Why the Mid-Cap Rotation Beat Mega-Cap Tech in June 2026

12 mins ago

The IRS does not tax a single dollar of unrealized gains under current law. Yet a single Biden-era proposal and one Supreme Court decision that deliberately left the question open have made the concept a live concern among wealth-preservation-minded investors. As of May 2026, the policy environment has moved in the opposite direction, with the Trump administration pursuing capital gains tax cuts rather than expansion. The constitutional question left unresolved by Moore v. United States (2024) and active state-level developments, however, keep the unrealized capital gains tax on the analytical agenda for long-term investors and financial planners. What follows maps the specific mechanics of such a tax, where the legal and legislative lines currently sit, how a parallel historical risk has resurfaced in investment commentary, and what strategies are being examined in response.

Under current U.S. tax law, gains exist on paper until a sale triggers a taxable event. This is the realisation principle, and it is foundational. IRS Topic 409 and Publication 544 (updated 2025) confirm that unrealized appreciation is not subject to capital gains liability until the asset is sold or otherwise disposed of.

IRS Publication 544 confirms that unrealized gains are not currently taxable. Capital gains tax liability arises only upon realisation, typically through a sale or exchange of the appreciated asset.

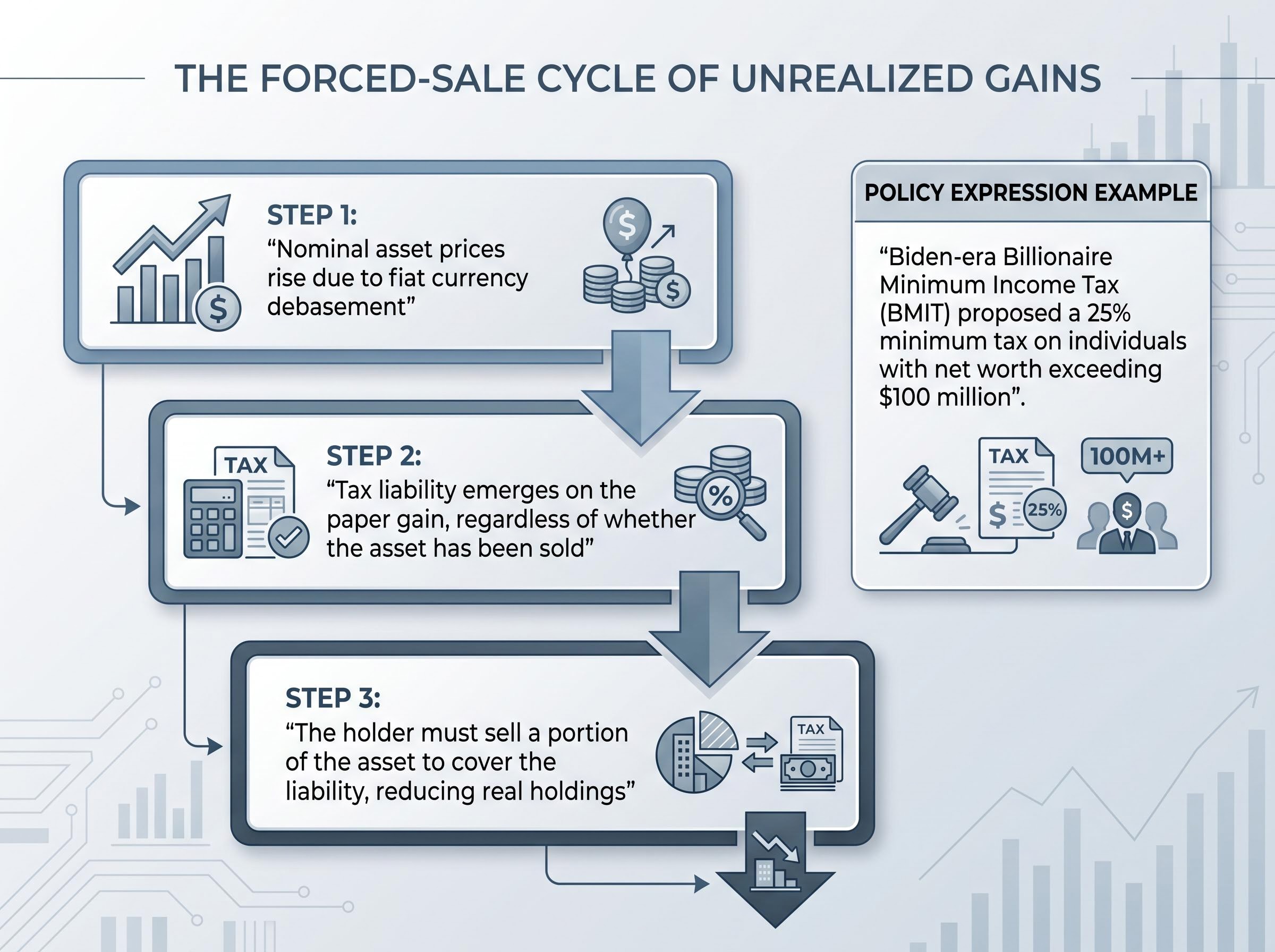

The Biden administration’s proposed Billionaire Minimum Income Tax (BMIT) would have removed that deferral for individuals with net worth exceeding $100 million, imposing a 25% minimum tax on unrealized gains across stocks, bonds, and real estate. Exclusions were debated for primary residences and qualified small business stock. The proposal was never enacted.

The distinction from a wealth tax matters. A wealth tax assesses total net worth. An unrealized gains tax targets the annual change in asset values, creating a specific mechanism: as fiat-driven nominal prices rise, annual tax bills on paper gains force asset sales to cover liabilities. That compulsory divestiture cycle is the damage pathway.

The asymmetry across asset types is pronounced. Liquid securities, with observable daily prices, are far more exposed to an annual mark-to-market regime than illiquid holdings.

Annual taxation of illiquid assets creates a persistent dispute: what is a private business interest, a real estate partnership, or a piece of art worth on any given assessment date? No readily observable annual price exists for these holdings.

Every legislative proposal in this space has struggled to define a workable methodology. The IRS and taxpayers would face recurring disagreements over fair market value, and the administrative burden of resolving those disputes at scale remains one of the primary practical obstacles to implementation.

No federal unrealized capital gains tax exists. The current administration’s direction is explicitly toward cuts, not expansion. The 119th Congress is debating capital gains indexing for inflation and rate reductions, not new taxation mechanisms.

The constitutional picture is less settled. In Moore v. United States (2024), the Supreme Court upheld a specific repatriation tax but ruled narrowly.

The Court in Moore v. United States explicitly declined to resolve the broader question of whether taxing unrealized gains is constitutionally permissible under the Sixteenth Amendment. That question remains legally undecided as of May 2026.

The Biden-era BMIT was proposed but never passed by Congress. It does not represent current law.

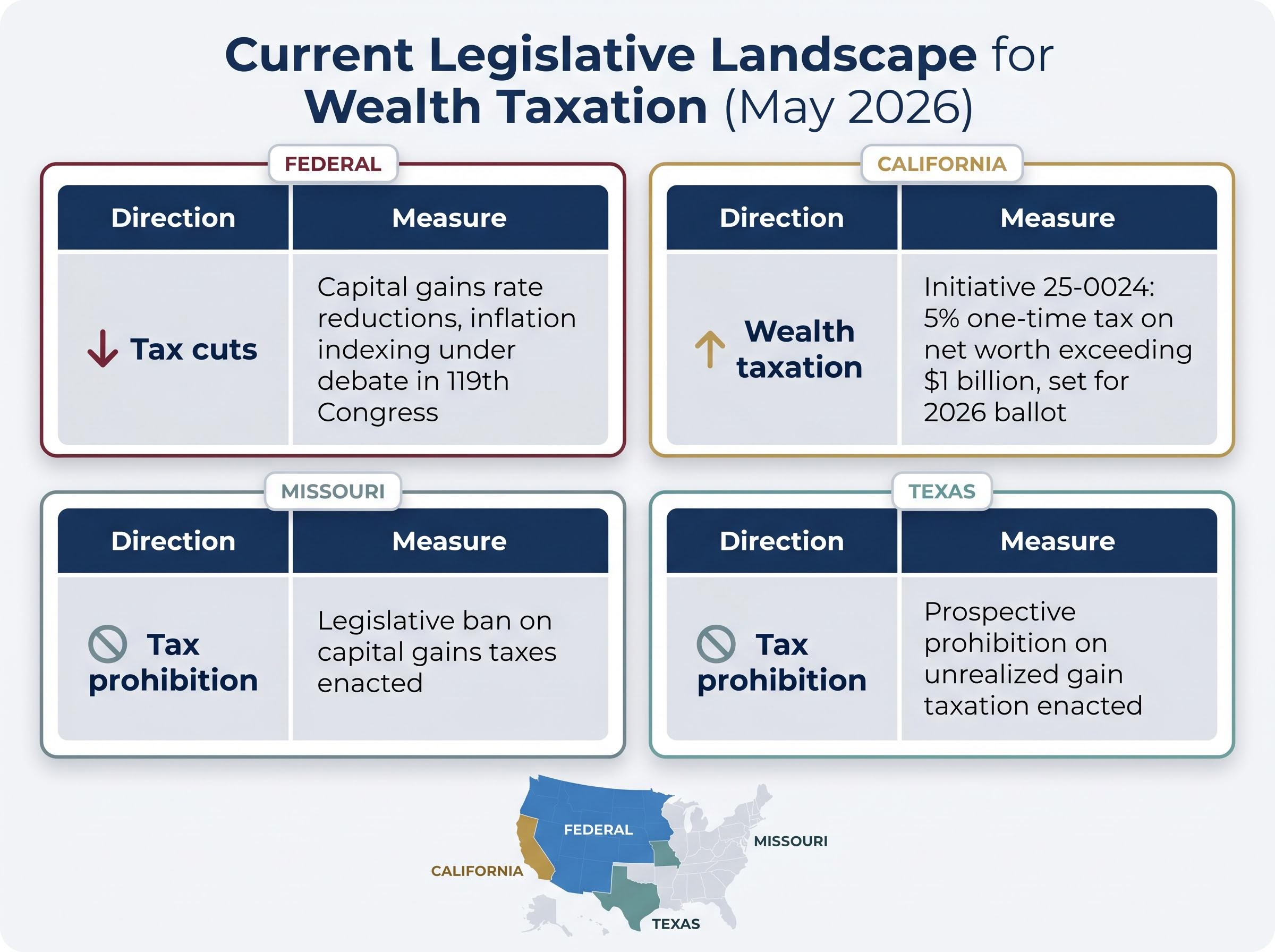

At the state level, the landscape is moving in both directions simultaneously. The table below maps the divergence.

| Jurisdiction | Direction of travel | Specific measure | Status |

|---|---|---|---|

| Federal | Tax cuts | Capital gains rate reductions, inflation indexing | Under congressional debate |

| California | Wealth taxation | Initiative 25-0024: 5% one-time tax on net worth exceeding $1 billion | Set for 2026 ballot |

| Missouri | Tax prohibition | Legislative ban on capital gains taxes, including unrealized gains | Enacted |

| Texas | Tax prohibition | Prospective prohibition on unrealized gain taxation | Enacted |

The gap between the policy conversation and the actual legal landscape is wide. The Committee for Responsible Federal Budget has estimated that the administration’s proposed cuts could add approximately $1 trillion to the national debt, a fiscal reality that could revive revenue-expansion proposals under a future administration. Investors who mistake advocacy commentary for enacted law risk misallocating protective strategies.

The analytical thread linking unrealized gains taxation and physical asset seizure is currency debasement. When fiat-driven nominal prices inflate asset values, an unrealized gains tax converts that inflation into a tax liability, even when no real wealth has been created.

The forced-sale cycle operates in three steps: 1. Nominal asset prices rise due to fiat currency debasement 2. Tax liability emerges on the paper gain, regardless of whether the asset has been sold 3. The holder must sell a portion of the asset to cover the liability, reducing real holdings

This mechanism operates without any deliberate confiscation intent. The erosion occurs through the tax code rather than executive order. The Biden-era BMIT, had it been enacted, would have been the concrete policy expression of this cycle for individuals with net worth exceeding $100 million.

The Dow-to-gold ratio illustrates the gap between nominal and real performance. At the time of recent source commentary, the ratio stood near 6-6.5, down from a 1999 peak of approximately 45. Measured in gold ounces rather than dollars, equity performance over the past quarter-century looks materially different.

A countervailing force exists. Proposals to index capital gains for inflation, currently under discussion in the 119th Congress, would partially offset this dynamic:

The connection between currency debasement and nominal-gains taxation is why finance-minded investors treat these as related risks rather than two separate policy debates.

Inflation-linked positioning, including allocations to Treasury Inflation-Protected Securities, real assets, and physical gold, represents the category of tools most directly responsive to the fiat-debasement-driven nominal gains risk the BMIT would have accelerated, because each of those instruments is designed to hold real value when currency purchasing power declines.

Executive Order 6102, signed in April 1933, required most U.S. citizens to deliver gold coins, bullion, and certificates to the Federal Reserve at $20.67 per troy ounce. The legal authority came from the Trading with the Enemy Act of 1917, as amended by the Emergency Banking Act of 1933. Exemptions covered jewellery, dental use, industrial and artistic use, and coin collections up to $100 face value.

Private gold ownership remained banned from 1933 until 1 January 1975, when President Ford restored the right. Today, gold is legal to own in all forms and is classified by the IRS as a collectible, subject to a 28% maximum long-term capital gains rate, compared with 20% for most other assets.

Central bank gold accumulation at the sovereign level reflects the same systemic motivation that made private gold reserves strategically significant in 1933: institutional actors are repositioning physical gold as a monetary hedge outside the fiat system, a behaviour pattern that underpins the current elevated price environment.

The gold standard context was structurally necessary to the 1933 order. The government needed private gold reserves to manage monetary policy under a system where the currency was convertible to gold. That structural dependency has no equivalent under the current fiat system.

The following framework isolates the conditions that would need to be present for a comparable action today:

The 1933 precedent is real, but its conditions were structurally specific. The fiat monetary structure removes the primary systemic motivation that existed at the time.

Three documented strategies have emerged in response to these interconnected risks, each addressing a different dimension of the exposure.

| Strategy | Risk addressed | Key legal consideration | Primary limitation |

|---|---|---|---|

| Physical asset conversion | Confiscation or seizure of bullion | 1933 exemptions covered jewellery, dental, industrial, and artistic use | No guarantee future exemptions mirror 1933 categories |

| Domestic jurisdictional planning | State-level unrealized gains taxation | Missouri and Texas prohibitions on capital gains taxes | Does not address federal-level exposure |

| International diversification | Single-jurisdiction concentration | Spreading assets across multiple legal systems | U.S. worldwide taxation of citizens |

The physical asset conversion strategy involves reframing bullion holdings into functional or decorative forms, such as jewellery, dishware, or sculpture, to fall under exemption categories that existed in 1933 and could recur in any future policy action. The logic is specific to confiscation risk rather than taxation risk.

Domestic jurisdictional planning leverages the divergence between states. Relocating to Missouri or Texas, where legislative bans on unrealized gains taxes are in place, addresses state-level exposure. It does not resolve federal-level risk.

A common misconception involves IRS Section 475, which permits a mark-to-market election for active traders. This is a narrow provision related to loss deductions and is unrelated to the broader wealth taxation proposals.

U.S. citizens owe federal taxes on worldwide income regardless of residence. Geographic relocation alone does not eliminate federal tax exposure; it is a partial solution rather than a complete one.

For those considering renunciation, the exit tax under IRC Section 877A applies to expatriating high-net-worth individuals. The strategic timing dimension is relevant: if exit tax regimes become more restrictive under future legislation, the window for tax-efficient expatriation could narrow. Each strategy carries distinct legal complexity and cost, and understanding which specific mechanism each addresses prevents investors from applying the wrong tool to their particular risk profile.

Investors exploring the mechanics of reducing appreciated positions without triggering avoidable tax events will find our full explainer on tax-efficient rebalancing execution, which covers the sequencing logic for new contributions, dividend redirection, tax-advantaged account sales, and taxable account liquidation, along with alternative capital destinations including private credit and market-neutral strategies.

Three observable developments would most significantly shift the risk calculation, ordered by near-term probability:

The Committee for Responsible Federal Budget has estimated that the current administration’s proposed capital gains tax cuts could add approximately $1 trillion to the national debt, creating fiscal conditions that could revive revenue-expansion proposals under a future administration.

The current policy direction reduces near-term federal risk. It does not resolve the constitutional ambiguity that Moore left open, and it does not prevent state-level experimentation from proceeding independently.

The unrealized capital gains tax risk is real as a policy concept. Constitutional ambiguity persists, and state-level experimentation is active. It is not, however, enacted federal law, and the current legislative direction is away from it.

The two risk mechanisms examined here, fiat-driven nominal gains taxation and physical asset seizure, share a common analytical thread rooted in currency debasement. Each requires a distinct legal and practical response. Conflating them or treating either as imminent without monitoring the specific signals leads to misallocated protective strategies.

The actionable monitoring framework is specific: track the California 2026 ballot initiative result and any future Supreme Court acceptance of a case directly testing unrealized gains constitutionality. These are the two nearest-term signals that would warrant recalibrating portfolio positioning.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. These statements regarding future legislative or judicial outcomes are speculative and subject to change based on political developments, market conditions, and legal proceedings.

An unrealized capital gains tax would impose a tax liability on the annual increase in asset values even if the asset has not been sold, removing the current realisation principle under which gains are only taxed upon sale or disposal. The Biden-era Billionaire Minimum Income Tax proposed a 25% minimum tax on unrealized gains for individuals with net worth exceeding $100 million, but it was never enacted.

No federal unrealized capital gains tax exists as of May 2026. Under current IRS rules confirmed in Publication 544, capital gains tax liability arises only when an asset is sold or exchanged, and the current administration is pursuing capital gains rate reductions rather than expansion.

The Supreme Court upheld a specific repatriation tax in Moore v. United States (2024) but ruled narrowly, explicitly declining to resolve whether taxing unrealized gains is constitutionally permissible under the Sixteenth Amendment, leaving that broader constitutional question legally undecided.

Missouri and Texas have both enacted legislative bans on capital gains taxes, including unrealized gains, while California has a measure on its 2026 ballot proposing a 5% one-time tax on net worth exceeding $1 billion, illustrating the divergence happening at the state level.

Investors are exploring three main approaches: converting physical assets like bullion into forms that may qualify for exemptions, relocating to states such as Missouri or Texas that prohibit unrealized gains taxes, and international diversification, though U.S. citizens remain subject to federal taxes on worldwide income regardless of where they reside.