Why Your ETF Portfolio May Be Less Diversified Than You Think

8 mins ago

For 27 years, Australian investors have planned around a single number when selling an investment asset: a 50% discount on capital gains for anything held longer than 12 months. On 12 May 2026, the federal budget confirmed that number no longer applies from 1 July 2027. In its place, the government will reinstate a Consumer Price Index (CPI) indexation model, the same framework Australia used before 1999, recalibrated for the current tax system and paired with a 30% minimum effective tax rate. This is not a marginal adjustment to capital gains tax settings. It is a structural reset of how taxable gains are calculated across property, equities, and business interests. What follows is a complete explanation of how the new mechanics work, which assets are captured, who faces higher or lower tax bills, and what the transition period between now and 2027 demands of anyone holding investment assets in Australia.

Capital gains tax (CGT) applies to the realised profit on investment assets at the point of sale. The gain is the difference between the sale price and the original cost base. It does not apply to an owner-occupied primary residence.

The asset classes captured by CGT include:

Before 1999, the mechanism for adjusting the taxable gain was indexation: the original cost base was adjusted for inflation using the CPI, and tax applied only to the real gain above that adjusted figure. The Howard government replaced indexation with a flat 50% discount for assets held longer than 12 months, arguing it was simpler and more predictable.

The CGT discount replacement is only one component of a three-pillar budget reform that also introduces a negative gearing ring-fence on established properties and a 30% minimum tax on discretionary trust distributions, with each pillar carrying distinct effective dates and grandfathering provisions that interact differently depending on how an investor holds their assets.

The 50% discount applied equally regardless of how long the asset was held beyond 12 months or how much inflation had actually eroded the real value of the gain. An investor who held through a decade of high inflation received the same reduction as one who held through near-zero inflation.

That bluntness is the conceptual problem the new system is designed to address. The discount was poorly calibrated to actual economic conditions, and the argument for returning to indexation rests on taxing only the portion of a gain that represents genuine economic profit rather than nominal price growth driven by inflation.

The core calculation under the new model follows a four-step sequence:

The formula is straightforward: taxable gain equals sale price minus CPI-adjusted cost base. The structural logic differs from the outgoing system because the inflation adjustment is calibrated to actual price-level changes over the specific holding period, rather than applying a blanket 50% reduction.

The 30% minimum effective rate is a distinct feature. For higher-income investors whose marginal rate already exceeds 30%, this provision changes nothing. For lower-income investors whose marginal rate sits below that threshold, the minimum rate increases their CGT liability beyond what a straight marginal-rate calculation would produce.

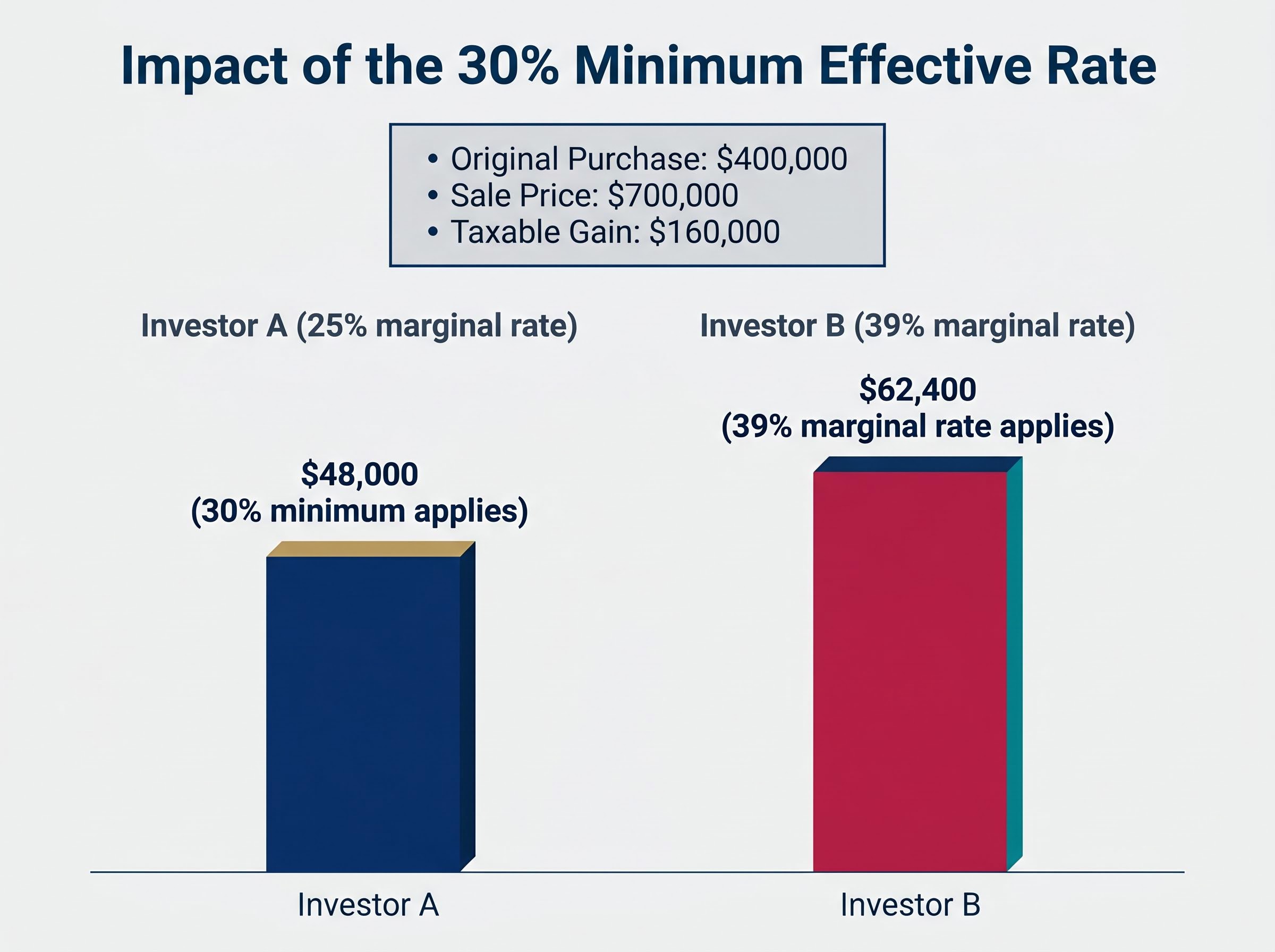

The following worked example illustrates how outcomes differ at two marginal rates. The CPI adjustment factor is illustrative.

| Component | Investor A (marginal rate 25%) | Investor B (marginal rate 39%) |

|---|---|---|

| Original purchase price | $400,000 | $400,000 |

| CPI adjustment factor (illustrative) | 1.35 | 1.35 |

| Indexed cost base | $540,000 | $540,000 |

| Sale price | $700,000 | $700,000 |

| Taxable gain | $160,000 | $160,000 |

| Applicable rate | 30% (minimum applies) | 39% (marginal rate applies) |

| Tax payable on gain | $48,000 | $62,400 |

Investor A’s marginal rate of 25% is overridden by the 30% floor, resulting in a higher tax bill than a straight marginal-rate calculation would produce. This provision is one of the features likely to attract detailed scrutiny once draft legislation is released.

The new indexation model applies across the full range of capital assets held by individual taxpayers: investment property, equities and shares, and business interests. The primary residence remains exempt, consistent with the existing CGT framework.

| Asset category | Treatment under new model |

|---|---|

| Established residential investment property | Captured: CPI indexation and 30% minimum apply |

| Newly constructed residential property | Exempt from changes |

| Equities and shares | Captured: CPI indexation and 30% minimum apply |

| Business interests | Captured: CPI indexation and 30% minimum apply |

| Pre-1985 assets | Newly captured: brought into CGT scope |

| Primary residence | Exempt (unchanged) |

The new-build exemption is a deliberate policy design. By carving out newly constructed dwellings, the government is directing investment capital toward new housing supply rather than established stock. This distinction may influence capital allocation decisions for property investors weighing renovation of existing holdings against acquisition of new builds.

Assets acquired before 20 September 1985 have sat entirely outside the CGT regime since its introduction. Under the new model, these pre-1985 assets are brought into scope for the first time. For long-term holders of legacy property, equities, or business interests acquired before that date, this represents the most significant shift in their tax position in decades.

Pre-1985 asset holders face a specific valuation risk that goes beyond simply being brought into scope: the new framework establishes a deemed cost base at 1 July 2027 equal to market value at that date, meaning the taxable gain on any future disposal is measured from that point forward rather than from the original acquisition price, creating an urgent need for formal valuations of legacy family properties and business interests before the start date.

Entity-level treatment, including how these changes interact with superannuation funds, trusts, and companies, remains unresolved. Budget materials indicate this will be addressed in draft legislation and the accompanying explanatory memorandum, expected during 2026.

The new system does not produce a uniformly worse or better outcome for all investors. The relative tax burden depends on two variables: the magnitude of the asset’s nominal appreciation and how much of that appreciation was driven by inflation rather than genuine demand.

Analysis from realestate.com.au found that approximately 27% of residential property investors who generated a capital gain over the past decade would have faced a lower taxable amount under indexation than under the flat 50% discount. Their gains were heavily inflation-driven, meaning the CPI adjustment stripped out a larger portion of the nominal increase than the blanket discount would have.

The share peaked at around 39% in Q4 2023, approximately 12 months after Australian inflation reached its recent high. During that window, a greater proportion of property disposals involved gains where general price-level rises, rather than asset-specific demand, accounted for most of the nominal increase.

Even in the pre-pandemic low-inflation environment, the share of investors who would have benefited from indexation sat at approximately 26%, indicating that a meaningful minority benefits from inflation-adjusted cost bases regardless of the broader inflationary environment.

The geographic picture adds further nuance.

| City | Recent capital growth trajectory | Likely comparative outcome |

|---|---|---|

| Sydney | Strong growth 2016-2022, high nominal gains | Flat 50% discount generally more favourable |

| Melbourne | Moderate growth, gap narrowing in recent years | Closer to neutral; outcome depends on specific holding period |

| Brisbane | Strong recent capital growth post-pandemic | More likely to face higher taxable gain under indexation |

Investors whose assets appreciated sharply due to genuine demand (particularly in Brisbane’s recent growth cycle) are more likely to face a higher taxable gain under the new model. Those whose nominal gains were substantially eroded by inflation may find the indexed cost base produces a smaller taxable figure than the old discount.

The market implications emerge from the policy design itself rather than from observed data, which remains limited one week after the announcement.

The lock-in risk is real. Investors holding assets with large embedded gains face a calculation: accelerate disposals before 1 July 2027 to realise gains under the current 50% discount, or defer sales beyond the start date and restructure around the new rules. Both responses carry costs, and the period between now and 2027 is likely to influence transaction timing across property and equity markets.

The lock-in effect operates as a structural distortion across asset classes: when the tax cost of disposal rises sharply, rational investors defer sales even when portfolio reallocation would otherwise be economically justified, reducing market liquidity and potentially concentrating wealth in assets held for tax reasons rather than return expectations.

The new-build exemption carries a structural incentive. By preserving favourable CGT treatment for newly constructed residential property, the policy explicitly aims to redirect investment capital toward new supply. Whether that incentive is sufficient on its own is a separate question. The absence of complementary state-level reforms, including upzoning, stamp duty restructuring, and planning approval acceleration, means the new-build carve-out is unlikely to resolve Australia’s structural housing shortage in isolation.

PropTrack has projected modest downward pressure on dwelling prices and slight upward pressure on rents in the near term as investors recalibrate their positions.

Total investment in capital assets is expected to decline modestly in absolute terms, though property (particularly new builds) may attract relatively stronger capital flows than other asset classes as the exemption takes effect.

Three uncertainties remain unresolved pending draft legislation:

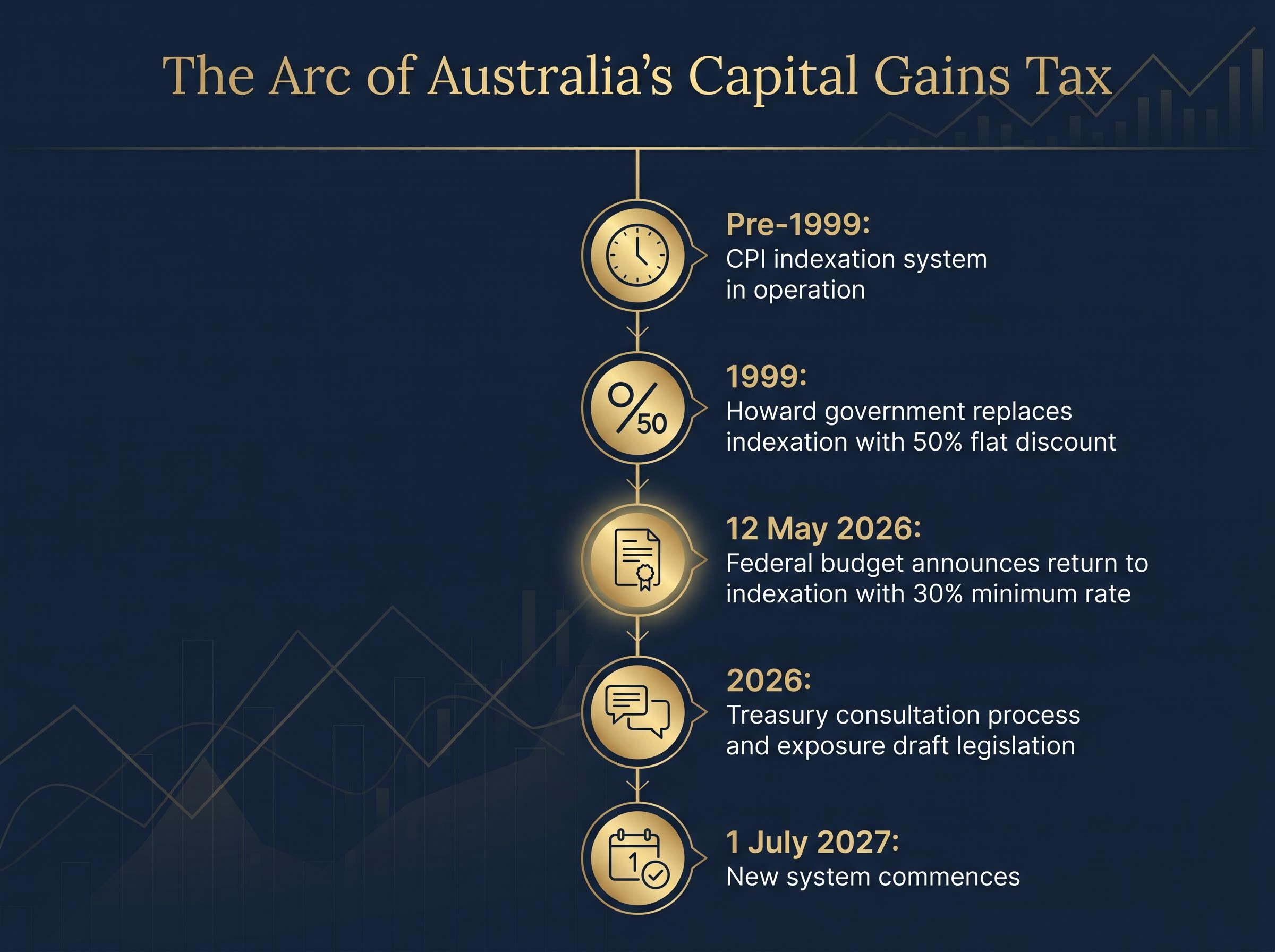

The return to indexation is not without precedent. It is, in a direct sense, a return to the system Australia used before 1999. Indexation was the original CGT adjustment mechanism from the regime’s inception, and the Howard government’s switch to the flat 50% discount was framed at the time as a simplification, not an improvement in precision.

The 2026 budget reversal reframes that decision. The government’s position is that the bluntness of the flat discount created inequities, overtaxing investors in high-inflation periods and undertaxing those in low-inflation periods, relative to the real economic gain actually realised.

The timeline of this policy cycle illustrates the arc:

The period between now and 1 July 2027 is the planning window. Investors can assess their position under both systems and make informed decisions about timing, structure, and capital allocation before the transition takes effect. The Treasury consultation process and exposure draft legislation expected during 2026 will resolve outstanding design questions, and tracking these releases is the single most productive step for any investor seeking clarity on entity-level treatment and precise implementation mechanics.

The core change can be stated in a single formulation.

From 1 July 2027, the tax benefit on a capital gain is no longer a flat 50% reduction. It is an inflation-adjusted cost base, calculated using CPI over the holding period, with the resulting gain taxed at the individual’s marginal rate or 30%, whichever is higher.

Three groups of investors face the most material exposure during the transition:

The next material event is the 2026 Treasury consultation process. Exposure drafts will clarify entity-level treatment for superannuation funds, trusts, and companies, alongside remaining design questions that Budget materials have not yet addressed. The window between now and 1 July 2027 is the period in which these details will emerge, and in which asset holders can plan accordingly.

For investors who have identified exposure across the three groups above and want a structured approach to the transition window, our comprehensive walkthrough of portfolio repositioning before 2027 covers the specific actions available before 30 June 2027, including crystallising gains under grandfathered rules, maximising concessional superannuation contributions using unused carry-forward cap space, and evaluating dividend-focused asset shifts that are entirely unaffected by the minimum tax floor.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. The CGT reform parameters described are based on the 12 May 2026 Budget announcement; final legislative details remain subject to the Treasury consultation process and passage of enabling legislation.

From 1 July 2027, Australia replaces the 50% flat CGT discount with a CPI indexation model, where the original cost base is adjusted for inflation over the holding period and the resulting gain is taxed at the investor's marginal rate or 30%, whichever is higher.

Under indexation, the original purchase price is multiplied by a CPI adjustment factor covering the holding period, producing an inflation-adjusted cost base; tax is then applied only to the gain above that figure, rather than to 50% of the total nominal gain.

The three groups facing the most material exposure are pre-1985 asset holders brought into CGT scope for the first time, established property investors in high-growth markets such as Brisbane, and lower-income investors whose marginal rate falls below the new 30% minimum floor.

Yes, newly constructed residential properties are carved out of the changes as a deliberate policy choice to direct investment capital toward new housing supply, while established residential investment properties remain fully captured by the indexation model and 30% minimum rate.

Investors should assess whether their assets are better positioned under the current 50% discount or the incoming indexation model, consider the timing of any disposals before the 2027 start date, and monitor the Treasury consultation process and exposure draft legislation expected during 2026 for clarity on entity-level treatment.