Why a Rising AUD Is Quietly Eroding Your International ETF Returns

11 hrs ago

A 36% tax on profits that have not been received, levied on assets that have not been sold. That is what Dutch residents will face from 2028 under legislation the lower house of parliament passed in February 2026. The Netherlands is not the first country to wrestle with how to tax investment wealth, but it is among the first in the developed world to move this far toward taxing paper profits at this rate. The proposal emerged from a court ruling that struck down the prior Dutch tax regime for taxing fictitious rather than actual returns, forcing a legislative rethink that has produced something more radical than the system it replaced. What follows explains what unrealised capital gains taxation actually means in practice, how the Dutch system is designed to work, what the Senate’s 36 pages of questions reveal about unresolved problems, and what investors outside the Netherlands should make of the direction of travel.

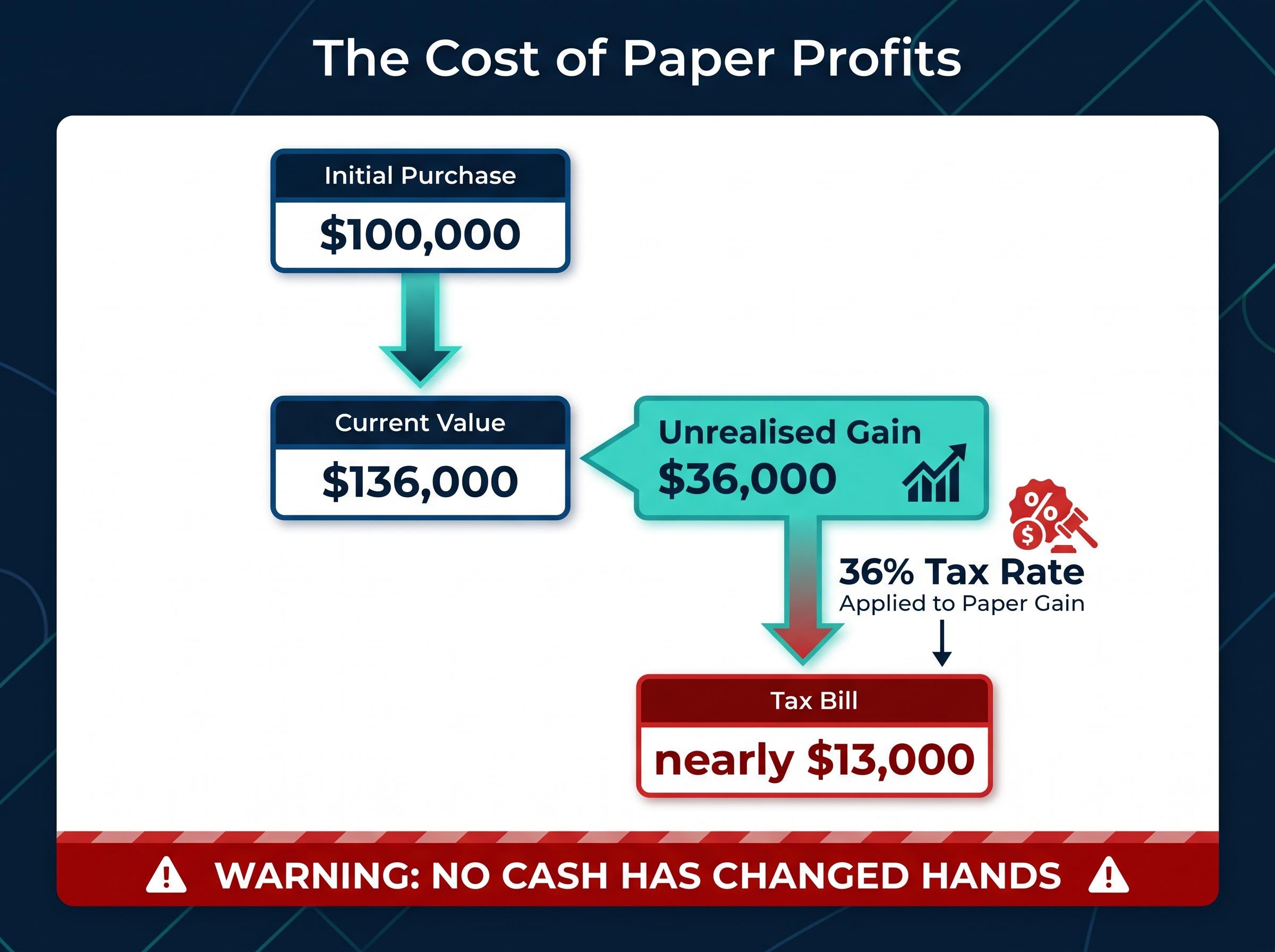

Consider an investor who bought shares for $100,000. Those shares are now worth $136,000. Under a conventional capital gains tax, nothing happens until the investor sells. The $36,000 gain is unrealised: it exists on a brokerage statement, not in a bank account.

Under the Dutch proposal, that $36,000 paper gain would be taxable at 36%, producing a tax bill of nearly $13,000, even though no sale has occurred and no cash has changed hands. The investor owes real money on theoretical profit.

This is the core tension. The tax liability is immediate and enforceable, but the asset generating it may be illiquid, difficult to value precisely, or declining in value by the time payment is due. The prior Dutch regime was struck down by courts precisely because it taxed assumed returns rather than actual ones. The replacement, paradoxically, taxes actual (but unrealised) gains, a different mechanism with its own set of frictions.

The distinction between realised and unrealised taxation is worth making explicit:

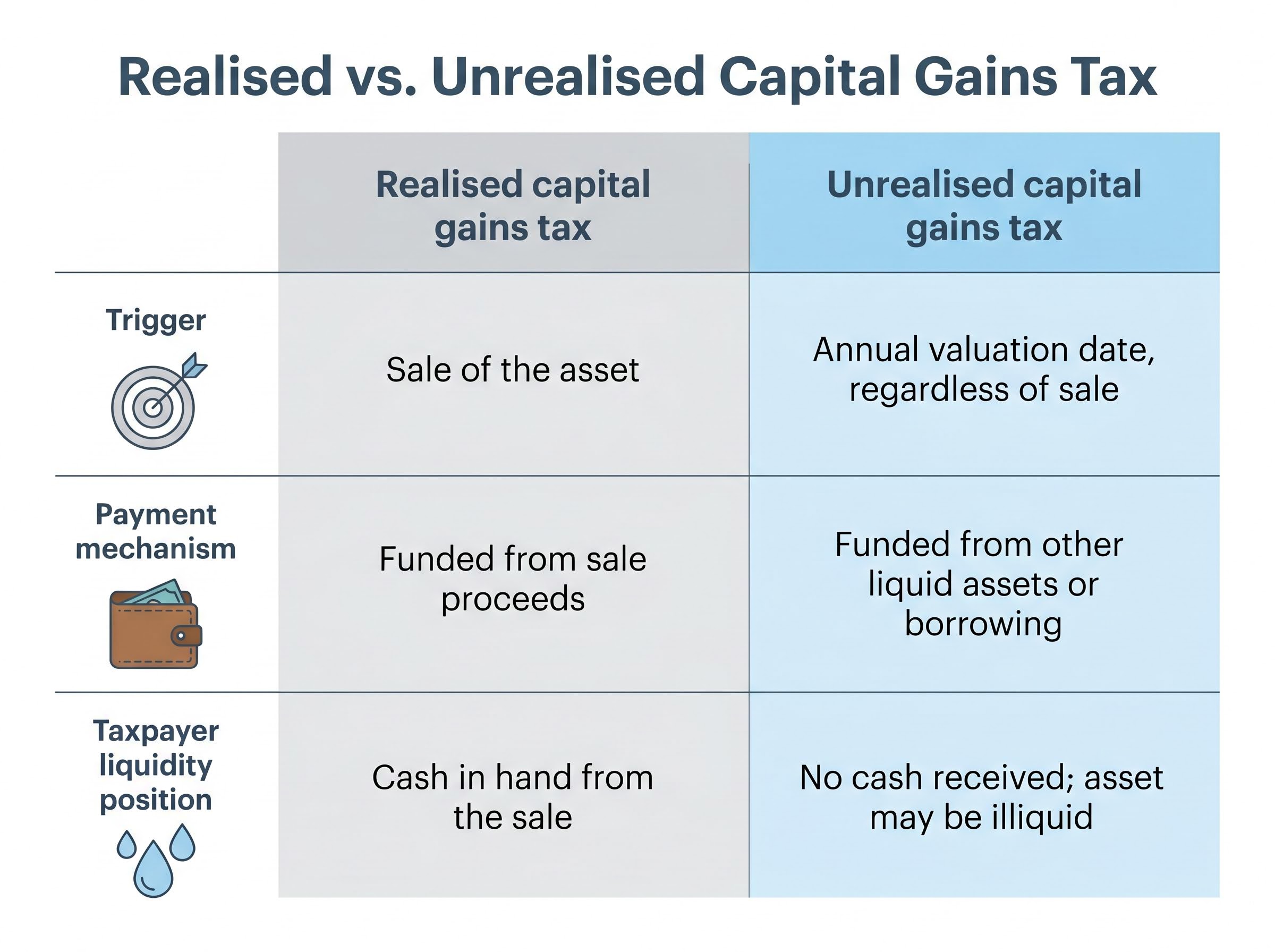

| Feature | Realised capital gains tax | Unrealised capital gains tax |

|---|---|---|

| Trigger | Sale of the asset | Annual valuation date, regardless of sale |

| Payment mechanism | Funded from sale proceeds | Funded from other liquid assets or borrowing |

| Taxpayer liquidity position | Cash in hand from the sale | No cash received; asset may be illiquid |

Understanding this distinction is the foundation for everything that follows. Readers who conflate the two will misread both the Dutch proposal and any future proposals in their own markets.

The Dutch proposal did not emerge from ideological ambition. It was forced into existence by a sequence of constraints, each narrowing the government’s options until the current design was what remained.

The Senate is now scrutinising the bill. On approximately 29 April 2026, Bloomberg reported that senators had submitted 36 pages of questions to Tax Minister Eelco Eerenberg, a volume that signals the upper chamber’s concerns go well beyond procedural formality.

Prime Minister Rob Jetten has publicly framed the unrealised gains tax as an interim measure, pending a transition to a conventional realised gains structure.

That framing matters. Even the government presenting the legislation characterises it as temporary, an acknowledgement that the design is a product of political constraint rather than policy preference. The Finance Ministry has ruled out a full legislative rewrite before the 2028 effective date, meaning the current structure will proceed with targeted modifications at most.

The tax applies to Dutch-resident taxpayers on unrealised gains across their investment portfolios. International investors holding Dutch securities are not directly subject to it.

A carveout exists for startup equity. Employees compensated with equity in companies operating for five years or fewer with annual revenues below 30 million euros currently qualify for conventional realised-gains treatment. A broader definition of qualifying startups is under consideration.

The proposed legislation includes a loss carryback mechanism designed to address the most visible objection: that investors might pay tax on gains that subsequently evaporate.

The mechanism does not, however, solve the immediate liquidity problem at the point the tax bill arrives. An investor holding illiquid assets, such as private company shares, real estate, or thinly traded securities, may not have the cash to pay the levy when it falls due. The refund comes later. The bill comes now.

Bloomberg reported on approximately 29 April 2026 that the Dutch Senate submitted 36 pages of questions to Tax Minister Eelco Eerenberg on the unrealised gains tax proposal, an unusually extensive submission that reflects the depth of unresolved concerns.

The Dutch Senate occupies a specific constitutional position: it cannot amend legislation directly. It can only return bills with questions and, ultimately, accept or reject them. A 36-page question document is not routine procedural correspondence. It is the Senate’s strongest available signal that the legislation, in its current form, presents problems the government has not adequately addressed.

The Dutch Senate legislative record for the proposal, published on the Eerste Kamer’s official wetsvoorstel register, documents the full text of the bill, the Senate’s submitted questions, and the government’s responses, providing the primary source for tracking how the scrutiny process unfolds ahead of the 2028 effective date.

Four categories of concern dominate the scrutiny:

| Challenge | Investor scenario | Addressed in current draft? |

|---|---|---|

| Liquidity constraints | Investor holds illiquid assets and lacks cash to pay the tax bill on paper gains | Partial (loss carryback exists, but does not provide upfront liquidity) |

| Valuation of illiquid holdings | Investor holds private company shares or thinly traded assets with no reliable market price | No (no standardised valuation methodology specified) |

| Loss carryforward treatment | Investor incurs losses that exceed gains in a given year and needs clarity on how these are treated across tax periods | Partial (mechanism exists but details remain under review) |

| Forced asset sales | Investor must sell holdings to generate the cash needed to pay the tax, potentially at depressed prices | No (no structural safeguard against forced liquidation) |

The Finance Ministry has committed to targeted adjustments rather than a full rewrite, meaning the architecture of the proposal will remain intact. The unresolved questions are not bureaucratic detail. They represent the real-world conditions under which some investors, particularly those with concentrated or illiquid portfolios, will face significant financial stress. The gap between the tax’s legal structure and its practical enforceability is the central risk for affected taxpayers.

The honest answer is that the evidence supports alertness, not certainty.

The fiscal pressure on investment wealth that is driving tighter capital gains frameworks across developed markets does not exist in isolation: the IMF Fiscal Monitor has recommended progressive wealth taxes across G20 economies as a response to asset price inflation dynamics that monetary tightening alone has failed to correct.

The Dutch proposal did not emerge in isolation. Governments across developed markets face fiscal pressure and are scrutinising how investment income is taxed. Whether that scrutiny leads elsewhere toward the unrealised gains model or toward tighter conventional frameworks depends on jurisdiction-specific politics, court constraints, and fiscal need.

Several recent developments illustrate the range of approaches:

The Australian CGT reform announced in the 2026 Federal Budget illustrates how governments can tighten investment taxation significantly while remaining within the realised-gains framework, replacing the longstanding 50% discount with inflation indexation and a 30% minimum effective rate from 1 July 2027.

The limits of direct comparison are real. The Netherlands arrived at its proposal because a constitutional court ruling eliminated the prior regime, not because a government chose the unrealised gains model on its merits. That makes it an imperfect template for jurisdictions without the same legal pressure.

The question for investors outside the Netherlands is not whether their own government will copy the Dutch model. It is whether the fiscal pressures and political logic driving the proposal are present in their own jurisdiction. In most developed markets, to varying degrees, they are.

The constitutional dimension of taxing paper profits remains unsettled in the United States, where the Supreme Court’s 2024 ruling in Moore v. United States deliberately left questions of unrealised gains constitutionality open, preserving the legal ambiguity that any future federal proposal would need to navigate.

The 2028 implementation date transforms the Netherlands from a policy debate into a live experiment. No developed-market government has previously attempted unrealised gains taxation at this scale on a modern, diversified investor population. The results will be cited in tax policy conversations globally for years.

Three propositions will be tested in real time:

Capital migration patterns in 2026 are already sorting sharply across geographies for reasons beyond tax policy, with AI-driven semiconductor investment and dollar feedback loops concentrating flows into US equities while European segments face structural headwinds including sluggish eurozone growth and elevated energy costs.

Dutch equity markets have remained positive since the lower house passage in February 2026, suggesting the market does not currently price in severe structural damage. Investor behaviour in the period between now and the 2028 effective date will be the more informative signal: portfolio restructuring, wealth management relocation flows, and any legal challenges filed before the tax takes effect.

Prime Minister Rob Jetten has described the unrealised gains tax as explicitly interim, pending a shift to a realised gains model, a signal that even the government presenting the legislation expects the current design to be replaced.

If the Dutch system produces widespread forced sales, capital flight, or successful legal challenges before 2028, other governments considering tighter investment taxation are likely to recalibrate toward realised-gains models rather than pursuing the unrealised approach.

The Netherlands’ unrealised capital gains tax is not a policy curiosity confined to one small European economy. It is a working prototype, however imperfect, for how governments under fiscal pressure might approach investment taxation when political and legal constraints narrow their options.

For affected Dutch-resident investors, the practical risks remain unresolved: liquidity at the point the tax bill arrives, valuation disputes for illiquid holdings, and the possibility that the tax structure forces asset sales at unfavourable prices. The Senate’s 36 pages of questions are a measure of those gaps.

For investors elsewhere, the period between now and 2028 will be more instructive than the legislative debate itself. How Dutch residents restructure their portfolios, whether capital migrates, and whether the administrative machinery can handle the complexity of marking diverse assets to market annually: these outcomes will shape tax policy conversations in every developed market that faces the same fiscal arithmetic.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements regarding tax implementation timelines and policy outcomes are subject to change based on legislative developments, court rulings, and political conditions.

The Netherlands unrealised capital gains tax is a 36% levy on paper profits from investment portfolios, meaning Dutch-resident taxpayers owe tax on gains that exist on paper each year, even if they have not sold any assets and received no cash.

The legislation passed the Dutch lower house in February 2026 and is scheduled to take effect from 2028, though the Senate is currently scrutinising the bill and the government has indicated the design may be an interim measure pending a shift to a conventional realised gains framework.

Only Dutch tax-resident individuals are directly subject to the 36% levy; international investors holding Dutch securities are not affected, and a carveout exists for employees holding equity in startups operating for five years or fewer with annual revenues below 30 million euros.

The proposed legislation includes a loss carryback mechanism that allows investors to claim a refund for tax already paid on gains that subsequently evaporate, though this does not solve the immediate liquidity problem of paying a tax bill before receiving any cash from a sale.

While no other developed market has matched the Dutch model directly, Australia announced a minimum 30% capital gains tax rate from 2027 using the realised gains framework, and fiscal pressures across developed markets are pushing governments to scrutinise investment taxation more broadly, making the Dutch experiment a closely watched policy test case.