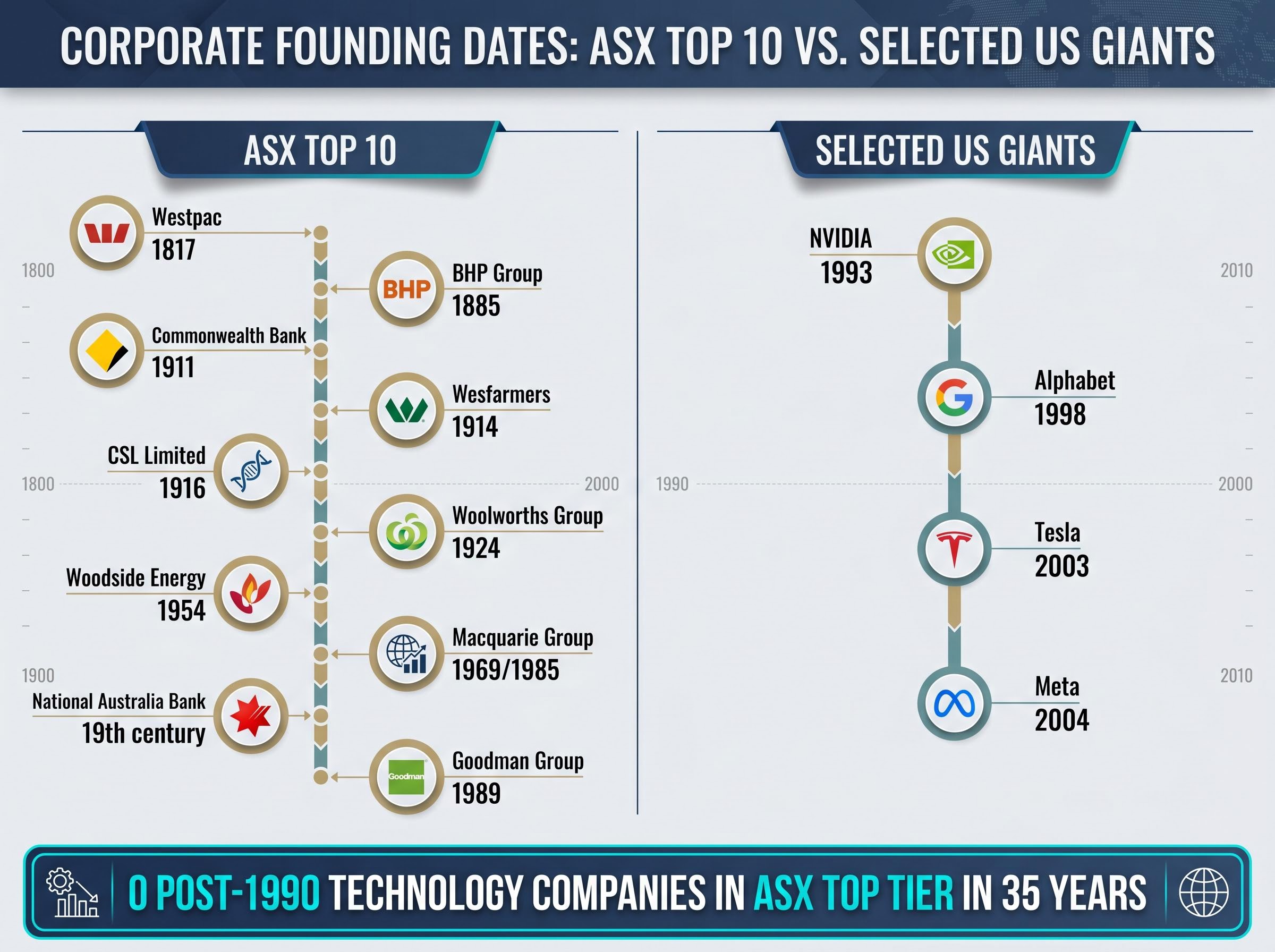

Every company in the ASX top 10 was founded before 1990. The youngest, Goodman Group, dates to 1989. In the United States, several of the largest companies by market capitalisation did not exist until the 1990s or later. That single comparison tells a structural story about Australia’s capacity to build innovation companies at scale.

The 2026-27 Federal Budget has now confirmed that the 50% capital gains tax (CGT) discount will be replaced by inflation indexation from 1 July 2027. Australia has made a consequential policy choice at precisely the moment AI-driven transformation is reshuffling global competitive advantage. The reform is not about property investors alone. Its logic cuts directly through the incentive architecture that motivates founders to build companies and talented employees to accept equity instead of salary.

What follows is an examination of why Australia has failed to produce globally competitive technology companies at scale, what structural forces explain the ASX’s compositional stagnation, and why the confirmed CGT reform raises specific and serious questions about whether Australia is moving in the right direction at the right time.

The ASX top 10 is a museum, not a marketplace of new ideas

Consider the founding dates of the companies that sit at the top of Australia’s equity market.

| Company | Approximate founding | Primary sector |

|---|---|---|

| Westpac | 1817 | Banking |

| BHP Group | 1885 | Resources |

| Commonwealth Bank | 1911 | Banking |

| Wesfarmers | 1914 | Conglomerate/Retail |

| CSL Limited | 1916 | Biopharmaceuticals |

| Woolworths Group | 1924 | Retail |

| Woodside Energy | 1954 | Energy |

| Macquarie Group | 1969/1985 | Financial services |

| National Australia Bank | 19th century | Banking |

| Goodman Group | 1989 | Industrial property/Logistics |

Banks, miners, a supermarket chain, a conglomerate, and a logistics property group. Goodman Group’s recent ascent into the top tier has been driven substantially by AI-linked data centre demand, not a technology founder story in the conventional sense. It is a real estate company that found itself in the path of a technology wave.

In the US, Alphabet (founded 1998), Meta (founded 2004), Tesla (founded 2003), and NVIDIA (founded 1993) all sit among the largest companies by market capitalisation. That difference is not cosmetic. The composition of a country’s largest public companies is a proxy for where its economy has been generating value. When no post-1990 technology company has reached the ASX top tier in 35 years, the question of structural cause is not academic.

When big ASX news breaks, our subscribers know first

Three structural headwinds that the rest of the world does not carry

Australia’s innovation gap is not the product of a single policy failure. Three distinct structural disadvantages compound against one another:

- A small domestic market that limits the addressable revenue base for early-stage companies, forcing premature internationalisation before product-market fit is fully established

- Constrained growth capital, with early-stage funding per capita running roughly 30% below comparable economies

- A dividend-focused corporate culture that rewards income distribution over reinvestment for compounding growth

Each operates as a separate mechanism, but together they form an additive constraint on scaling.

According to the Tech Council of Australia (March 2024), Australia had $12 in angel and seed funding per working-age Australian in 2021, approximately 30% less than Canada.

That per-capita gap matters because it compounds across funding rounds. Companies that struggle to secure seed capital take longer to reach Series A. By the time they do, international competitors have often seized the market position.

The offshore dependency figure sharpens the picture further. In 2025, 66% of Australian startup deals involved at least one international investor, up from 57% in 2024, according to Cut Through Venture and Folklore Ventures. At Series A and beyond, offshore investor participation has become the norm rather than the exception. This is not a sign of cosmopolitan success. It signals structural reliance on capital that Australia’s own ecosystem cannot generate at sufficient scale.

What the CGT discount actually did for founders, and what indexation costs them

How the old system worked for founders

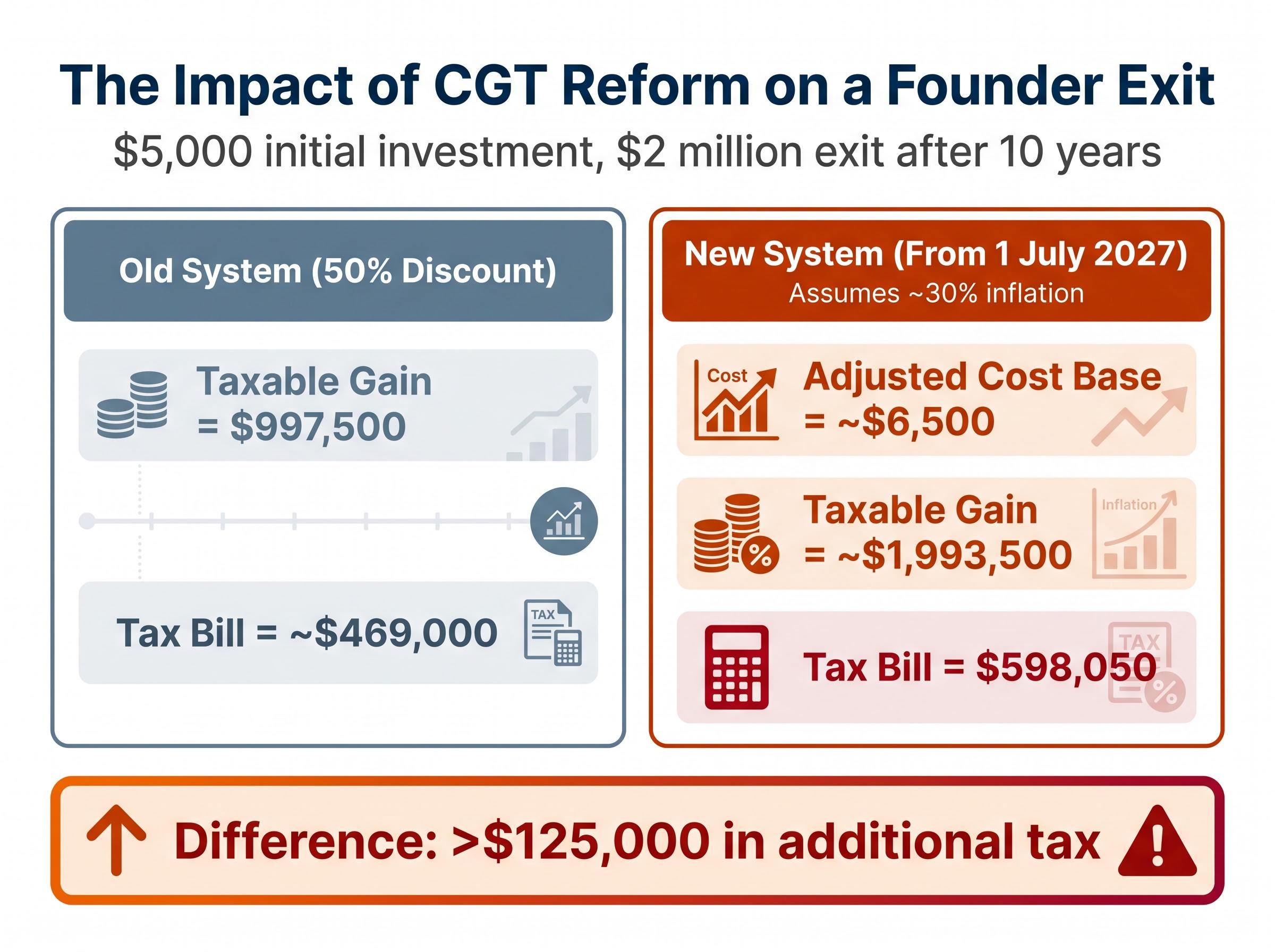

Under the existing framework, a capital gain on an asset held for more than 12 months qualifies for the 50% CGT discount. Only half of the nominal gain is added to taxable income and taxed at the individual’s marginal rate. For an individual on the top marginal rate of 47% (including the Medicare levy), the effective tax rate on a qualifying capital gain falls to approximately 23.5%.

For a founder who invested a few thousand dollars to establish a company, spent years drawing below-market salary, and then sold equity after a decade of value creation, the discount recognised something specific: the bulk of the gain was not inflation, and it was not passive appreciation. It was the product of sustained personal risk and effort.

What the indexation shift means in practice

The confirmed reform, applying from 1 July 2027, replaces the 50% discount with cost-base indexation (adjusting the original cost base for inflation) plus a 30% minimum tax rate on capital gains. The reform applies to individuals, trusts, and partnerships on assets held more than 12 months, and is prospective only, according to the 2026-27 Federal Budget documents confirmed by EY, KPMG, NAB, and Perpetual.

The 2026-27 Federal Budget tax reform documentation confirms the prospective-only application of the new regime, meaning assets acquired before 1 July 2027 retain access to the existing discount, while all post-commencement acquisitions will fall under the indexation and minimum rate framework.

For a founder, the arithmetic changes substantially:

The CGT indexation methodology that applies to gains accruing after 1 July 2027 uses annual CPI data to step up the cost base each year, meaning the relief it provides tracks inflation rather than the growth rate of the underlying asset; for high-growth startup equity, where real appreciation typically far exceeds CPI, the effective taxable gain under indexation will be materially larger than under the old 50% discount in most scenarios.

- Under the old discount: A founder who invested $5,000 and sold for $2 million after 10 years would have a taxable gain of approximately $997,500 (half the nominal gain), producing a tax bill of roughly $469,000 at the top marginal rate

- Under indexation: If cumulative inflation over that decade was approximately 30%, the adjusted cost base rises to roughly $6,500. The taxable gain becomes approximately $1,993,500, with tax of at least $598,050 at the 30% minimum rate

The difference, more than $125,000 in additional tax on a $2 million exit, falls entirely on founders whose initial outlay was small and whose gain reflects years of value creation rather than inflation. Indexation provides meaningful relief when the cost base is large. For founders, it is not.

The founder exit economics under the new regime have been modelled in detail, with Stockspot’s analysis showing a business founder selling a $1 million company could lose more than $225,000 in after-tax proceeds compared with the old discount, a figure that compounds across the thousands of founders who will reach liquidity events in the years immediately following the 2027 transition.

Chris Brycki, founder of Stockspot, has spoken publicly about taking no salary in his first year and earning roughly 10% of his prior corporate income in subsequent years. That pattern is common across early-stage founders. The equity stake is the deferred compensation for those years of below-market pay, and the tax treatment of that equity shapes the entire risk-reward calculation.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Equity compensation and the talent calculus inside Australia’s startups

The CGT reform debate has been framed primarily around founders and property investors. That framing misses the broader impact on the workforce inside early-stage companies.

Equity functions as deferred compensation in startups, not a speculative bonus on top of market salary. Early-stage companies cannot match corporate salary benchmarks. Equity is the primary mechanism for attracting and retaining skilled talent willing to accept that trade-off. Consider the specific decisions at stake:

- A senior engineer leaving a $220,000 banking role for a $150,000 salary plus equity in a Series A company

- An early marketing hire accepting $90,000 and a meaningful equity grant when comparable agency roles pay $130,000

- A second-year product manager choosing between a graduate programme at a listed company and a startup offering equity worth multiples of salary if the company succeeds

- A technical co-founder accepting no salary for 12 months, relying entirely on equity as future compensation

If equity gains are taxed at or near the highest marginal rate, the arithmetic behind each of these decisions shifts. The gap between salary certainty and equity risk widens.

The Tech Council of Australia (2024) explicitly flags the risk of brain drain if Australia does not remain competitive on policy settings relative to peer ecosystems, stressing that global tech talent is highly mobile.

Australia’s tech workforce does not operate in a closed market. The 66% offshore investor participation rate in 2025 deals already demonstrates how easily capital, and the companies it flows into, can shift jurisdictions. If domestic equity economics deteriorate relative to equivalent roles in the US or UK, the marginal decision to stay becomes harder to justify for precisely the workers Australia can least afford to lose.

The 2025 funding recovery masks the depth of Australia’s scaling problem

The recovery is real and worth acknowledging. Australian startups raised approximately $5.4 billion in 2025, up 31% from $4.18 billion in 2024, according to Cut Through Venture and Folklore Ventures. Q4 2025 delivered over $2 billion, the strongest quarter since the 2021 peak. Queensland crossed the $500 million mark for the first time, raising $504 million across 61 deals.

| Year | Total startup funding (A$ billions) | Source |

|---|---|---|

| 2021 | $10B+ | Statista |

| 2023 | ~$3.5B | Statista |

| 2024 | $4.18B | Cut Through Venture / Folklore |

| 2025 | ~$5.4B | Cut Through Venture / Folklore |

A single strong year does not dissolve a structural pattern. Three indicators define the ceiling that sits above the recovery:

- Per-capita funding gap: Early-stage funding per working-age Australian remains approximately 30% below Canada, according to the Tech Council of Australia

- Offshore dependency: 66% of 2025 deals required at least one international investor, meaning Australian companies increasingly rely on foreign capital to scale

- Scaling lag: NSW startups attracted 65% of total startup funding in 2024, according to Startup Genome, reflecting geographic concentration that limits ecosystem breadth

The 2025 recovery is occurring against a backdrop of AI-driven capital reallocation globally. That creates both opportunity and competitive pressure: US and other ecosystems are scaling AI companies far faster. A funding recovery moment is precisely when policy settings should be removing friction, not adding it.

The per capita economic conditions underpinning the startup ecosystem tell a sharper story than headline GDP: corporate insolvencies reached their highest level since the 1990-91 recession in 2025, real wages declined as inflation outpaced wage growth, and consumer confidence fell to a 50-year low, forming the demand-side backdrop against which Australia’s innovation funding gap and the CGT reform debate both sit.

The reform arrives at the worst possible moment for Australian ambition

AI-driven transformation represents a genuine window. Sectors that lock in dominant positions during the current cycle could hold structural advantages for decades. Australia’s window to produce globally competitive AI-adjacent companies is measurable in years, not decades.

The CGT reform taking effect from 1 July 2027 will begin shaping founder and talent decisions from mid-2026 onward, as companies formed now will model their expected exit economics under the new regime.

The collision is specific: the policy change lands at the precise moment when the opportunity cost of deterring company formation is highest. Goodman Group’s AI and data centre-driven growth illustrates how Australia can benefit from the AI cycle as an infrastructure play, but a logistics property company reaching the ASX top 10 through technology demand is not the same as producing a software or platform company of equivalent scale. The structural gap persists.

The government’s stated rationale for the reform, fiscal repair and a fairness argument between capital income and labour income, deserves acknowledgment. These are not trivial concerns. The prospective-only application reduces the injustice of retroactive change. But the question of whether an innovation-sector exemption or alternative mechanism warranted more considered policy treatment than it received remains open.

These statements are speculative and subject to change based on market developments and company performance.

The Tech Council of Australia’s framing is direct: competitive tax settings are necessary to retain mobile global tech talent. That framing does not require endorsing the old system wholesale. It requires recognising that removing a partial counterweight to Australia’s structural disadvantages, without replacing it, carries a measurable cost.

Australia’s innovation future is still a choice, not a verdict

The ASX top-10 composition is not an accident. It is the product of compounding policy and market conditions over 30 years. The 2025 funding recovery, growing offshore investor engagement, and AI-linked capital flows create genuine conditions for change. But conditions and outcomes are not the same thing.

A more innovation-aware approach need not require wholesale CGT reform reversal. Specific mechanisms could include a tailored treatment for startup equity and founder gains; indexation combined with a reduced rate for assets held beyond a threshold period; or a formal review mechanism that models impacts on startup ecosystems before implementation.

If Australia’s next 30 years look like the last 30 at the top of the ASX, the cost will be measured not in failed startups but in the productivity, wages, and global relevance that scaled technology companies generate. The composition of the index will tell the story. The question is whether the policy settings being locked in today will produce a different chapter.