Santos has cut its Scope 1 and 2 emissions by 42% since the 2019-20 baseline and survived a Federal Court greenwashing challenge in February 2026. Yet the appeal filed by the Australasian Centre for Corporate Responsibility (ACCR) remains live, and the emissions category that accounts for more than 75% of the company’s total footprint carries no binding net-zero target. Australian mandatory climate disclosure rules commenced on 1 January 2025, placing Scope 3 reporting inside the regulatory frame for large ASX-listed companies. For investors in Santos (ASX: STO) and its oil and gas peers, the question is no longer whether ESG risk exists but how to read it accurately given a fast-shifting legal and regulatory environment. This analysis unpacks the Scope 1, 2, and 3 emissions framework, explains what the ongoing ACCR appeal means for litigation exposure, assesses the company’s strategic response, and identifies what investors evaluating ASX energy stocks need to weigh right now.

Why Scope 3 is the number that Santos’ net-zero target leaves out

Scope 1 emissions are those a company produces directly from its own operations: gas processing, flaring, fugitive methane releases. Scope 2 covers the emissions generated by purchased electricity and energy used in those operations. Scope 3 captures everything else in the value chain, and for an oil and gas producer, that category is dominated by one thing: the combustion of the fuel that customers burn after buying it.

| Scope | Definition | Santos example | Net-zero target? |

|---|---|---|---|

| Scope 1 | Direct emissions from owned or controlled sources | Gas processing, flaring, fugitive methane at operated facilities | Yes: net-zero by 2040 |

| Scope 2 | Indirect emissions from purchased energy | Electricity consumed at processing plants and offices | Yes: net-zero by 2050 |

| Scope 3 | All other value chain emissions (upstream and downstream) | Customers burning the natural gas and oil Santos sells | No binding reduction target |

How this plays out for Santos specifically

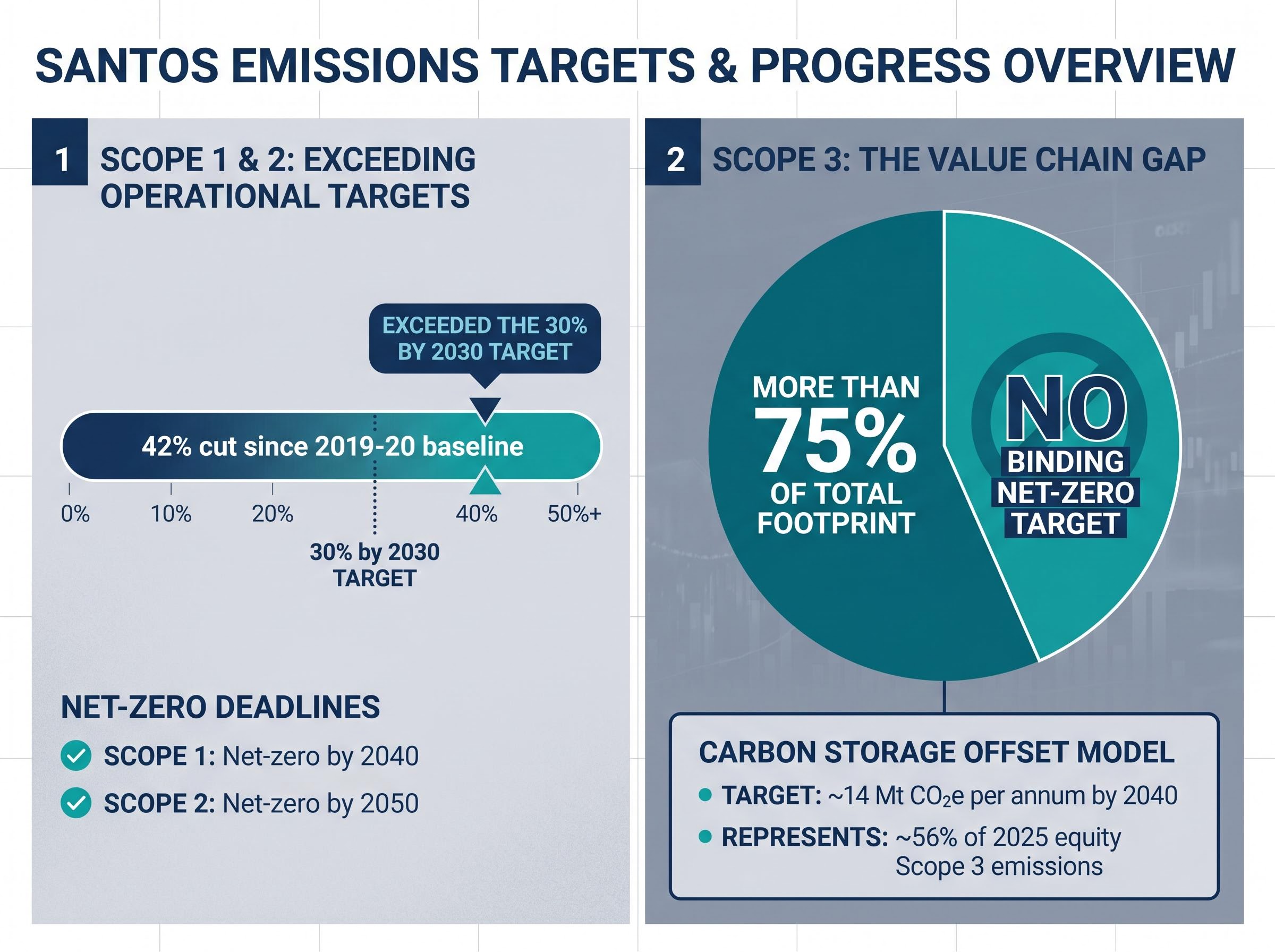

Santos has already exceeded its 2030 Scope 1 and 2 reduction target of 30%, delivering a 42% cut from the 2019-20 baseline. Its 2023 Scope 3 materiality assessment confirmed four material categories under its own framework. Yet the largest single emissions category, the one representing more than 75% of the total footprint, sits outside any binding net-zero commitment.

The distinction matters structurally. Scope 1 and 2 emissions are things Santos can engineer away through operational changes, electrification, and carbon capture at its own facilities. Scope 3 emissions are generated by customers, utilities, and end-users who burn the product Santos sells. Investors who read the headline net-zero commitment without understanding this exclusion are working with an incomplete picture of the company’s decarbonisation trajectory.

When big ASX news breaks, our subscribers know first

The ACCR greenwashing case: what the court decided, and what remains unresolved

The Federal Court dismissed all ACCR claims against Santos on 17 February 2026. The court found that Santos’ disclosures at its 2021 Investor Day Presentation and Climate Change Report, including representations about carbon capture and storage (CCS) reliance, blue hydrogen, and Scope 3 emissions from natural gas consumption, were not legally misleading.

That ruling lasted exactly one month as a standalone data point. ACCR filed a Notice of Appeal on 17 March 2026 (some sources cite 19 March). As of May 2026, the appeal remains unresolved.

- ACCR claim filed: Allegations of misleading and deceptive conduct regarding Santos’ climate disclosures

- 2021 Investor Day Presentation: The specific disclosures at issue, covering CCS reliance, blue hydrogen, and Scope 3 representations

- 17 February 2026: Federal Court dismisses all ACCR claims

- 17 March 2026: ACCR files Notice of Appeal

- May 2026: Appeal ongoing, no resolution reported; no ASIC enforcement actions or penalties against Santos

Law firms Clayton Utz and White & Case characterised the dismissal as positive for governance and investor confidence. Clifford Chance noted broader implications for corporate climate disclosure practice. These assessments predate the appeal filing.

The court found that Santos’ disclosures were not legally misleading. It did not validate CCS and blue hydrogen as commercially certain pathways. The distinction between legal sufficiency and substantive credibility is the gap that the appeal keeps open.

For investors, the appeal means the February ruling cannot be treated as a definitive reduction in litigation risk. The case retains the potential to set binding precedent on how Australian courts interpret climate-related disclosures, a matter relevant to every ASX-listed energy company.

Santos’ strategic response: the carbon storage offset model

Santos’ approach to Scope 3 is not a reduction target. It is a commercial carbon storage target: building and operating a business capable of storing approximately 14 Mt of gross third-party CO2 equivalent per annum by 2040. According to Santos’ Climate Transition Action Plan, that figure represents approximately 56% of 2025 equity Scope 3 emissions.

Carbon storage target: approximately 14 Mt gross third-party CO2e per annum by 2040, representing approximately 56% of 2025 equity Scope 3 emissions.

The model depends on CCS achieving commercial viability at scale, and on customers and suppliers participating in CO2 storage arrangements including CCS for blue hydrogen. Santos frames this within a three-horizon strategic roadmap:

- Horizon 1: Backfill and sustain existing production to generate cash flow

- Horizon 2: Decarbonise operations (the Scope 1 and 2 targets sit here)

- Horizon 3: Develop clean fuels, including blue hydrogen and CCS at commercial scale

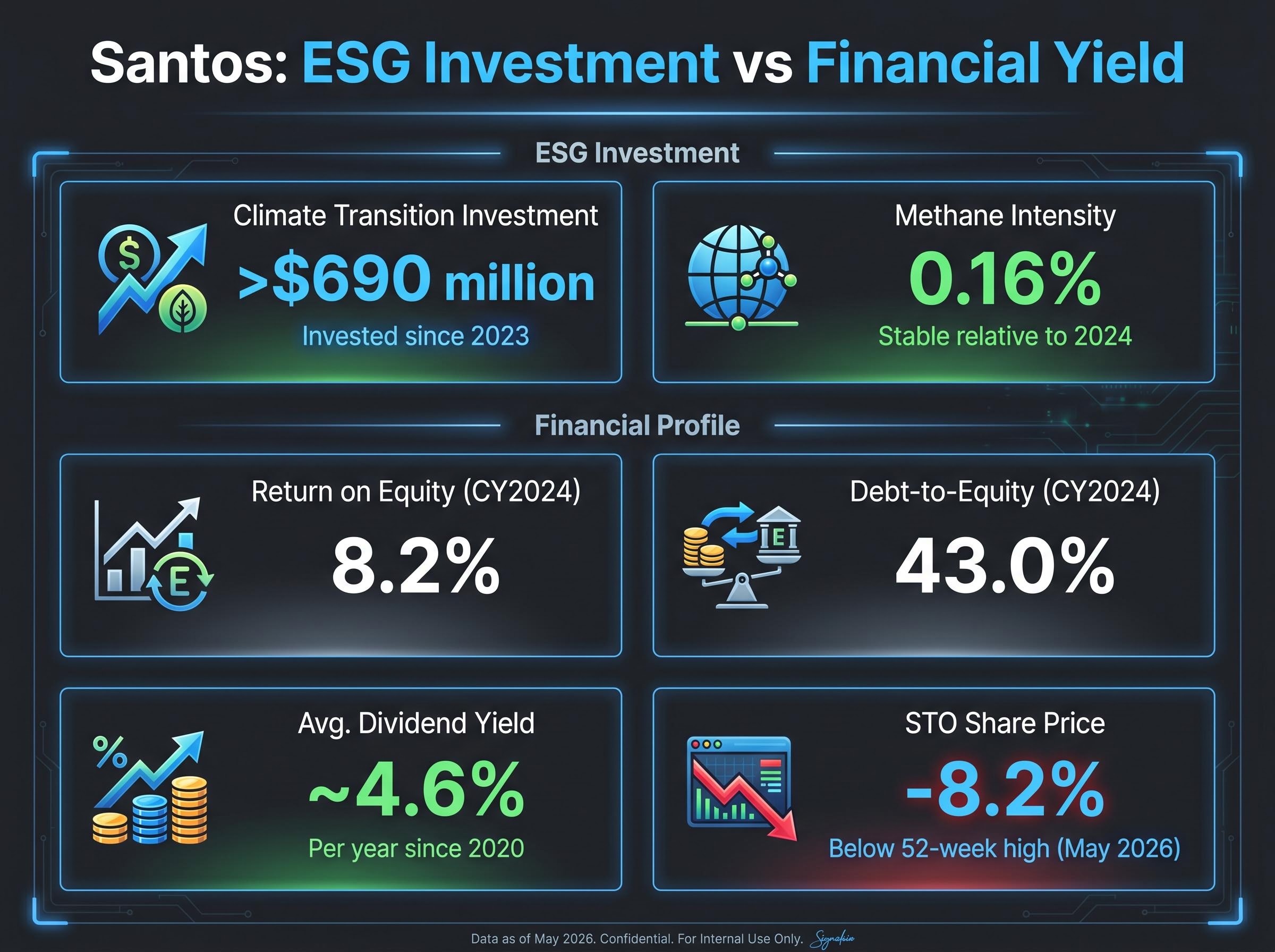

Since 2023, Santos has invested over $690 million in the Climate Transition Action Plan. Methane intensity has held at 0.16%, stable relative to 2024. Asset-level decarbonisation plans were developed in 2024, and supplier and customer engagement for data collection was initiated the same year.

Whether this constitutes genuine decarbonisation or a structural credibility gap is the central ESG judgement investors need to make. The offset model does not reduce the volume of fossil fuels sold; it proposes to counterbalance downstream emissions through storage. The commercial viability of that counterbalance at the stated scale remains unproven.

Large-scale CO2 sequestration projects are already progressing outside Australia, with Worley securing detailed engineering work on QatarEnergy’s carbon storage facility targeting 4.3 million metric tonnes of permanent CO2 storage per annum, a real-world data point against which Santos’ 14 Mt by 2040 commercial target can be calibrated.

Australia’s mandatory climate disclosure rules and what they mean for Scope 3

Australia’s mandatory climate disclosure regime commenced on 1 January 2025 under the Treasury Laws Amendment (Financial Market Infrastructure and Other Measures) Act 2024. Group 1 entities, which include large ASX-listed companies, must comply for financial years beginning on or after that date.

The regime requires disclosures across all three emissions scopes, aligned with Australian Sustainability Reporting Standards (ASRS), which are based on International Sustainability Standards Board (ISSB) standards. Key disclosure obligations include:

- Scope 1 emissions reporting

- Scope 2 emissions reporting

- Scope 3 emissions reporting (phased)

- ASRS alignment with ISSB-based standards

- Limited assurance on Scope 3 beginning in year two of the regime

No significant amendments to the disclosure regime or new ASIC enforcement actions related to Scope 3 have been publicly detailed as of May 2026.

ASX continuous disclosure obligations now attach liability at the point of internal awareness rather than at formal announcement, a standard confirmed by the Federal Court’s April 2026 penalty against Electro Optic Systems, and the same evidentiary logic is increasingly being applied to climate-related disclosures as ASIC’s greenwashing surveillance intensifies.

What phased Scope 3 assurance means in practice

Year two of the mandatory regime introduces limited assurance on Scope 3 figures for the first time. This means the 2026 reporting year is when external scrutiny of reported Scope 3 data materially increases. Companies will face higher evidentiary standards for the figures they disclose, and any material gaps between stated targets and actual emissions measurement will become harder to defend.

Santos’ 2023 Scope 3 materiality assessment and 2024 supplier engagement position it ahead of some peers on the disclosure curve. That head start has value, but it does not exempt the company from the same assurance standards that will apply across the sector. Scope 3 shifts from a voluntary framing exercise to a hard compliance variable once external assurance commences.

ASIC’s final sustainability reporting guidance, published on 31 March 2025, confirmed that Scope 3 estimation methodologies are permissible during a transition period, but also set the evidentiary standard that companies will be held to once limited assurance commences in year two of the regime.

Woodside and the sector pattern: Santos is not an isolated case

In April 2026, the Federal Court dismissed by consent a Greenpeace lawsuit against Woodside Energy alleging misleading climate and emissions strategy claims, including Scope 3 representations. The case was resolved without admission of liability.

| Company | Case type | Scope 3 allegations | Outcome | Current status (May 2026) |

|---|---|---|---|---|

| Santos | Misleading conduct (contested) | Scope 3 representations, CCS reliance, blue hydrogen | Dismissed 17 February 2026 | ACCR appeal filed, ongoing |

| Woodside | Misleading conduct (by consent) | Climate strategy and Scope 3 emissions claims | Dismissed by consent, April 2026 | Resolved, no admission of liability |

Two dismissals, one contested and one by consent, may deter future similar claims. They do not resolve the underlying substantive questions about Scope 3 credibility that animated both cases. ASIC maintains ongoing greenwashing surveillance across the sector as of May 2026, with no sector-wide enforcement actions detailed. Investors evaluating any ASX oil and gas holding should treat Scope 3 litigation exposure as a sector-level feature, not a company-specific anomaly.

The next major ASX story will hit our subscribers first

How to read Santos’ ESG risk as an investor right now

Santos’ ESG risk picture splits into two distinct layers. On one side, the company’s Scope 1 and 2 progress is materially ahead of its own targets, having already achieved a 42% reduction against a 30% goal. This reduces near-term regulatory and reputational risk on operational emissions.

On the other side, the Scope 3 position remains structurally unresolved. The carbon storage offset model is ambitious but unproven at scale, the ACCR appeal keeps litigation risk alive, and mandatory Scope 3 assurance is approaching. These are medium-term risks that do not collapse neatly into a buy-or-avoid signal.

The financial context sits alongside this ESG assessment. Santos reported a return on equity of 8.2% in CY2024, below the 10% threshold often used as a blue-chip benchmark. Its debt-to-equity ratio stood at 43.0% in CY2024, and its average annual dividend yield has been approximately 4.6% per year since 2020. The STO share price sits 8.2% below its 52-week high as of May 2026.

ISS and ACSI-aligned institutional investors have maintained cautious positions pending the ACCR appeal outcome, with ESG-focused funds highlighting persistent litigation risk as a factor in their assessments.

Rather than a binary verdict, investors monitoring Santos’ ESG exposure should track five specific variables:

- ACCR appeal outcome: The single most consequential near-term event for litigation risk and potential precedent

- Year-two Scope 3 assurance trigger: When external scrutiny of reported Scope 3 figures commences under the mandatory regime

- Carbon storage target progress: Whether Santos demonstrates credible commercial progress toward the 14 Mt by 2040 target

- CCS commercial proof points: Any evidence that carbon capture and storage is scaling toward viability at the levels Santos’ strategy requires

- ASIC enforcement developments: Any sector-wide or Santos-specific regulatory action on climate-related disclosures

The Scope 3 question will define how Australian energy stocks are valued through the decade

Santos sits at the intersection of three live pressures: an active litigation appeal with precedent-setting potential, a mandatory disclosure regime entering its assurance phase, and a sector-wide pattern of Scope 3 scrutiny that shows no sign of receding. The February court ruling established that Santos’ disclosures were legally sufficient. Whether the company’s decarbonisation pathway is substantively credible is a separate question, and it is the one that investors, regulators, and assurance providers will continue to test.

Clean energy investment in Australia reached a record $12.7 billion in 2024 before slumping roughly 20% in 2025 due to grid connection bottlenecks rather than deteriorating economics, a pattern that shapes the competitive landscape Santos navigates as it positions blue hydrogen and CCS as its own Horizon 3 revenue streams.

Readers applying this framework to their own ASX energy holdings should review Santos’ Climate Transition Action Plan documents and the ASRS Scope 3 disclosure guidance issued under the mandatory regime.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.