Goldman Sachs analyst Dominic Wilson issued a client note on 18 May 2026 warning that the tail risk of a renewed Middle East conflict or prolonged Strait of Hormuz closure remains inadequately priced into financial markets, even as equities have rebounded to cycle highs and the Iran ceasefire holds nominally in place. With Brent crude above $109 per barrel, the U.S. Energy Information Administration (EIA) treating the Strait as still effectively closed through late May, and AI-heavy indices including the Nasdaq, South Korean, and Taiwanese benchmarks trading near pre-conflict levels, a gap is opening between market surface calm and the underlying risk distribution. Goldman characterises that distribution as more balanced than markets are pricing. What follows unpacks what the underpricing warning means in practical terms: what re-escalation scenarios could do to oil prices and rate markets, why the AI equity rally is obscuring a geopolitical risk signal, and how to read the current calm without mistaking it for resolution.

Goldman’s warning: what “underpriced tail risk” actually means

The surface picture looks orderly. Equities sit at cycle highs. Oil is elevated but stable. A ceasefire nominally holds in the Gulf. For most market participants, this combination reads as a situation that has been priced and absorbed.

Goldman’s Dominic Wilson is arguing it has not. The core claim in the 18 May note is specific: the market-implied probability of a severe downside scenario, a ceasefire collapse, a full and prolonged Hormuz closure, or broader regional re-escalation, is lower than Goldman’s estimated actual probability of that scenario occurring. That gap between implied and estimated probability is what “underpriced tail risk” means.

Current oil prices illustrate the distinction. Brent settled near $109.26 on 17 May 2026; WTI settled near $105.42. Those levels reflect the ongoing supply disruption as the market’s base case. They do not reflect the additional, probability-weighted cost of a far worse outcome.

Goldman Sachs characterised the overall risk distribution as “more evenly balanced” following the asset price rebound, a framing that includes both an upside relief scenario and a downside tail that current prices are not adequately discounting.

The ceasefire compressed risk premia across asset classes. Wilson’s argument is that the severe downside scenario did not compress proportionately.

When big ASX news breaks, our subscribers know first

The ceasefire that did not resolve anything

The ceasefire was real, and so was the initial relief. Equities rallied. Risk premia compressed. The narrative shifted toward normalisation.

Then the operational details failed to follow. The EIA, in assumptions reported by Reuters on 12 May 2026, stated that it was treating the Strait of Hormuz as remaining shut through at least the end of May. Tanker traffic and shipping insurance markets continue to reflect disruption-level conditions rather than a return to pre-conflict flows. Brent above $109 and WTI above $105 corroborate the ongoing supply constraint in price terms.

The 57% surge in Brent crude from around $70 per barrel in late February 2026 to above $110 by mid-May reflects the near-total removal of Gulf supply from commercial markets, not a gradual tightening cycle, which is precisely why current prices encode an ongoing shock rather than a forward-looking risk premium.

Three indicators distinguish the current state from genuine resolution:

- The EIA’s operational assumptions treat the Hormuz closure as ongoing through late May, structurally inconsistent with a normalisation narrative

- Shipping insurance markets have not repriced to pre-disruption levels, signalling that underwriters assess physical transit risk as unresolved

- Oil prices remain $30-$40 above pre-conflict levels, reflecting an active supply shock rather than a fading one

The ceasefire is nominally in place but widely characterised as fragile, with ongoing proxy incidents and residual tensions reported through mid-May. A headline that reads “ceasefire holds” does not describe what is happening in the Strait.

Why oil above $100 does not mean the full risk is priced

The intuition is understandable: oil is already elevated, so surely the risk is in the price. The argument fails because current prices above $105-$110 reflect the ongoing supply disruption as the market’s base case. They represent what is already happening, not what could happen next.

Goldman’s note frames this asymmetry directly. A phased resumption of energy flows through the Strait could provide material relief to oil prices and rate markets currently priced in a notably hawkish manner. That is the upside scenario. The inverse, a full ceasefire collapse or prolonged total closure, is not symmetrically priced on the downside.

The transmission to rate markets is direct. The Federal Reserve and European Central Bank both held rates unchanged across their March-May 2026 meetings, with official communications referencing geopolitical tensions and energy price shocks as upside inflation risks. Goldman has revised its 2026 rate-cut outlook, projecting fewer reductions from developed and emerging market central banks than previously anticipated.

Saudi Aramco CEO Amin Nasser has warned that supply normalisation into 2027 is a plausible outcome, a timeline that places the oil-inflation-rates chain well outside the window that current Fed and ECB pause decisions were calibrated around.

The Federal Reserve April 2026 FOMC statement cited elevated inflation partly reflecting the increase in global energy prices and noted that developments in the Middle East were contributing to a high level of uncertainty about the economic outlook, providing the official basis for the Committee’s decision to hold rates unchanged.

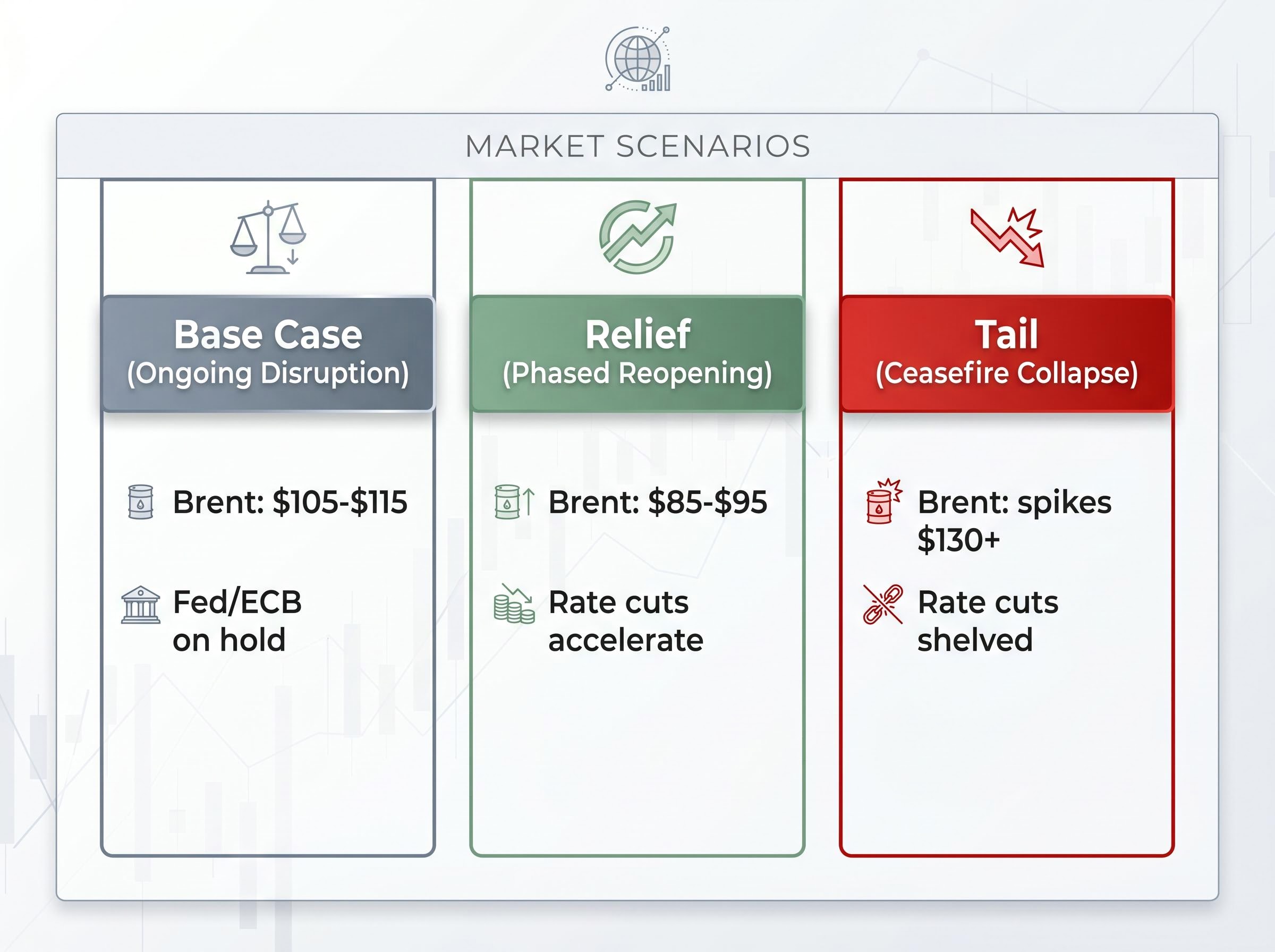

| Scenario | Oil price implication | Rate market impact | Equity exposure |

|---|---|---|---|

| Base case (ongoing disruption) | Brent holds $105-$115 range | Fed and ECB on hold; cuts delayed | Elevated energy input costs; AI leadership masks index stress |

| Relief (phased reopening) | Brent falls toward $85-$95 | Rate-cut timelines accelerate | Broad equity relief rally; rate-sensitive sectors benefit |

| Tail (ceasefire collapse) | Brent spikes above $130+ | Rate cuts shelved; inflation expectations re-anchor higher | Growth equities, EM semiconductors, and rate-sensitive assets face sharp repricing |

For investors in bonds, real estate, and growth equities, the oil-rates-geopolitics chain is the most direct transmission mechanism from a Hormuz tail scenario to portfolio damage.

What “underpriced risk” means: a plain-language guide for investors

Markets feel calm. Indices are at highs. The instinct is to read that calm as a signal that the worst is over. Goldman’s warning is that calm can also mean the market has stopped paying attention to a risk that has not gone away.

A risk premium is the additional return or price adjustment that markets demand to compensate for the possibility of a bad outcome. When a threat emerges, such as the Hormuz disruption earlier in 2026, risk premia spike. When conditions stabilise, even partially, those premia compress.

The sequence works like this:

- A geopolitical event occurs and risk premia spike across oil, equities, and credit markets

- A ceasefire or partial stabilisation compresses those premia as market participants re-weight toward the most probable (base case) outcome

- The probability of the severe tail scenario remains elevated, but its cost is no longer fully reflected in asset prices because the base case has absorbed the market’s attention

Goldman Sachs identified that the ceasefire enabled “substantial compression of risk premiums across multiple asset classes,” a compression that outpaced the actual reduction in tail-scenario probability.

This is the gap Wilson’s note targets. AI-concentrated indices including Korea, Taiwan, and Nasdaq have recovered to pre-conflict price levels. Emerging market assets have rallied broadly. The observable compression is real. Whether it is proportionate to the actual change in risk is the question Goldman is answering with “no.”

The AI equity rally and the risk signal it is obscuring

The Nasdaq, alongside Korean and Taiwanese semiconductor benchmarks, is trading at or near cycle highs as of May 2026. That strength feels like a vote of confidence. Goldman’s analysis suggests it is also distorting the signal investors use to gauge systemic risk.

The mechanism is specific. Divergence between winning and losing AI companies is driving elevated single-stock volatility. At the same time, that winner-loser dispersion is pushing stock-to-stock correlations to historically low levels. Low cross-stock correlation mechanically constrains broader index-level volatility, including the VIX.

The result is a market where:

- Single-stock volatility within the AI sector is elevated as capital concentrates in perceived winners

- Cross-stock correlation is suppressed because the dispersion dynamic reduces the tendency of stocks to move together

- Index-level volatility (VIX) reads as subdued, not because systemic risks have been resolved, but because the structural composition of the market is dampening the signal

Why VIX is not the right gauge right now

Goldman has also flagged a valuation layer on top of the geopolitical concern. Technology investment spending as a share of GDP has now exceeded the peaks recorded in the late 1990s, according to the firm’s May 2026 assessment. That spending concentration raises its own set of risks independent of the Hormuz situation.

Bank of America’s public framing offers a counterpoint, citing “AI and earnings strength outweighing geopolitical concerns” and “resilient market breadth supporting a broader uptrend.” The divergence between these two institutional readings is itself informative: Goldman sees a volatility signal structurally masked by AI dispersion; Bank of America sees earnings strength validating the rally.

Investors relying on VIX or broad index volatility as a proxy for systemic risk may be reading a structurally distorted signal in the current environment.

Investors wanting to understand why the AI-driven signal distortion runs deeper than a single market cycle will find our full explainer on AI forecasting blind spots, which examines how instruction-tuning and reinforcement learning from human feedback structurally bias large language models toward median outcomes, making them unreliable precisely in the tail-risk scenarios Goldman’s note is flagging.

The risk is not resolved, it is redistributed

Goldman’s characterisation of the risk distribution as “more evenly balanced” is a warning, not a reassurance. Balanced means both the upside scenario (a phased Hormuz reopening that eases oil prices and accelerates rate-cut timelines) and the downside tail (a ceasefire collapse that sends Brent above $130 and shelves monetary easing) are live outcomes. Current asset prices, Goldman argues, are not reflecting both sides symmetrically.

Bank of America (May 2026): “So far, global growth has absorbed the Hormuz oil shock… economic resilience and diversification should help investors navigate near-term uncertainty.”

That framing represents a genuine institutional counterpoint. Growth has proved resilient to date, and diversification has provided a degree of insulation. Whether resilience to date constitutes full pricing of forward-looking tail risk is where the two views diverge. Goldman’s revised 2026 rate-cut outlook, projecting fewer reductions than previously anticipated across developed and emerging markets, suggests the hawkish backdrop is not temporary.

The practical implication is not a call to panic. It is a prompt to stress-test. Investors in equities, rate-sensitive assets, and emerging markets with AI semiconductor exposure face a tail that is live, unresolved, and, by Goldman’s assessment, underpriced. Wilson’s note is an invitation to ask whether current portfolio positioning survives the scenario that markets have largely stopped pricing.

The EM semiconductor exposure concentrated in Korean and Taiwanese benchmarks carries a second, compounding layer of risk beyond geopolitics: an 18-24 month capex-to-revenue lag identified by Morningstar analyst Dennis Li, combined with Gartner’s estimate that only 20% of current AI agent pilots are scalable to production by 2027, means that the same indices Goldman flags as masking systemic risk are also priced for an AI revenue ramp that has not yet materialised.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. These statements reflect analyst assessments and are subject to change based on market developments and geopolitical conditions.