According to market data, four companies currently control approximately 18.3% of the broader S&P 500 equity index. Microsoft, Meta, Amazon, and Alphabet are preparing to release their first-quarter earnings disclosures between April 29 and April 30, 2026. Their anticipated capital expenditure signals a transition phase where infinite corporate capital meets the finite physical resources of the United States power grid.

Sustained AI infrastructure demand has created an unprecedented financial velocity, forcing markets to recalibrate baseline expectations for corporate spending. Total 2026 artificial intelligence capital expenditures across these major technology firms are estimated to reach between $630 billion and $690 billion.

This massive financial outlay explicitly connects three critical market forces for investors. Technology earnings are currently driving alternative energy sector breakouts, yet underlying software monetisation friction threatens to complicate the prevailing market narrative. Understanding this intersection helps separate routine corporate procurement from generation-defining physical infrastructure investments.

Hyperscale Capital Allocation in the First Quarter

The sheer financial velocity of the current market moment is visible in the forward guidance emerging from early 2026 technology disclosures. Major ecosystem players are signalling unyielding corporate confidence in future computing requirements, despite broader macroeconomic uncertainties. Analysts anticipate Meta will report first-quarter 2026 year-over-year revenue growth of 31.1% to 31.3%.

This influx of capital has triggered a historic semiconductor supercycle, with major hyperscalers projected to deploy up to $700 billion across physical hardware and data centre construction.

This revenue expansion is being directly channelled into hardware procurement. Meta has set its 2026 capital expenditure targets between $115 billion and $135 billion. Microsoft is demonstrating a similar trajectory, with broader 2026 total revenue estimates projected to land between $324 billion and $327 billion.

These figures establish the baseline metrics investors need to benchmark upcoming earnings reports.

| Company | Key 2026 Revenue Metric | Estimated 2026 Capital Expenditure |

|---|---|---|

| Meta | 31.1% to 31.3% (Q1 YoY Growth) | $115 billion to $135 billion |

| Microsoft | $324 billion to $327 billion (Total Annual Estimate) | Included in broader $630 billion to $690 billion aggregate |

This capital allocation represents a structural shift in how hyperscalers view their operational priorities. The commitment to massive infrastructure spending operates on the assumption that computing power will be the primary currency of the next decade. However, this assumption relies on physical realities that corporate balance sheets cannot easily manipulate.

These financial commitments demonstrate that technology leaders view hardware accumulation as an absolute requirement rather than an optional growth lever. Amazon is similarly anticipated to report strong ongoing demand for its cloud computing infrastructure. These staggering figures represent a defining moment in market history, setting up a direct collision with the physical limitations of the natural world.

When big ASX news breaks, our subscribers know first

Why Artificial Intelligence is Breaking the Traditional Power Grid

Corporate capital alone cannot resolve the computing bottlenecks emerging across the United States. A fundamental difference in power density separates standard enterprise data centres from specialised artificial intelligence workloads. Conventional facilities require predictable, moderate electricity flows to maintain standard server racks.

Advanced computing chips draw significantly more power and generate intense heat, requiring sophisticated cooling mechanisms and massive continuous energy supplies. The conventional grid infrastructure in the United States is fundamentally unequipped to handle this rapid, concentrated surge in demand. Regional utility operators are already facing multi-year backlogs for new grid interconnections.

The recently published DOE data center energy report projects massive escalations in baseline electricity consumption over the coming decade, validating concerns that current power generation capacity will struggle to support sustained artificial intelligence deployment.

This physical limitation dictates the pace of software development and effectively positions utility and energy stocks as proxy technology investments. To bypass these constraints, data centre operators are exploring a spectrum of alternative power solutions.

Hybrid Models and Fuel Cells: These immediate bridging technologies integrate hydrogen and dedicated on-site power generation to ensure continuous operation without grid reliance. Standard Renewables: Wind and solar power offer carbon reduction benefits but face severe intermittency constraints, rendering them insufficient for base-load requirements on their own. * Nuclear Small Modular Reactors (SMRs): These systems hold the theoretical promise of reliable, low-carbon power, though practical construction delays and regulatory hurdles limit their immediate viability.

The necessity of off-grid energy transitions is reshaping corporate procurement strategies. Isolated operational models are no longer speculative experiments; they are absolute requirements for scaling processing capacity. Investors are consequently reweighting their portfolios to capture the capital overflowing from technology sectors into alternative energy providers.

The Bloom Energy Blueprint and Off-Grid Acceleration

The physical constraints of the power grid are already translating into actionable corporate results for alternative energy providers. Bloom Energy recently reported first-quarter 2026 revenue of $751.1 million, representing a 130.4% year-over-year increase. This financial performance stands as the clearest market validation of the off-grid power transition thesis.

The company has subsequently upwardly modified its full-year 2026 revenue projections.

Market Validation Signal Bloom Energy experienced a massive 208% surge in product revenue during the first quarter, signalling a definitive shift in how hyperscale data centres are procuring their base-load power.

This surging product revenue is not occurring in a vacuum. It reflects a broader necessity for reliable, low-carbon, on-site power generation that bypasses conventional utility limitations. The market responded immediately to these operational shifts, with Bloom Energy experiencing an after-hours share value escalation following a major strategic announcement.

The Oracle Collaboration Mechanics

The catalyst for this share price movement was Bloom Energy’s newly announced enterprise partnership with Oracle. The strategic synergy involves deploying fuel cell servers directly to specialised artificial intelligence data centres. This explicit replacement of traditional utility power allows operators to completely bypass regional grid interconnect queues.

By generating power on-site, the collaboration ensures operational continuity while reducing carbon emissions and water usage. The mechanics of this partnership illustrate exactly how alternative energy providers are capturing the massive capital expenditures detailed in hyperscale earnings guidance. When standard utilities cannot meet the timeline or capacity requirements of technology giants, off-grid solutions become the mandatory alternative.

Securing this continuous power is essential as enterprise hardware prices for high-capacity models continue to surge, with major suppliers already reporting production constraints through the remainder of the year.

Monetisation Friction and the OpenAI Reality Check

Despite the astronomical hardware and energy expenditures flowing through the market, a concerning disconnect is emerging between infrastructure investment and end-user monetisation. The current pace of consumer software adoption is beginning to lag behind the financial velocity of data centre expansion. This fundamental friction point is introducing necessary caution into the broader investment supercycle.

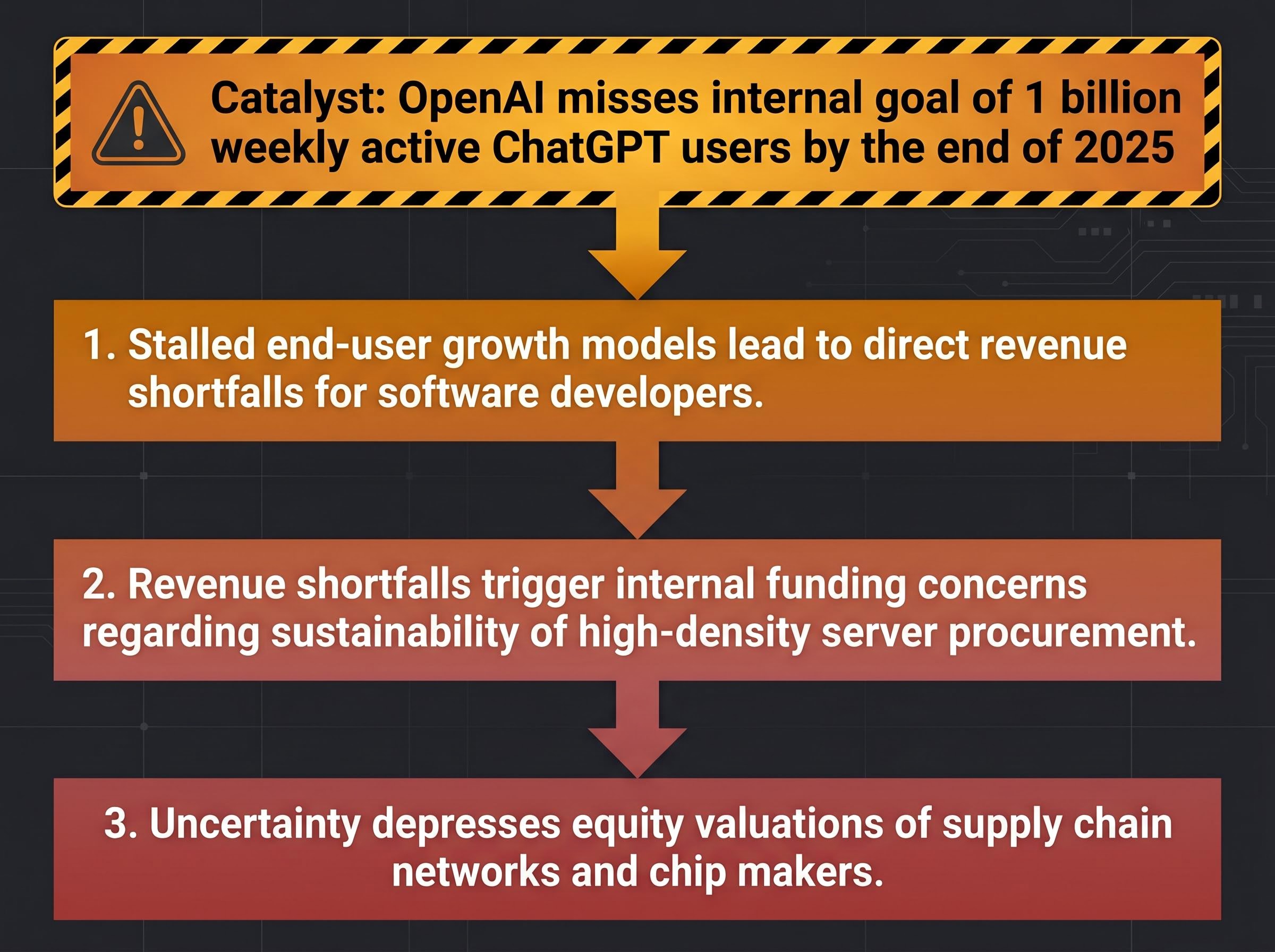

OpenAI has reportedly failed to reach its internal goal of 1 billion weekly active ChatGPT users by the end of 2025. This shortfall has triggered internal leadership concerns regarding how to sustainably fund massive, ongoing infrastructure expansions. The combination of stalled user adoption and unyielding compute costs creates a precarious revenue dynamic for the broader ecosystem.

These internal targets missed by major players are placing downward pressure on infrastructure partners. The negative investor sentiment is rippling through the equity markets, depressing valuations across the semiconductor and database supply chains.

The cascading market effects follow a distinct sequence:

- Stalled end-user growth models lead to direct revenue shortfalls for software developers.

- These revenue shortfalls trigger internal funding concerns regarding the sustainability of high-density server procurement.

- The resulting uncertainty depresses the equity valuations of supply chain networks and chip makers reliant on those ongoing orders.

This reality check protects investors from one-sided market exuberance. While the physical rollout of off-grid energy and server racks continues rapidly, the underlying software must eventually generate sufficient cash flow to justify the capital outlay. If monetisation continues to stall, the current pace of corporate spending will face severe analytical scrutiny in the coming quarters.

For readers analyzing the durability of this investment wave, our full explainer on tech hardware valuations breaks down how physical supply chain bottlenecks and lagging software profitability could compress equity premiums across the broader S&P 500.

Navigating the Next Phase of the Compute Supercycle

The remainder of 2026 will force the market to reconcile hyperscale spending ambitions with physical energy limitations and software monetisation hurdles. The upcoming earnings calls from Microsoft, Meta, Amazon, and Alphabet will definitively prove whether corporate leaders intend to maintain their aggressive capital expenditure trajectories despite slowing user adoption rates.

Investors must carefully balance their exposure across this evolving sector. Technology infrastructure holdings remain foundational, but the physical bottlenecks make alternative energy solutions an equally necessary component of a modern portfolio. The companies capable of delivering immediate, grid-free power will likely continue capturing the overflow of technology capital.

However, the disconnect identified at the software level demands vigilant monitoring. If the gap between infrastructure costs and software revenue widens, the supercycle could experience a painful recalibration. Market participants should look for explicit management commentary on power procurement strategies and active user growth metrics to navigate the months ahead.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.