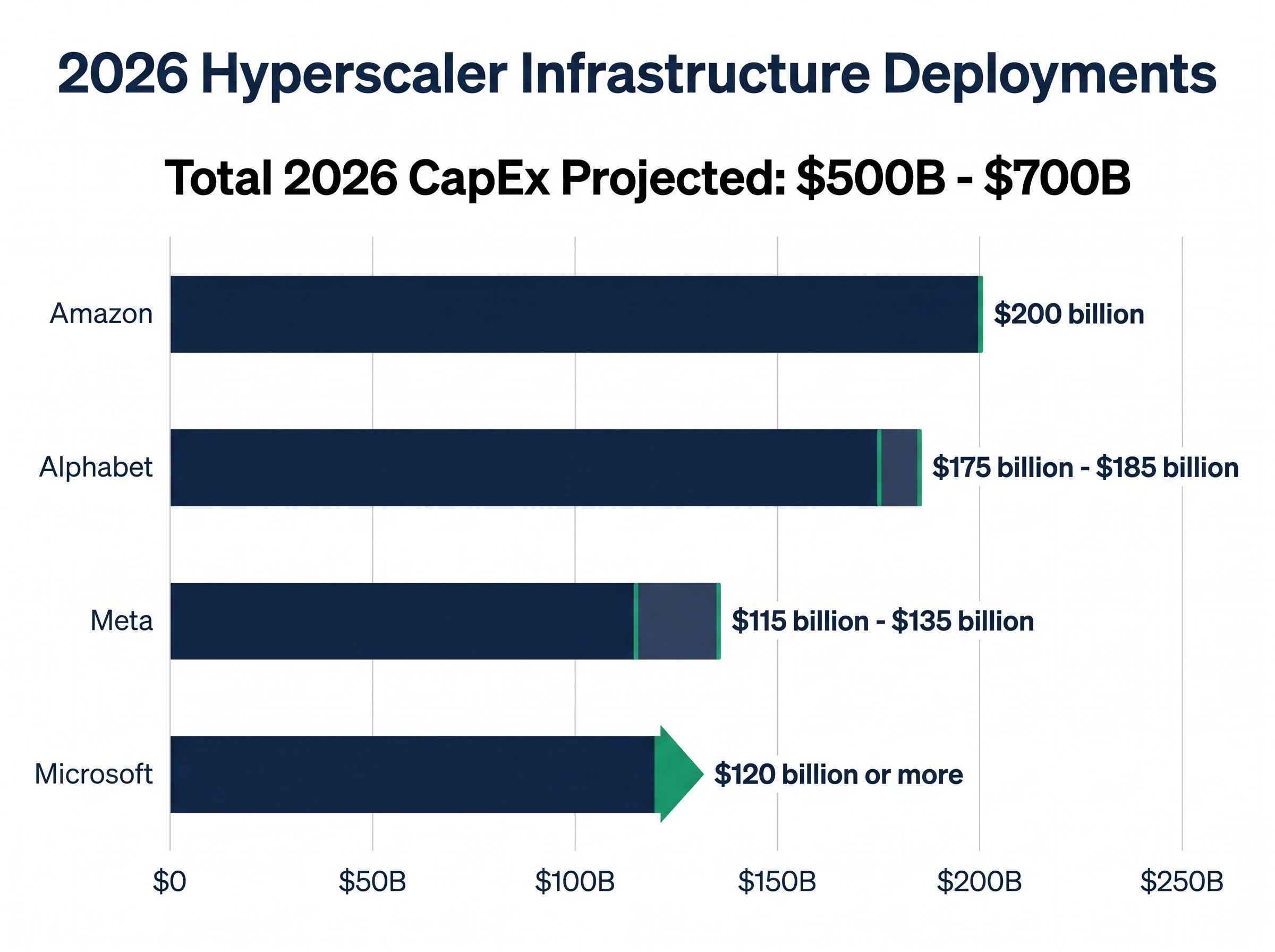

Wall Street aggregate projections place 2026 artificial intelligence capital expenditures between $500 billion and $700 billion. This spending surge represents necessary capacity building rather than speculative investment. Major hyperscalers recognise that securing immediate physical infrastructure is a prerequisite for maintaining future market share.

This influx of capital is actively forcing analysts to recalibrate S&P 500 valuation models as traditional metrics fail to account for the immediate revenue expectations placed on new computing facilities.

Understanding the velocity of this capital deployment helps investors recognise a critical market dynamic. The infrastructure buildout is fully funded and structurally inevitable, creating a secure foundation for downstream service providers. The Futurum Group outlines exactly where this capital is deploying across the primary ecosystem:

Amazon: $200 billion, predominantly directed toward data centre capacity expansion Alphabet: Projected allocations between $175 billion and $185 billion Meta: Scaling aggressively to between $115 billion and $135 billion Microsoft: Base commitments of $120 billion or more for facility development

The financial tension behind these figures is immediate and severe. A Campaign US analysis warns that hyperscaler free cash flow could drop by as much as 90%. This compression occurs because aggressive infrastructure deployment dramatically outpaces near-term revenue generation.

Historical Spending Context According to Goldman Sachs, historical consensus consistently underestimates hyperscaler spending. Current data points to recent upward trends revising expectations toward the $670 billion threshold.

Companies are prioritising physical dominance over immediate margin preservation.

Data centres require base-load power to function effectively. This concept refers to the minimum level of uninterrupted, high-density electricity needed to maintain continuous operations without fluctuation. Intermittent renewable sources, such as wind or solar, cannot provide this baseline reliability without extensive and costly battery storage support.

Aging United States electrical grid infrastructure struggles to accommodate massive load requests. These legacy systems were designed for predictable commercial growth, not the exponential spikes associated with modern computing facilities. Regional utility approval processes often stretch across multiple years for new grid connections. This failure of traditional timelines operates as the primary catalyst forcing technology companies to seek independent generation solutions.

The official NERC long-term reliability assessment forecasts electricity demand growing by 224 gigawatts over the next decade, a surge that threatens to overwhelm existing regional capacities.

Industry projections indicate artificial intelligence will drive a 50% or greater increase in overall data centre energy demand by 2027. This timeline severely misaligns with public utility upgrade schedules.

High-density computing clusters require dense power profiles that standard commercial grid lines cannot safely sustain. Long-term forecasts show broader base-load power demand growing between 50% and 165% by 2030.

This structural deficit explains the sudden valuation premiums applied to alternative power providers. Off-grid generation operates as a mandatory operational requirement for the technology sector rather than a discretionary environmental initiative. Facilities must secure independent power to guarantee uptime.

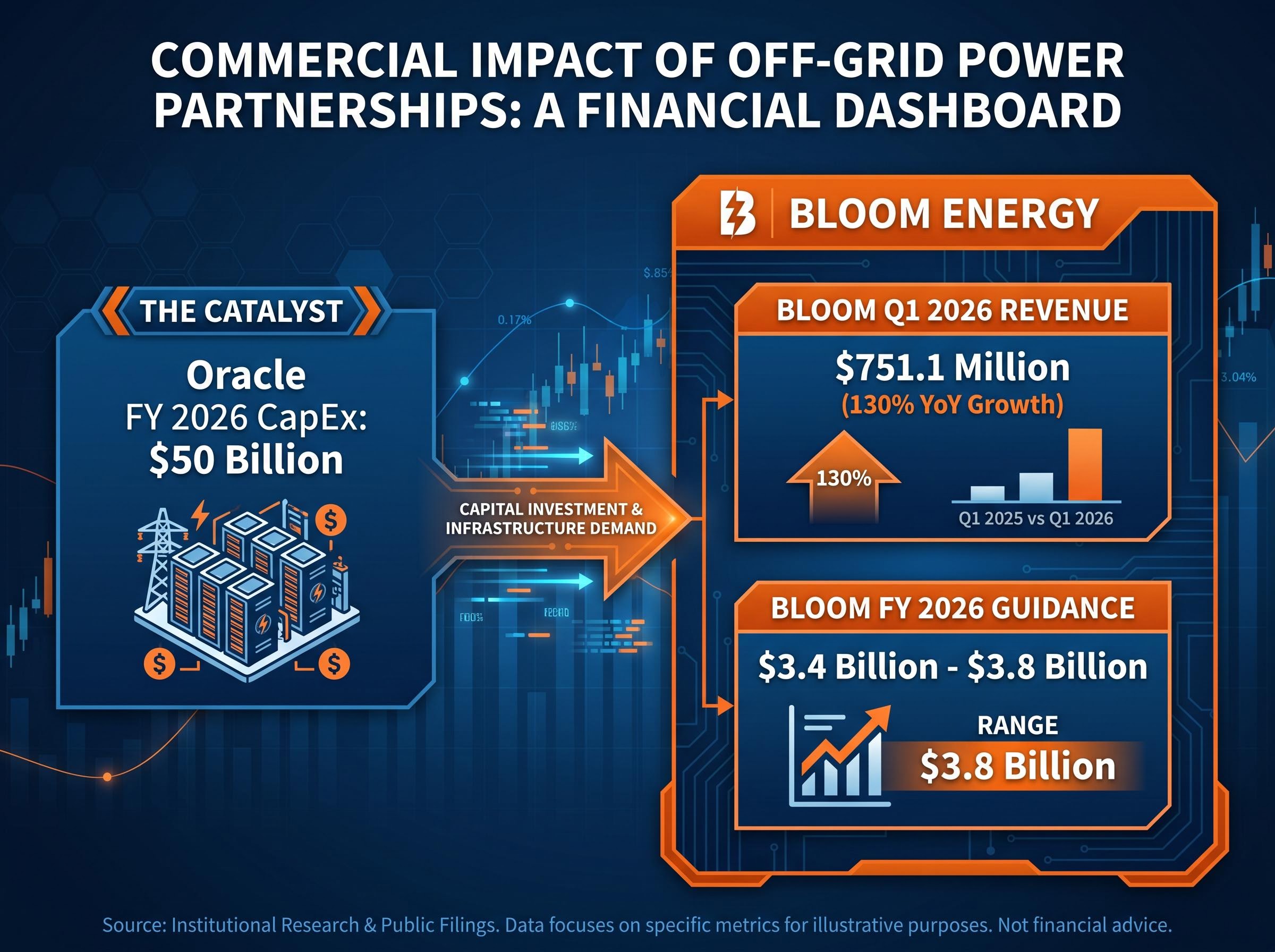

The strategic partnership between Bloom Energy and Oracle provides the defining case study for off-grid power deployment. Oracle recently committed to a $50 billion fiscal year 2026 capital expenditure target focused heavily on cloud computing expansion. To bypass regional grid constraints and activate new data centres on schedule, Oracle utilises Bloom Energy’s independent generation solutions.

This urgency to circumvent power limitations is directly tied to broader hardware supply chain bottlenecks; deploying billions in specialized compute infrastructure requires absolute certainty that facilities can power them up immediately upon delivery.

This direct pipeline to hyperscaler capital is generating verifiable financial expansion. Bloom Energy reported record first-quarter 2026 revenue of $751.1 million.

Unprecedented Growth Pace Bloom Energy’s $751.1 million first-quarter performance represents a 130% year-over-year surge, driven directly by the immediate need for artificial intelligence infrastructure power.

Following this quarterly result, Bloom Energy released an upwardly revised full-year 2026 guidance between $3.4 billion and $3.8 billion. The market responded immediately, driving an after-hours gain for Bloom Energy stock. This relationship functions as a repeatable, highly lucrative blueprint.

Other technology giants are actively replicating this model to secure their own operational independence. The transition to alternative power providers is already generating massive revenue expansion for companies capable of deploying immediate base-load solutions. It proves the commercial thesis that grid bypass strategies are fully funded.

The broader ecosystem of companies resolving the hyperscaler capacity deficit offers distinct commercial investment profiles. Solutions range from immediate natural gas bridges to long-term microreactor strategies. Brookfield Renewable Partners is gaining significant market momentum through fuel cell deployment collaborations. These partnerships are specifically designed to serve high-density computing facilities outside traditional utility jurisdictions.

New Fortress Energy utilises liquefied natural gas to bridge immediate and medium-term capacity needs. This approach allows operators to power new facilities immediately while they wait for permanent public grid updates. Traditional natural gas operators, including Cheniere Energy and EQT, capture secondary benefits from this sector rotation. They supply the underlying commodity feeding the broader base-load growth projected over the next decade.

For clean, permanent off-grid solutions, Nano Nuclear Energy targets the upcoming demand for portable microreactors. This technology caters specifically to the growing need for uninterrupted, zero-emission base-load generation.

| Company Name | Technology Segment | Deployment Timeline | Primary Catalyst |

|---|---|---|---|

| Bloom Energy | Fuel Cell Generation | Immediate | Direct hyperscaler partnerships |

| New Fortress Energy | Liquefied Natural Gas | Immediate to Medium-term | Bridging grid connection delays |

| Brookfield Renewable Partners | Alternative Energy / Fuel Cells | Medium-term | Infrastructure deployment collaborations |

| Nano Nuclear Energy | Microreactors | Long-term | Clean off-grid base-load demand |

This breakdown helps investors distinguish between temporary bridge providers and permanent structural solutions. Evaluating these equities requires identifying which operators hold immediate deployment capabilities versus those relying on long-term development cycles.

Investors exploring the downstream beneficiaries of this transition will find our deep-dive into AI hardware monetization useful, as it outlines how semiconductor suppliers are capturing immediate, guaranteed revenue streams while alternative energy providers race to power the newly delivered chips.

The ultimate goal for hyperscalers extends far beyond temporary capacity fixes. Technology giants require permanent insulation from regional grid vulnerability and public utility delays. The convergence of technology capital and alternative energy creates an entirely new class of utility-scale infrastructure companies.

CreditSights estimates that $450 billion of the aggregate sector capital expenditure is explicitly dedicated to artificial intelligence infrastructure this year. This magnitude of private funding accelerates a radical, long-term shift toward behind-the-meter generation models. The transition from public utilities to private power independence follows a distinct, privately funded progression.

Further CreditSights hyperscaler capital expenditure estimates reveal that approximately 75% of this spending targets physical AI infrastructure directly, confirming the overwhelming priority tech giants place on hardware acquisition.

Evaluating future technology earnings calls requires listening specifically for these off-grid power acquisition strategies. These announcements serve as leading indicators of operational resilience. Financial projections regarding energy transition timelines are subject to market conditions and shifting regulatory approval frameworks.

Hyperscaler capital expenditures currently operate as the most powerful force influencing the industrial economy. Solving the physical power bottleneck remains the primary constraint on digital growth across the technology sector. This dynamic guarantees that capital will continue flowing toward any infrastructure provider capable of delivering reliable base-load generation on commercial timelines.

This multi-year investment cycle provides a durable thesis for tracking secondary market beneficiaries. As technology companies bypass legacy grids, independent power producers capture unprecedented revenue streams.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.

AI energy stocks refer to companies providing power generation and infrastructure solutions specifically for the high-density electricity demands of artificial intelligence data centers, often bypassing traditional utility grids.

Major technology hyperscalers are investing hundreds of billions in AI energy infrastructure to secure immediate physical capacity, overcome the limitations of aging power grids, and ensure uninterrupted, high-density electricity for their data centers.

Investors should look for companies with immediate deployment capabilities, proven partnerships with hyperscalers, and solutions that address base-load power requirements for data centers, distinguishing between temporary and permanent solutions.

The "bypass blueprint" describes the strategy where technology giants, such as Oracle, partner with alternative power providers like Bloom Energy to deploy independent, off-grid generation solutions, circumventing traditional utility constraints and accelerating data center activation.

Base-load power is the minimum level of uninterrupted, high-density electricity required for continuous operation. It is critical for AI data centers to maintain uptime and performance, which intermittent renewable sources alone cannot reliably provide without extensive storage.