Why Your ETF Portfolio May Be Less Diversified Than You Think

51 mins ago

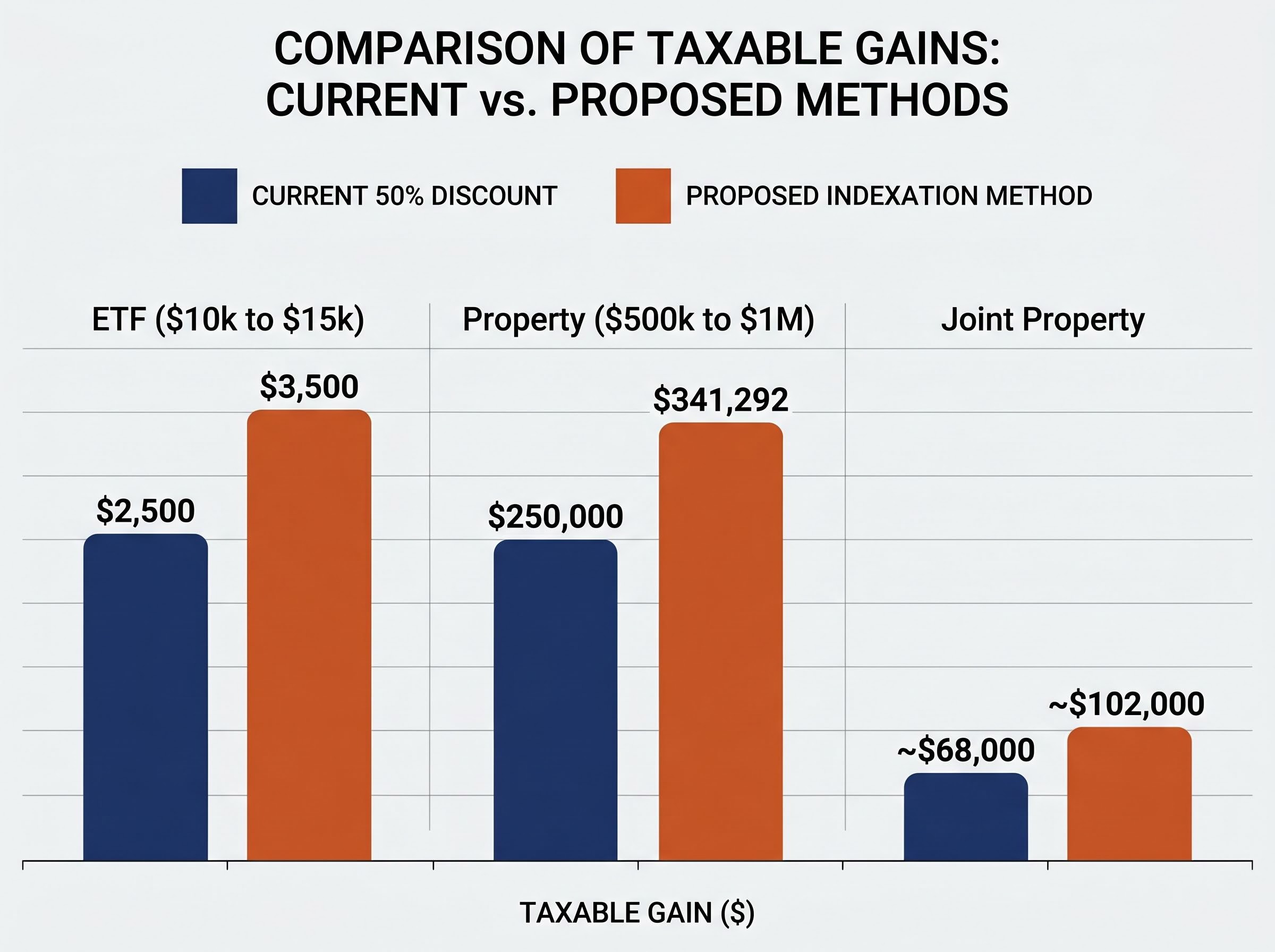

A $500,000 property purchased in 2015 and sold today generates roughly $250,000 in taxable gains under the current rules. Under the proposed capital gains tax framework announced in the 2026-27 Federal Budget, the same sale could produce around $341,000 in taxable gains, a 36% increase before any adjustment for the new minimum tax rate. The Australian Federal Budget on 12 May 2026 formally confirmed the replacement of the 50% CGT discount with an inflation-indexed cost base method and a 30% minimum tax floor on real gains. The measures are not yet legislated, but if passed, they take effect from 1 July 2027. That gives investors who act now roughly 13 months to reposition their portfolios under the rules they know.

This guide covers the four most practical strategies available before the proposed Australian CGT changes take hold: locking in grandfathered gains, redirecting contributions into superannuation, pivoting toward dividend-focused assets, and reconsidering the legal structures through which investments are held. Each lever carries distinct tradeoffs, and not every strategy suits every investor. What follows is a clear view of what each one does, who it suits, and how to sequence the planning.

Start with the arithmetic. Under the current 50% CGT discount, an investor who buys an asset and sells it at a profit after 12 months halves the taxable gain before adding it to their income. The proposed system replaces that flat discount with an inflation-adjusted cost base: the original purchase price is increased by cumulative inflation over the holding period, and only the gain above that adjusted figure is taxable. On top of that, a 30% minimum tax floor applies to the real gain, regardless of the investor’s marginal rate.

These are two separate impacts that compound each other. The indexation change narrows the discount for most investors (inflation rarely matches the 50% discount’s effect over medium-term holds). The 30% floor then ensures no investor pays less than 30% on whatever real gain remains.

The CGT indexation mechanics under the proposed rules are more layered than the headline CPI adjustment suggests, with the split-calculation obligation for assets crossing the 1 July 2027 boundary creating valuation complexity that no ATO worksheet currently addresses.

The 2026-27 Federal Budget tax reform documentation confirms that the proposed replacement of the 50% CGT discount operates independently of the 30% minimum floor, meaning both changes apply simultaneously to any qualifying disposal after 1 July 2027.

Consider the gap in dollar terms across three common scenarios:

| Scenario | Taxable gain (current 50% discount) | Taxable gain (proposed indexation method) |

|---|---|---|

| ETF: $10,000 growing to $15,000 over 5 years (15% cumulative inflation) | $2,500 | $3,500 |

| Property: $500,000 purchase doubling to $1,000,000 over 10 years | $250,000 | $341,292 |

| Joint property (combined tax at marginal rates) | ~$68,000 | ~$102,000 |

In the ETF example, the inflation-adjusted cost base rises to $11,500, producing $3,500 in taxable real gains and a minimum tax liability of $1,050 at the 30% floor.

For joint property owners, the proposed rules could increase the combined tax burden by approximately 50%, from around $68,000 to approximately $102,000, before any other planning is applied.

One point of clarity on legislative status: these measures were announced in the 2026-27 Federal Budget but have not yet been introduced to Parliament as a bill. Details could change before any law passes. Every strategy discussed below should be evaluated with that uncertainty in mind.

The proposed framework includes a genuine concession for existing investors. Gains accrued on assets held before 1 July 2027 retain eligibility for the existing 50% discount under grandfathering provisions. For any investor considering a disposal within the next 13 months, this creates a window to crystallise gains under the more favourable treatment.

The decision logic runs through four questions, roughly in this order:

If the answers favour action, the grandfathering window has real value. Triggering a disposal before July 2027 locks in the 50% discount on the full accumulated gain. Waiting means accepting the dual-calculation burden described below.

For investors who hold assets through the 1 July 2027 boundary and sell later, the total gain on a single asset must be apportioned between two periods. The pre-2027 portion (where the 50% discount applies) and the post-2027 portion (where the new indexation method applies) would each be calculated separately, likely based on the ratio of time held in each period or a market value at the boundary date.

No ATO formula or worksheet for this dual calculation exists as of mid-May 2026. This is expected given the recency of the Budget announcement. Investors should monitor ATO and Treasury publications as a bill progresses through Parliament. The administrative complexity of this dual obligation grows with every year an investor delays a decision, which is one reason the grandfathering window deserves attention now rather than after the bill is tabled.

The tradeoff is real, however. Triggering a disposal before July 2027 also triggers a current-year tax liability. The calculus depends on each investor’s marginal rate, holding period, and expectations for the asset’s future growth.

Superannuation is explicitly excluded from the proposed CGT changes. Gains on assets held inside super continue to be taxed at 15% in the accumulation phase, or zero in pension phase. Under a framework that reprices personal capital gains upward, super’s relative advantage over personal holdings widens materially.

Three contribution strategies deserve evaluation before 30 June 2026:

| Contribution type | 2025-26 cap | Tax on entry | Tax on earnings | Division 296 risk |

|---|---|---|---|---|

| Concessional | $30,000 | 15% | 15% (accumulation) / 0% (pension) | Balances above $3M |

| Non-concessional | $120,000 | 0% | 15% (accumulation) / 0% (pension) | Balances above $3M |

| Carry-forward concessional | Unused caps from prior 5 years | 15% | 15% (accumulation) / 0% (pension) | Balances above $3M |

The transfer balance cap (the ceiling on assets that can be moved into the fully tax-free pension phase) sits at $2 million, projected to index to $2.1 million. For couples, the combined figure exceeds $4 million in tax-free pension phase assets.

Super’s tax advantage is real but not unlimited. Division 296, which received Royal Assent on 13 March 2026 and applies from 1 July 2026, imposes additional tax on superannuation balances above $3 million. Investors above that threshold face a different calculus.

Pitcher Partners’ analysis of the Division 296 legislation confirms Royal Assent was received on 13 March 2026, with the additional tax on superannuation earnings for balances above $3 million applying from 1 July 2026, a start date that precedes the proposed CGT changes by a full year.

For investors below the $3 million threshold, the window before July 2027 represents a clear priority to redirect capital into the only major investment structure explicitly shielded from the proposed changes. The contribution caps are the practical constraint on how much can be moved, making them the most actionable figures in this planning exercise.

Carry-forward concessional contributions from the 2020-21 financial year expire permanently on 30 June 2026, meaning eligible members who have not yet deployed that unused cap space will lose it regardless of what CGT reform ultimately passes, making the super contribution deadline the most time-critical action on this list.

Dividend income is taxed at the investor’s marginal rate. It is entirely unaffected by the proposed CGT changes. No 30% minimum floor applies. No indexation method is involved. Under a framework that specifically reprices capital gains upward, the relative tax cost of earning returns through dividends versus capital appreciation shifts materially in favour of income.

A $1 million portfolio yielding 2-4% annually generates approximately $20,000-$40,000 in passive income, added to the investor’s marginal rate calculation. For Australian equities, franking credits often reduce the effective tax rate on that income well below the headline marginal rate.

Asset types typically associated with dividend income that Australian investors should consider include:

Building an ASX dividend income portfolio requires more than selecting high-yield stocks; payout ratio sustainability, franking coverage ratios, and ex-dividend date timing each determine whether the income stream holds up across market cycles and whether the franking credit refund mechanism delivers its full benefit.

The tradeoff deserves direct acknowledgement. Dividend-focused assets tend to generate lower capital appreciation. Investors still in the wealth accumulation phase who expect high portfolio growth will give up some compounding upside by rotating toward income holdings. For investors in or approaching retirement, however, the combination of franked dividend income and reduced need to sell assets (avoiding CGT events entirely) makes dividend-focused portfolios structurally more efficient under the proposed rules than they were under the 50% discount era.

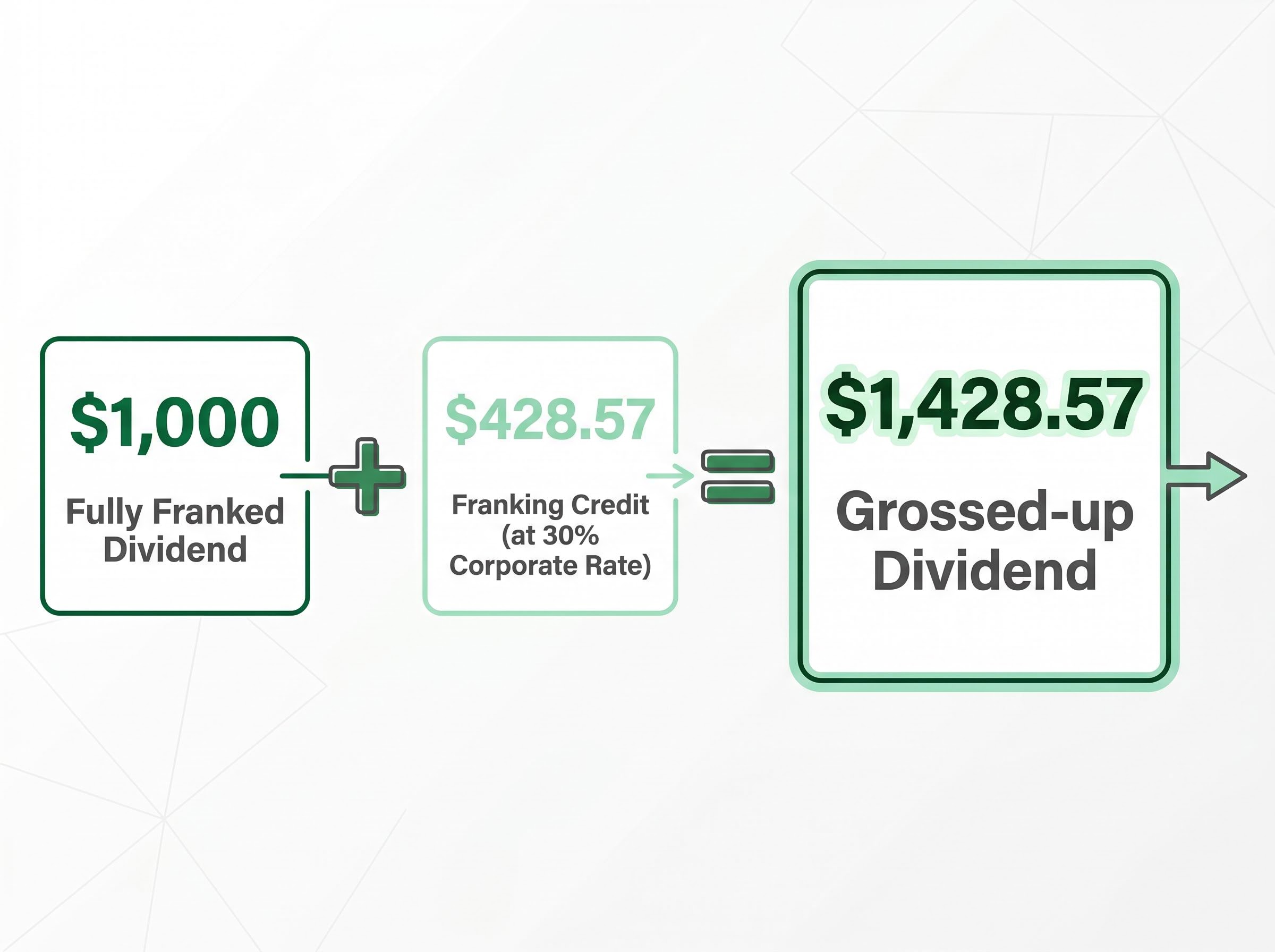

Australia’s imputation system works by attaching a credit to dividends for corporate tax already paid. When a company pays corporate tax at 25-30% (depending on whether it qualifies as a base-rate entity with aggregated turnover below $50 million), that tax is passed to the shareholder as a franking credit, reducing the investor’s personal tax liability by the credit amount.

A $1,000 fully franked dividend from a company paying the 30% corporate rate arrives with a $428.57 franking credit, meaning the investor’s grossed-up dividend is $1,428.57. Tax is calculated on the grossed-up amount at the investor’s marginal rate, then the $428.57 credit is subtracted. For investors in lower tax brackets, the credit may exceed the tax owed, resulting in a refund of the excess. This makes franked dividends particularly efficient for retirees or part-pension recipients.

The discretionary trust’s historical CGT advantage rests on one mechanism: the ability to distribute discounted capital gains to individual beneficiaries at their marginal rates, multiplying the benefit of the 50% discount across the family group. A trust holding growth assets could distribute gains to a low-income beneficiary, who would then apply the 50% discount and pay tax at a low marginal rate.

Under the proposed framework, that advantage is materially diminished. If the discount is replaced by inflation indexing and a 30% minimum floor applies to gains distributed through the trust, the primary planning rationale for holding growth assets inside a discretionary trust weakens significantly. The trust still distributes gains, but the gains themselves attract more tax before any distribution occurs.

The company structure offers a different pathway. Corporate tax at 25-30% is paid internally on profits, generating franking credits. Those credits are distributed to shareholders when profits are paid as dividends. The structure allows reinvestment and compounding within the entity before distribution, and the franking credits offset shareholders’ marginal tax on receipt.

| Attribute | Discretionary trust | Company |

|---|---|---|

| CGT treatment of gains | Distributed to beneficiaries (discount diminished under proposed rules) | Taxed at corporate rate internally |

| Distribution flexibility | High (discretion over beneficiaries) | Lower (dividends pro-rata to shareholdings) |

| Tax on retained earnings | Must distribute or face s99A risk | 25-30% corporate rate |

| Franking credit generation | No | Yes |

| Restructuring complexity | N/A (existing structure) | CGT and stamp duty triggered on transfer |

Restructuring from a trust to a company triggers CGT and potentially stamp duty in its own right. The cost of restructuring must be weighed against the projected tax saving over the investor’s holding horizon. No restructuring decision should be made without advice from a qualified tax adviser.

Post-Budget analysis from major tax law firms including Gilbert + Tobin, Hall & Wilcox, and Arnold Bloch Leibler is expected to address the trust-versus-company comparison in detail as the legislative process progresses. As of mid-May 2026, no verifiable dated analysis on this specific comparison has been published, given the recency of the Budget announcement. Division 7A risk for company structures (where retained profits accessed informally by shareholders may be treated as deemed dividends) also requires careful management.

Not every lever suits every investor, and not every lever carries the same urgency. The recommended planning sequence, ordered by deadline and decision reversibility:

Which lever matters most depends on the investor’s situation:

The proposed changes are not yet law. No bill has been introduced to Parliament, and the political process could amend or abandon these measures before Royal Assent. Strategic positioning should be proportionate to the probability of passage rather than treating the outcome as certain.

The proposed changes, if passed, will permanently alter the relative attractiveness of different investment structures and asset types. The grandfathering window is explicitly time-limited by the reform design. That said, the gap between a Budget announcement and enacted legislation is real, and investors who overcommit to repositioning before a bill even exists carry their own risk.

The proportionate response is to begin. Specific actions available this week:

The options narrow progressively as the July 2027 date approaches and the legislative process advances. Starting the conversation with a qualified tax adviser or financial planner now, before the bill is tabled, is the single highest-value action available.

Investors exploring the long-run compounding implications of the proposed changes will find our comprehensive walkthrough of low-turnover CGT strategies, which models the terminal wealth gap between old and new effective CGT rates on a $100,000 portfolio over 30 years and covers buy-only rebalancing, super structuring, and portfolio documentation steps specific to the pre-2027 transition window.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. The proposed CGT changes discussed are Budget measures that have not yet been legislated. These statements are speculative and subject to change based on market developments and the progress of the legislative process.

The 2026-27 Federal Budget proposes replacing the current 50% CGT discount with an inflation-indexed cost base method and introducing a 30% minimum tax floor on real capital gains, with both changes applying simultaneously to any qualifying disposal after 1 July 2027.

A property purchased for $500,000 in 2015 and sold after doubling in value could produce around $341,000 in taxable gains under the proposed rules, compared to roughly $250,000 under the current 50% discount, a 36% increase before any adjustment for the new minimum tax rate.

No, superannuation is explicitly excluded from the proposed CGT changes, with gains on assets held inside super continuing to be taxed at 15% in the accumulation phase or zero in the pension phase, making it the primary tax shelter investors should prioritise before July 2027.

The proposed framework includes a concession allowing gains accrued on assets held before 1 July 2027 to retain eligibility for the existing 50% CGT discount, meaning investors who dispose of assets before that date can crystallise gains under the more favourable current treatment.

The most urgent actions include maximising superannuation contributions before 30 June 2026 (when carry-forward caps from 2020-21 expire permanently), assessing whether to trigger disposals of large unrealised gains before July 2027, and scheduling a review with a qualified tax adviser before the bill is tabled.