SK Hynix’s $26.5B Nasdaq Listing Shatters ADR Demand Records

7 hrs ago

The S&P/ASX 200 added 99.4 points on Tuesday as Donald Trump’s decision to step back from planned military action against Iran swept risk back into global markets. The index closed at 8,604.7, a gain of 1.17%, but underneath that headline number the session told a more complicated story. Advancing stocks outnumbered decliners 206 to 77 in the broader ASX 300, a complete reversal of the prior session’s tone, yet money rotated sharply into defensives and yield-sensitive sectors while Materials finished essentially flat and Technology closed lower. The pattern pointed to a market that was selective rather than uniformly bullish.

This wrap covers every sector’s performance, the commodity moves driving divergence within Materials, the individual stocks that moved most on company-specific news, and what the technical picture suggests about whether Tuesday’s recovery has legs.

Trump’s reversal on planned strikes against Iran eased two pressure points simultaneously: crude oil prices fell and bond yields pulled back. ICE Brent crude dropped 1.9% to US$109.98 per barrel, removing a cost-of-living headwind that had been compressing consumer sentiment for weeks. The yield relief, in turn, gave rate-sensitive sectors room to rally.

The rally’s character, though, was rotation rather than broad risk-on buying. Small Ordinaries gained just 0.62%, roughly half the benchmark’s move, and the Australian dollar fell 0.48% to 0.7134 against the USD, a signal that foreign exchange markets were pricing a more cautious read on the global outlook than equities suggested.

Tuesday’s 3:1 advance-decline ratio was a clear improvement on recent sessions, but ASX market breadth had been deteriorating sharply in the weeks prior, with 22 index constituents hitting 52-week lows in the first week of May even as the headline index barely moved, a pattern that makes single-session breadth readings a less reliable gauge of underlying health than a multi-week trend.

206 stocks advanced against just 77 decliners in the ASX 300, a breadth ratio of nearly 3:1.

At the Australian close, US S&P 500 futures sat 0.18% lower at 7,412.75 and Nasdaq futures had declined 0.31% to 29,004.5, suggesting Wall Street was not extending the optimism with the same conviction.

Consumer Staples led the session with a 3.00% gain, the clearest expression of the day’s logic. Lower crude prices reduce input and transport costs for supermarket chains and food producers, and the market moved to price that benefit immediately. Communication Services followed at +2.66%, while Health Care added 1.87%.

The yield-sensitive sectors told their own story. Real Estate rose 1.81% and Financials gained 1.72%, both responding to the pullback in bond yields that accompanied the easing in geopolitical risk. These are sectors that compress when yields rise and expand when they fall; Tuesday delivered the latter.

For investors wanting to build a systematic framework around the kind of rotation Tuesday illustrated, our comprehensive walkthrough of sector rotation strategy covers the four business cycle phases, the sectors that structurally lead each phase, and the Relative Rotation Graph tools that institutional desks use to track capital flows in real time before official economic data confirms the shift.

| Sector | Change (%) | Closing level |

|---|---|---|

| Consumer Staples | +3.00% | 11,674.1 |

| Communication Services | +2.66% | 1,765.1 |

| Health Care | +1.87% | 22,728.8 |

| Real Estate | +1.81% | 3,554.1 |

| Financials | +1.72% | 9,235.2 |

| Consumer Discretionary | +1.52% | 3,389.2 |

| Industrials | +1.23% | 7,953.2 |

| Utilities | +1.02% | 10,137.4 |

| Energy | +0.52% | 10,760.7 |

| Materials | -0.07% | 23,870.8 |

| Information Technology | -0.43% | 1,724.9 |

Materials shed 0.07% and Information Technology fell 0.43%, the only two sectors to finish in the red. Their absence from the rally reinforces the read that Tuesday’s move was a defensive rotation, not a uniform risk appetite recovery.

The Consumer Staples surge had a specific catalyst at its centre. JPMorgan upgraded Woolworths (WOW) to Overweight from Neutral and raised its price target to $37.00 from $35.00. The stock responded with a 3.7% gain to close at $34.21.

JPMorgan upgraded Woolworths to Overweight from Neutral on 19 May 2026, lifting its price target to $37.00 from $35.00.

The upgrade pulled the broader staples cohort higher:

The major banks, meanwhile, rode the bond yield pullback from recent multi-year highs. When yields fall, bank net interest margin pressure eases and the present value of future earnings rises, a mechanical tailwind for the sector.

AMP and QBE both outperformed the big four, each gaining 2.9%. The distinction matters: broker re-ratings like the Woolworths upgrade tend to carry a longer duration effect than a single session’s yield move, which can reverse overnight.

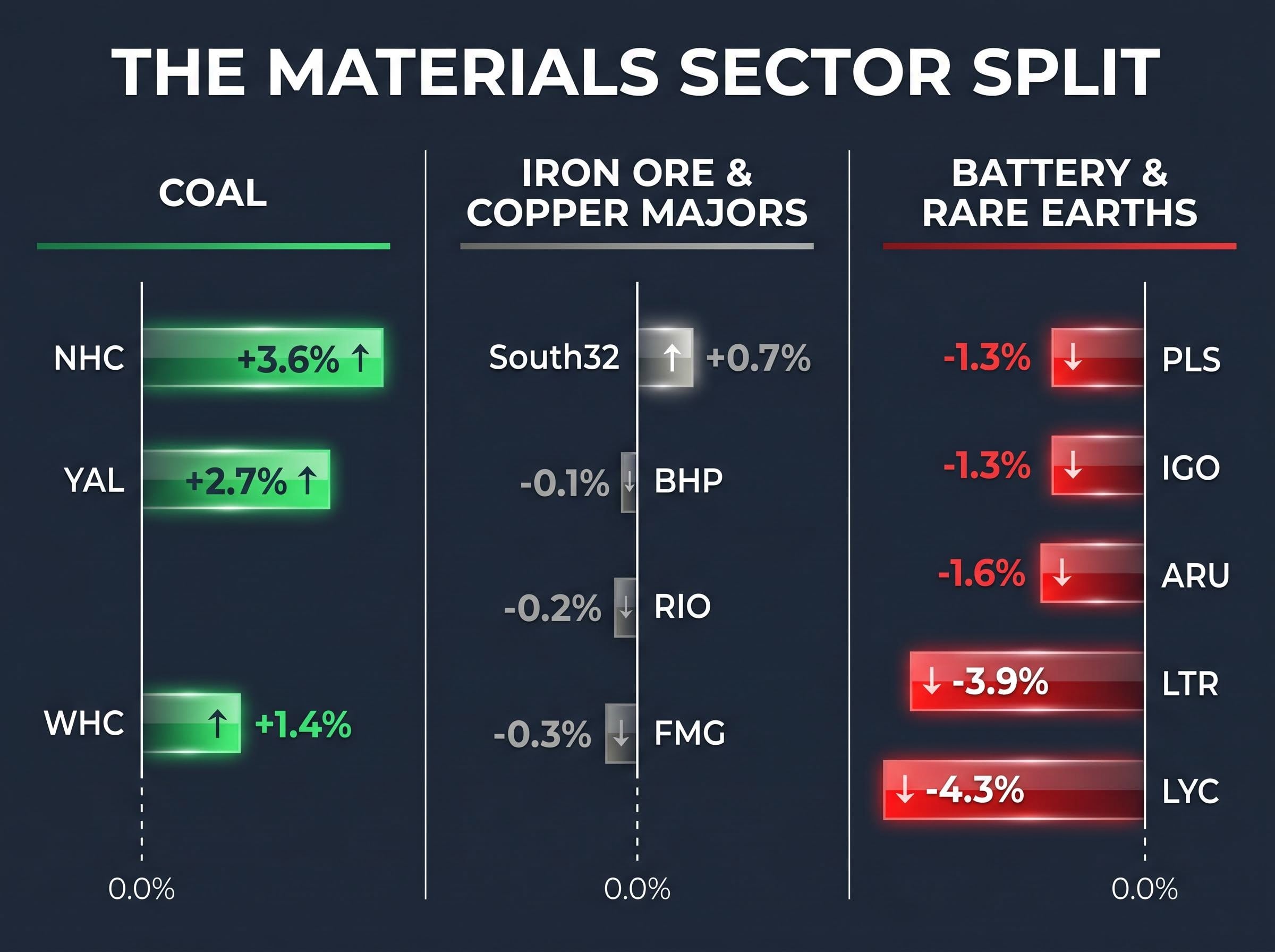

The Materials index shed 0.07%, a number that concealed a three-way split between iron ore weakness, coal strength, and sustained selling in battery materials.

SGX iron ore futures fell 0.9% to US$107.30 per tonne, their fourth consecutive daily decline and now more than 4% below the prior week’s two-year peak. COMEX copper futures dropped 0.7% to US$6.27 per pound.

Both RIO and BHP found buyers at intraday lows, suggesting value-oriented demand emerged as prices dipped, but neither could push into positive territory by the close.

globalCOAL Newcastle futures rose 1.2% to $140.45 per tonne, and the ASX-listed coal producers tracked the move closely.

NdPr oxide prices (a rare earths pricing benchmark) in China fell 0.5% to CNY 711,500 per tonne, while GFEX lithium carbonate futures dropped 3.9% to CNY 184,060 per tonne, their fifth straight session of declines. Australian spodumene slipped 2.0% to US$2,745 per tonne, also a fifth consecutive daily fall.

The flat Materials index number was an averaging illusion. Coal surged, iron ore slipped, and battery materials sold off, each driven by distinct commodity fundamentals that require separate monitoring.

Tuesday’s standout movers each carried a distinct corporate story rather than a shared macro driver.

4DMedical’s clinical data showed a 76% response rate for CT:VQ-guided patient selection compared with 46% under standard care. The share price fell 8.8% regardless, a disconnect that may reflect market scepticism about the timeline to commercial adoption rather than the clinical outcome itself.

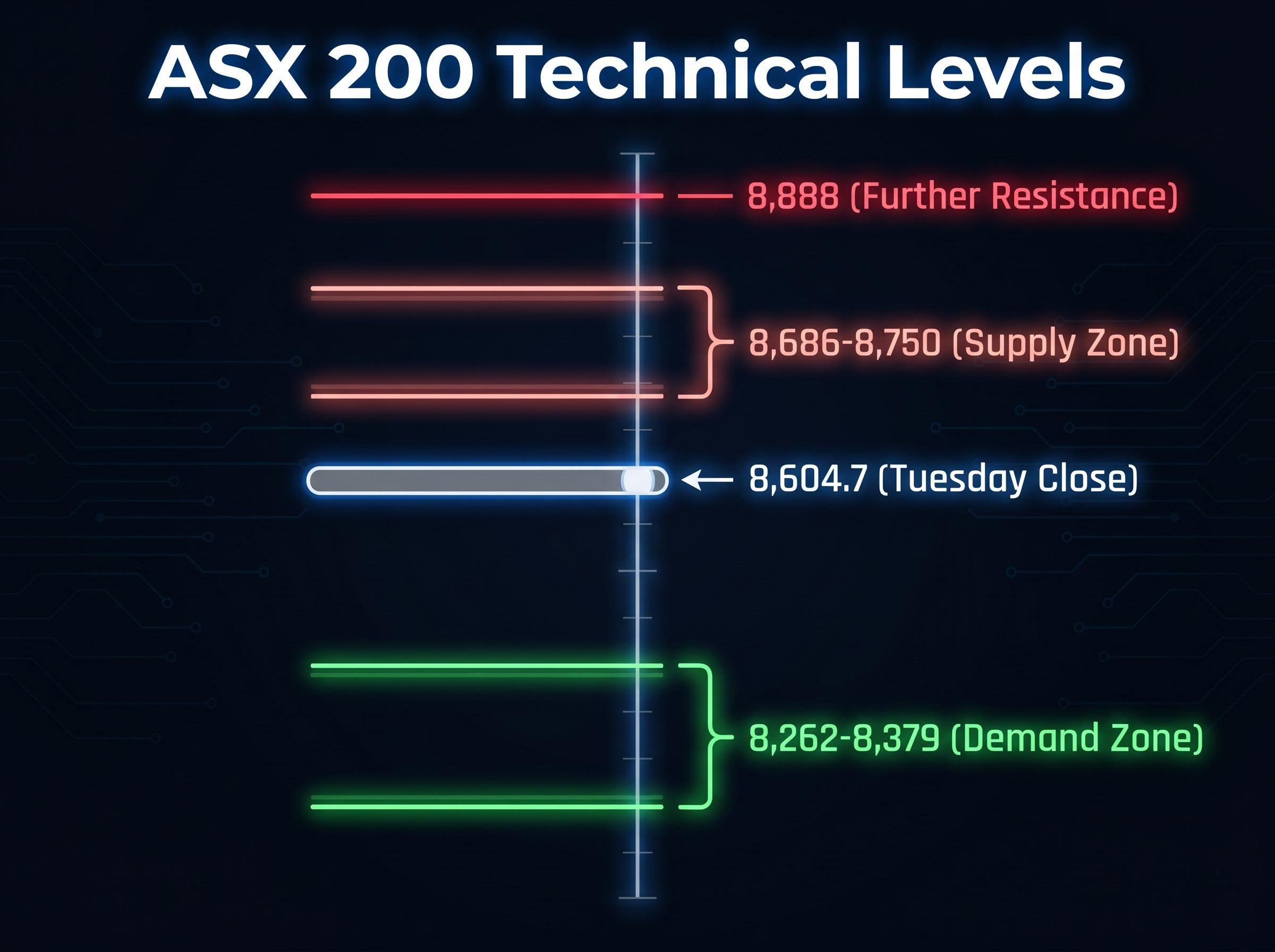

One strong session has not altered the structural outlook. According to Carl Capolingua, Senior Editor at Market Index, the ASX 200’s short-term and long-term trend ribbons still sit above the index price and function as resistance rather than support. The index remains technically in a downtrend.

The technical configuration described by Carl Capolingua, where downtrend ribbons sit above price and function as resistance rather than support, mirrors the structure of the 2022-2023 ASX market cycle drawdown phase, when multiple failed tests of trend ribbon resistance preceded the eventual breakout and a prolonged recovery that significantly rewarded patience over reactive repositioning.

Carl Capolingua, Senior Editor at Market Index, described Tuesday’s session gain as “roughly average in size” with “unimpressive” volume.

The immediate overhead obstacle is a supply zone at 8,686-8,750, where the combined downtrend ribbons converge. Further resistance sits at 8,888.

By contrast, the Nasdaq Composite carries a more constructive structure, with excess demand intact and dip-buying at 25,739 establishing a demand floor. The Nasdaq’s short-term uptrend support ribbon sits at 24,473-25,052, well below its supply point at 26,708. The ASX does not yet share that favourable positioning.

A close above 8,750 would signal a genuine reversal. A failure at resistance followed by a close below 8,379 would confirm the downtrend remains intact.

The data calendar for the remainder of the week will either reinforce or complicate the conditions behind Tuesday’s recovery.

Westpac’s Consumer Sentiment index sits at 83 in May, still deeply pessimistic and well below the 100 neutral threshold. Both forward-looking sub-indexes are at their weakest combined reading since November 2022.

The depth of consumer pessimism behind that Westpac reading reflects per capita recession conditions that have been building since mid-2025: real wages declined as the Wage Price Index failed to keep pace with inflation, corporate insolvencies reached their highest level since the 1990-91 recession, and the Strait of Hormuz fuel shock added more than one percentage point to headline CPI in March, compressing household budgets well before Tuesday’s crude relief arrived.

If Iran tension stays subdued and Australian employment holds near 4.3%, the conditions that fuelled Tuesday’s rally remain in place. The technical resistance at 8,686-8,750 is the first real test of whether they are sufficient.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

—

An ASX market wrap is a daily summary of the Australian Securities Exchange's performance, covering index moves, sector results, commodity drivers, and notable individual stock movers to give investors a complete picture of the session.

Consumer Staples gained 3.00%, the best of any sector, driven by a JPMorgan upgrade of Woolworths to Overweight with a price target lift to $37.00, which pulled the broader cohort including Coles and Metcash higher.

The Materials index shed 0.07% because it masked three separate commodity trends: iron ore futures fell 0.9%, lithium carbonate futures dropped 3.9% for a fifth straight session, while Newcastle coal futures rose 1.2%, with the opposing moves cancelling each other out at the index level.

The immediate supply zone sits at 8,686-8,750 where downtrend ribbons converge, with further resistance at 8,888; a close above 8,750 would signal a genuine reversal, while a close below 8,379 would confirm the downtrend remains intact.

Australia's April Employment Change is due Thursday, forecast at +15,700 with the unemployment rate expected to hold at 4.3%, while US Flash PMI data and Federal Reserve minutes from the May meeting will also be released mid-week.