CBA Share Price Falls 10.4% in Largest Single-Day Drop on Record

1 hr ago

On 12 May 2026, Treasurer Jim Chalmers handed down an Australian Federal Budget that dismantled investment tax settings unchanged for decades. Three reforms arrived in a single announcement: the 50% capital gains tax discount replaced by cost-base indexation, negative gearing restricted on residential property, and a new 30% minimum tax rate imposed on discretionary trust distributions. For millions of Australian property investors, share investors, SMSF trustees, and trust beneficiaries, the tax environment shifted in one evening. Some trigger dates have already passed. This article explains each reform, identifies who is affected and from when, and outlines the practical steps investors should be considering now.

The 2026-27 Federal Budget did not adjust a single tax lever. It moved three at once, each targeting a different mechanism Australian investors have relied on to manage the tax burden on investment returns.

The three measures share a common thread: each reduces a tax benefit that has been available to investors holding property, shares, or trust structures. Taken together, they represent a connected reconfiguration of how investment returns are taxed in Australia, not three separate tweaks.

The combined decade-long revenue impact of the three reforms is estimated at $77 billion, a figure that frames the scale of the structural shift and explains why the Government views these measures as a durable reconfiguration rather than a marginal revenue adjustment.

Gemma Dale, Director of SMSF and Investor Behaviour at nabtrade, described the reforms as among the most significant changes to investment taxes in recent years. (nabtrade Insights, 13 May 2026)

Some decisions cannot be deferred. The budget date itself, 12 May 2026, serves as the trigger for the negative gearing restriction, meaning the clock started four days ago.

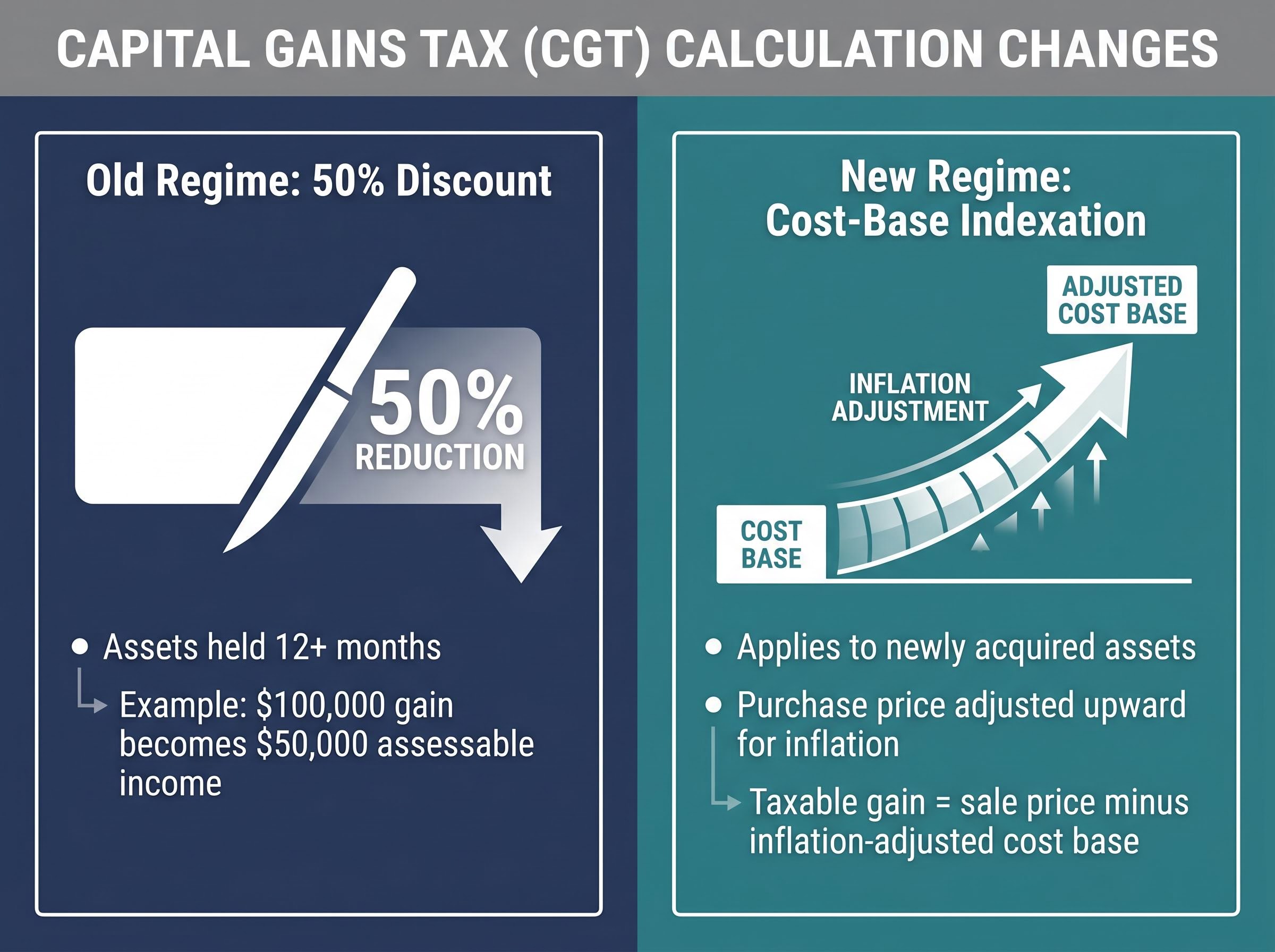

For more than two decades, Australian investors who held an asset for at least 12 months before selling could halve the taxable capital gain. A $100,000 gain became $50,000 in assessable income, regardless of how long the asset was held or what inflation did to the cost base over that period.

That mechanism is now replaced for newly acquired assets. Under cost-base indexation, the purchase price of an asset is adjusted upward in line with inflation before the gain is calculated. The taxable gain is the difference between the sale price and the inflation-adjusted cost base, not the raw purchase price.

The reform is forward-looking. Assets already held retain their existing CGT treatment. The change applies to new acquisitions under the 2026-27 and 2027-28 financial year implementation framework, according to the Budget Papers published at budget.gov.au.

| Feature | Old Regime (50% Discount) | New Regime (Cost-Base Indexation) |

|---|---|---|

| How the gain is calculated | Taxable gain halved by 50% flat discount | Cost base adjusted for inflation; gain is sale price minus indexed cost |

| Who it applies to | All assets held 12+ months (existing holdings) | New asset acquisitions post-budget |

| When it takes effect | Remains for pre-budget assets | 2026-27 / 2027-28 financial year framework |

For long-term share investors and SMSF trustees, the outcome depends on the inflation environment. In low-inflation periods, indexation may produce a smaller reduction than the flat 50% discount. In higher-inflation periods, the indexed cost base rises faster, and the taxable gain could be lower. Neither outcome can be assumed without modelling specific scenarios.

The trigger date has already passed. Residential properties purchased after 12 May 2026, the night the budget was delivered, will lose negative gearing benefits from 1 July 2027 in most cases. Both new and existing residential properties acquired after the budget date are caught by the restriction, not only new builds.

Three investor cohorts now face different positions:

The grandfathering provisions are date-specific. Properties settled before budget night retain their treatment indefinitely under the current framework published at budget.gov.au. The phased implementation across the 2026-27 and 2027-28 financial years, confirmed in Perpetual Private analysis dated 13 May 2026, gives investors purchasing in the transitional window limited time before the restriction applies.

The grandfathering provisions are date-specific, and the full terms covering both the CGT indexation change and the negative gearing restriction are set out in the Budget Papers at budget.gov.au, which confirm that properties settled before budget night retain their treatment indefinitely under the current published framework.

The loss of negative gearing offsets changes the cash flow arithmetic on leveraged property investment. Investors considering new residential property purchases now face a structurally different cost-benefit calculation and will need to reassess expected net returns on any acquisition made from this point forward.

A critical distinction embedded in the new rules is that the negative gearing ring-fence applies differently to established properties versus new builds, with full deductibility against all income preserved for new residential construction as a deliberate supply-side incentive, meaning the after-tax case for new builds has materially strengthened relative to established stock.

Discretionary trusts, commonly known as family trusts, have historically given trustees flexibility over how investment income is distributed among beneficiaries. A trustee could direct income to a beneficiary on a lower marginal tax rate (an adult child, a retired spouse, or a family member with limited other income) and reduce the overall tax paid by the family group on that investment return. This practice, known as income splitting, has been one of the primary tax-efficiency advantages of holding investments through a discretionary trust structure.

The 2026-27 Budget introduces a 30% minimum tax rate on distributions from discretionary trusts.

30% minimum tax rate on discretionary trust distributions, regardless of the marginal rate of the beneficiary receiving the distribution. (Source: budget.gov.au Budget Papers)

Under the reform:

Implementation sits within the 2026-27 and 2027-28 financial year framework, according to the Budget Papers and analysis from both nabtrade and Perpetual Private published on 13 May 2026.

For the significant number of Australian self-managed investors and family wealth structures using discretionary trusts, this reform removes one of the core tax-efficiency levers the structure has provided. Beneficiaries who have been receiving distributions at rates below 30% will face a materially higher tax burden on those same distributions going forward.

Three simultaneous reforms require a structured response rather than piecemeal reactions. The following steps reflect the order in which decisions are most time-sensitive:

nabtrade Insights (Gemma Dale, 13 May 2026) and Perpetual Private analysis (13 May 2026) both provide publicly available investor-focused coverage of all three reforms for those seeking immediate detail.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

The budget announcement is not the final word. Legislation enacting the three reforms has not yet passed parliament and will proceed through the standard legislative process, meaning detail may be refined before the measures become law.

ATO technical guidance, SMSF Association commentary, and Tax Institute analysis are all expected to emerge in the weeks following the budget as the profession responds. The phased implementation timelines across 2026-27 and 2027-28 mean some investors retain a window to act before restrictions fully apply.

Investors exploring how the changed tax settings alter the relative appeal of shares versus property will find our deep-dive into how the CGT reforms affect ASX equities, which examines why margin lending and franking credits make listed equities structurally better positioned under the new framework and which ASX stock types face the smallest after-tax return reduction.

| Reform | Trigger Date | Effective Date |

|---|---|---|

| CGT: cost-base indexation replaces 50% discount | New acquisitions post-budget | 2026-27 / 2027-28 FY framework |

| Negative gearing restrictions | Properties purchased after 12 May 2026 | 1 July 2027 (most cases) |

| 30% minimum tax on discretionary trust distributions | Budget announcement 12 May 2026 | 2026-27 / 2027-28 FY framework |

Understanding that this is an evolving legislative situation, not a finalised rulebook, is itself actionable information. Investors who engage with professional advice now are better positioned to respond as implementing legislation and ATO guidance clarify the precise rules.

The three reforms operate together. An investor who holds residential property, shares, and a discretionary trust structure faces compounding changes to their tax position, not a single adjustment.

The 2026-27 financial year is a transition year. Decisions made during this period, whether to acquire property, purchase new assets, or distribute trust income, will carry long-term tax consequences under the reformed framework. Professional advice is the most important step before any significant investment action.

Investors should consult a registered tax adviser or financial planner familiar with the Budget Papers before making acquisition, disposal, or trust distribution decisions. Legislative updates and ATO guidance will continue to emerge at budget.gov.au as the implementation process advances.

Past performance does not guarantee future results. These reforms are subject to legislative passage and may be refined during the parliamentary process.

Cost-base indexation adjusts the original purchase price of an asset upward in line with inflation before calculating the capital gain, meaning you are only taxed on the real gain above inflation rather than receiving a flat 50% discount on the total gain. This new method applies to assets acquired after the 2026 Federal Budget and replaces the longstanding 50% CGT discount for newly purchased assets.

Residential properties purchased after 12 May 2026 will lose negative gearing benefits from 1 July 2027, while properties already owned before budget night are grandfathered and retain their existing negative gearing treatment indefinitely. New residential construction is treated differently, with full deductibility against all income preserved as a supply-side incentive.

Under the 2026-27 Budget reform, all distributions from discretionary trusts are subject to a minimum 30% tax rate regardless of the individual beneficiary's personal marginal tax rate, eliminating the income-splitting advantage where trustees could previously direct income to low-income beneficiaries taxed at 0% or 19%. The measure is being implemented within the 2026-27 and 2027-28 financial year framework.

Investors should first confirm whether any residential property contracts signed after 12 May 2026 fall under the new negative gearing restriction timeline, then model CGT outcomes under cost-base indexation for any planned new asset purchases, and review discretionary trust distribution strategies with a registered tax adviser before the 2026-27 financial year begins.

No, the three reforms announced in the 2026 Federal Budget have not yet passed parliament and will proceed through the standard legislative process, meaning details may be refined before they become law. Investors are advised to monitor ATO guidance and Budget Papers at budget.gov.au as implementing legislation progresses.