Chalmers Targets CGT, Negative Gearing and Trusts in 2026 Budget

1 hr ago

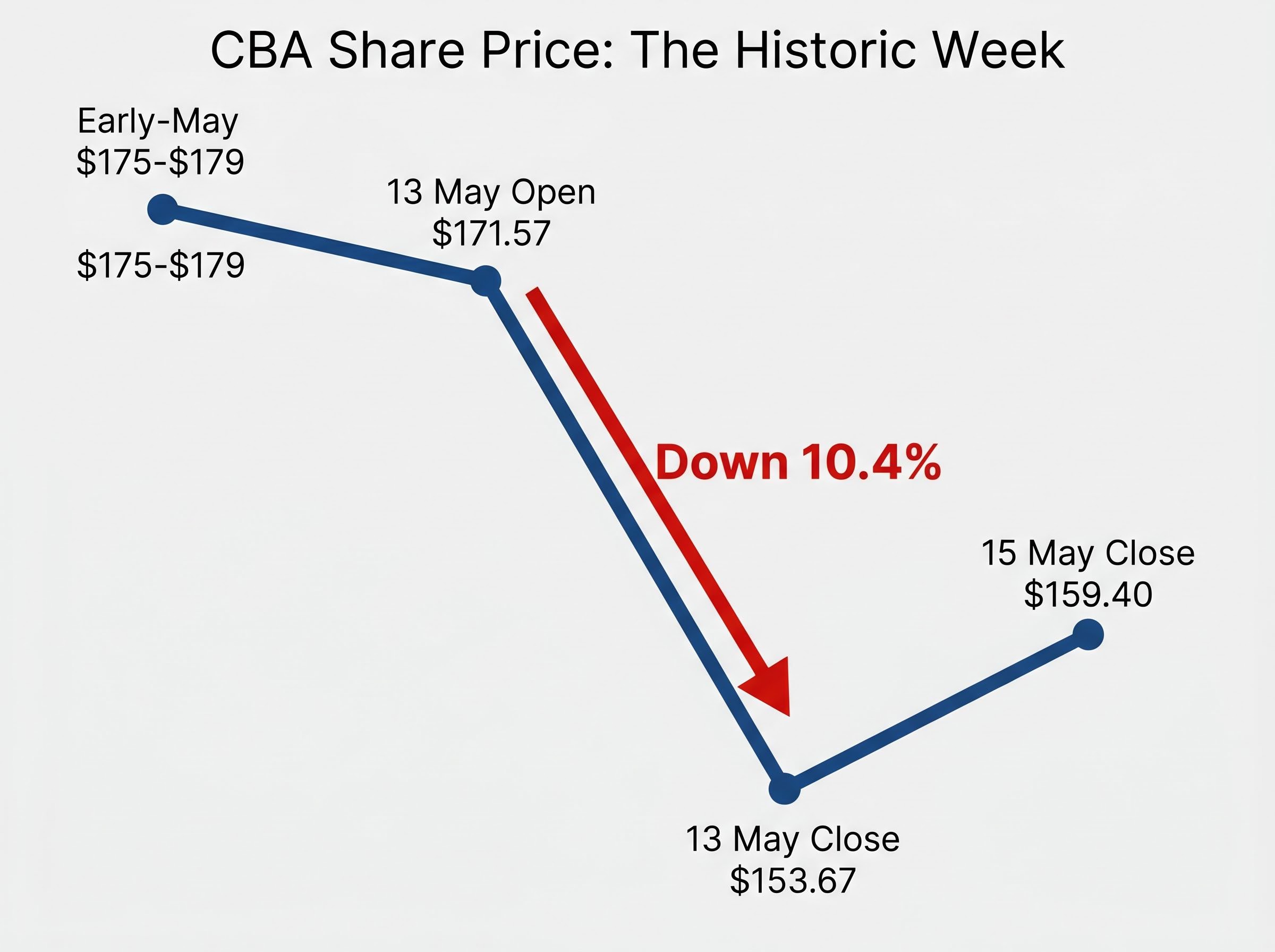

Commonwealth Bank shares recorded their largest single-day fall in the company’s listed history on Wednesday 13 May 2026, shedding 10.4% in a single session to close at $153.67. The decline wiped billions from market capitalisation and sent a shock through a shareholder base that stretches from self-managed super funds to the country’s largest institutional portfolios.

The collapse followed the release of CBA’s Q3 FY2026 trading update, which revealed a modest profit dip and a deliberate build-up in collective loan-loss provisions against an uncertain macroeconomic backdrop. For a stock that had been trading at premium multiples relative to every domestic and global banking peer, the market’s response was swift and severe.

What follows unpacks exactly what the quarterly numbers showed, why management’s provisioning decision rattled investors, what the pre-existing valuation picture meant for the severity of the fall, and what analysts are now saying about where the CBA share price heads from here.

The numbers tell the story before any interpretation is needed. CBA opened Wednesday at $171.57 and never recovered. Selling accelerated through the session, and the stock closed at $153.67, a 10.4% decline that ABC News confirmed as the largest single-day fall on record for the bank.

“Largest one-day fall on record, closing 10.4 per cent lower.” — ABC News, 13 May 2026

By Thursday 15 May 2026, a partial recovery had lifted the price to $159.40. That still left the stock down approximately 9.4% for the week from early-May levels near $175-$179.

The key price data points for the week:

For the large number of Australians who hold CBA directly or through superannuation, the dividend context matters. On a total-return basis, the $4.95 in fully-franked dividends over the trailing twelve months partially cushions the 6.09% capital decline, though it does not eliminate it.

CBA’s Q3 FY2026 trading update, released on 13 May 2026, covered the quarter ended 31 March 2026. It was a Pillar 3 capital and risk disclosure, not a full results announcement, which limits the granularity of available figures.

The headline metrics were modest rather than alarming:

APRA’s unquestionably strong capital framework established 10.5% CET1 as the benchmark for major Australian banks, which means CBA’s reported ratio of 11.6% sits meaningfully above the regulatory floor and reflects a capital buffer that management has preserved even while absorbing the provision build.

| Metric | Value | Change |

|---|---|---|

| Unaudited cash NPAT | ~$2.7 billion | Down 1% vs avg H1 FY2026 quarterly cash NPAT |

| CET1 capital ratio | 11.6% | Remains well above regulatory minimums |

A quarterly cash profit of approximately $2.7 billion is not a figure that, on its own, signals distress. The 1% decline relative to the average quarterly earnings from the first half of FY2026 represented a softening, not a collapse.

That gap is the central puzzle of this week. A 1% earnings dip would not ordinarily move a major bank stock by 10% in a single session. Something else in the update did most of the market damage, and it sits in the provisioning line.

One reason the 28.5x forward earnings multiple became such a vulnerability is that PE ratios mislead bank investors in ways that are less visible with industrial stocks: a single provision movement can suppress or inflate reported earnings significantly, making the PE ratio at any given moment a partial reflection of management’s accounting decisions as much as the bank’s true earnings power.

CBA increased its collective loan-loss provisions during the quarter, despite an already-strong provisioning base. Management cited several macroeconomic risk factors as contributing to the decision:

Collective vs specific provisions: Collective provisions are set aside against loans that have not yet defaulted but that management believes carry elevated future risk. Specific provisions, by contrast, are charged against individual loans already identified as impaired. CBA’s build was collective, a precautionary move rather than a response to loans already going bad.

The distinction matters because the decision to raise collective provisions flows directly through the income statement. It suppresses reported profit even when no individual loans have soured. That accounting effect contributed directly to the quarter’s 1% earnings softening.

KPMG’s Big Four Banks 2025 report, published in November 2025, described the broader sector as experiencing slightly higher expected credit loss provisions in line with portfolio growth, though arrears remained low and credit quality broadly benign. CBA’s decision to build provisions beyond that baseline tells investors that its leadership believes conditions are becoming less certain. That forward-looking signal, more than the profit dip itself, is what the market responded to on Wednesday.

The provisioning signal landed on a stock that had left itself almost no margin for disappointment.

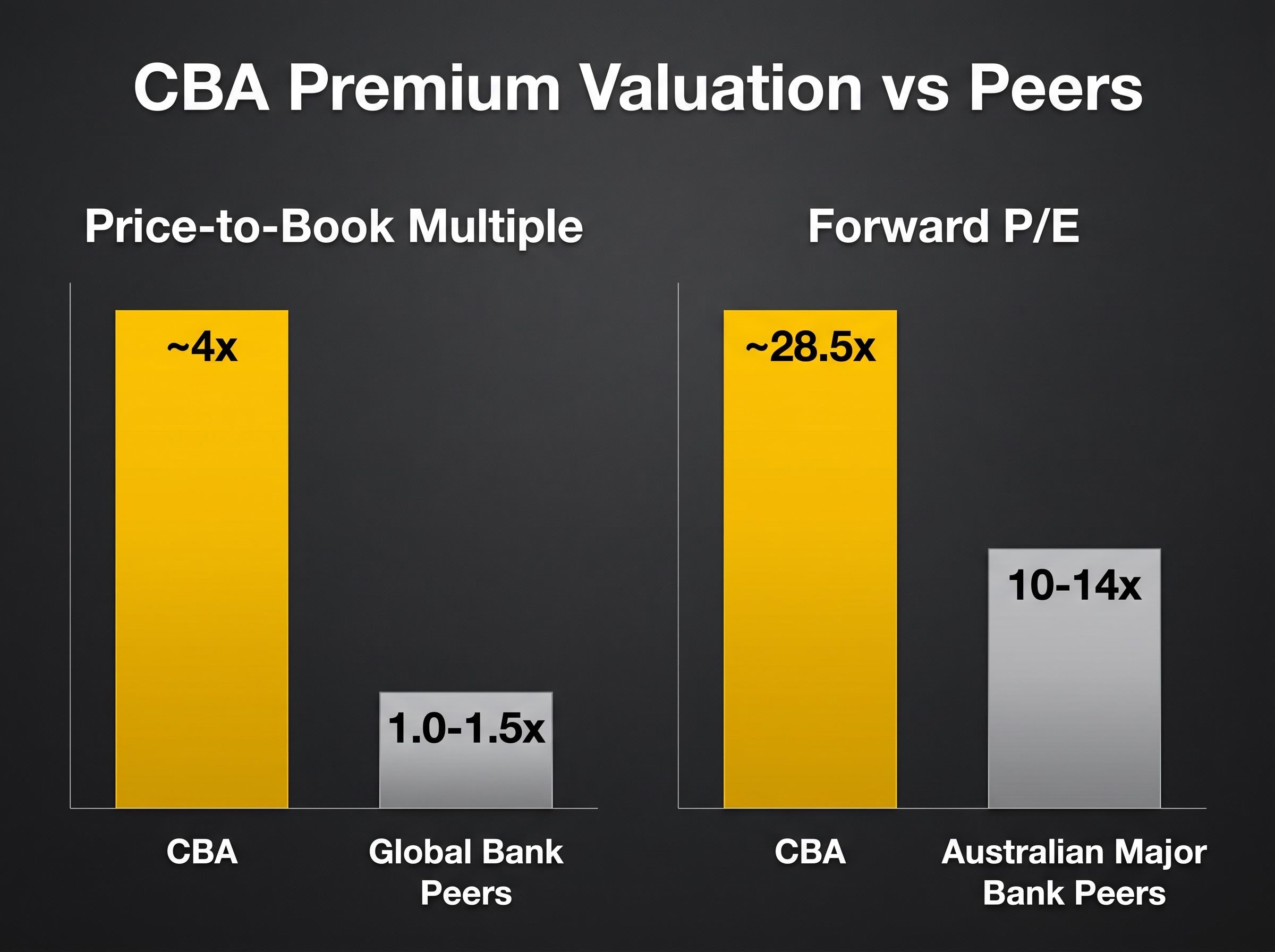

Heading into the Q3 update, CBA was trading at:

That valuation premium had been the subject of sustained broker concern. UBS had maintained a Sell rating with a price target of $96.07, arguing the stock was structurally vulnerable to a sharp correction on any disappointment. A Motley Fool Australia retrospective published on 2 January 2026 noted CBA had already experienced a 21% peak-to-trough move during 2025, evidence that correction risk at elevated multiples was not theoretical.

Part of what sustained the premium for so long was structural demand for CBA shares from compulsory superannuation inflows, ASX 200 index weighting, and SMSF familiarity bias, mechanical buying forces that income-based valuation models do not capture and that help explain why broker Sell ratings had limited effect on the share price through most of 2025 and into 2026.

At approximately 28.5x forward earnings, CBA’s valuation had built in a growth trajectory that left the stock highly vulnerable to disappointment. Wednesday’s result provided that disappointment.

When a stock prices in optimism of that magnitude, even a marginal shortfall can trigger a disproportionate re-rating. A 1% profit dip becomes a 10.4% share price fall not because the result was catastrophic, but because the valuation starting point had priced in near-perfection.

For readers less familiar with bank accounting, collective provisions are worth understanding from the ground up. They appear regularly in bank results and carry more information than many investors realise.

In plain terms, a collective provision is money a bank sets aside against loans that have not yet gone bad but that management believes carry elevated future risk given current economic conditions. Unlike specific provisions, which are charged against individual loans already identified as impaired, collective provisions are forward-looking and based on management’s assessment of where the economy is heading.

The mechanics work in five steps:

The accounting link is direct. When CBA raised its collective provision in Q3 FY2026, that increase was charged as an expense in the quarter, reducing the reported cash net profit after tax. The $2.7 billion quarterly result already reflects the drag from this provision build. Had management held provisions steady, the reported profit figure would have been higher, and the quarter-on-quarter decline would have been smaller or potentially nonexistent.

CBA’s FY25 Annual Report described the bank’s prior provisioning environment as characterised by low arrears and stable unemployment. The decision to build provisions beyond that baseline, in a quarter where KPMG had described sector-wide credit quality as broadly benign, is what gave the move its signalling weight.

NAB’s $706 million credit impairment charge in April 2026, linked to geopolitical volatility and stress in agriculture, transport, and manufacturing, triggered a 3.6% single-day fall of its own, establishing a sector pattern where forward-looking provision signals consistently punish share prices far beyond what the profit impact alone would suggest.

The range of analyst views on CBA following Wednesday’s sell-off is wide enough to reflect genuine disagreement about how far the re-rating has left to run.

Macquarie has a revised price target of $114, a figure that sits well below the current trading level of approximately $159.40 but represents a less bearish stance than some peers.

Filip Tortevski, a technical analyst at Wealth Within, offered a more cautionary view. Tortevski characterised CBA’s post-2020 momentum as resembling a technology stock and pointed to historical precedents: an approximately 60% decline during the Global Financial Crisis and an approximately 44% fall between 2015 and the COVID-era low.

Tortevski described Wednesday’s sell-off as “potentially the first significant warning sign of an emerging correction cycle,” with a downside scenario targeting approximately $95, representing roughly 50% from recent highs.

| Analyst / Firm | Price Target | Implied Move from $159.40 |

|---|---|---|

| Macquarie | $114 | -28.5% |

| Filip Tortevski, Wealth Within | ~$95 (downside scenario) | -40.4% |

| UBS (pre-result) | $96.07 | -39.7% |

No updated price targets or rating changes from UBS, Morgan Stanley, Goldman Sachs, or Citi have been publicly confirmed in direct response to the 13 May update. The full picture of institutional broker positioning remains incomplete at the time of writing.

Investors wanting to quantify how far the current price remains from model-implied fair value will find our full explainer on CBA’s intrinsic value estimates, which runs three DDM scenarios (including a franking-adjusted gross dividend case), benchmarks the current PE against the 10-year historical median, and compiles every major broker price target published as of May 2026.

Three forces converged to produce this week’s record fall: a modest Q3 profit dip, a forward-looking provision signal that told investors management sees rising uncertainty, and a valuation starting point that had priced in almost no room for disappointment. None of these alone would have generated a 10.4% single-session decline. Together, they did.

The uncertainty is honest. No post-result executive commentary from CBA has been publicly confirmed, and broker updates are still emerging. The $159.40 close on Thursday represents a partial recovery, not a resolution.

CBA’s trailing fully-franked dividend yield of 3.11% and a CET1 capital ratio of 11.6% provide context for the bank’s underlying financial position, though neither eliminates the risk of further valuation adjustment.

For long-term holders, the question is whether Wednesday marked a one-off re-rating or the beginning of a larger correction cycle. That question cannot be answered with the information available today.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.

Three forces combined to produce the record fall: a modest 1% quarterly profit dip, a deliberate build in collective loan-loss provisions signalling management's concern about macroeconomic uncertainty, and a starting valuation of approximately 28.5x forward earnings that left no room for disappointment.

A collective provision is money a bank sets aside against loans that have not yet defaulted but that management believes carry elevated future risk. When a bank raises its collective provision, the increase is charged as an expense through the income statement, directly reducing reported cash profit for that period.

CBA reported a CET1 capital ratio of 11.6% in its Q3 FY2026 update, which sits well above the APRA regulatory minimum of 10.5% and indicates the bank has maintained a meaningful capital buffer even while absorbing the provision build during the quarter.

Macquarie holds a revised price target of $114, implying a further decline of around 28.5% from the $159.40 close on 15 May 2026. UBS had a pre-result Sell target of $96.07, while technical analyst Filip Tortevski at Wealth Within cited a downside scenario of approximately $95, representing roughly 40% below that closing price.

Heading into the Q3 update, CBA traded at approximately 28.5x forward earnings and around 4x book value, compared to 10-14x forward earnings and 1.0-1.5x book value for most domestic and global banking peers, making it one of the most expensively valued major banks in the world.