KB Securities analyst Jeff Kim has assigned SK Hynix a price target of 3,000,000 won and upgraded Samsung Electronics to Buy with a 450,000-won target, framing AI infrastructure investment not as a capital expenditure cycle but as a race for platform dominance that could reshape the global economy. The note, published in May 2026, arrives as SK Hynix trades near 1,835,000 KRW and Samsung near 270,500 KRW, meaning the bull case implies substantial upside even from dramatically re-rated starting points. KB’s core claim: new memory production lines will not reach mass production until after 2027, creating what the firm calls a “zero-supply era” for the industry. What follows unpacks the specific analytical pillars behind that thesis, what the data supports, where it carries genuine risk, and what a business model shift in memory means for how investors should evaluate AI memory stocks.

Why KB Securities sees a structural supply void forming after 2027

The boldest claim in Jeff Kim’s note is not a price target. It is a supply forecast: new memory production lines will not reach mass production until after 2027, leaving the industry in a structural supply void rather than a temporary tightness.

KB Securities frames hyperscaler spending not as a capital expenditure competition but as a “race for platform dominance,” a distinction that redefines how demand should be modelled for memory producers.

That framing matters because it implies demand is not cyclical. If hyperscalers are building for platform lock-in rather than capacity replacement, their purchasing commitments extend further and contract less sharply in downturns. KB’s note estimates AI token consumption at major cloud platforms will roughly triple within six months and reach approximately seven times current levels year-over-year. The three pillars supporting the thesis are:

- AI data centre operators currently account for approximately 70% of total memory shipments, anchoring demand concentration

- New production lines are not expected to reach mass production until after 2027, creating a multi-year supply gap

- AI token consumption growth at major cloud platforms is projected to triple within six months and reach roughly seven times current levels on a year-over-year basis

KB raised its SK Hynix price target from 2,800,000 won to 3,000,000 won, maintaining a Buy rating, while upgrading Samsung Electronics to Buy at 450,000 won. The question is whether the mechanism behind the supply void holds up under scrutiny.

When big ASX news breaks, our subscribers know first

Reading the hyperscaler capex numbers behind the demand thesis

The demand side of KB’s thesis rests on a specific trajectory: hyperscaler AI infrastructure spending accelerating through 2026 and 2027 at a pace that overwhelms available memory capacity. The quarterly disclosures from the four largest U.S. cloud operators tell part of that story.

Alphabet reported Q1 2025 capital expenditure of $12.0 billion, with management indicating full-year 2025 capex would be “significantly higher” than 2024. Amazon spent $14.7 billion in Q1 2025, guiding for a “meaningful” increase across the year. Microsoft posted $14.0 billion in Q3 FY2025 (quarter ended 31 March 2025), reiterating expectations for “elevated” spending over several years. Meta Platforms raised its 2025 capex outlook to $35-40 billion and flagged continued growth into 2026.

| Company | Most Recent Quarterly Capex | Forward Guidance Language |

|---|---|---|

| Alphabet | $12.0B (Q1 2025) | “Significantly higher” full-year 2025 |

| Amazon | $14.7B (Q1 2025) | “Meaningful” increase in 2025 |

| Microsoft | $14.0B (Q3 FY2025) | “Elevated” multi-year spending |

| Meta | $35-40B (2025 full-year outlook) | 2026 growth flagged |

What companies disclosed versus what analysts project

None of these companies publicly commits to a specific combined 2026 or 2027 aggregate capex figure. KB Securities models a combined $725 billion in capex from four major U.S. cloud operators in 2026, representing 77% year-over-year growth, crossing $1 trillion in 2027. Those figures are analyst projections, not company guidance.

The demand side of the thesis is anchored by hyperscaler capex commitments that are now publicly documented quarter by quarter, with Amazon, Microsoft, Alphabet, and Meta collectively spending $130 billion in Q1 2026 alone before any full-year guidance figure is applied.

The distinction matters for conviction. The multi-year, explicitly forward-looking language from each CFO independently supports a sustained demand thesis. But the precise scale of the acceleration, and the revenue it implies for memory producers, depends on KB’s modelling assumptions rather than confirmed corporate commitments.

HBM supply constraints and the packaging bottleneck most investors miss

High Bandwidth Memory (HBM) is a specialised form of DRAM where multiple memory chips are stacked vertically and connected using tiny vertical channels called through-silicon vias (TSVs). This stacking allows far more data to move between memory and processors simultaneously, which is why AI chips from NVIDIA and AMD depend on it. The supply economics of HBM are fundamentally different from standard DRAM because production faces three compounding constraints, not one:

- DRAM die capacity: Leading-edge DRAM wafer starts are finite, and HBM consumes more die area per gigabyte than conventional modules

- TSV packaging complexity: Stacking eight or twelve DRAM layers with TSV interconnects requires precision manufacturing with lower yields than standard packaging

- CoWoS and OSAT advanced packaging capacity: The final integration step, where HBM modules are mounted alongside GPU dies on an advanced substrate, remains the binding bottleneck

According to Yole Group, HBM demand grew at more than 100% CAGR from 2023 to 2025, a pace that has consistently outstripped capacity additions across all three constraint layers.

TrendForce (reporting in February 2025) projected HBM supply would remain tight through at least 2025, with 2026 characterised as “tight but gradually improving.” TSMC has reported CoWoS packaging yields exceeding 98%, but yield is not the constraint; total available packaging capacity is. Even with high yields, throughput expansion takes years.

Who is adding supply, and how fast

Micron has stated it is sold out of HBM capacity through at least 2025 under long-term agreements, with incremental HBM3E output targeted for 2025-2026 from its Hiroshima fab and U.S. facilities. Samsung is expanding HBM3E and HBM4 lines across its Korean DRAM fabs, with progressive capacity additions expected through 2025-2027. Industry commentary generally frames Samsung as narrowing the gap with SK Hynix in HBM3E, with potential for share gains when HBM4 ramps.

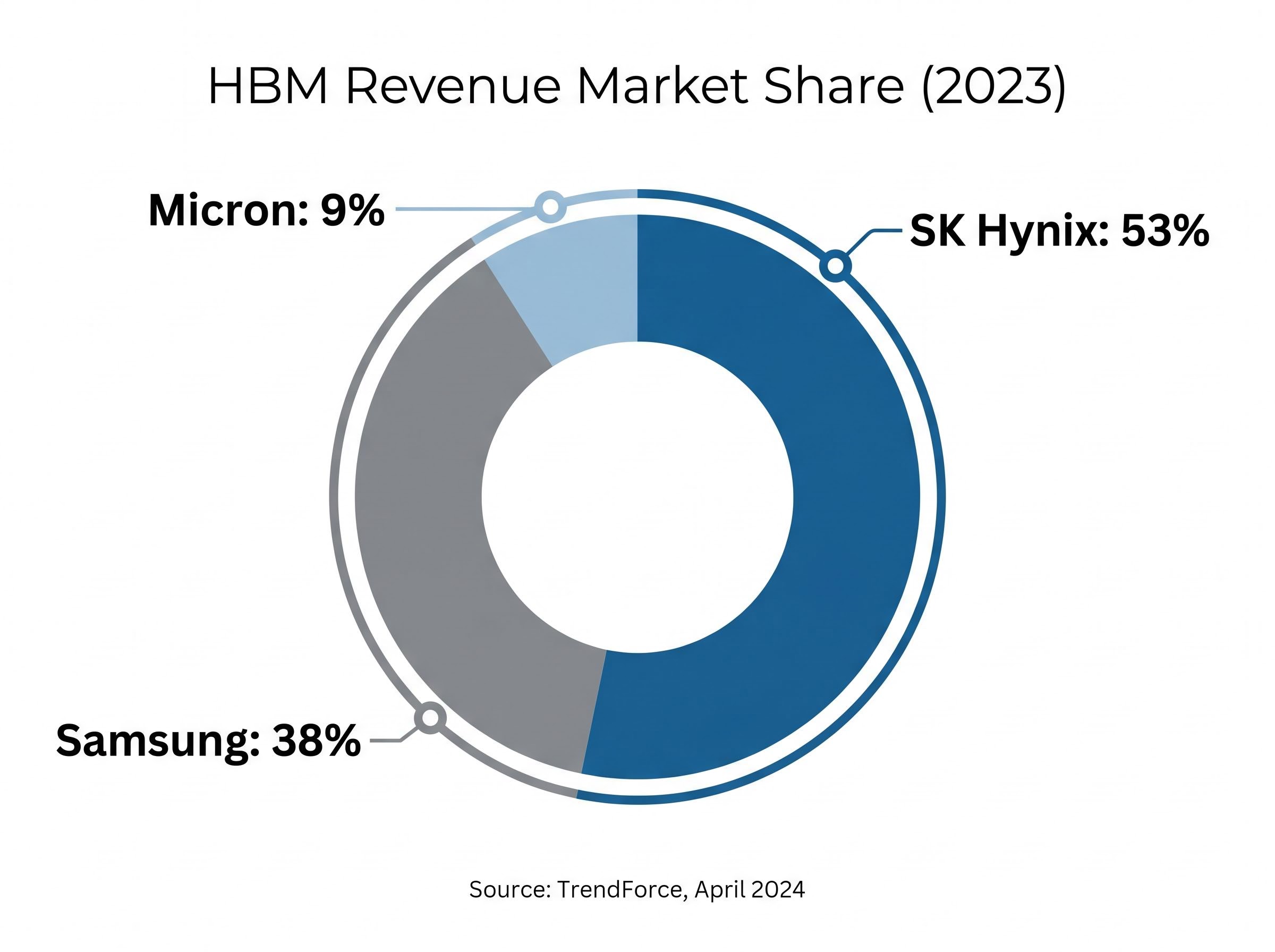

CXMT (ChangXin Memory Technologies) in China has been increasing overall DRAM capacity, but as of 2025 there are no verified large-scale HBM shipments into leading AI GPUs. U.S. export controls restricting EUV lithography access constrain CXMT’s ability to close the technology gap on a 2026-2027 horizon. As of 2023, SK Hynix held 53% HBM revenue market share (TrendForce, April 2024), Samsung held 38%, and Micron held 9%.

Chinese memory producer access to EUV lithography equipment remains constrained by U.S. export controls, and the diplomatic framework governing those restrictions is itself a moving variable, with Bloomberg Intelligence estimating a 70% probability of partial trade de-escalation that could shift the competitive landscape for CXMT on a 2026-2027 horizon.

The BIS export controls on advanced semiconductors, announced in December 2024, explicitly target high-bandwidth memory and restrict EUV lithography access to Chinese fabs, providing the regulatory foundation for why CXMT cannot credibly close the HBM technology gap on a 2026-2027 horizon.

The pricing forecasts that make or break the investment case

KB’s price targets for both stocks rest on average selling price (ASP) projections well beyond historical precedent. The numbers are specific, and they are aggressive.

| Metric (KB 2026 Forecast) | SK Hynix | Samsung Electronics |

|---|---|---|

| DRAM ASP Growth (YoY) | +194% | +297% |

| NAND ASP Growth (YoY) | +244% | +256% |

| 2026 Operating Profit | 277 trillion won | Not specified at comparable detail |

| 2026 Operating Margin | 78.1% | Not specified at comparable detail |

A 78.1% operating margin would represent the highest globally for a major semiconductor company, surpassing even TSMC’s peak margins. For these numbers to materialise, the supply void must hold, hyperscaler demand must accelerate on the projected trajectory, and pricing power must persist without meaningful competitive erosion through 2026.

KB projects SK Hynix’s Q2 2026 operating profit will surge more than eight times year-over-year to 70 trillion won. That figure, expected within weeks, represents the nearest verifiable checkpoint for the entire thesis. If the actual result approaches that magnitude, the full-year 277 trillion won projection gains credibility. If it falls materially short, the ASP assumptions underpinning both price targets face immediate re-examination.

How long-term contracts could transform memory from commodity to infrastructure business

The least discussed element of KB’s thesis may be the most consequential for long-term valuation. SK Hynix has reportedly shifted toward long-term supply agreements extending through 2028-2030, a structural change in how memory capacity is sold.

KB Securities describes SK Hynix’s contracting model as “foundry-style,” where customers place advance orders and production follows committed demand, analogous to how TSMC operates in logic chip fabrication.

The re-rating logic follows a specific sequence:

- Spot commodity model: Memory prices set by quarterly supply-demand balance, producing volatile earnings and compressed valuation multiples

- Long-term contract model: Multi-year agreements lock in volumes and pricing bands, reducing earnings volatility

- Earnings predictability improves: Lower volatility commands a structural premium from institutional investors

- Multiple expansion potential: If the market reclassifies memory as infrastructure rather than commodity, historical cycle-based valuation frameworks become inappropriate

With AI data centre operators accounting for approximately 70% of total memory shipments, the customer base is already concentrated enough for long-term contracting to reshape the revenue profile. KB further identifies agentic AI expansion into on-device and physical AI applications as the next demand broadening vector, reinforcing the long-duration nature of the thesis.

The structural memory supercycle differs from every prior DRAM upcycle in one critical dimension: demand is broadening beyond the hyperscaler tier into agentic AI, AI smartphones, AI PCs, and automotive ADAS, which raises memory intensity across the entire hardware stack rather than concentrating risk in a single demand source.

If this transition holds, investors applying historical memory cycle multiples may be systematically undervaluing these stocks. If it does not, and memory reverts to spot-price economics during the next demand softening, the premium evaporates.

The next major ASX story will hit our subscribers first

Where the thesis could fail: risks that serious investors need to price in

The bull case deserves the same scrutiny as the bear case. Four categories of risk warrant consideration:

- Supply response risks: Micron’s HBM3E ramp, Samsung’s own capacity additions, and gradual OSAT packaging expansion could soften the supply void earlier than KB projects

- Data vintage risk: Core supply tightness data from TrendForce and Yole is 12-plus months old; the 2026-2027 supply balance could look materially different in fresh industry data

- Valuation starting point risk: SK Hynix at approximately 1,835,000 KRW has already exceeded Morgan Stanley’s confirmed January 2026 target of 840,000 won; margin of safety depends almost entirely on KB-tier scenarios materialising

- Model assumption risk: KB’s $725 billion aggregate capex estimate and ASP forecasts are analyst projections, not company-confirmed figures

Supply risks versus valuation risks

These categories are distinct in kind. Supply risks, such as a faster-than-expected Micron ramp or OSAT capacity expansion, would undermine the fundamental thesis itself. Even if the supply void is real, the valuation starting point creates a separate risk layer. The updated 2026 Samsung broker consensus range sits at approximately 250,000-350,000 won (based on Marketscreener and Investing.com data, May 2026), which sits below KB’s 450,000-won target.

Investors entering at current price levels are not buying the beginning of a re-rating. They are buying the continuation of one. The risk-reward calculation is meaningfully different from where this thesis originated.

What the KB thesis actually demands of investors evaluating AI memory stocks

KB’s thesis operates on three layers: a structural supply deficit through 2027 and beyond, a foundry-model re-rating of memory earnings, and hyperscaler demand durability measured in trillions of dollars of cumulative capex. Accepting the thesis requires accepting ASP and margin projections well beyond historical precedent, including a 78.1% operating margin for SK Hynix that would be unprecedented among major semiconductor companies globally.

KB projects SK Hynix will achieve a 78.1% operating margin in 2026, a figure that, if realised, would represent the highest among global semiconductor producers and the single most extraordinary quantitative claim in the thesis.

The alternative reading is that current valuations, with SK Hynix at approximately 1,835,000 KRW versus a 3,000,000-won target and Samsung at approximately 270,500 KRW versus 450,000 won, already price substantial optimism. Three checkpoints will help investors calibrate:

- Q2 2026 SK Hynix operating profit result: the projected more-than-eight-times year-over-year surge to 70 trillion won is the nearest verifiable test

- Next TrendForce HBM supply update: fresh 2026 data would either confirm or complicate the “zero-supply era” framing

- Next round of hyperscaler capex guidance: any softening in multi-year language would directly weaken the demand foundation

Monitoring these datapoints allows investors to stress-test the thesis against incoming evidence rather than reacting to share price movement alone.

Investors wanting to apply a rigorous analytical lens to the KB price targets will find our full explainer on semiconductor valuation frameworks in 2026 useful, which examines PEG ratios for hypergrowth names, EV/EBITDA for cyclical recovery stocks, and cycle-adjusted forward estimates for memory names specifically, including where Micron’s current multiple sits relative to historical memory-sector peaks.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections referenced in this article are subject to market conditions and various risk factors.