WTI Jumps 1.6% as Iran Strikes Shatter Hormuz Deal Hopes

1 hr ago

Cisco shares surged 16.5% on 14 May 2026, delivering one of the largest single-session gains in the company’s recent history. The catalyst was not a product launch or an acquisition. It was a quarterly earnings report that paired a workforce reduction of nearly 4,000 jobs with a near-doubling of the company’s full-year artificial intelligence order forecast. That pairing captures a dynamic reshaping how investors read enterprise technology stocks: headcount cuts no longer signal distress when AI infrastructure demand is accelerating hard enough to overwhelm any operational friction. What follows explains what Cisco’s Q3 FY2026 results reveal about hyperscale capital expenditure flowing beyond chips into networking and switching, what the second restructuring round in three months signals about strategic direction, and what both developments mean for evaluating enterprise tech stocks in the current environment.

The stock move is the story’s clearest signal. Cisco (CSCO) traded in an intraday range of $99.30 to $101.99 on 14 May, gaining approximately 16% in a single session and ranking among the top percentage gainers across U.S. markets. A company announcing thousands of job cuts does not typically produce that reaction. The order book does.

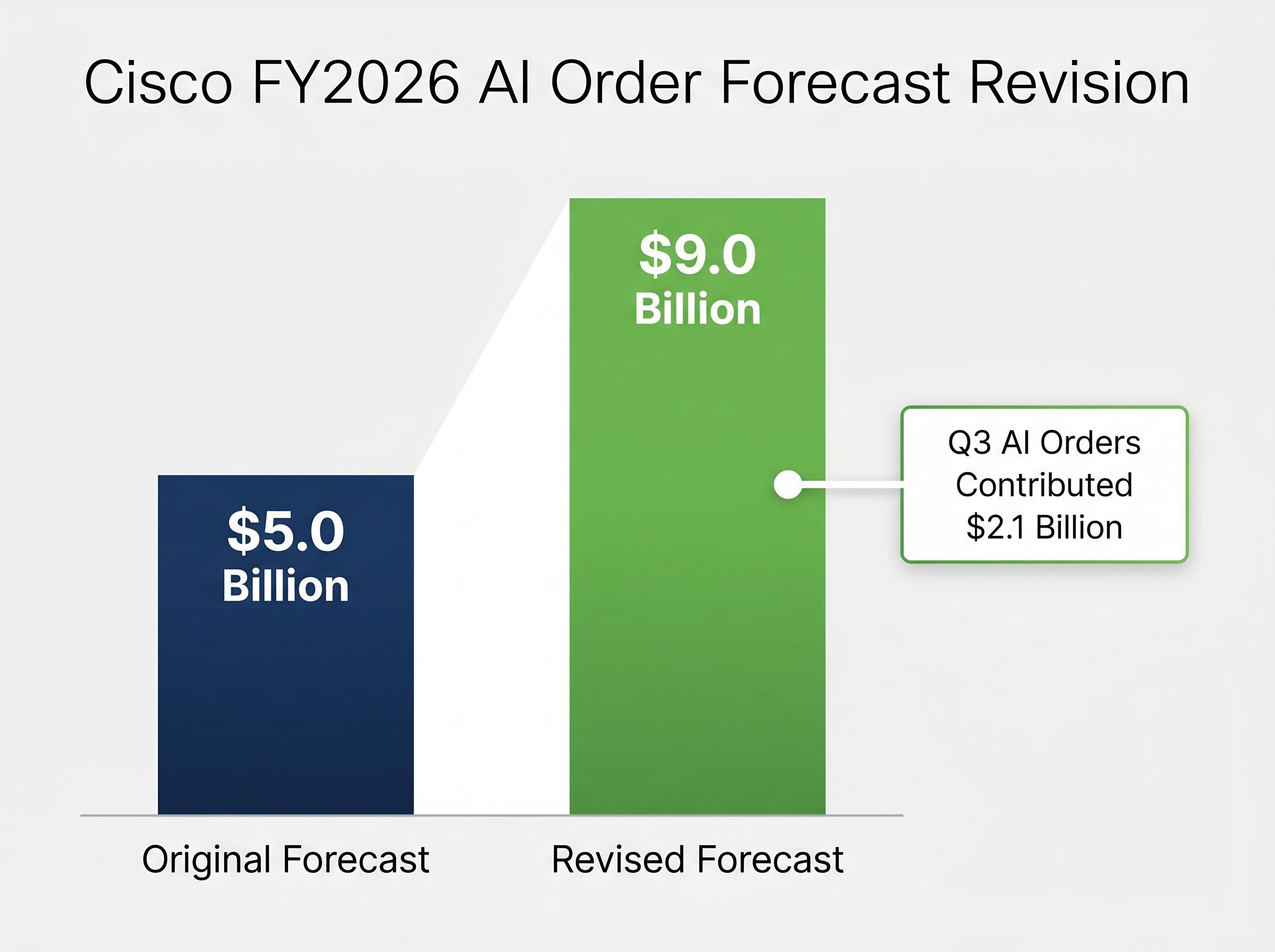

Cisco raised its full-year FY2026 AI order expectation from approximately $5.0 billion to $9.0 billion, nearly doubling the forecast mid-year. Q3 alone contributed $2.1 billion in AI orders, a single-quarter figure large enough to force the full-year revision.

Full-year AI order forecast revised: from approximately $5.0 billion to $9.0 billion, a near-doubling driven by Q3 hyperscaler demand.

The Q3 financial results provided the foundation:

Analysts responded to the order acceleration, not the restructuring headline. The distinction matters: the stock gained because verified customer demand nearly doubled the company’s own mid-year projection, not because cost cuts promised margin improvement.

The AI investment wave spent its first phase concentrated at the chip layer. Companies bought GPUs. They bought compute. Cisco’s Q3 results show that phase has matured, and capital expenditure is now flowing into the infrastructure those chips depend on: networking, switching, optics, and security.

The AI infrastructure investment cycle has concentrated roughly 75% of hyperscaler capital, approximately $450 billion in 2026, in physical hardware and data centre construction rather than software, which is precisely why vendors supplying the physical layer are generating order growth that outpaces software peers by a wide margin.

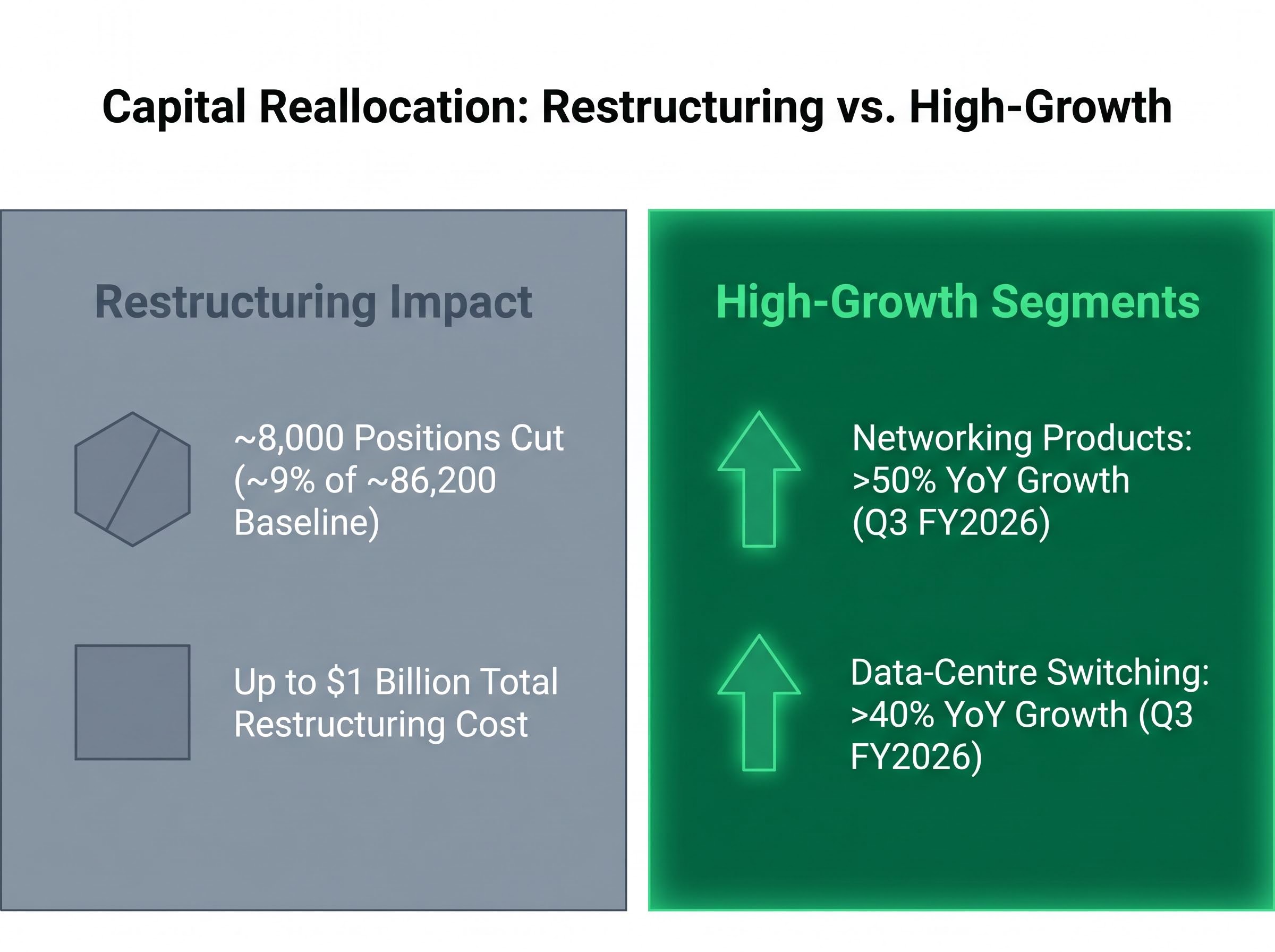

The product-level growth figures make the shift concrete. Cisco’s networking products grew more than 50% year on year in Q3 FY2026. Data-centre switching grew more than 40% over the same period. These are not software subscription metrics. They are physical infrastructure orders from hyperscalers building out AI-capable data centres at scale.

The mechanism is straightforward. A data centre full of GPUs requires networking infrastructure to move data between those processors. As hyperscaler capital expenditure on AI compute has scaled, the downstream demand for the networking layer has followed. Cisco occupies that layer, and Q3 is the quarter where the spending arrived in force.

The demand is not confined to hyperscalers. CEO Chuck Robbins identified an emerging enterprise upgrade cycle during the Q3 earnings period.

“For the first time this quarter… enterprise customers are now actually upgrading their infrastructure in preparation for AI. Some are taking dollars set aside for AI to spend on modernising infrastructure to get ready for that.” — Chuck Robbins, CEO, Cisco (per Diginomica)

Several transactions exceeding $100 million each were signed with global enterprises during Q3, focused on network modernisation and AI/ML deployment. These are not hyperscaler contracts. They are enterprise customers reallocating AI budgets toward the infrastructure prerequisite for AI workloads, a spending pattern that broadens the addressable market beyond the largest cloud providers.

Enterprise AI infrastructure readiness is now a spending priority in its own right: research suggests 70-80% of enterprise AI pilots fail or stall when the underlying network and data integration layer is inadequate, which helps explain why enterprises are reallocating AI budgets toward modernisation rather than applications.

The instinct is to read layoffs as a distress signal. Two rounds of cuts totalling approximately 8,000 positions in three months would ordinarily raise questions about a company’s trajectory. The financial structure of Cisco’s restructuring tells a different story.

The first round, announced in February 2026, eliminated approximately 4,000 jobs. The second round, announced alongside Q3 earnings in May 2026, cut fewer than 4,000 additional positions. Against a baseline workforce of approximately 86,200 employees, the cumulative reduction represents roughly 9% of headcount.

Cisco confirmed it will continue hiring in strategic areas: silicon and AI chips, optics, security, and AI capability development. Robbins framed the cuts as shifting investments toward areas “where demand and long-term value creation are strongest.” The company is not shrinking. It is reallocating capital from lower-priority functions toward the business lines generating 50%+ year-on-year growth.

| Round | Announcement | Jobs Cut | Restructuring Cost |

|---|---|---|---|

| First | February 2026 | ~4,000 | Included in up to $1B total |

| Second | May 2026 | <4,000 | ~$450M charged in Q4 FY2026; remainder into FY2027 |

The total restructuring cost of up to $1 billion, with approximately $450 million allocated to Q4 FY2026, will weigh on near-term earnings. That cost is the price of repositioning a workforce of more than 86,000 toward AI infrastructure demand that nearly doubled the company’s own order forecast.

The guidance revision is the financial output of everything the AI order data signalled.

Cisco raised its full-year FY2026 revenue guidance to a range of $62.8 billion to $63.0 billion, up from a prior range of $61.2 billion to $61.7 billion. At midpoint, the upgrade represents approximately $1.6 billion to $1.8 billion in additional revenue, a roughly 2.7% uplift.

| Metric | Prior Guidance | New Guidance | Change |

|---|---|---|---|

| FY2026 Revenue | $61.2B–$61.7B | $62.8B–$63.0B | +~$1.6B–$1.8B (~2.7%) |

The causal chain is direct:

CFO Scott Herren indicated an expectation of at least $6.0 billion in AI hyperscale-side revenue for FY2027, a forward signal that, if confirmed, would suggest the Q3 acceleration is not a single-quarter anomaly. The broader market context reinforced the reaction: the Nasdaq Composite closed at 26,402.34 on 14 May, with the S&P 500 at 7,444.25, both at or near record levels, driven by AI-linked technology stocks.

AI spending as a share of GDP reached 4.9% in Q1 2026, surpassing both the dot-com peak of approximately 4.2% and the cloud buildout peak of approximately 3.8%; that scale context matters when assessing whether Cisco’s revised $9 billion full-year AI order target represents a durable structural shift or a single-cycle anomaly.

Cisco’s Q3 results illustrate a three-part pattern that is appearing across the enterprise technology sector as companies respond to the AI infrastructure spending wave:

Cisco is not the only beneficiary of the infrastructure spending expansion. On 14 May, semiconductor-adjacent names also advanced:

Forbes reporting on Nvidia’s $5.5 trillion valuation milestone, reached on 13 May 2026, coincided with the S&P 500 posting a record close above 7,450, establishing the broader market backdrop against which Cisco’s own single-session surge registered as one of the standout moves in an already elevated tape.

The question to ask when the next enterprise technology company announces simultaneous layoffs and a guidance upgrade: is the order book growing faster than the restructuring cost, and are the new hire areas aligned with where verified customer demand is actually building?

Investors wanting a structured framework for applying that three-part test across the broader hardware supplier universe will find our dedicated guide to evaluating AI stocks in the hardware capex cycle, which walks through how semiconductor, optics, and networking names are positioned relative to the $600-750 billion hyperscaler spend and where the software monetisation lag poses the primary valuation risk.

Cisco’s Q3 FY2026 results mark a structural inflection point. AI investment has matured from a chip-layer phenomenon into a full-stack infrastructure rebuild, and Cisco is the clearest public data point confirming that transition. The simultaneous layoff and guidance upgrade is not a contradiction. It is a signal that hyperscaler and enterprise capital expenditure has reached the networking layer.

Uncertainties remain. Named hyperscaler customers have not been disclosed. The FY2027 AI revenue figure of at least $6.0 billion requires transcript confirmation. Restructuring charges of up to $1 billion will compress near-term earnings. U.S. equity markets sit at record levels despite above-forecast inflation readings and a rate-hike probability that has risen to over 28% by year-end.

The specific data points to watch in the months ahead:

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements, including revenue guidance and AI order projections, are subject to change based on market conditions and company performance.

Cisco stock surged 16.5% because the company nearly doubled its full-year FY2026 AI order forecast from approximately $5.0 billion to $9.0 billion, driven by $2.1 billion in AI orders during Q3 alone, signalling accelerating hyperscaler demand for networking infrastructure.

Cisco revised its full-year FY2026 AI order forecast to approximately $9.0 billion, up from a prior estimate of around $5.0 billion, following a single quarter in which AI orders reached $2.1 billion.

Cisco supplies the networking, switching, and optics infrastructure that AI-capable data centres require to move data between GPU processors; as hyperscaler capital expenditure on AI compute has scaled, downstream demand for this physical layer has followed, with Cisco's networking products growing more than 50% year on year in Q3 FY2026.

The two rounds of cuts totalling approximately 8,000 positions represent a capital reallocation rather than a distress signal; Cisco confirmed it is continuing to hire in silicon, AI chips, optics, and security, shifting investment toward the business lines generating 40-50% year-on-year growth.

Cisco raised its full-year FY2026 revenue guidance to a range of $62.8 billion to $63.0 billion, up from a prior range of $61.2 billion to $61.7 billion, representing an uplift of approximately $1.6 billion to $1.8 billion at midpoint.