Most Australian ETF investors have never checked whether their name actually appears on the share register for the units they own. The distinction between seeing a personal Holder Identification Number and seeing a platform’s nominee name is not cosmetic. It determines who the law recognises as the owner of those assets, what happens if a broker fails, and how tax reporting works at the end of every financial year.

With Australia’s ETF market now at a record A$346 billion in funds under management as of May 2026, more retail investors are choosing between brokerage platforms than ever before. Yet the most consequential difference between many of those platforms, how assets are actually held and who legally owns them, rarely features in comparison guides focused on fees or app design. What follows is a structural explanation of CHESS-sponsored and custodial brokerage arrangements, covering legal ownership, investor protection, tax reporting, and administrative burden, giving Australian ETF investors a clear framework for evaluating which model suits their situation.

The two ways a broker can hold your ETF units

Every time an Australian investor buys an ETF on the ASX, the units are settled through one of two ownership structures. The difference is not about the quality of the platform or the ETF itself. It is about whose name the law attaches to those holdings.

Investors who want to confirm what an ETF is before working through the ownership question will find that the unit trust structure sitting beneath every ASX-listed ETF is the same legal architecture that makes both CHESS sponsorship and custodial arrangements possible.

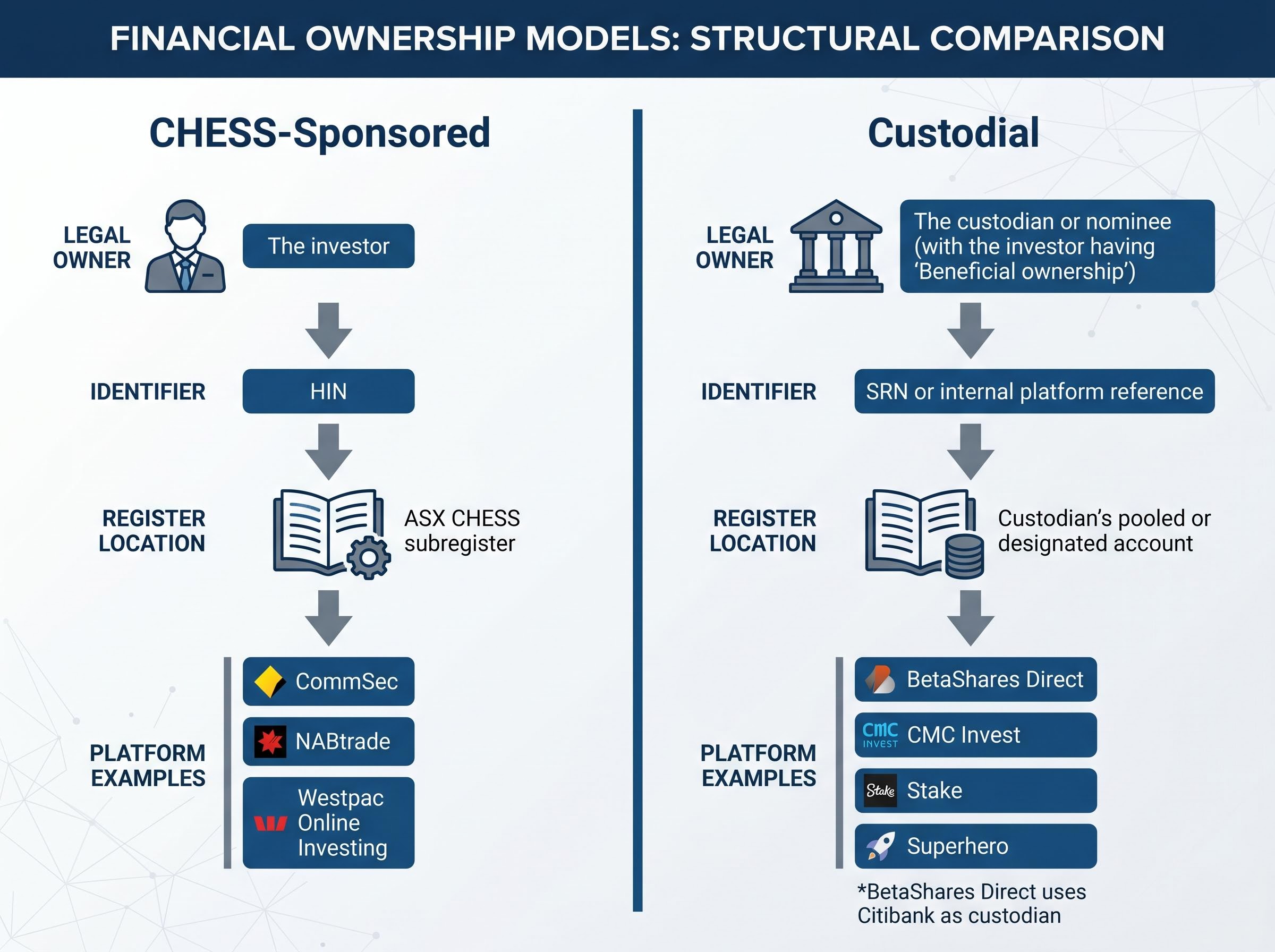

CHESS-sponsored: your name on the register

Under a CHESS-sponsored arrangement, the investor’s holdings are recorded directly on the ASX CHESS (Clearing House Electronic Subregister System) subregister. Each investor receives a unique Holder Identification Number (HIN), which identifies them as the legal owner of the securities on the ASX register.

This means an investor can verify their holdings independently through share registries such as Computershare or MUFG, without relying on the broker’s internal records.

Custodial: beneficial ownership via a third party

Under a custodial or nominee model, the platform or its appointed custodian is the legal holder of the securities. The investor holds beneficial ownership only, meaning they are entitled to the economic returns, but a third party’s name sits on the register.

Holdings are typically tracked via a Security Reference Number (SRN) or an internal platform reference within the custodian’s pooled or designated account. BetaShares Direct, for example, uses Citibank as its custodian, a large institutional entity separate from the broker itself.

Both models give the investor the same economic rights to returns and capital growth. The difference is in the nature of ownership itself.

| Feature | CHESS-Sponsored | Custodial |

|---|---|---|

| Legal Owner | The investor | The custodian or nominee |

| Investor Identifier | HIN (Holder Identification Number) | SRN or internal platform reference |

| Register Location | ASX CHESS subregister | Custodian’s pooled or designated account |

| Platform Examples | CommSec, NABtrade, Westpac Online Investing | BetaShares Direct, CMC Invest, Stake, Superhero |

When big ASX news breaks, our subscribers know first

What direct ownership actually changes in practice

The legal distinction matters. But so does the daily experience of living with each model across years of investing.

CHESS-sponsored accounts carry a layer of administrative overhead that custodial platforms eliminate. Under CHESS sponsorship, investors typically need to:

- Register individually with share registries such as Computershare or MUFG

- Supply a Tax File Number to each registry separately

- Manage dividend reinvestment preferences through external registry systems

- Receive physical mail from the ASX and registries for holding statements and corporate actions

CHESS-sponsored investors also gain access to certain corporate actions, such as share purchase plans and buybacks, that custodial investors may have more limited access to.

Under the custodial model, the administrative texture is different:

- A single app interface consolidates all holdings

- No external registry interactions are required

- Tax reporting, dividend management, and administration are handled within the platform

- The experience is, as BetaShares Direct describes it, designed for investors seeking a simple, fully digital, automated workflow

The economic rights to investments, including returns, capital growth, and distributions, are equivalent under both models. The difference is in administrative experience and the nature of legal title.

For investors who value operational simplicity, the custodial model removes meaningful friction. For those who want direct control and the ability to participate in corporate actions, CHESS sponsorship preserves those capabilities.

If the platform fails, what happens to your assets

This is the section most investors skip and most need. The risk is not binary, and the difference between the two models is more nuanced than many online comparisons suggest.

CHESS-sponsored and broker insolvency

Under CHESS sponsorship, the investor’s assets are held on the ASX register independently of the broker. If the broker becomes insolvent, the holdings do not form part of the broker’s estate. The investor’s HIN and on-register ownership survive the broker’s failure, and holdings can be transferred to another CHESS-sponsored broker.

The investor’s name on the ASX subregister is, in effect, independent of the broker’s financial health.

Custodial and broker insolvency

Under the custodial model, assets are held on trust by the custodian and are generally intended to be segregated from the platform’s own balance sheet. This means they should not automatically form part of an insolvent estate.

That said, the word “should” carries weight here. Administrative delays and documentation hurdles are realistic in a platform failure scenario. The custodian is a separate institutional entity (such as Citibank in the case of BetaShares Direct), which adds a layer of structural protection. But no recent Australian court decision has tested the recovery process in a mainstream custodial ETF brokerage context.

The ASIC client money provisions under the Corporations Act 2001 establish that client funds held in trust accounts must be segregated from a firm’s own assets, a requirement that underpins the structural protection custodial platforms rely on to keep investor holdings separate from the platform’s own balance sheet.

Custodial insolvency protection depends on the integrity of the trust structure and asset segregation arrangements. To date, no major Australian retail custodial brokerage failure has stress-tested this protection in practice.

ASIC has issued general warnings about platform failure risk, particularly for governance-deficient or scam-adjacent platforms, but these warnings do not specifically target mainstream custodial brokers operating under standard trust arrangements. The distinction between structural risk and practical risk is worth holding in mind: the custodial model is designed for protection, but the protection has not been tested under pressure in this specific context.

How custodial investing became the dominant model in Australian wealth management

Investors who instinctively distrust the custodial model may not realise that their own superannuation balance is almost certainly held the same way.

Australia’s superannuation system is estimated at approximately A$4.5 trillion in total assets, and the vast majority of those assets are held under custodial arrangements.

This is not a marginal or experimental structure. Custodial holding is the institutional standard in Australian wealth management, and it became so for three structural reasons:

- Operational scale. Institutional custodians such as major banks provide settlement, safekeeping, and corporate action processing infrastructure that individual share registries do not replicate at the same scale.

- Asset segregation by design. Custodial arrangements are built around trust structures that separate client assets from the custodian’s own balance sheet as a foundational design principle.

- Regulatory oversight of custodian entities. Custodians operating in Australia are subject to regulatory obligations governing how they hold and report on client assets.

The superannuation system’s broad custodial architecture has not produced systemic investor losses from custody failures. Custodial platforms such as BetaShares Direct (with Citibank as custodian) extend the same structural logic to individual ETF investors, offering the operational simplicity that the super system already demonstrates at scale.

Viewing custodial as inherently riskier than CHESS sponsorship misreads the institutional context. The question is not whether custodial works at scale; the question is whether the specific platform’s trust and segregation arrangements are sound.

Superannuation’s custodial architecture, which manages approximately A$4.5 trillion in member assets under the same trust and asset segregation principles described here, has generated sustained scrutiny over structural costs that sit outside standard fee disclosures, a parallel that retail ETF investors in custodial platforms would benefit from understanding.

Tax reporting, switching platforms, and what CHESS or custody means for your paperwork

The ownership model choice has downstream consequences that surface every financial year and every time an investor considers switching brokers.

Under a CHESS-sponsored arrangement, investors typically receive individual AMIT (Attribution Managed Investment Trust) statements from each share registry for each ETF holding. These must be obtained from registries such as Computershare or consolidated via third-party tax tools. The process can involve multiple logins, separate correspondence, and manual aggregation.

Custodial platforms often consolidate tax reporting into a single annual statement. Some, such as BetaShares Direct, pre-fill investment income data directly to myGov via the ATO, reducing the manual burden at tax time.

| Consideration | CHESS-Sponsored | Custodial |

|---|---|---|

| Tax Reporting Method | Individual AMIT statements from each registry | Consolidated statement; some platforms pre-fill to ATO |

| Switching Process | HIN transfer between CHESS-sponsored brokers | In-specie transfer required; potential CGT event |

| SMSF Suitability | Preferred by some trustees for on-register auditability | Not prohibited; platform-level records must meet compliance |

Transferring ETF holdings from a custodial platform to a CHESS-sponsored broker involves an in-specie transfer. This may trigger a CGT event depending on the timing and structure, and investors should assess the tax implications carefully before initiating a switch.

The ATO guidance on CGT and in-specie transfers confirms that moving units between custodial and CHESS-sponsored structures can constitute a CGT event, making the timing and structure of any platform switch a material tax consideration for investors with unrealised capital gains.

On the SMSF front, self-managed super fund trustees have specific record-keeping and compliance obligations under ATO rules. Custodial platforms are not prohibited for SMSFs, but some trustees prefer CHESS sponsorship for the direct auditability that on-register ownership provides. The suitability depends on the trustee’s compliance framework and auditor requirements.

The model choice is not irreversible. Most platforms allow transfers. But fees may apply, CGT implications must be assessed, and the administrative cost of switching compounds the longer the investor waits to make a deliberate decision.

How to choose between the two models based on what you actually need

The right model depends on what the investor actually values, not on which platform has the most polished marketing.

Investors who typically favour CHESS sponsorship

- Those who prioritise direct legal ownership and the ability to verify holdings on the ASX register

- Investors who want to participate in corporate actions such as share purchase plans and buybacks

- SMSF trustees who require on-register auditability for compliance purposes

- Investors comfortable managing multiple registry accounts and external correspondence

Investors who typically favour custodial platforms

- Digital-first investors who prefer a single consolidated app experience

- Dollar-cost averaging practitioners who benefit from automated, low-friction investing workflows

- Investors who prioritise consolidated tax reporting and ATO pre-fill functionality

- Those seeking low administrative overhead across a long-term buy-and-hold portfolio

Named CHESS-sponsored brokers include CommSec, NABtrade, Westpac Online Investing, and Morgans. Named custodial brokers include BetaShares Direct (with Citibank as custodian), CMC Invest, Stake, and Superhero. No major Australian broker has publicly switched between models since 2024, indicating structural stability in the market.

The model choice is not irreversible, but switching has tax implications. The decision is worth making consciously upfront rather than defaulting to whichever platform has the best app rating or lowest headline brokerage fee.

Total cost of ownership extends beyond the platform’s headline brokerage fee and includes the management expense ratio, bid-ask spreads, and the administrative overhead associated with the chosen ownership model, all of which compound silently across a long accumulation horizon.

Ownership model clarity is a foundation, not a footnote

The distinction between CHESS-sponsored and custodial ownership is one of the most consequential and least-discussed choices Australian ETF investors face. It deserves deliberate consideration.

The core trade-off is straightforward. CHESS sponsorship offers direct on-register legal ownership and register independence, at the cost of greater administrative complexity. Custodial platforms offer operational simplicity and consolidated reporting, at the cost of one layer of institutional dependency.

As Australia’s ETF market continues its record growth past A$346 billion, more investors will face this choice. Understanding the structural logic behind each model is the prerequisite for making it well.

Australian ETF market growth at a five-year compound annual rate above 26% has brought a new cohort of investors into platforms they may have chosen primarily on app design or headline brokerage fees, with the structural ownership question often unexamined until a platform failure or tax event makes it relevant.

A practical first step: check whether the current broker provides a HIN or an SRN. That single data point reveals which model is in use, and whether it aligns with the investor’s ownership preferences, tax situation, and long-term platform needs.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.