A share price down roughly approximately 31% in a single calendar year is not background noise. For A2 Milk Company (ASX: A2M), the decline through 2025 raised a direct question: is this a business in structural decline, or a profitable consumer staples name temporarily mispriced by sentiment?

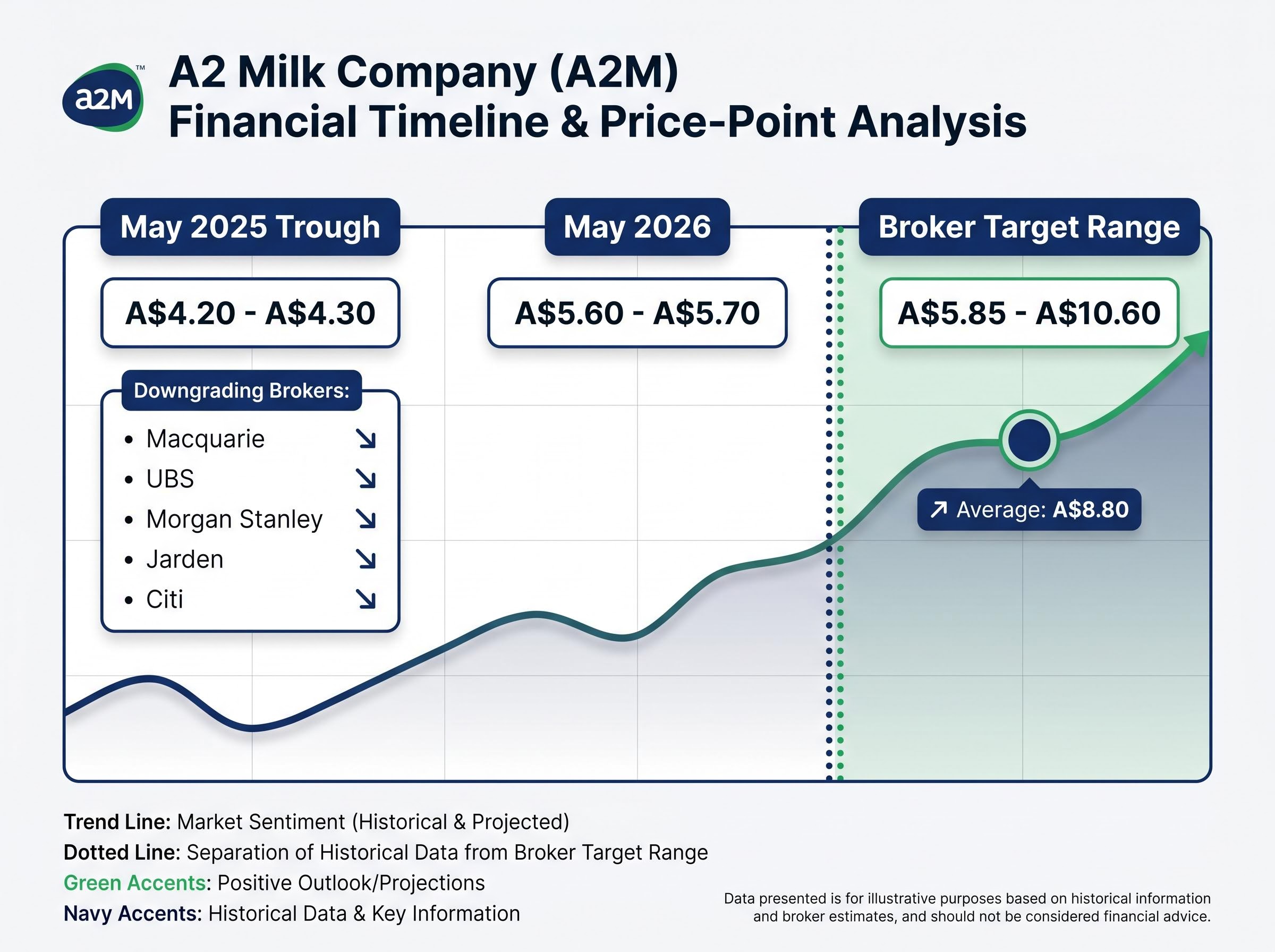

A2M entered 2025 as a cash-generative company with a genuine competitive differentiator and a recovering China business. By mid-2025, the stock had shed more than a third of its value, driven by cautious management commentary, a wave of broker downgrades, and structural concerns about China’s infant-formula market. By May 2026, A2M shares had partially recovered to around A$5.60-5.70, but the stock remains well below its pre-selloff levels.

What follows is an examination of what actually drove the fall, what the underlying financials reveal about the quality of A2M’s business, and what investors should weigh before concluding the selloff represents opportunity or warning.

What sent A2M shares down more than 38% in 2025

The selloff was not a single event. It was a convergence of disappointments, each reinforcing the last, that pushed A2M shares from their January 2025 levels to the A$4.20-4.30 range by May 2025.

The catalysts arrived in layers:

- 1H FY25 trading update disappointment: The February 2025 update revealed slower-than-expected China-label infant-formula growth, opening a gap between management’s measured tone and the market’s optimistic expectations.

- Guidance and margin concerns: FY25 outlook commentary pointed to moderate rather than high-teens revenue growth, with elevated marketing spend expected to pressure operating margins.

- Broker downgrades: Macquarie, UBS, Morgan Stanley, Jarden, and Citi all cut price targets in the weeks following the update, amplifying the selling pressure.

- Macro China headwinds: China’s declining birth rate and a slowing consumer added sector-wide caution toward all China-exposed dairy names.

- Synlait Milk overhang: Financial uncertainty at Synlait Milk, A2M’s primary manufacturing partner, was repeatedly flagged as a risk factor throughout 2024-2025.

Management described the China infant-formula environment as “challenging” and “highly competitive” in the February 2025 1H FY25 update, language that contrasted sharply with the recovery narrative investors had been pricing in.

The gap between what the market expected and what management delivered was the initial trigger. The broker downgrades, macro headwinds, and Synlait concerns made investors reluctant to buy the dip early, extending the decline across several months.

The ASX consumer staples sector as a whole has delivered negative average annual returns over the five years to May 2026, a counterintuitive outcome for a category often labelled defensive, and one that frames why individual stock selection within the sector matters more than broad sector exposure.

When big ASX news breaks, our subscribers know first

A2 Milk’s business model: how the company actually makes money

Before any financial analysis can land properly, the structure of A2M’s business needs to be understood on its own terms. The numbers look the way they do because of specific choices about how the company produces and distributes its products.

The asset-light production model

A2 Milk, established in New Zealand in 2000, does not own farms or manufacturing facilities in the traditional sense. The company sources milk through more than 25 certified dairy farming partners in Australia and contracts Synlait Milk in New Zealand for infant-formula production.

This keeps capital requirements low and returns on invested capital relatively high. It also creates concentration risk. Until 1 January 2025, Synlait held exclusivity over A2M’s infant-formula manufacturing. That exclusivity has since ended, and the company has expanded its commercial relationship with Yashili New Zealand to diversify its production base. The trade-off between capital efficiency and supply concentration remains the central structural tension in A2M’s business model.

How A2M reaches Chinese consumers

A2M’s core product proposition, that A2 beta-casein protein is easier to digest than conventional A1 milk protein, commands a premium price point in both China and Australia. Reaching Chinese consumers requires consistent brand investment across several channels:

- Cross-border e-commerce (CBEC) platforms such as Tmall and JD.com, which have become the primary route to market

- Mother-and-baby stores within mainland China

- Daigou (personal shoppers), a channel that has shrunk structurally since pre-COVID levels

This channel mix is more stable than the daigou-dependent model of earlier years, but it requires sustained marketing spend. That spending is the direct reason margins have been under pressure, a cost of doing business in China rather than a sign of operational weakness.

Revenue and profit growth: what the numbers reveal about trajectory

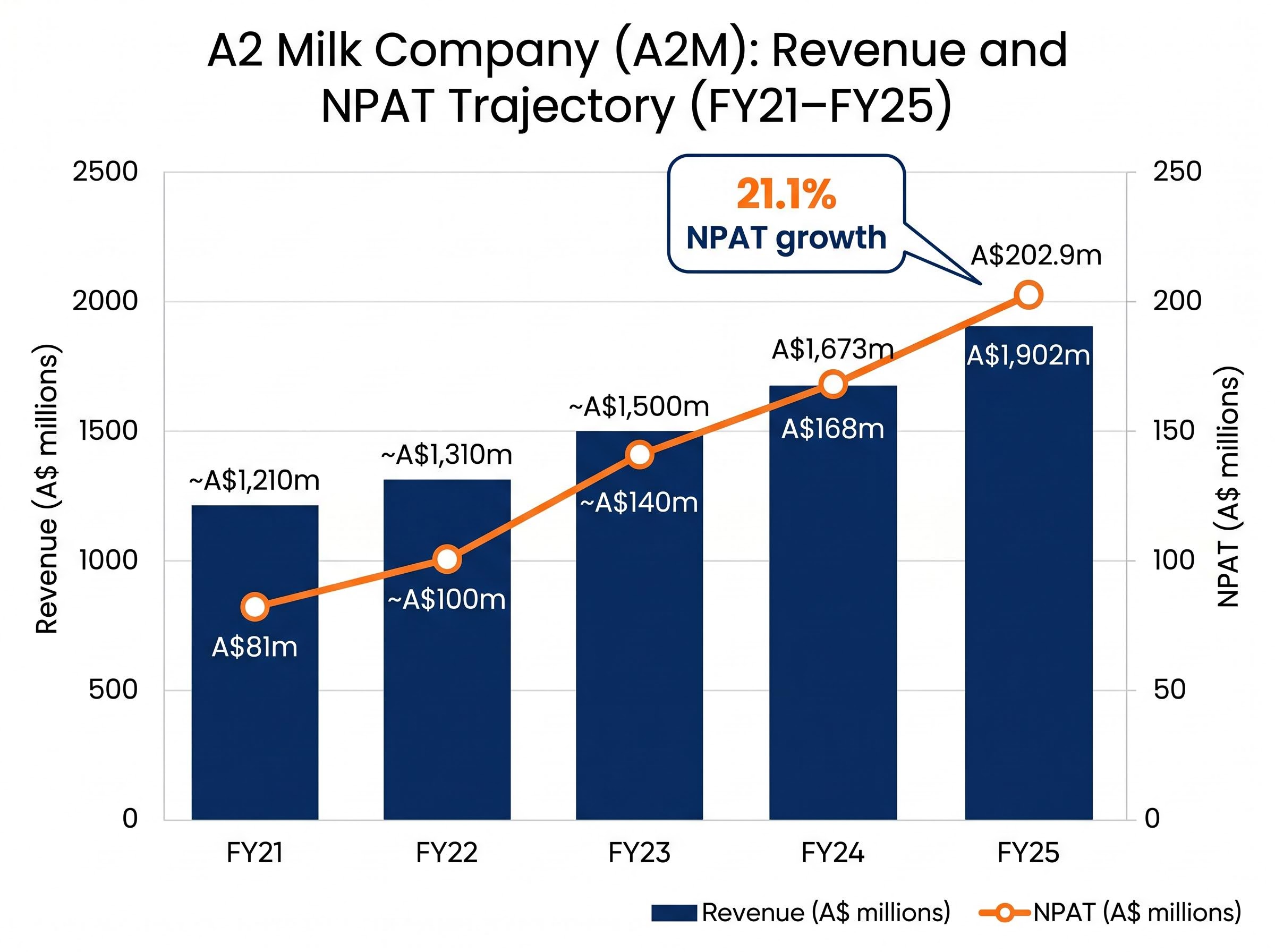

The revenue and profit data tell a story of genuine recovery. From FY21 to FY24, A2M rebuilt its earnings base at a pace that exceeded what most brokers had modelled during the post-COVID trough.

| Year | Revenue (A$m) | NPAT (A$m) |

|---|---|---|

| FY21 | ~1,210 | 81 |

| FY22 | ~1,310 | ~100 |

| FY23 | ~1,500 | ~140 |

| FY24 | 1,673 | 168 |

| FY25 | 1,902 | 202.9 |

Revenue grew at a compound annual rate of approximately 11.6% from FY21 to FY24, reaching A$1,673 million. Net profit attributable to shareholders more than doubled over the same period, from A$81 million to A$168 million.

Then came FY25. The year the market feared would disappoint actually delivered stronger results than the cautious February 2025 guidance had implied. Revenue grew 13.5% to A$1.902 billion. Net profit after tax grew 21.1% to A$202.9 million.

FY25 NPAT growth of 21.1% arrived against a backdrop of broker downgrades and a share price that had already fallen more than 30%, a gap between market sentiment and business performance that is central to the investment question.

FY26 guidance has since been upgraded. Initial targets of high single-digit revenue growth with EBITDA margins of 15-16% were revised upward to low double-digit revenue growth, with NPAT expected slightly higher than FY25. The trajectory remains intact.

Return on equity and capital efficiency: is A2M using shareholder funds well

Revenue growth tells investors the business is expanding. Return on equity (ROE) tells them something subtly different and more investment-relevant: whether the company is generating adequate returns on the capital shareholders have entrusted to it.

ROE measures net profit as a percentage of shareholders’ equity, the portion of company assets funded by shareholders rather than debt. It captures how efficiently a business converts equity into earnings. A commonly referenced benchmark is 10%; companies consistently above this level are generally considered to be deploying capital effectively.

Return on equity sits alongside earnings per share, revenue growth, profit margins, and price-to-earnings ratios as one of the five core metrics that together describe how a business is actually performing; each metric answers a different question, and no single figure, including return on equity, is sufficient without the others to form a complete picture of value.

A2M’s most recently reported ROE sits at approximately 12.8%.

That figure carries more weight when considered alongside the business model. A2M’s asset-light structure, with no owned farms or factories, means the equity base is relatively lean. Low capital intensity tends to produce higher ROE because less equity is tied up in physical assets.

For context, Wesfarmers reported an FY24 ROE of 30.3%, though direct comparison has limits given Wesfarmers is a mature, diversified, and more leveraged business.

What ROE does and does not tell investors:

- It measures efficiency of equity deployment, a quality signal for growth-stage businesses

- It does not account for how much debt a company uses to amplify returns

- It is most useful in context: business stage, capital structure, and sector norms all matter

- A single metric, including ROE, is insufficient for a complete valuation assessment

An ROE of 12.8% in a growth-stage business with low debt and an expanding revenue base suggests A2M is not burning through capital to chase growth. That distinction matters for consumer staples companies targeting emerging markets, where capital discipline often separates compounders from capital-hungry growers.

The structural headwinds that make China exposure a genuine risk

The bullish case for A2M rests on recovery and re-rating. The bearish case rests on structural forces that recovery alone may not overcome. Both deserve full weight.

Demographic and competitive pressure in China’s infant-formula market

China’s birth rate continues to fall, directly shrinking the addressable market for infant formula. No amount of market share gain can fully offset a declining pool of consumers in the medium term. According to coverage from Reuters and Bloomberg News in early 2025, some parents were also trading down to cheaper brands amid broader economic uncertainty.

At the same time, local Chinese brands have gained share, supported by government policy favouring domestic champions. International brands including A2M have absorbed higher promotional spending to defend their positions, particularly on CBEC platforms. English-label infant-formula sales have shown stronger relative growth compared to China-label volumes in recent periods, but the competitive dynamics remain demanding.

A2M’s response has included higher marketing spend, deeper CBEC platform investment, and category diversification into adult nutrition. Whether these measures can sustain premium returns in a contracting market is the central question for the China business.

What the Synlait situation means for investors

Synlait Milk faced significant financial challenges through 2024-2025, including high debt levels and the need to renegotiate banking facilities. For A2M, which concentrated its infant-formula manufacturing with Synlait for years, this created a supply-security risk that investors priced into the stock.

Synlait’s financial position through the 2024-2026 period, including an $80.6 million NPAT loss, $472 million in net debt, and banking covenant renegotiations, provides the specific context behind why investors treated the manufacturing concentration risk as a genuine supply-security concern rather than a theoretical one.

The exclusivity arrangement ended on 1 January 2025, and A2M has expanded its relationship with Yashili New Zealand to diversify production. Synlait remains a key partner as of the latest reporting. The partial mitigation is real, but supply-chain diversification involves execution risk and potential capital requirements that are not yet fully resolved.

The three structural headwinds in summary:

- Demographic: China’s falling birth rate is shrinking the infant-formula addressable market

- Competitive: Domestic Chinese brands are gaining share with government policy support, forcing higher marketing spend from international players

- Supply chain: Synlait’s financial stress created concentration risk that diversification has only partially addressed

The next major ASX story will hit our subscribers first

Where the evidence actually points for investors reconsidering A2M shares

The data pulls in two directions. FY25 outperformance and the FY26 guidance upgrade suggest the business is executing better than the market feared in early 2025. The structural China headwinds and residual supply-chain risk suggest the recovery may have a lower ceiling than the pre-selloff valuation implied.

Broker consensus reflects this tension. The average price target sits near A$8.80 as of May 2026, implying meaningful upside from the current A$5.60-5.70 level. The range, however, spans from approximately A$5.85 to A$10.60, a width that signals genuine uncertainty rather than conviction.

The consensus average price target near A$8.80 implies significant upside from the current A$5.60-5.70 trading range. The wide spread between the lowest and highest targets, from approximately A$5.85 to A$10.60, reflects how differently brokers are weighing the structural risks against the earnings trajectory. Broker-specific targets should be treated with appropriate caution, as some figures have not been independently verified against primary sources.

With a market capitalisation of approximately A$4.1 billion, FY25 revenue of A$1.902 billion, and NPAT of A$202.9 million, the earnings base is established. The question is whether it justifies a re-rating or whether the current price already captures the recovery.

Before forming a view, investors should be able to answer:

- What is the conviction level on China’s infant-formula market stabilising, or at least declining at a rate A2M’s share gains can offset?

- Is the Synlait execution risk adequately mitigated by the Yashili diversification, or does residual concentration remain a material concern?

- Does premium dairy demand in China and Australia have enough durability to sustain A2M’s margins beyond the current cycle?

- At the current share price, does the earnings trajectory justify buying, or is the market already pricing in a recovery that may stall?

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

The selloff tells part of the story, the fundamentals tell the rest

The 2025 selloff was not irrational. The guidance miss was real, the China headwinds are structural, and the Synlait overhang carried genuine supply-chain risk. Investors who sold had reasons.

The fundamentals, however, do not support a verdict of structural decline. A revenue CAGR of approximately 11.6% from FY21 to FY24, FY25 NPAT growth of 21.1%, an ROE of 12.8%, and an upgraded FY26 outlook collectively describe a business with quality characteristics that survived a severe sentiment correction.

No single metric, whether ROE, revenue growth, or broker target, is sufficient for a complete valuation. The metrics discussed here represent a limited selection that provides analytical foundation, not an investment conclusion. The gap between the selloff’s severity and the underlying business performance is the starting point for due diligence, not the end of it.

For readers wanting to assess whether the partial recovery to A$5.60-5.70 represents fair value or a continued premium, our dedicated guide to A2M’s P/S valuation examines the current multiple against the five-year historical average, the H1 FY26 revenue momentum, and the specific catalysts, including the Synlait-Synergy merger and the August 2026 full-year result, that could shift the premium either way.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

—