National Australia Bank shares have retreated roughly 25% from their early-2026 peak near $50, and for income-focused investors that pullback has done something worth examining closely. At $37.86 as of 21 May 2026, the stock’s grossed-up NAB dividend yield has climbed to approximately 6.5%, materially above what Commonwealth Bank offers and well ahead of most term deposit rates. The question is whether that improved yield represents a genuine buying opportunity or simply fair compensation for a stock the broader analyst community has turned cautious on. Seven brokers revised their ratings or price targets following NAB’s 4 May 2026 half-year result, and the skew was notably negative on capital upside. This analysis works through NAB’s FY27 dividend forecasts, the grossed-up yield mechanics, how the stock compares to Westpac and ANZ, what a concrete $8,000 investment would actually return, and what the analyst consensus means for income investors specifically.

What NAB’s FY26 half-year result says about dividend sustainability

NAB reported FY26 half-year underlying cash earnings of $3.6 billion on 4 May 2026, and the number told a steady-state story rather than a growth story. The key result metrics:

- Cash earnings: $3.6 billion for the half

- Year-on-year change: up 0.1%

- Half-on-half change: up 2.3%

Those are modest figures. They are also precisely the kind of figures that underpin a well-covered dividend rather than threaten one. The board held the interim dividend at 85 cents per share, fully franked, signalling confidence in coverage rather than a reluctance to grow the payout.

Ord Minnett described NAB as “good value for income investors after the share price retreat,” reaffirming its Accumulate rating and highlighting the dividend as “well covered” (The Australian, 19 May 2026).

Citi offered a more measured reading, calling the 85 cent interim dividend “sustainable but not a catalyst” given the modest profit trajectory (Reuters Australia, 9 May 2026). For income investors, that distinction matters. Sustainability is the floor this section needed to establish, and the half-year numbers establish it clearly.

When big ASX news breaks, our subscribers know first

How franking credits change the NAB yield calculation

The cash yield at current prices

At $37.86 per share (AFR, 22 May 2026), NAB’s forward cash dividend yield depends on whose forecast is used. Ord Minnett projects an FY27 dividend of $1.72 per share, fully franked, implying a cash yield of 4.54%. The CMC Invest consensus sits slightly lower at $1.70 per share, producing a cash yield of approximately 4.49%.

Both figures fall in a narrow band. The cash yield, whichever estimate is preferred, sits around 4.5%.

What franking credits add to that figure

For Australian resident taxpayers entitled to franking credits, that 4.5% cash yield understates the real return. Fully franked dividends carry a credit for the 30% corporate tax already paid by the company. The grossing-up calculation divides the cash dividend by 0.70 to arrive at the pre-tax equivalent.

| Source | Forecast Dividend | Cash Yield | Grossed-Up Yield |

|---|---|---|---|

| Ord Minnett | $1.72 | 4.54% | ~6.50% |

| CMC Invest consensus | $1.70 | ~4.49% | ~6.42% |

A grossed-up yield of approximately 6.5% compares favourably to term deposit rates and most hybrid securities available to Australian investors as of May 2026. The franking credit is the mechanism that transforms a mid-range cash yield into a competitive income proposition.

For investors who want to apply the 30/70 grossing-up formula to their own holdings across different tax brackets, our dedicated guide to franking credit calculations walks through the arithmetic step by step, including the specific scenarios where SMSF pension-phase members receive the full credit as a direct ATO cash refund rather than a tax offset.

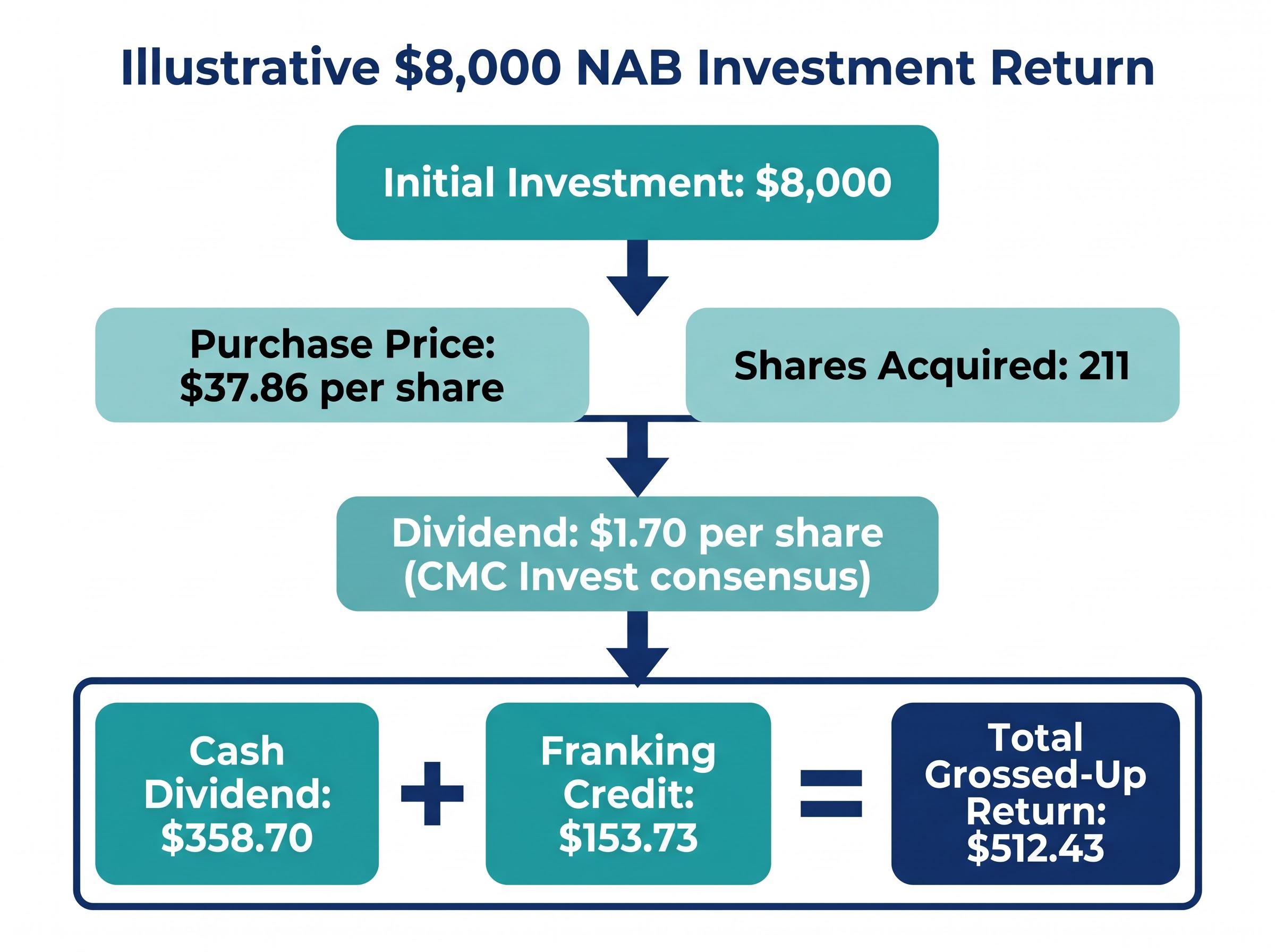

Illustrative Income Calculations

Percentages inform. Dollar figures decide. Here is the worked example using the more conservative CMC Invest consensus dividend of $1.70 per share:

- Purchase price: $37.86 per share

- Shares acquired: approximately 211 shares ($8,000 ÷ $37.86)

- Cash dividend received: approximately $358.70 (211 × $1.70)

- Franking credit value: approximately $153.73 ($358.70 × 30/70)

- Total grossed-up return: approximately $512.43

That is the income side. The capital side is less generous. The CMC Invest consensus price target sits at $38.74 (Reuters Australia, 9 May 2026), implying roughly 2.3% upside from $37.86. On an $8,000 position, that translates to approximately $185 in potential capital appreciation.

Motley Fool Australia labelled NAB a “Hold for yield, not for growth” (14 May 2026), citing limited earnings per share expansion and downside risk if credit losses normalise.

The characterisation fits the numbers. An income investor buying here is collecting a meaningful grossed-up return of around $512 on $8,000, while accepting that the capital is unlikely to move substantially in either direction based on current consensus.

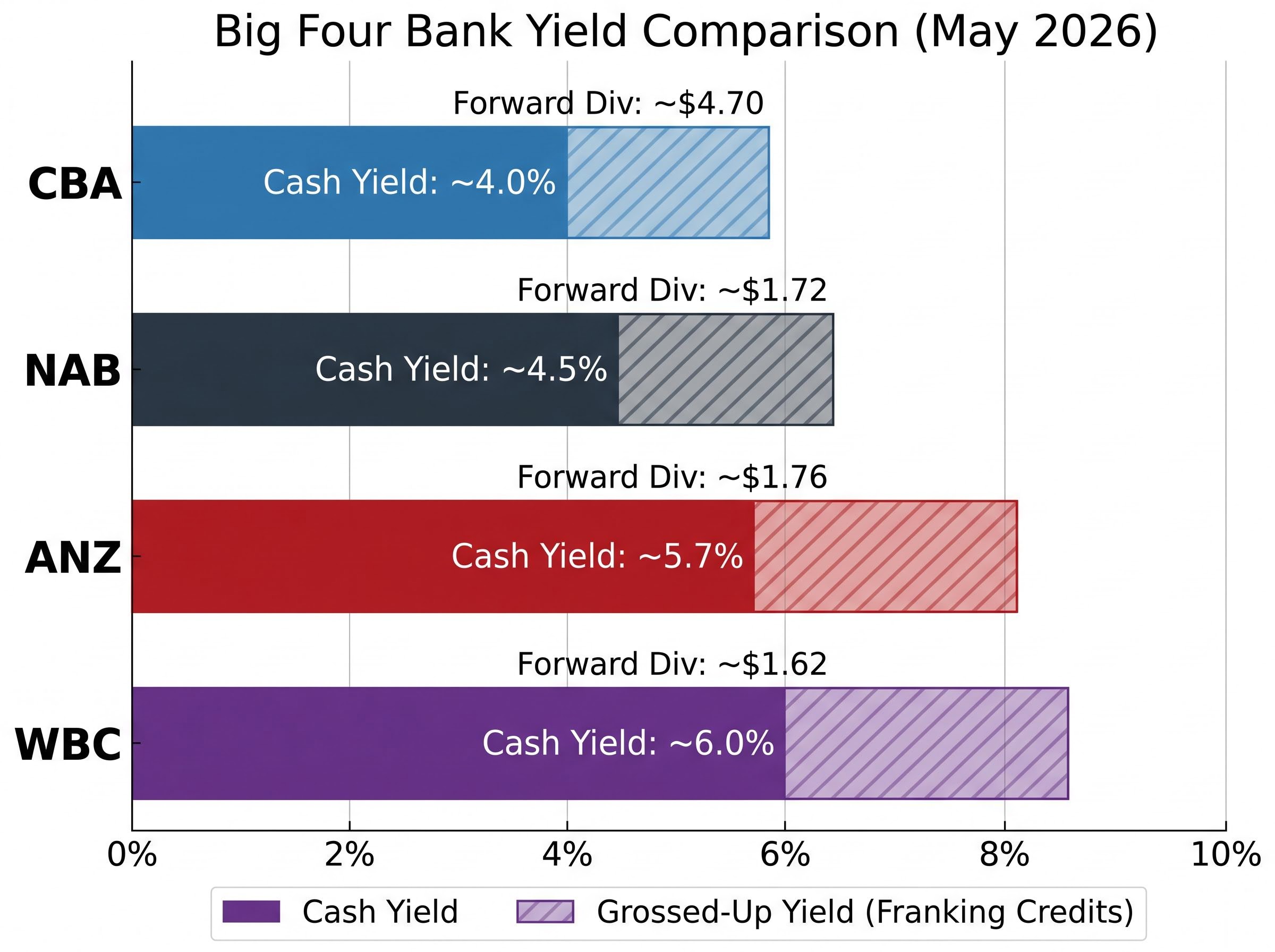

How NAB’s yield compares to the other big four banks

| Bank | Forward Dividend | Cash Yield | Grossed-Up Yield | Source |

|---|---|---|---|---|

| CBA | ~$4.70 | ~4.0% | ~5.7-5.8% | CMC Invest / AFR, May 2026 |

| NAB | ~$1.72 | ~4.5% | ~6.5% | Ord Minnett / The Australian, 19 May 2026 |

| ANZ | ~$1.76 | ~5.7% | ~8.1% | CMC Invest / UBS via AFR, May 2026 |

| WBC | ~$1.62 | ~6.0% | ~8.6% | CMC Invest / Macquarie, May 2026 |

The hierarchy is clear. CBA offers the lowest yield, trading at a premium that reflects its perceived quality. Westpac and ANZ sit at the top, with grossed-up yields above 8%. NAB occupies the middle position.

The way franking credit adjustments shift the rankings among the big four is particularly significant for ANZ, whose headline yield advantage over NAB narrows considerably once partial franking is applied, a dynamic the May 2026 half-year results confirmed across all four banks.

The AFR characterised NAB as “a middle-of-the-pack income option” with “safer but less spectacular yield” relative to Westpac (13 May 2026). The AFR Chanticleer column added that NAB’s “balance between yield, dividend stability, and capital strength will appeal to conservative retirees” (17 May 2026).

An income fund manager quoted in AFR Smart Investor described NAB as “the most balanced of the big four for income portfolios, not the highest yield, but one of the more dependable” (3 May 2026).

Higher yield at Westpac and ANZ comes with different business mix and risk profiles. NAB’s middle position is the trade-off: less income, but a dividend history and payout ratio that income investors with lower risk tolerance may find more comfortable.

Why analysts are cautious on NAB despite the dividend appeal

The post-result broker action summary

Seven brokers acted on NAB following the 4 May 2026 half-year result. The direction was overwhelmingly cautious:

| Broker | Previous Rating | New Rating | Price Target |

|---|---|---|---|

| Macquarie | Outperform | Neutral | $39.00 |

| Goldman Sachs | Buy | Neutral | $40.10 |

| Jarden | Overweight | Neutral | $38.00 |

| UBS | Sell | Sell | $35.00 |

| Morgan Stanley | Underweight | Underweight | $36.50 |

| Citi | Neutral | Neutral | $38.50 |

| Ord Minnett | Accumulate | Accumulate | $40.00 |

Three brokers downgraded. Two held negative ratings. One held Neutral with a lower target. Only Ord Minnett maintained a positive stance, with a $40.00 price target.

What analyst caution actually means for income investors

The concerns centre on earnings growth, not income sustainability. Morgan Stanley cited “limited earnings leverage.” Macquarie flagged flattening net interest margins. UBS highlighted “sub-par ROE versus CBA and ANZ.” Goldman Sachs expects “low single-digit EPS growth.”

No broker identified dividend sustainability as a risk. No broker modelled a dividend cut.

Payout ratio sustainability is the measure that separates a reliable income stream from a yield trap, and across the big four banks the April 2026 analysis showed ANZ and Westpac both sitting above their own stated target ranges, a signal income investors weighing NAB’s more modest yield should factor into their comparison.

Reuters Australia observed that “dividends look well covered, but limited capital upside tempers enthusiasm” (9 May 2026). The consensus price target of approximately $38.70 implies only modest capital appreciation from $37.86. For growth investors, that is a problem. For income investors buying at this price for the 6.5% grossed-up yield, the question is different: is the dividend safe? On current evidence, the answer is yes.

The income case for NAB in 2026 is real, but it is not the whole picture

The regulatory backdrop explains why NAB’s payout ratio is unlikely to stretch dramatically higher. APRA’s 30 September 2025 guidance to all authorised deposit-taking institutions emphasised that boards should “avoid materially increasing payout ratios where stress test results indicate capital could fall towards prudential minima under plausible downturn scenarios.” The Australian interpreted this as effectively ending the era of 80%-plus payout ratios for the majors (2 October 2025).

APRA capital adequacy guidance under APG 110 establishes the specific conditions under which authorised deposit-taking institutions face automatic restrictions on capital distributions, including dividends, when CET1 ratios fall within or below prescribed buffer ranges, making the regulatory ceiling on payout ratios a structural feature rather than a discretionary board preference.

The RBA’s Financial Stability Review (October 2025) confirmed that major banks’ CET1 ratios (the core measure of a bank’s capital strength relative to its risk-weighted assets) sit comfortably above regulatory minima, but warned against complacency on credit losses. The income case rests on stability, not expansion.

Three conditions define that case:

- Yield level: grossed-up yield of approximately 6.5%, attractive relative to term deposits and hybrids

- Dividend coverage: half-year earnings comfortably cover the 85 cent interim payout, with no broker flagging sustainability risk

- Regulatory environment: APRA framework supports steady, fully franked distributions but limits scope for aggressive payout increases

Morningstar Australia described NAB’s dividend as “reliable rather than exciting” (29 April 2026), a characterisation that captures the stock’s positioning precisely.

The share price retreat from near $50 to $37.86 is the mechanism that improved the yield. It is not, by itself, a reason to expect capital appreciation. The Australian Wealth noted the grossed-up yield “looks attractive relative to term deposits and hybrids” (19 May 2026), but the income case and the capital case are different propositions, and this stock is currently offering one far more convincingly than the other.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

NAB as an income stock in 2026: dependable, not dazzling

NAB’s grossed-up yield of approximately 6.5% represents a genuine income opportunity following the share price pullback, but it is a middle-of-the-road proposition within the big four. The dividend is well covered. The regulatory environment supports steady distributions. Analyst caution reflects limited capital upside rather than income risk; income investors and growth investors are asking fundamentally different questions about this stock.

For conservative income investors and retirees seeking fully franked dividends with reasonable capital stability, NAB merits serious consideration at current prices. Those seeking to maximise raw yield should compare Westpac and ANZ carefully, understanding the different risk profiles those higher yields carry.

Investors wanting to position NAB within a broader income strategy will find our comprehensive walkthrough of ASX dividend portfolio construction covers sector diversification requirements, payout ratio screening, and how to combine fully franked bank shares with property and infrastructure holdings to reduce concentration risk across a retirement income portfolio.

For further context on how the big four banks compare on total shareholder returns, or a deeper explanation of how franking credits interact with different tax brackets, related analyses on ASX bank dividends and franking credit mechanics offer additional detail.

—