Soft Payrolls, Sticky Wages: the Fed’s Dilemma in 2026

6 hrs ago

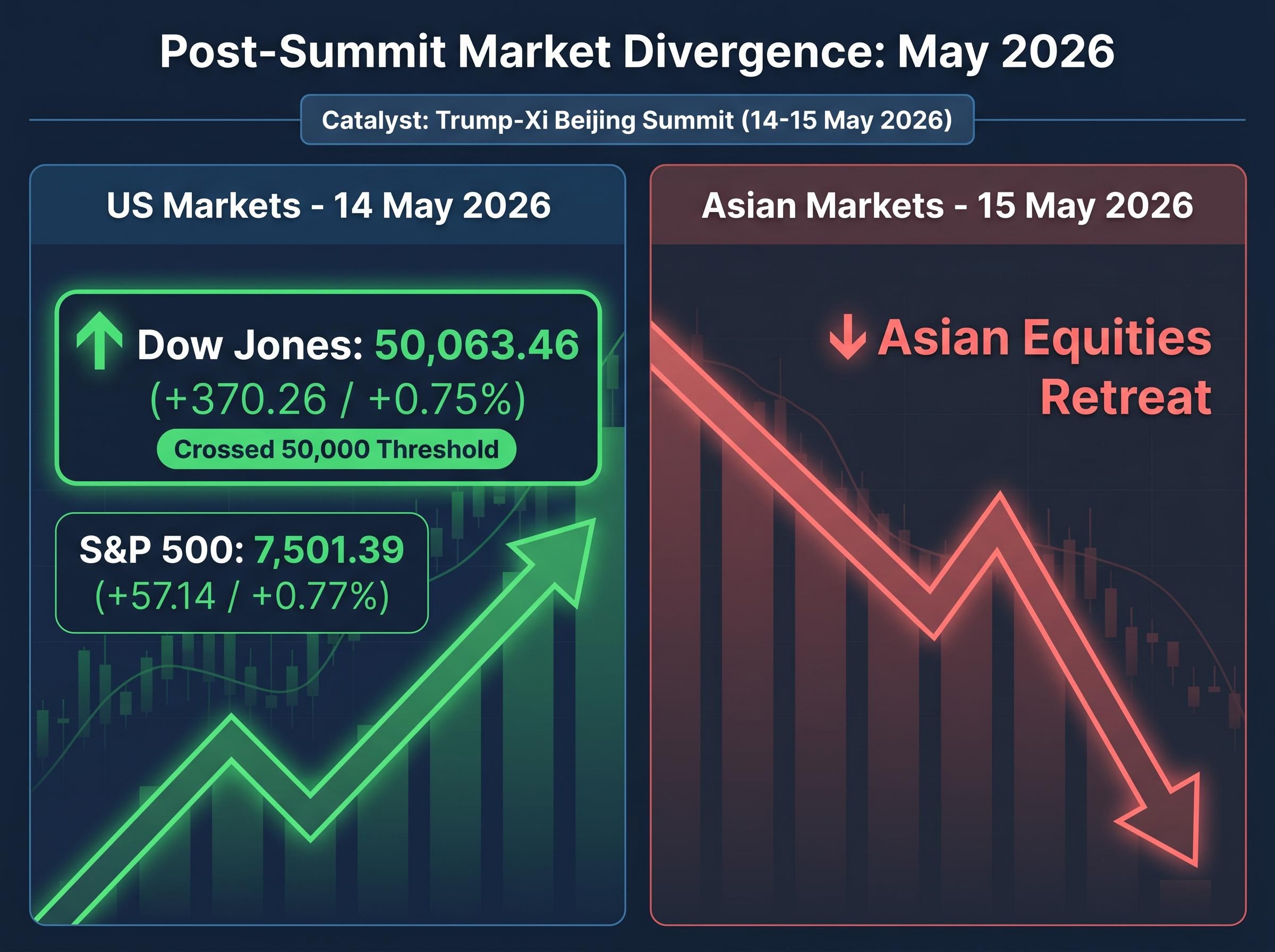

On 15 May 2026, the Dow Jones Industrial Average closed above 50,000 for the first time in months. Across the Pacific, Asian equities fell. Both moves traced back to the same event: the Trump-Xi bilateral summit in Beijing on 14-15 May 2026. That divergence, a rally and a retreat triggered by the same two days of talks, is the most honest market signal available about what the summit actually resolved and what it left open. The meeting covered trade stabilisation, Taiwan arms sales, semiconductor export controls, critical minerals, and Iran peace brokering, making it one of the most consequential geopolitical events of the year for investors. The backdrop included Operation Epic Fury, the US-Israel military operation that disrupted Strait of Hormuz shipping earlier in 2026 and amplified Beijing’s incentives to seek a deal. This analysis unpacks what happened across each issue area, maps the market reactions that followed, and provides an institutional-grade framework for interpreting what comes next across equities, energy, and currencies.

The confirmed agenda items from the 14-15 May bilateral spanned five distinct clusters:

Trade stabilisation was the headline outcome, and US equities responded accordingly. The Dow Jones closed at 50,063.46, up 370.26 points (+0.75%) on 14 May 2026. The S&P 500 finished at 7,501.39, gaining 57.14 points (+0.77%). S&P 500 Futures held at 7,525.25 as of 19:22 ET on 14 May, suggesting the rally had legs into the following session.

The tariff adjustment provided the floor. It did not define the ceiling.

InsightForward’s analysis of “Transactionalism and Great Power Politics” frames summits under this administration as nodes where tariffs, technology controls, Taiwan, and third-country conflicts can be linked in unexpected ways, creating both bundled breakthroughs and asymmetric risks that single-issue pricing misses entirely.

Each of the remaining four agenda items carries independent market-moving potential that the trade outcome does not neutralise. Investors who priced only the tariff headline on 14 May captured one variable out of five.

The divergence between confirmed outcomes and pre-summit market pricing is itself a data point: the Nasdaq rose approximately 1.1% and the Shanghai Composite hit its highest close since July 2015 on Day 1 optimism, pricing across all three agenda items simultaneously before any communique language had been confirmed.

Xi Jinping identified Taiwan as the single most critical matter to address with President Trump, issuing an explicit warning that mishandling the situation risks armed conflict. This was the clearest stated red line from the summit.

Xi’s warning on Taiwan constituted the most directly confrontational language of the two-day meeting, positioning the island’s status as a potential trigger for military escalation between the two largest economies.

Trump, for his part, indicated he intended to raise US arms sales to Taiwan during the talks, establishing an adversarial dynamic within the meeting itself. The result was a summit that simultaneously produced trade relief and heightened the military signalling around the Taiwan Strait.

The DSCA Taiwan Security Cooperation Initiative, established under US law and tracked through official program coding, provides the statutory framework within which any arms sales to Taiwan occur, meaning Trump’s stated intent to raise arms sales at the summit referenced a formalized policy channel with defined legal parameters rather than an ad hoc negotiating position.

Stalled versus resumed arms sales to Taiwan function as a proxy signal for the trajectory of US-China military deterrence. Lazard’s “Top Geopolitical Trends in 2026” analysis frames these decisions as trajectory signals: they affect broader Asian risk premia, not just defence-sector pricing.

Asian equities retreated on 15 May despite the trade optimism from the prior session, consistent with residual Taiwan and technology uncertainty. The directional framework supported across institutional analyses is direct: Taiwan escalation risk correlates with raised global risk premia, downside in Asian equities, and semiconductor sector pressure. For US investors with Asia-Pacific equity exposure, this is the variable most likely to drive sustained risk repricing, independent of whatever short-term relief the trade outcome provides.

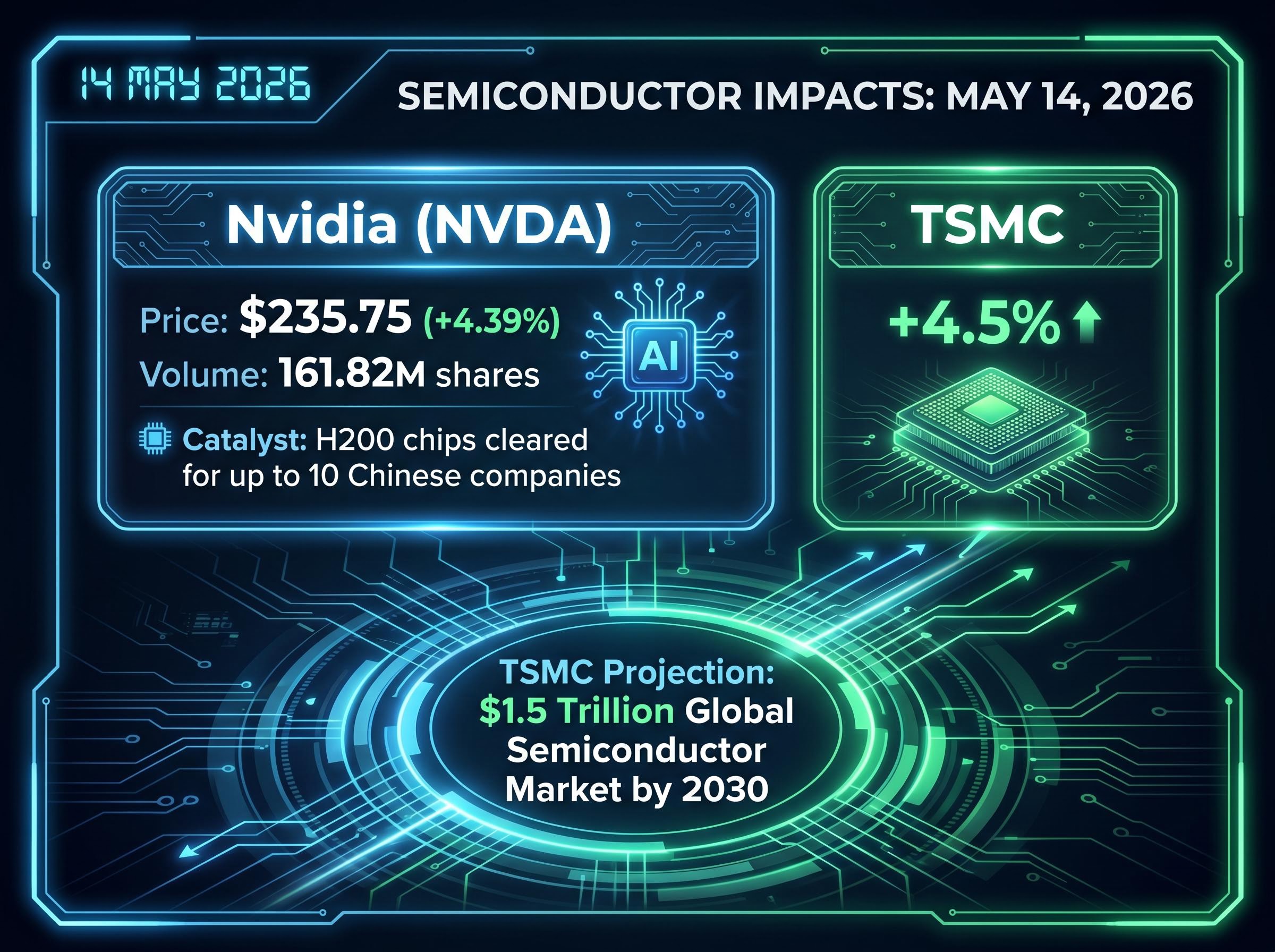

Nvidia shares surged more than 4% to an all-time high of $235.75 (+4.39%) on 14 May 2026, on volume of approximately 161.82 million shares. US-listed TSMC shares gained 4.5% on the same session. The catalyst: Reuters reported that US regulators had permitted Nvidia to sell H200 chips to as many as 10 Chinese companies, with Nvidia CEO Jensen Huang present in China alongside Trump during the summit week.

| Company | 14 May Move | Catalyst | Forward Risk Factor |

|---|---|---|---|

| Nvidia | +4.39% to $235.75 | H200 sales clearance to Chinese firms | Durability of case-by-case licensing regime |

| TSMC | +4.5% | Broader semiconductor trade optimism | Taiwan geopolitical risk; projected $1.5 trillion global semi market by 2030 |

TSMC has projected the global semiconductor market could exceed $1.5 trillion by 2030, a figure that underscores the scale of what export control policy is shaping. Nasdaq 100 Futures edged up just 0.1% to 29,713.0 on 14 May, suggesting the broader market was not fully pricing in a sector breakout.

The semiconductor issue is structural, not episodic. BlackRock, Lazard, and institutional analyses across the sector classify export controls and AI restrictions as permanent features of the investment landscape. The forward questions for investors are:

The Nvidia clearance is the most tangible sector-level outcome of the summit week. Its durability remains uncertain: a case-by-case licensing regime creates episodic volatility, not a resolved structural environment.

The regulatory clearance that drove Nvidia’s 4.39% gain is complicated by Beijing’s customs block on H200 shipments: Washington shifted from a presumption-of-denial to a case-by-case review standard in January 2026, but no commercial shipments to Alibaba, Tencent, or ByteDance have been completed, meaning the controlling barrier has moved from Washington to Beijing without removing the underlying access constraint.

The causal chain from military operation to diplomatic posture runs in a straight line:

A ceasefire subsequently took hold, according to a White House release, but the energy market consequences extended through the summit week. Oil futures gained over 1.5% on a weekly basis during the summit period, reflecting combined Hormuz and geopolitical risk premium.

BlackRock’s geopolitical risk framework identifies chokepoint disruption as producing “outsized consequences for Europe and Asia” via energy price spikes and growth shocks, a template that applies directly to both the Hormuz scenario and potential Taiwan Strait disruptions.

China’s offer to broker Iran peace was not a gesture of goodwill. It was a direct response to a material economic threat. Energy investors need to price not just the physical disruption but the diplomatic consequence: if China-brokered Iran stabilisation gains traction, it introduces a new variable capable of compressing oil risk premia relatively quickly.

Hormuz risk premium persistence operates on a longer timeline than diplomatic announcements: the near-total withdrawal of commercial war-risk insurance effectively closed the Strait to standard commercial traffic even when physical passage was technically possible, and the IEA projects a two-year supply chain recovery timeline under a best-case resolution, meaning China-brokered Iran stabilisation would compress energy risk premia gradually rather than immediately.

Lazard’s geopolitical advisory offers the core reframe: the right question is not whether a summit is “good” or “bad” but how it shifts the trajectory of economic nationalism across semiconductor controls, arms sales signals, and critical mineral leverage. A summit that opens a licensing channel for chips while hardening the rhetoric on Taiwan has moved two trajectories in opposite directions, and pricing only one produces a distorted risk picture.

The directional framework supported across institutional analyses maps two scenarios against their asset-class implications:

| Scenario | Taiwan Outcome | Tech/Semis | Energy/USD | Asian Equities |

|---|---|---|---|---|

| Escalation | Arms sales resumed; rhetoric hardens | Semiconductor pressure; tighter controls | Higher energy risk premia; stronger USD | Significant downside; raised risk premia |

| Stabilisation | Tacit limits; de-escalation signals | Relief rally; licensing channels hold | Easing risk premia; softer USD vs EM FX | Risk-on rotation into Asia/EM |

BCA Research provides a temporal calibration: geopolitical risk is expected to move sideways in 2026 as the US pursues a tariff truce ahead of midterms. The 14-15 May summit is one node in that longer diplomatic arc, not a terminal resolution.

The World Economic Forum’s Global Risks Report offers the structural overlay. Its cascading-impact model encourages mapping summit outcomes into time-horizon buckets rather than treating them as single-session events. In short-term windows, risk-on and risk-off rotations dominate, as the 14-15 May session demonstrated. Over medium-term horizons, sector reweighting around semiconductors and defence takes hold. Over the long term, supply-chain restructuring and on-shoring beneficiaries emerge as durable positioning themes.

Lazard adds a lagging variable: critical mineral counter-leverage is a response mechanism China can deploy following any summit it perceives as unfavourable. This tool operates on a slower timeline than tariff adjustments but produces durable effects on input costs for advanced manufacturing.

BlackRock’s geopolitical risk framework classifies US-China tech restrictions and Taiwan tensions as structural volatility drivers, not one-time shocks. The framework is repeatable: apply it to the next tariff announcement, the next arms sale decision, or the next bilateral meeting, and the analytical architecture holds.

The Dow Jones closed at 50,063.46 (+0.75%) on 14 May. The S&P 500 finished at 7,501.39 (+0.77%). The NASDAQ Composite reached 26,635.22 (+0.88%). US equities treated the summit as a trade stabilisation event, and for US-listed multinationals, that was the variable that mattered most.

Asian equities retreated on 15 May. USD safe-haven demand eased slightly on trade optimism, as noted in CNBC coverage. Oil futures gained over 1.5% weekly, reflecting unresolved energy risk.

The two reactions are not contradictory. They are the most honest market read of what the summit actually resolved and what it did not.

Brookings research on geopolitical financial fragmentation documents how sustained US-China rivalry reshapes cross-border capital flows and introduces persistent divergence between markets exposed to different sides of the strategic competition, providing the academic baseline for interpreting why US and Asian equity reactions to the same summit can move in opposite directions without contradiction.

The divergence between US and Asian equity reactions is not a contradiction; it is the market’s own geopolitical risk assessment in real time, pricing trade resolution as a US-positive and Taiwan/technology uncertainty as an Asia-negative simultaneously.

Three unresolved pressure points will determine whether the divergence narrows or widens in the weeks ahead:

The Trump-Xi summit of 14-15 May 2026 was a trade stabilisation node within a larger structural contest over Taiwan, technology, and energy access. The market reaction on both sides of the Pacific captured exactly that distinction: trade relief for US equities, residual risk for Asian markets exposed to the unresolved agenda items.

BCA Research expects geopolitical risk to move sideways through 2026, with the administration pursuing a tariff truce ahead of midterm elections. This summit is one point in that arc, not its conclusion. BlackRock classifies US-China competition as a structural, not cyclical, driver of market volatility, a classification that means each bilateral meeting recalibrates the trajectory without resolving it.

The actionable posture for investors: monitor semiconductor licensing decisions, Taiwan arms sales signals, and Iran stabilisation progress as the three live variables most likely to move the geopolitical risk premium embedded in global equities through the remainder of 2026.

Investors who treat this summit as a resolved event will be mispricing the risk surface. Those who treat it as a recalibration point within a structural contest, one that shifted specific trajectories without closing any of them, will be better positioned for what follows.

The actionable counterpart to this analytical posture is a geopolitical portfolio resilience framework built around permanent allocations rather than reactive repositioning: BlackRock and Vanguard both recommend a 5-10% strategic gold allocation with quarterly rebalancing as the core mechanism, and gold reached approximately $4,739 per ounce in May 2026 with institutional forecasts targeting $5,000-6,300 per ounce by end-2026.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements regarding geopolitical outcomes, policy trajectories, and market impacts are speculative and subject to change based on developments beyond any single summit’s scope.

The Trump-Xi bilateral summit held on 14-15 May 2026 in Beijing covered five major issues: trade and tariff stabilisation, Taiwan arms sales, semiconductor export controls, critical mineral access, and Iran peace brokering following Operation Epic Fury. The trade stabilisation outcome was the headline result, driving a rally in US equities while Asian markets retreated on residual geopolitical uncertainty.

Nvidia shares surged more than 4% to an all-time high of $235.75 on 14 May 2026 after Reuters reported US regulators had permitted Nvidia to sell H200 chips to as many as 10 Chinese companies. However, the durability of this outcome remains uncertain because Beijing's customs block on H200 shipments means the controlling barrier shifted from Washington to Beijing without fully resolving the underlying access constraint.

US equities priced the summit primarily as a trade stabilisation event, benefiting US-listed multinationals, while Asian markets retreated on 15 May due to residual uncertainty over Taiwan arms sales and semiconductor export controls. The divergence reflects the market's simultaneous assessment of trade relief as a US-positive and Taiwan and technology risk as an Asia-negative.

Operation Epic Fury was a US-Israel military operation launched on 28 February 2026 that targeted Iran's leadership and disrupted Strait of Hormuz shipping, spiking energy import costs for Asian economies including China. The economic pain from that disruption gave Beijing strong incentives to attend the summit and offer to help broker an Iran peace deal, which was reported by CNBC on 14 May 2026.

Institutional analyses identify three live variables most likely to move the geopolitical risk premium through the remainder of 2026: the status of Taiwan arms sales decisions and their deterrence signalling, the durability of the semiconductor case-by-case licensing regime, and the trajectory of China-brokered Iran stabilisation talks and their effect on energy risk premia.