Australia’s largest listed companies now face a legal obligation to disclose climate risks within the same regulated framework that governs their financial accounts. The mandatory sustainability reporting regime under the Corporations Act took effect for Group 1 entities with financial years beginning on or after 1 January 2025, and many of those inaugural reports have already been lodged with ASIC. The regulator has flagged it will publish preliminary observations shortly to help entities with 30 June reporting dates prepare their own first submissions. At the same time, the Australian Government’s 2025-26 Budget announced a proposed consultation on reducing the reporting burden while preserving core requirements, adding a layer of uncertainty to an already complex compliance environment. What follows is an explanation of what mandatory sustainability reporting actually requires, how ASIC is overseeing it, what the burden-reduction proposal may or may not change, and how investors can read these new disclosures to separate credible climate management from compliance boilerplate.

Why Australia now has mandatory climate disclosures, not voluntary ones

For years, Australia’s largest companies produced voluntary climate reports aligned with the Task Force on Climate-related Financial Disclosures (TCFD) framework. CBA, BHP, ANZ, Westpac, and Rio Tinto all published versions. The problem was not that the reports did not exist. The problem was that no two of them were comparable.

Each company chose its own boundaries, its own scenario assumptions, and its own metrics. Investors attempting to compare climate risk exposure across a portfolio found themselves reading five different frameworks dressed in the same TCFD language. Aspirational targets sat alongside hard data without distinction. There was no enforcement mechanism when a disclosure was misleading or incomplete, and no assurance requirement to verify the numbers.

From voluntary TCFD to legally binding ASRS

The legislative response was direct. In 2024, Parliament passed amendments to the Corporations Act establishing a mandatory climate reporting regime built on Australian Sustainability Reporting Standards (ASRS 1 and ASRS 2), developed by the Australian Accounting Standards Board (AASB). These standards translate TCFD concepts, governance, strategy, risk management, and metrics and targets, into binding disclosure requirements. They are substantially aligned with the IFRS Sustainability Disclosure Standards issued by the International Sustainability Standards Board (ISSB), supporting international comparability.

The AASB’s ASRS 2 explanatory statement confirms that the Australian standards are substantially aligned with IFRS S2 issued by the ISSB, meaning Australian mandatory disclosures share a common architecture with the international framework that governs climate reporting in comparable markets.

Group 1 entities, those meeting large-entity thresholds, became the first required to report, with obligations applying from financial years beginning on or after 1 January 2025. The shift from the old voluntary regime to the new mandatory one rests on three differences:

- Legal enforceability: Disclosures now carry the same legal weight and penalty regime as audited financial statements under the Corporations Act.

- Standardised requirements: ASRS 1 and ASRS 2 prescribe what must be disclosed, removing the optionality that made voluntary reports incomparable.

- Assurance requirements: Mandatory reports must be subject to independent assurance, starting with limited assurance and increasing to reasonable (audit-level) assurance over time.

When big ASX news breaks, our subscribers know first

What Group 1 entities must actually disclose and who comes next

A mandatory sustainability report is not a corporate ESG brochure. It is a structured document organised around four disclosure pillars prescribed by ASRS 2. Understanding these pillars allows investors to navigate any report efficiently rather than reading it cover to cover.

| Disclosure pillar | What it requires | What investors look for |

|---|---|---|

| Governance | Board and management oversight structures for climate-related risks and opportunities | Named accountability, committee structures, board climate competency |

| Strategy | Climate-related risks and opportunities, scenario analysis, and impact on business model | Paris-aligned scenarios, credible transition plans, identified abatement levers |

| Risk management | Processes for identifying, assessing, and managing climate-related risks | Integration with enterprise risk management, not siloed climate risk processes |

| Metrics and targets | Greenhouse gas emissions (Scope 1, 2, and where applicable Scope 3), targets, and progress | Quantified interim milestones, methodological transparency, data quality indicators |

Group 1 entities must lodge these reports with ASIC as part of the annual report. Scope 1 and Scope 2 greenhouse gas emissions are mandatory. Scope 3 disclosures are required for most Group 1 entities, though transitional relief provisions apply to some categories.

Assurance is currently limited assurance over prescribed elements, with a legislative pathway toward reasonable assurance as the regime matures.

The regime expands beyond Group 1 on a phased basis:

- Group 1: Large listed and unlisted companies meeting prescribed size thresholds; reporting from financial years beginning on or after 1 January 2025.

- Group 2: Mid-sized entities enter in subsequent years, broadening the regime’s reach.

- Group 3: Smaller entities follow later, eventually extending mandatory reporting to a much wider population.

How to read a mandatory sustainability report as an investor

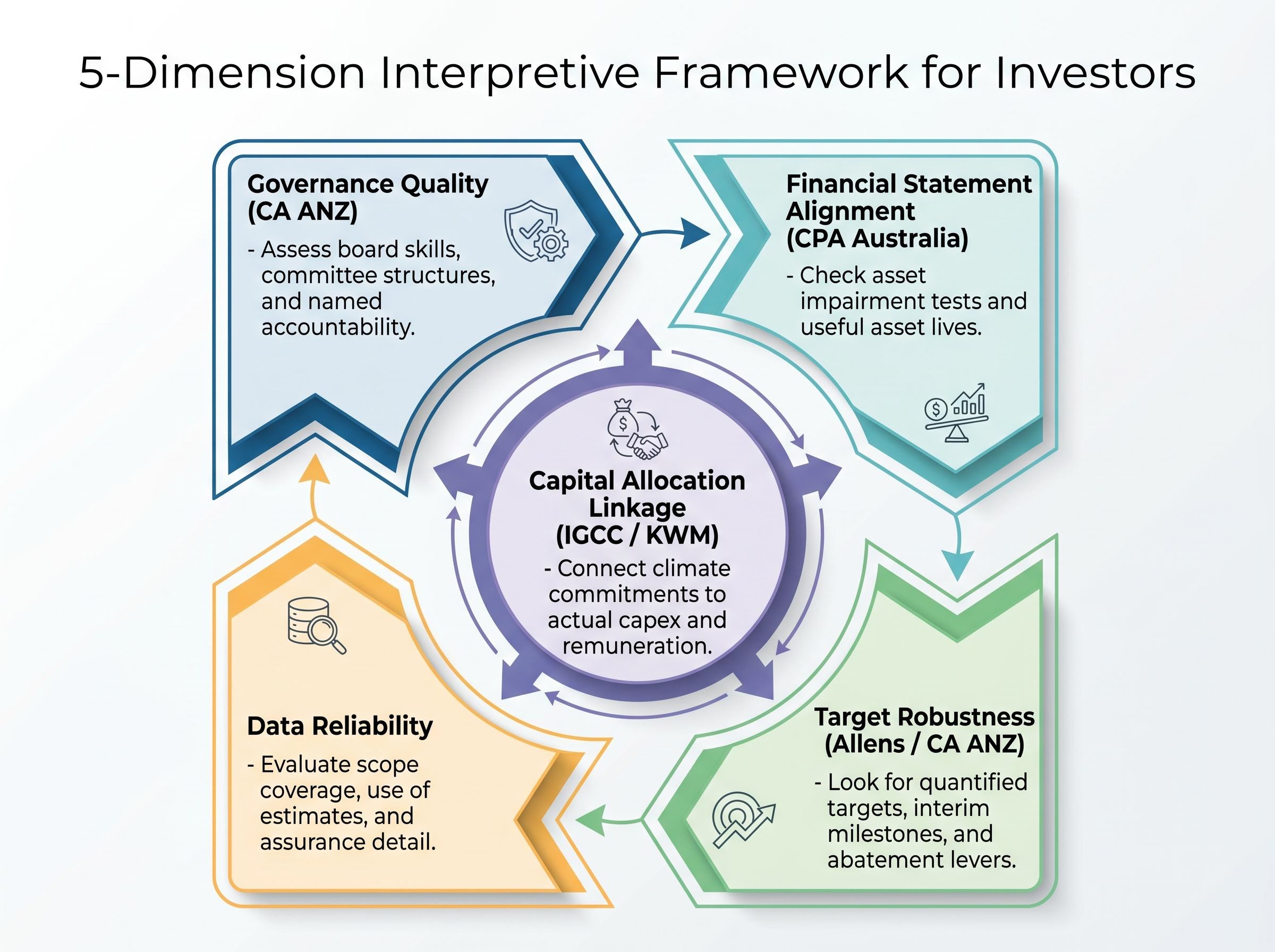

Knowing what the framework requires is one thing. Knowing how to use it is another. Across guidance published by CPA Australia, Chartered Accountants Australia and New Zealand (CA ANZ), the Investor Group on Climate Change (IGCC), King & Wood Mallesons (KWM), and Allens, a consistent interpretive framework emerges. It centres on five dimensions investors can apply to any report opened this reporting season:

- Governance quality: Assess board skills, committee structures, and named accountability mechanisms. CA ANZ guidance highlights these as indicators of genuine capacity to manage climate risk, not just stated intent.

- Alignment with financial statements: CPA Australia emphasises checking whether the climate narrative is consistent with accounting assumptions elsewhere in the annual report, particularly around asset impairment tests and useful asset lives.

- Robustness of targets and transition plans: Allens guidance advises looking for specificity: quantified targets, clear interim milestones, and identified abatement levers. CA ANZ adds that highly optimistic scenarios without credible transition plans should be discounted.

- Data reliability: Evaluate scope coverage, methodological transparency, use of estimates, and the detail provided on assurance. Variable data quality remains one of the most common weaknesses.

- Capital allocation linkage: IGCC and KWM guidance both stress the connection between climate commitments and actual capital expenditure and remuneration structures. A company that sets a net-zero target but allocates no capex toward it is telling investors two different stories.

Transition plan credibility has become the central analytical variable separating genuine decarbonisation commitments from aspirational statements, particularly as the scale of capital required for net-zero alignment has shifted climate tech from a speculative venture theme into a multi-trillion-dollar infrastructure investment cycle where capex allocation is observable and comparable.

Disclosures where the climate narrative is inconsistent with financial statement assumptions deserve specific scrutiny. Auditors review both documents. When the sustainability report describes stranded-asset risk but the financial statements assume unchanged asset lives, investors should ask why.

KWM advises treating the mandatory disclosure floor as a baseline and using peer comparison of scenario analysis and transition plans to identify outliers. The Principles for Responsible Investment (PRI) adds that investors should focus on forward-looking indicators, transition plans, capex, and governance quality, rather than historical emission trends alone.

ASIC’s oversight role and what its preliminary observations signal

ASIC is not waiting for companies to self-correct. The regulator has confirmed it will commence formal reviews of lodged Group 1 sustainability reports during 2026 and will publicly report its findings, mirroring the approach it uses in its financial-reporting surveillance programme. That public-reporting commitment matters. It means investors will have an independent quality signal on the disclosure landscape, not just company self-assessments.

The mandatory sustainability regime sits alongside Australia’s continuous disclosure obligations under the Corporations Act, a framework where ASIC has demonstrated it will pursue individual executives personally when disclosures are late, incomplete, or materially misleading.

ASIC’s preliminary observations on the first Group 1 reports are expected shortly. These are specifically designed to help entities with 30 June reporting dates prepare their own submissions, but they will also serve as an investor-facing benchmark: a first indication of where the regulator found weaknesses in the inaugural cohort.

KPMG analysis of ASIC’s 2025-26 surveillance program details how the regulator has structured its review of Group 1 sustainability reports, including the specific focus areas drawn from Regulatory Guide 280, providing preparers and investors with a practical map of where ASIC scrutiny is concentrated.

Separately, ASIC has engaged with the six largest audit firms regarding firm-wide responses to independence and conflict-of-interest findings from Report 817 (released 2025), and on readiness to assure climate disclosures under the new regime. Herbert Smith Freehills reported that ASIC held supervisory meetings with these firms to understand how they would apply assurance standards to sustainability reports.

What assurance actually covers in Year 1

The applicable assurance standards are ASAE 3000 (assurance engagements other than audits or reviews of historical financial information) and ASAE 3410 (assurance engagements on greenhouse gas statements), both overseen by the AUASB.

In the regime’s first phase, assurance is limited assurance over prescribed elements of the climate disclosure, not the full sustainability report. The practical meaning for investors:

- Limited assurance (current): The auditor confirms that nothing has come to their attention causing them to believe the disclosed information is materially misstated. This is a negative-assurance standard with a lower evidentiary bar.

- Reasonable assurance (future pathway): The auditor positively confirms accuracy, equivalent to an audit-level standard. This is legislated to phase in over time.

The distinction matters for how much weight investors place on specific numbers. Limited assurance provides a floor of credibility; it does not guarantee the precision investors are accustomed to in audited financial data.

The proposed burden-reduction consultation and what it may or may not change

The 2025-26 Australian Government Budget announced a proposed consultation on options to reduce the sustainability reporting burden while preserving core requirements. As of mid-May 2026, no consultation paper has been published. The Treasury climate-related financial reporting hub continues to focus on implementation of the enacted regime rather than hosting a separate burden-reduction process.

Reform themes discussed in legal commentary and Budget analysis include:

- Possible deferral or phasing adjustments for smaller entities (Groups 2 and 3)

- Simplification of scenario analysis or financed-emissions expectations for some entities

- Streamlining overlap between the Corporations Act regime and other ESG reporting frameworks

What is confirmed versus what remains under discussion:

- Confirmed: ASIC continues administering and enforcing the mandatory framework. Group 1 obligations remain fully in force. ASIC’s formal review programme proceeds as planned.

- Under discussion: Phasing adjustments for smaller entities, potential simplification of certain disclosure requirements, overlap reduction with other reporting regimes.

ASIC has explicitly stated: “ASIC’s administration of the mandatory climate reporting framework will continue regardless of any forthcoming reforms.”

Group 1 entities are not affected by any proposed phasing adjustment discussions, which focus on Groups 2 and 3. For investors analysing large ASX-listed companies, the disclosure framework governing those reports is stable and enforceable now.

What the first wave of mandatory reports reveals about corporate Australia’s climate readiness

The inaugural cohort of mandatory sustainability reports has begun to reveal a pattern. According to survey data from KPMG’s ASX Sustainability Reporting Survey 2023-24 and PwC’s 2024 ASX ESG Reporting Insights, governance disclosures and TCFD-style structural framing represent the strongest dimension across large reporters. High-level scenario analysis and qualitative risk descriptions are generally competent.

The gaps are more telling. Across multiple sources, the recurrent investor concerns cluster around the same weaknesses.

Scope 3 coverage and methodologies represent the most contested terrain in inaugural mandatory reports, and the Santos case illustrates the stakes concretely: more than 75% of the company’s total emissions footprint sits in a Scope 3 category carrying no binding net-zero commitment, a gap that mandatory assurance requirements will subject to higher evidentiary standards from year two onward.

| Areas of relative strength | Recurrent investor concerns |

|---|---|

| Governance disclosures and board oversight structures | Inconsistent or limited Scope 3 coverage and methodologies |

| TCFD-aligned report structuring | Insufficient linkage between climate targets and capex or remuneration |

| High-level scenario analysis and qualitative risk descriptions | Variable GHG data quality and reliance on estimates |

| Large ASX-listed entities leading on early compliance | Aspirational long-term commitments without quantified interim milestones |

PwC’s Financial and Sustainability Reporting Update for June 2026 contains initial observations on the inaugural mandatory year, confirming this pattern extends into the first legally required reports.

Named entity highlights: what early commentary says

CBA and ANZ face ongoing scrutiny on financed-emissions methodology and fossil-fuel portfolio alignment. Market Forces’ Big Four Banks Climate Scorecard 2024 reviews both banks’ disclosures against Paris-alignment benchmarks and argues they remain insufficiently stringent. IGCC commentary has raised similar concerns about the credibility of transition-plan commitments relative to continued fossil-fuel lending exposure.

BHP is considered at the more advanced end on scenario analysis depth. The Responsible Investment Association Australasia (RIAA) has referenced BHP’s Climate Transition Action Plan 2024 as relatively detailed on commodity-price and demand assumptions. The ongoing challenge centres on Scope 3 ambition, specifically whether medium-term targets are adequate given the scale of downstream emissions.

Rio Tinto has improved site-level decarbonisation disclosure, with more granular project-level detail. The Australasian Centre for Corporate Responsibility (ACCR) has published specific critiques of Rio Tinto’s reliance on emerging technologies and offsets to meet long-term targets, questioning whether these assumptions are sufficiently conservative.

Regulatory scrutiny is real, and so is the opportunity for investors who engage with these reports

Mandatory sustainability reporting is a structural change in the information available to Australian investors. It is not a temporary policy experiment. ASIC’s active surveillance programme and commitment to public reporting mean the quality floor is enforceable in a way voluntary disclosure never was.

The framework will evolve. The burden-reduction consultation may adjust requirements for smaller entities. Assurance standards will tighten as the regime matures toward reasonable assurance. But the core disclosures that Group 1 entities must produce, governance, strategy, risk management, and metrics, are stable and in force now.

Three specific actions investors can take this reporting season:

- Apply the five-dimension interpretive framework (governance quality, financial statement alignment, target robustness, data reliability, capital allocation linkage) to every mandatory sustainability report reviewed.

- Watch for ASIC’s preliminary observations on the first Group 1 reports, expected shortly, and use them as a calibration guide for assessing disclosure quality across the cohort.

- Compare across peers using the common ASRS disclosure structure, which for the first time allows direct comparison of scenario assumptions, emissions data, and transition plans across companies in the same sector.

Investors who engage seriously with mandatory disclosures now, while the regime is new and quality varies, are positioned to identify transition-risk outliers before the market fully prices them. PRI guidance reinforces this point: systematic use of these disclosures to assess portfolio exposure to transition and physical climate risks, with emphasis on forward-looking indicators, is where the analytical advantage sits.

Clean energy investment positioning is one concrete area where mandatory disclosures provide new analytical inputs: scenario analysis and transition plans in ASRS reports can now be benchmarked against the actual capital flows reshaping the domestic and global energy mix, giving investors a basis for assessing whether a company’s stated transition pathway is credible relative to the sector’s real-world investment trajectory.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.