How Wesfarmers’ AI Strategy Is Built to Compound Returns

5 hrs ago

Morgan Stanley named Nokia a top equity pick on 22 May 2026, setting a Helsinki price target of €14 and a New York Stock Exchange target of $16.50, implying roughly 11% upside from the stock’s current Helsinki trading level of approximately €12.56. The upgrade arrives after a 150% gain over the prior twelve months, a run that has transformed Nokia’s equity story from legacy telecom turnaround into an active debate about how to value a company repositioning itself at the centre of AI infrastructure spending. What follows is an assessment of the Morgan Stanley thesis, the structural argument underpinning it, the specific catalysts that could prove or disprove it, and the bear case that commercial-intent readers need before forming a view on the Nokia stock forecast.

The call came from Terence Tsui and his team at Morgan Stanley, who raised Nokia’s Helsinki price target from €11 to €14 and the NYSE ADR target from $13 to $16.50. The “top pick” designation carries weight beyond the target itself; it signals that among the full coverage universe available to the team, Nokia is the single name they want clients allocated to right now.

The gap between the current price (approximately €11.73 in Helsinki) and the €14 target is modest in isolation. What makes the call significant is the framing: Morgan Stanley is not chasing momentum from the prior year’s rally. The thesis rests on a valuation re-rating driven by Nokia’s structural shift toward AI data centre connectivity, a business mix change that the team believes the market has not yet fully priced.

That conviction, however, is far from unanimous across the sell side.

Goldman Sachs upgraded Nokia to Neutral from Sell in March 2026, setting a price target of €8.00. That target sits 36% below where the stock trades today, making Goldman’s Neutral the effective floor of institutional scepticism. Deutsche Bank holds a Buy rating, with multiple target increases through 2026 confirmed directionally, though specific post-Q1 2026 targets remain behind paywalls.

The table below illustrates the spread.

| Broker | Rating | Price Target (Helsinki) |

|---|---|---|

| Morgan Stanley | Overweight (Top Pick) | €14.00 |

| Deutsche Bank | Buy | Multiple hikes in 2026 (specific target unconfirmed) |

| Goldman Sachs | Neutral | €8.00 |

Positions from J.P. Morgan, UBS, Barclays, Citi, and BofA are not publicly confirmed with specific 2026 targets. The distance between Morgan Stanley’s €14 and Goldman’s €8 represents one of the widest analyst spreads on a major European technology name, and that disagreement is itself the starting point for any informed assessment.

For most of its modern history, Nokia built the mobile network equipment that telecom operators used to deliver wireless connectivity. Base stations, radio access networks, 5G rollouts. That business still exists, but the growth engine Morgan Stanley is underwriting sits in a different part of the company entirely.

Nokia’s optical and IP networks segment builds the physical infrastructure that connects data centres to one another and to the wider internet. In practical terms, this means fibre-optic transport systems that move enormous volumes of data at high speed between facilities, IP routing hardware that directs that traffic efficiently, and the network management software that orchestrates both. As AI workloads scale, the volume of data moving between GPU clusters, training environments, and inference endpoints scales with it, and every byte of that traffic needs physical connectivity infrastructure.

The demand environment Nokia is attempting to capture is being shaped by hyperscaler AI capital expenditure that reached $130 billion in Q1 2026 alone across Amazon, Microsoft, Alphabet, and Meta, with full-year 2026 combined projections sitting at $725 billion and a trajectory toward $1 trillion annually by 2027.

The core product categories relevant to the AI data centre thesis include:

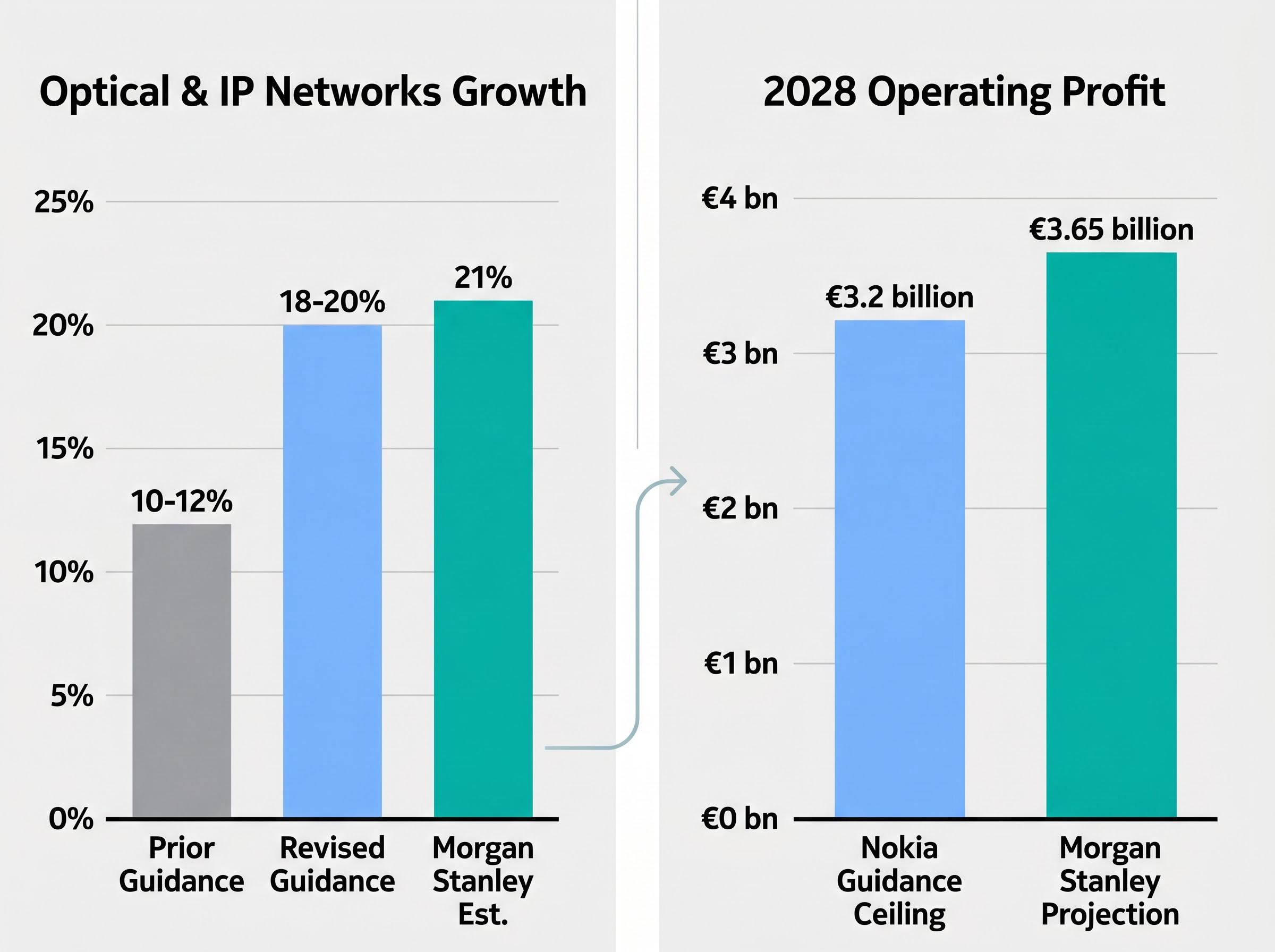

Nokia’s 2025 AI and cloud revenues reached €1.1 billion, a figure Morgan Stanley characterises as below peer levels. The optical and IP networks segment saw its revenue growth guidance revised upward to 18-20%, from prior guidance of 10-12%. Morgan Stanley’s own estimate for the segment sits at 21% growth, above even the company’s revised ceiling.

Morgan Stanley characterises Nokia as possessing scarcity value as a Western-origin connectivity infrastructure supplier, a differentiator at a time when geopolitical considerations increasingly influence procurement decisions for data centre infrastructure.

Nokia’s SEC Form 6-K for Q2 and Half Year 2025 noted strong demand in Optical Networks and IP Networks from data centre and cloud customers, consistent with the broader thesis that AI compute build-outs are pulling optical networking demand higher.

The instinct when hearing that Nokia generated €1.1 billion in AI and cloud revenue in 2025 is to compare that figure to the tens of billions flowing through hyperscaler capital expenditure budgets and conclude that Nokia’s share is small. Morgan Stanley’s argument runs in the opposite direction.

When a company’s AI-related revenue is a small fraction of its total, each new contract moves the growth rate more dramatically than it would for a competitor already operating at high penetration. A $200 million hyperscaler win for a company generating €1.1 billion in AI revenue adds nearly 18% to the segment. The same contract for a peer already at €5 billion adds 4%. The proportional impact compounds across multiple wins.

Morgan Stanley frames the low base as accumulated upside optionality rather than competitive underperformance. The three structural reasons behind this view:

Cisco’s AI networking revenue trajectory, where AI orders nearly doubled to a $9 billion full-year forecast and data-centre switching grew more than 40% year on year in Q3 FY2026, provides the closest publicly available benchmark for what hyperscaler-driven optical and IP networking demand looks like when it reaches higher penetration levels than Nokia currently holds.

Morgan Stanley’s 2028 operating profit projection for Nokia stands at €3.65 billion, above the company’s own guidance ceiling of €3.2 billion. Nokia’s Q2 2025 filings reference growing orders from “large cloud and content providers” for optical transport, though the company does not name specific hyperscaler customers.

No new named hyperscaler optical or AI infrastructure contract has been publicly confirmed since January 2025. The upside case is structurally grounded but remains speculative until contract announcements provide confirmation.

The structural thesis is one thing. The catalysts that could force the market to reprice the stock in the near term are something else entirely, and Morgan Stanley has flagged three.

Ciena’s fiscal Q2 2026 earnings, expected around 4 June 2026, function as an optical sector read-through. Ciena operates in the same optical networking demand environment, and its revenue trajectory and forward guidance offer the closest publicly available signal on whether hyperscaler optical spending is accelerating, plateauing, or decelerating. A strong Ciena quarter would provide data that supports Nokia’s segment growth assumptions.

The broader sector move on 14 May 2026, when AI infrastructure stocks including Arista, Super Micro, Marvell, and Broadcom surged in sympathy with Cisco’s AI order announcement, illustrates how sentiment across optical and networking names can shift rapidly when hyperscaler spending data arrives ahead of expectations.

Potential hyperscaler partnership announcements represent the single most powerful catalyst. Nokia’s filings confirm growing webscale demand without naming customers. A publicly confirmed contract with a named hyperscaler would convert the speculative upside case into a quantifiable revenue event.

Euro Stoxx 50 re-inclusion would trigger a mechanical buying dynamic. Nokia was removed from the index in September 2025. The next periodic review cycle falls in September 2026. If Nokia’s market capitalisation qualifies it for re-inclusion, passive funds tracking the index would be required to purchase shares regardless of their fundamental view. No official STOXX forward guidance on Nokia’s re-inclusion prospects exists.

| Catalyst | Expected Timing | Confirmation Status |

|---|---|---|

| Ciena fiscal Q2 2026 earnings | 4 June 2026 (expected) | Scheduled |

| Named hyperscaler contract win | No specific date | Unconfirmed; no post-January 2025 announcement |

| Euro Stoxx 50 re-inclusion | September 2026 review cycle | Speculative; no STOXX forward guidance |

The distinction matters: Ciena earnings are a scheduled, observable event. Hyperscaler wins and index inclusion are conditional, and treating them as equivalent in probability would overstate the near-term case.

Nokia’s Helsinki-listed shares have risen approximately 150% over the past twelve months and more than 100% year-to-date as of 22 May 2026. For investors encountering the AI infrastructure thesis now, the arithmetic demands scrutiny.

Morgan Stanley’s €14 target implies roughly 11% upside from current levels. Goldman Sachs’s €8.00 target implies approximately 36% downside. That spread, on the same stock at the same moment, captures the full width of institutional disagreement about what Nokia’s transformation is worth today.

Goldman’s more conservative view reflects scepticism about how quickly Nokia can close the AI revenue gap with peers already further along the hyperscaler penetration curve. At €8.00, the Neutral rating effectively prices Nokia’s optical networking growth as incremental rather than inflectionary.

European equity structural headwinds, including sluggish eurozone growth, elevated energy costs, and an ECB holding rates at 2.00% with no near-term stimulus catalyst, have created a context where Nokia’s Helsinki listing faces sector-agnostic multiple compression pressure that would not apply to a US-listed pure-play optical networking competitor.

The bear case rests on several specific risk factors investors should monitor:

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The Morgan Stanley upgrade is a precisely articulated bet on a specific sequence of events. For it to pay off, four conditions would need to hold:

Each of these conditions is plausible within the current AI infrastructure spending cycle. None is guaranteed.

Nokia’s positioning as a Western connectivity infrastructure supplier in a capital expenditure-intensive AI build-out cycle provides the structural backdrop. Stock performance, however, will ultimately follow contract wins and earnings delivery rather than positioning alone.

The Morgan Stanley upgrade at €14 defines the bull case with analytical precision. The Goldman Sachs Neutral at €8.00 defines the floor of informed scepticism. The next six months of catalysts, Ciena’s read-through in early June, any hyperscaler announcements as they emerge, and the Euro Stoxx 50 review in September, will narrow the range between them. For investors evaluating AI infrastructure exposure through connectivity and networking rather than compute or energy, Nokia presents a rare Western-listed option at a price that already reflects much of the structural re-rating story. Whether the remaining upside justifies the entry depends on which side of the analyst divide the incoming data supports.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

—

Morgan Stanley set a Helsinki price target of €14 and a NYSE ADR target of $16.50 on 22 May 2026, designating Nokia as a top equity pick and implying roughly 11% upside from the stock's trading level of approximately €12.56 at the time of the call.

Morgan Stanley's upgrade is driven by Nokia's structural shift toward AI data centre connectivity, specifically its optical and IP networks segment, which the team believes the market has not yet fully priced despite revised growth guidance of 18-20% and a low base that amplifies the proportional impact of each new hyperscaler contract win.

Three catalysts Morgan Stanley highlighted are Ciena's fiscal Q2 2026 earnings (expected around 4 June 2026) as an optical sector read-through, a potential named hyperscaler partnership announcement, and Nokia's possible re-inclusion in the Euro Stoxx 50 during the September 2026 review cycle, which would trigger mechanical buying from passive funds.

The bear case includes no confirmed hyperscaler contracts since January 2025, Goldman Sachs holding a Neutral rating with an €8.00 target implying 36% downside, Morgan Stanley's 2028 operating profit projection of €3.65 billion exceeding Nokia's own guidance ceiling of €3.2 billion, and the risk that much of the structural re-rating is already reflected in the share price after a 150% gain.

Nokia generated €1.1 billion in AI and cloud revenues in 2025, which Morgan Stanley characterises as below peer levels; however, the firm frames this low base as accumulated upside optionality, since each new hyperscaler contract win has a proportionally larger impact on Nokia's growth rate than it would for a competitor already at higher penetration levels.