The four dominant AI hyperscalers plan to deploy a combined US$725 billion toward AI-related infrastructure this calendar year. Yet most Australian retail investors accessing this theme are still buying semiconductor ETFs, while the physical layer powering those chips remains underowned. Power grids, liquid cooling systems, copper transmission cables, and grid equipment operators are not headline names, but they are the load-bearing walls of the AI data-centre buildout. Two ASX-listed ETFs give retail investors direct access to this layer: VanEck’s IFRA and Global X’s AINF. Together they represent contrasting approaches. One is a broad, income-generating infrastructure fund repriced by the AI narrative; the other is a concentrated, thematic bet on the specific companies building the power and cooling backbone of data centres globally. This analysis breaks down what each ASX AI ETF actually holds, how they have performed, what they cost, and where an analyst is recommending entry points, so Australian investors can determine whether one, both, or neither belongs in their portfolio.

The physical bet that semiconductor bulls are missing

The AI investment hierarchy has a visibility problem. GPUs and chips sit at the top of investor consciousness, attracting the bulk of retail flows. But underneath every rack of Nvidia accelerators sits a prerequisite layer: power delivery systems, liquid cooling infrastructure, transmission cables, and grid equipment. Without them, the silicon does nothing.

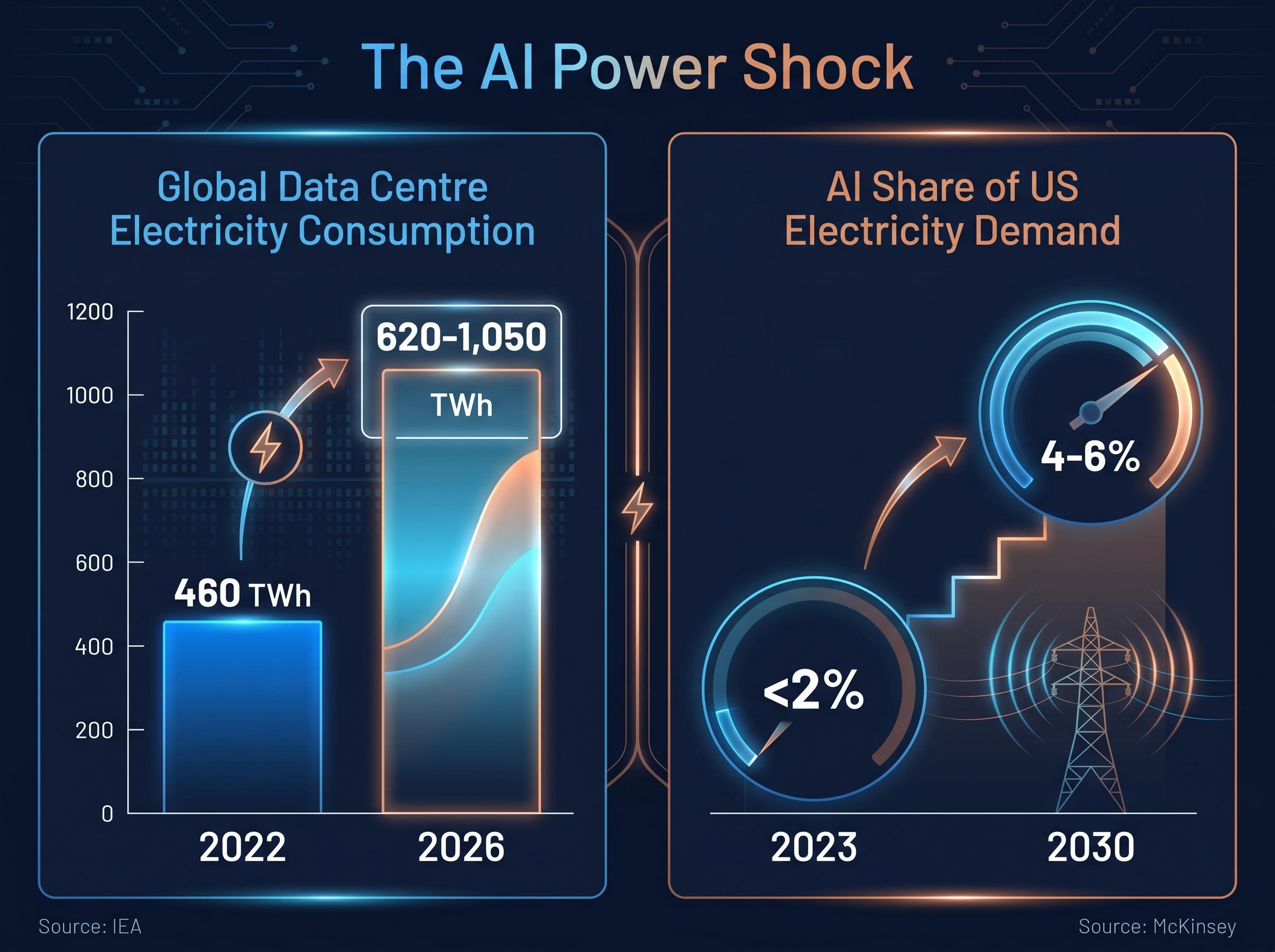

The scale of demand at this physical layer is not speculative. According to the International Energy Agency, global electricity consumption by data centres is projected to reach 620-1,050 TWh in 2026, up from approximately 460 TWh in 2022. McKinsey estimates AI data centres could account for 4-6% of total US electricity demand by 2030, up from less than 2% in 2023. US grid investment may need to increase by US$30-50 billion per year above current plans to accommodate AI-related load growth.

Global electricity consumption by data centres is projected to reach 620-1,050 TWh in 2026, up from approximately 460 TWh in 2022 (IEA, Electricity 2025).

CBRE Investment Management expects global power demand for data centres to more than double by 2030. Four sub-themes consistently surface across Australian media commentary as investable angles within this buildout:

- Copper, for transmission and data-centre cabling

- Uranium and nuclear, for baseload power generation

- Liquid cooling systems, for AI-specific thermal management

- Power management and grid equipment, for transmission and generation upgrades

AINF and IFRA are the two most accessible ASX-listed vehicles for capturing this physical infrastructure layer, each approaching the thesis from a fundamentally different angle.

Investors weighing ETF-level exposure against direct equity positions will find that ASX infrastructure investment models span a wider set of structures than the two funds covered here, including colocation operators, property groups with data-centre exposure, and network services providers, each carrying a distinct earnings profile within the same structural demand trend.

When big ASX news breaks, our subscribers know first

What AINF actually owns, and why it is built differently

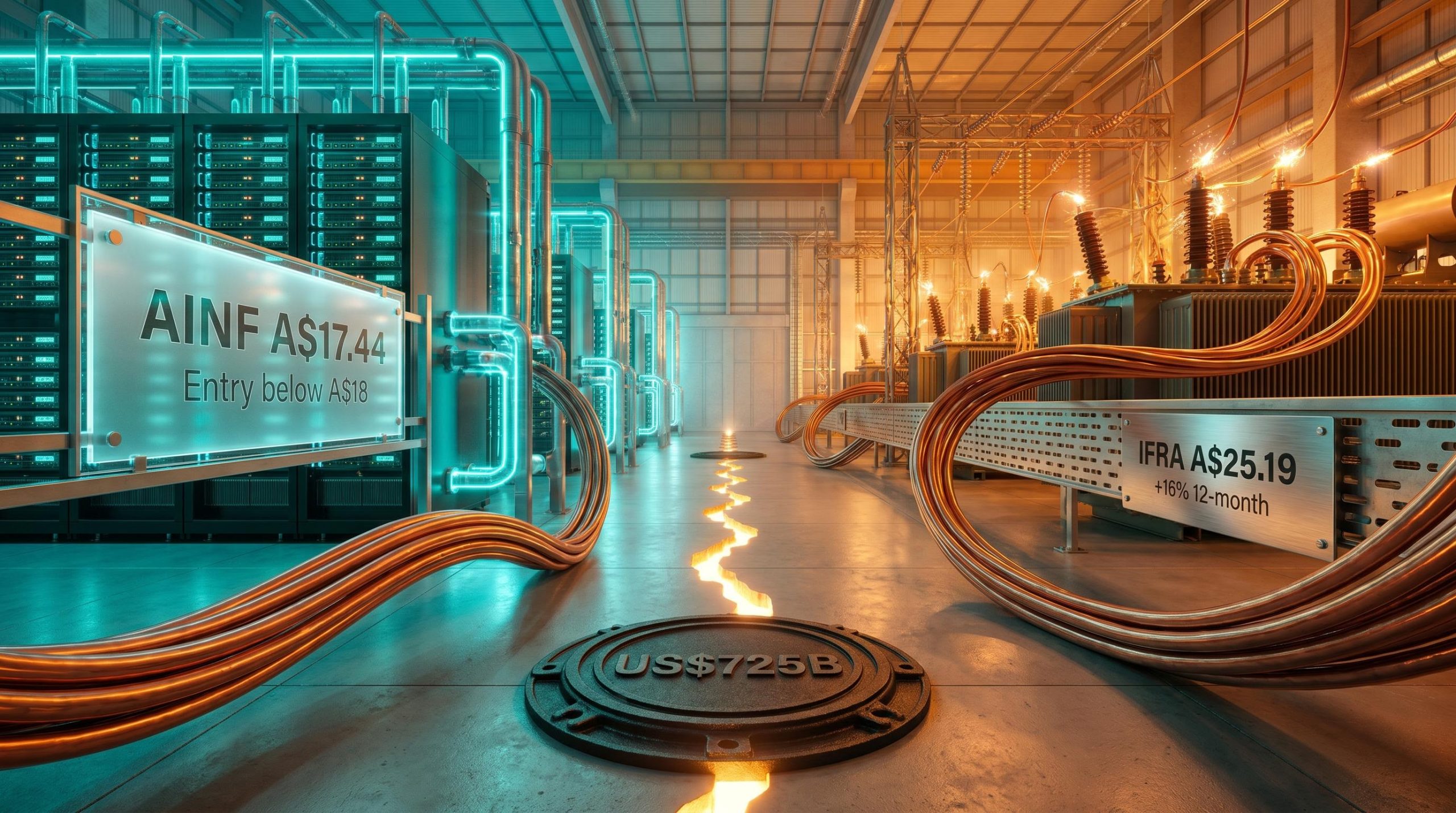

Global X’s AINF (ASX: AINF) launched on 28 April 2025 and has accumulated A$127.57 million in funds under management as at 15 May 2026. Its management expense ratio sits at 0.57% p.a.

The fund holds approximately 31 positions, a deliberately concentrated portfolio built around a specific thesis: own the companies physically constructing the power, cooling, and connectivity infrastructure inside and around AI data centres. The top three holdings illustrate that thesis in action.

| Company | Ticker | Weight | AI Infrastructure Role |

|---|---|---|---|

| Delta Electronics | Taiwan: 2308 | 6.67% | Power supply systems and liquid cooling for AI servers; new offerings improve energy efficiency by up to 15% vs prior generation |

| Vertiv Holdings | NYSE: VRT | 6.04% | Liquid cooling and power infrastructure for hyperscale data centres; Q1 2025 net sales US$1.88 billion, up from US$1.68 billion in Q1 2024 |

| GE Vernova | NYSE: GEV | 5.99% | Grid solutions and gas power businesses enabling AI-driven electricity demand |

Vertiv’s Q1 2025 results are particularly instructive. The company cited AI data-centre demand, particularly liquid cooling, as its primary growth driver. Multiple Wall Street analysts, including Barclays, raised price targets in May 2025 on the strength of that cooling thesis.

The currency exposure question

AINF does not hedge its portfolio back to Australian dollars. With approximately 50% of its holdings listed in the United States, returns for Australian investors are partly a function of USD/AUD exchange rate movements. This is not a minor footnote. A 5% move in the currency pair can materially alter a calendar-year return. IFRA, by contrast, hedges to AUD, a structural difference investors should account for when sizing positions.

How IFRA became the default infrastructure allocation for Australian advisers

VanEck’s IFRA (ASX: IFRA) manages approximately A$1.88-1.90 billion as at 18 May 2026. That figure is not accidental. It reflects years of systematic inclusion in adviser model portfolios across Australia, driven by a combination of broad diversification, low fees, and a reliable income stream.

IFRA holds approximately 150 positions spanning five infrastructure sub-categories:

- Electric utilities

- Toll roads (including Transurban Group as its largest individual holding, giving the fund an Australian anchor)

- Pipelines

- Airports

- Rail networks

Over 70% of the portfolio is exposed to US and Canadian listed companies, but the AUD currency hedge removes the foreign exchange volatility that income-focused investors cannot absorb in a core allocation. The fund’s management expense ratio of 0.20% p.a. makes it one of the cheapest infrastructure vehicles on the ASX.

ASIC’s exchange traded products framework governs the disclosure, licensing, and conduct obligations that apply to ASX-listed ETFs such as AINF and IFRA, establishing the regulatory baseline Australian retail investors can rely on when comparing product structures.

Morningstar Australia identified IFRA as “one of the primary vehicles local investors are using” for regulated utilities and transport infrastructure.

Performance has reinforced the adviser thesis. IFRA’s unit price stood at A$25.19 on the reporting day, up 1.2% on the session, with a year-to-date gain of approximately 8% and a 12-month return exceeding 16%. The forward dividend yield sits at nearly 3% over the next 12 months. For advisers constructing model portfolios that need both capital growth and income, those metrics explain why IFRA’s FUM continues to grow.

How the AI repricing changed the story for listed infrastructure

Listed infrastructure, as a category, refers to regulated or quasi-monopoly assets with long-duration cash flows: toll roads, utilities, pipelines, and grid operators. For years, these assets were valued primarily as bond proxies, offering steady yields that competed with fixed income for the defensive portion of investor portfolios.

The AI data-centre buildout has introduced a demand shock that is repricing this relationship. Hyperscaler combined AI capital expenditure, estimated at US$725 billion for the current calendar year according to Shaw and Partners’ James Gerrish, is pulling forward grid investment timelines by years. Between 70-75% of that combined capex is directed toward AI infrastructure specifically. CBRE estimates that non-energy infrastructure investments should amount to approximately 1% of global GDP, or US$11.5 trillion across sectors globally.

The physical bottlenecks in AI infrastructure, specifically power availability and energy storage rather than silicon supply, are the same constraints that will determine whether hyperscaler capex translates into sustained earnings growth for the grid operators and cooling equipment makers sitting inside both AINF and IFRA.

The distinction for investors evaluating AINF and IFRA is directness of exposure. IFRA benefits indirectly: its utilities and grid operators see rising load demand from data centres, which flows through to higher regulated earnings and asset-base growth. AINF benefits directly: its holdings are the equipment makers, cooling system providers, and power electronics companies physically building the data-centre supply chain.

| Characteristic | AINF | IFRA |

|---|---|---|

| Thesis type | Direct AI infrastructure | Indirect (utilities, grid operators) |

| MER | 0.57% p.a. | 0.20% p.a. |

| FUM | A$127.57M | ~A$1.88-1.90B |

| Holdings | ~31 | ~150 |

| Currency hedge | No | Yes (AUD) |

| Income yield | Not established | Nearly 3% forward |

| Typical portfolio role | Tactical thematic sleeve | Core or satellite income |

Morningstar Australia has framed this as a complementary pairing: IFRA as “steady ballast,” AINF as a concentrated thematic. Most investors would treat IFRA as a core or satellite allocation and AINF as a small tactical position.

Return profiles, entry points, and what an analyst is watching

The performance gap between the two funds tells the story of their different risk characters. AINF’s unit price stood at A$17.44 on the reporting day, down 2.5% in a single session, with a year-to-date gain of approximately 17% and a 2026-to-date return of approximately 20%. IFRA, on the same day, gained 1.2% to A$25.19, with a steadier 8% year-to-date return.

That single-day divergence, one fund down 2.5% while the other gained 1.2%, illustrates the volatility premium embedded in AINF’s concentrated structure.

AINF’s 12-month return trajectory, approximately 65% to its mid-May all-time high, reflects the same three macro forces that drove Asian tech names simultaneously: the AI chip demand surge, record hyperscaler capex commitments, and a broad repricing of the physical supply chain that connects semiconductor production to grid delivery.

Shaw and Partners’ James Gerrish has provided specific entry-point guidance on both funds. For AINF, the preferred entry sits below A$18, with additional buying interest on dips below A$17.

Analyst entry-point guidance on AINF: preferred entry below A$18, with additional buy interest on dips below A$17 (James Gerrish, Shaw and Partners).

For IFRA, Gerrish holds a bullish long position; the fund is included in the Market Matters Core ETF portfolio. For context, the SEMI ETF (ASX: SEMI), a semiconductor-focused alternative, has delivered a year-to-date gain of approximately 51% with a preferred entry point near A$31.

Three variables differentiate the risk and return profiles of AINF and IFRA:

- Concentration level: 31 holdings versus approximately 150

- Currency hedge status: unhedged (AINF) versus AUD-hedged (IFRA)

- Income yield: no established yield (AINF) versus nearly 3% forward (IFRA)

Firstlinks noted in February 2026 that newer, narrow AI funds show strong early flows but exhibit more sensitivity to AI newsflow, while infrastructure ETFs with larger FUM bases tend to deliver more stable performance.

These entry points and return figures represent one analyst’s view and are not financial advice. Past performance does not guarantee future results.

One thesis, two very different risk profiles, one portfolio decision

AINF and IFRA are not competitors. They are portfolio complements operating within the same structural thesis at different points on the risk spectrum. IFRA serves as a core or satellite income infrastructure holding, where AI demand provides a growth tailwind on top of regulated cash flows. AINF serves as a tactical thematic sleeve for investors with higher risk tolerance and a conviction view on the AI data-centre equipment cycle.

The fee differential reinforces this framing. AINF’s 0.57% MER versus IFRA’s 0.20% MER becomes meaningful over holding periods beyond three years, compounding alongside returns. Morningstar has noted AINF is “too new and too specialised” for a full star rating, while IFRA carries an established track record. Firstlinks cautions that most FUM in the AI infrastructure theme remains in broader vehicles like IFRA, with narrower AI thematics more sensitive to sentiment cycles.

Risks to monitor for each fund

AINF:

- Portfolio concentration across just 31 holdings amplifies single-stock risk

- Sensitivity to AI capex cycle slowdowns or hyperscaler spending deferrals

- No AUD currency hedge exposes Australian holders to USD/AUD movements

IFRA:

- AI demand growth may already be partially priced into regulated utility valuations

- Broad diversification across 150 holdings dilutes pure AI infrastructure upside

- Forward dividend yield of nearly 3% may compress if interest rate expectations shift

The infrastructure layer is not a trade, it is a multi-year build

The data-centre buildout driving both funds is measured in decades, not quarters. The University of Texas at Austin’s Energy Infrastructure of the Future project estimates the US energy system transition will require trillions of dollars of infrastructure investment by 2050, with AI-driven data-centre growth explicitly cited as a contributor. CBRE expects global power demand for data centres to more than double by 2030.

McKinsey projects AI data centres could account for 4-6% of total US electricity demand by 2030, up from less than 2% in 2023.

Investors considering AINF, IFRA, or both should verify current NAV, fees, and holdings via the official product pages before making any allocation decision. VanEck’s IFRA page is available at vaneck.com.au and Global X’s AINF page at globalxetfs.com.au.

For readers wanting to understand where semiconductor-focused ETFs sit alongside infrastructure plays in a layered AI portfolio, our dedicated guide to SEMI and GXAI walks through the full chip production chain exposure in SEMI, the broader hardware-to-software spectrum in GXAI, and the four material risks, including US-China export controls and Taiwan supply-chain concentration, that apply across all three fund types.

The structural demand is not a forecast; it is already visible in utility order books, hyperscaler capital budgets, and grid operator earnings. How investors choose to access it, through IFRA’s steady compounding, AINF’s concentrated thematic exposure, or a combination of both, should reflect their own risk tolerance, income requirements, and time horizon.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.