How the US Government Became Intel’s Investor and Deal Broker

49 mins ago

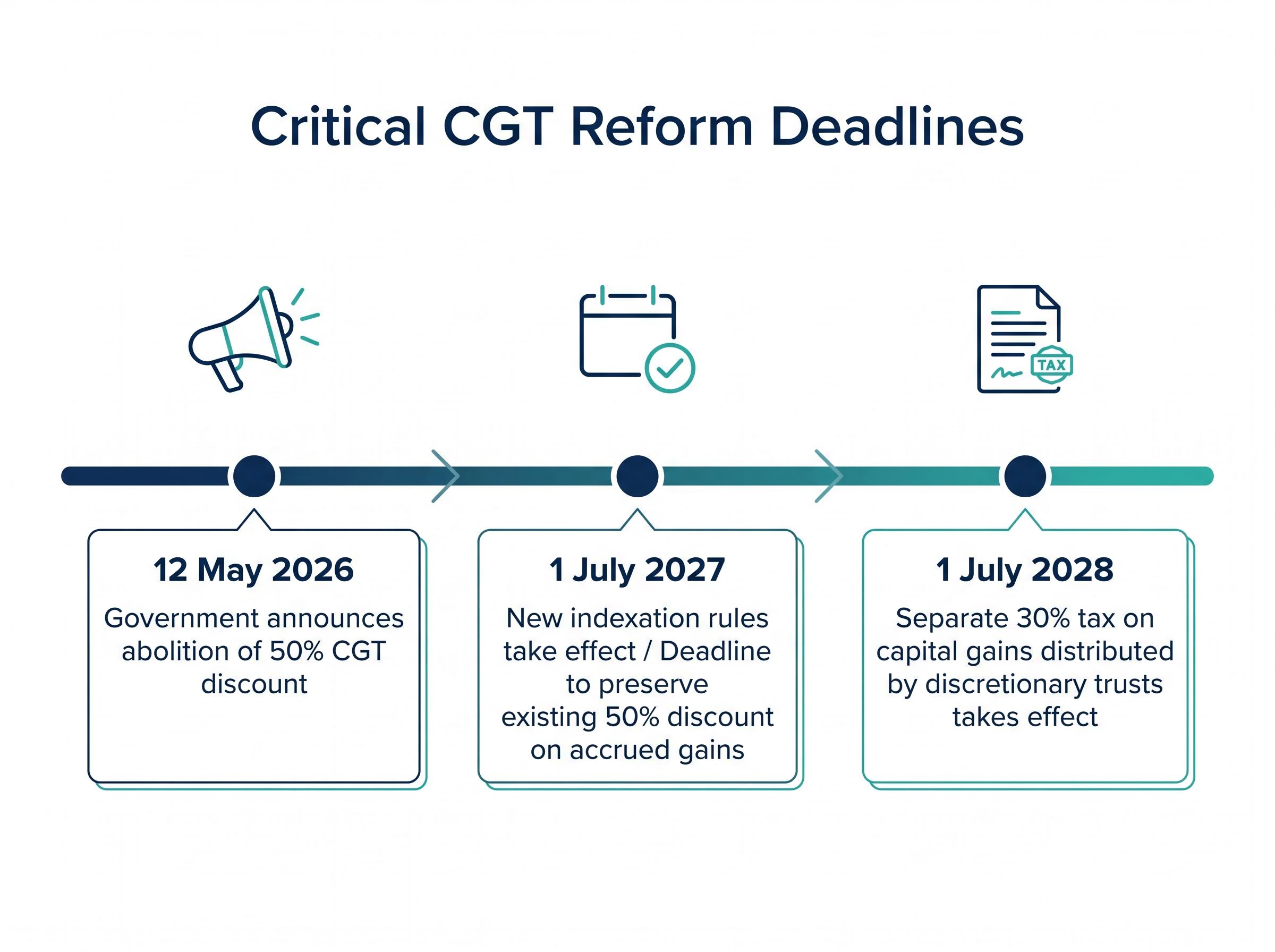

A quarter of all Australian property investors who generated a capital gain over the past decade would have paid less tax under the incoming indexation model than under the 50% discount it is replacing. That counterintuitive finding is the starting point for understanding Australia’s most significant capital gains tax reform in nearly three decades. On 12 May 2026, the federal government announced it would abolish the 50% CGT discount for assets held longer than 12 months, replacing it with inflation-adjusted cost base indexation and a 30% minimum tax rate, effective 1 July 2027. The policy has sparked immediate debate over what it will do to property prices, rental supply, investor portfolios, and housing affordability over the decade ahead. What follows cuts through the noise to examine who actually wins and loses under the new rules, how outcomes differ across Sydney, Melbourne, and Brisbane, and why the reform’s success in generating new housing supply ultimately depends on decisions made in state planning departments rather than Canberra.

The prevailing narrative frames the reform as a straightforward tax increase on all property investors. The mechanics tell a different story.

Under the replacement model, an asset’s cost base is indexed to the Consumer Price Index. Only the real, inflation-adjusted gain is then taxed at either the investor’s marginal rate or 30%, whichever is higher. This is not a new invention. Australia used this exact indexation method before 1999, when the Howard government replaced it with the flat 50% discount. The reform is a return to an earlier approach, not an untested experiment.

The 1999 Treasury announcement on CGT indexation confirmed that from 1 October 1999, the Howard government would freeze cost base indexation and allow individuals to instead include half the nominal gain in assessable income, establishing the 50% discount regime that the 2026 reform now reverses.

Several features add further complexity. Pre-1985 assets retain their existing treatment. For assets purchased before 1 July 2027 but sold after that date, gains are apportioned: pre-cutoff gains remain under the current rules, while gains arising after the changeover fall under the new regime. A separate 30% tax on capital gains distributed by discretionary trusts is proposed from 1 July 2028.

For assets purchased before the cutoff and sold after it, the split-calculation rule apportions gains by accrual date, meaning pre-transition gains retain the 50% discount while gains accruing from 1 July 2027 fall under the new indexation regime. Superannuation funds and SMSFs are explicitly carved out of the new framework, preserving their existing CGT treatment in full.

| Attribute | Existing 50% discount | New indexation model (from 1 July 2027) |

|---|---|---|

| Tax base | 50% of nominal gain excluded | Only real (inflation-adjusted) gain taxed |

| Minimum rate | None (taxed at marginal rate) | 30% minimum on capital gains |

| New builds | No special treatment | Carved out; retain preferential treatment |

| Pre-1985 assets | CGT-exempt | Brought within the new framework |

| Trust structures | 50% discount available | Separate 30% trust tax proposed from 1 July 2028 |

Newly constructed residential properties are deliberately excluded from the new CGT treatment. The carve-out creates a relative tax advantage for investors in new builds versus established stock. This is the reform’s supply-side mechanism: by making new construction more attractive on an after-tax basis, the government aims to redirect investor capital toward adding dwellings rather than bidding up prices on existing ones.

The assumption that indexation is universally worse for investors does not survive contact with the data.

PropTrack analysis found that roughly a quarter of property investors who generated a gain over the past decade would have faced a lower taxable amount under indexation than under the 50% discount. That proportion is not static. It peaked at 39% in Q4 2023, approximately 12 months after Australian headline inflation hit its highest level.

The 39% peak share in Q4 2023 arrived roughly a year after Australia’s inflation peaked, illustrating a direct relationship: as inflation erodes more of the nominal gain, indexation shelters a larger portion of the investor’s return.

The underlying logic is straightforward. Indexation favours investors when inflation is high and nominal price growth is modest, because a larger share of the nominal gain is reclassified as inflation rather than real profit. The flat 50% discount favours investors when prices rise strongly ahead of inflation, because half the gain is excluded regardless of what inflation did during the holding period. In the low-inflation, pre-pandemic environment, a smaller share of gains would have been lower under indexation.

The conditions under which each model produces a better outcome:

The effect mirrors bracket creep in income tax: taxing nominal rather than real gains applies an inflationary distortion that penalises investors for holding through high-inflation periods. The indexation model removes that distortion.

The same national policy produces distinctly different outcomes depending on which city an investor’s property sits in.

Sydney’s strong price growth between 2016 and 2022 meant the flat 50% discount was significantly more advantageous for most sellers in that period. Real appreciation outpaced inflation by a wide margin, and the flat discount sheltered a larger absolute dollar amount than indexation would have. That advantage has narrowed in more recent years as Sydney’s price growth moderated, but the city remains a market where the current regime has generally delivered the better tax outcome for sellers.

Melbourne is moving in the opposite direction. A growing share of investor asset sales in recent years would have produced a lower taxable gain under indexation, reflecting subdued local price growth relative to inflation. For Melbourne landlords who bought in 2017-2018 and held through a period of flat-to-modest returns while CPI accumulated, the new regime may represent an improvement.

Brisbane tells a third story. Stronger recent price growth means sellers there are more likely to face a higher taxable gain under indexation than under the flat discount. The city’s trajectory is the inverse of Melbourne’s.

| City | Recent price growth trajectory | Likely outcome: indexation vs flat discount | Direction of change in recent years |

|---|---|---|---|

| Sydney | Strong 2016-2022, moderating recently | Flat discount generally more favourable | Advantage narrowing |

| Melbourne | Subdued relative to inflation | Growing share where indexation is better | Shifting toward indexation advantage |

| Brisbane | Strong recent growth | Indexation more likely to disadvantage sellers | Moving away from indexation advantage |

A Sydney landlord and a Melbourne landlord face genuinely different calculations under the same national policy. The city in which a property is held is a material input into the reform’s portfolio impact.

The grandfathering deadline is already functioning as a forcing mechanism, even before the legislation has been fully drafted.

Investors holding properties with large unrealised nominal gains face the strongest motivation to crystallise those gains under the existing 50% discount before 1 July 2027. The incentive structure is unambiguous: gains realised before that date remain under the current rules, while gains arising after it fall under the new regime. For assets held across the cutoff, gains are apportioned by accrual date.

BDO Australia has framed the 1 July 2027 boundary as an active planning deadline, not a theoretical future concern, with advisers already counselling clients to model the choice before transitional rule uncertainty makes late-moving decisions riskier.

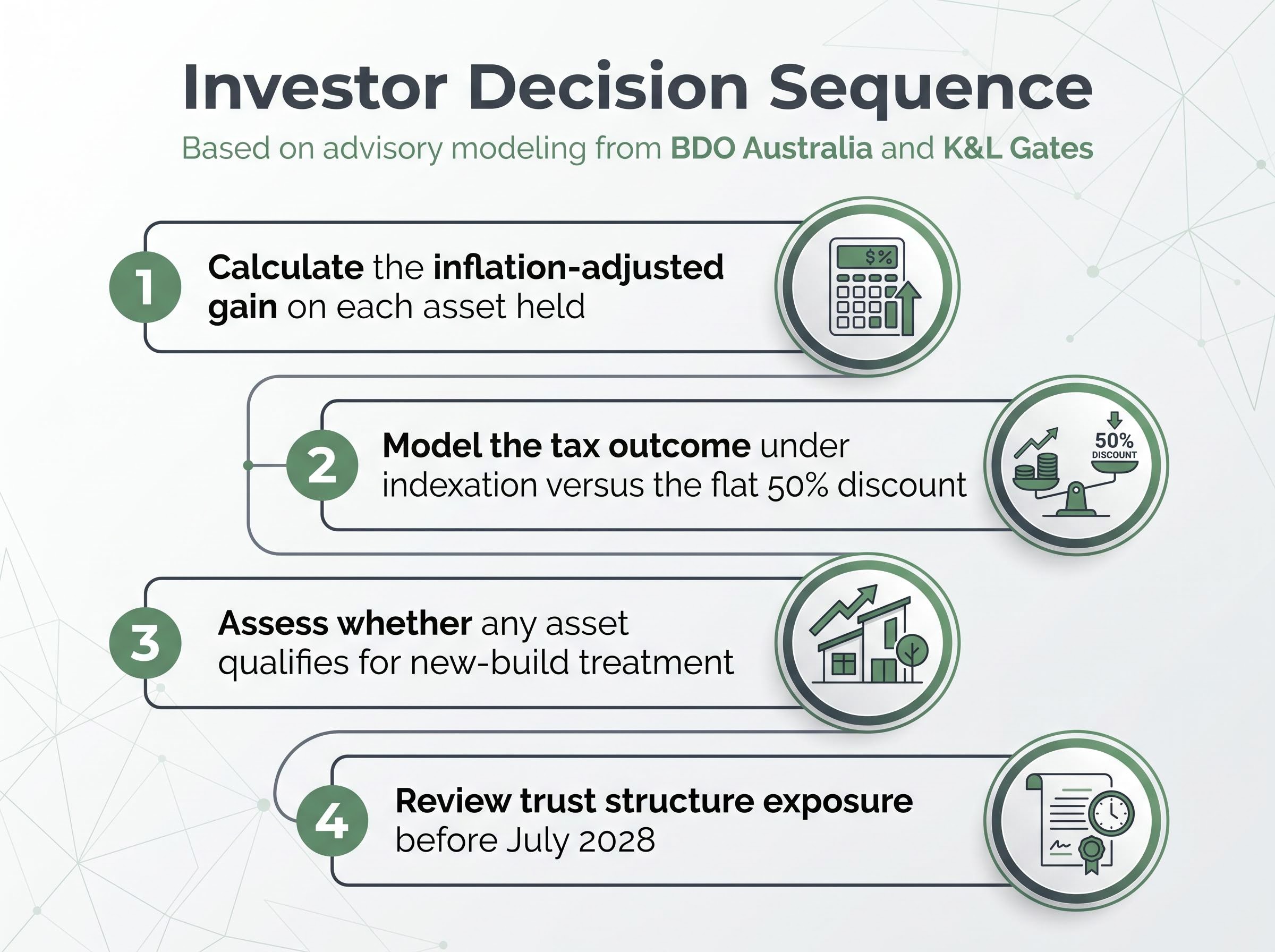

Advisers at both BDO Australia and K&L Gates are counselling clients to run the numbers now. The four principal strategies being modelled:

The sell-now narrative warrants complication, however. Investors in assets with modest nominal gains relative to inflation may find the indexation model comparable or preferable. For them, an accelerated sale may be unnecessary or even counterproductive, locking in transaction costs and forfeiting future rental income to avoid a tax change that would not have disadvantaged them.

Higher effective CGT rates under the new regime create a lock-in effect that could reduce asset turnover beyond the pre-2027 sell-down window, as investors who hold past the transition date face a structurally higher barrier to realising gains and redeploying capital into new positions.

Commentary cited by ABC News has raised concerns about investor withdrawal from the rental market and the risk of reduced rental supply in markets already experiencing low vacancy. Trust structure investors face additional urgency given the separate 2028 deadline.

The new-build carve-out can redirect investor capital toward development. It cannot create the conditions for that development to proceed.

Planning approvals, zoning reform, builder capacity, and financing costs all sit at state and local government level. The federal tax lever pulls in one direction; whether the supply response follows depends on an entirely separate set of decisions being made in Sydney, Melbourne, and Brisbane planning departments.

The negative gearing ring-fence for established properties acquired after 12 May 2026 compounds the CGT deadline for investors making new acquisitions: deductibility against non-rental income is removed on the same asset class where the CGT discount is also being withdrawn, creating a paired reduction in the after-tax return on established investment property.

PropTrack has noted that the reform’s longer-term housing supply impact is less certain given persistent state and local planning constraints. Supply-demand fundamentals in Australian housing have not changed as a result of the CGT policy alone.

No surfaced source identifies a coordinated state response specifically designed to amplify the CGT new-build incentive. The state planning reform debate (upzoning, transport corridor density, activity centre approvals) is the structural bottleneck that determines whether redirected investor capital translates into actual dwellings. Even the federal government’s own budget framing acknowledges the dual intent of the reform: redirect investment toward new construction while moderating total sector-wide investment. Those two goals exist in partial tension, and resolving that tension requires state-level execution the federal government cannot guarantee.

Near-term price softening in established property is plausible given anticipated investor sell-downs ahead of the July 2027 deadline. Domain research commentary has flagged rental supply pressure as a genuine risk in markets with low vacancy, though the scale of that pressure depends on how many investors actually exit before the changeover.

The uniform application of the new CGT rules across all capital asset classes (except new builds) limits the likelihood of a sharp property-specific exodus. Property does not become dramatically less attractive relative to equities or other domestic asset classes under the reform; the effective tax change applies broadly.

PropTrack analysis indicates that supply-demand fundamentals have not changed as a result of the policy alone, and that overall property investment is expected to moderate rather than grow under the new regime.

Three unknowns will determine the reform’s actual market impact:

No quantified city-by-city price forecasts specifically linked to the CGT change are available from current sources. The government has framed the reform as intended to free up established stock for owner-occupiers, increase supply via new builds, and improve intergenerational fairness. The real market impact will be measured over years, not months, and it will interact with planning reform, interest rate cycles, and demographic demand in ways no single budget announcement can pre-determine.

The core decision facing property investors reduces to a three-way choice: sell before July 2027 to lock in the current discount; hold and model whether indexation produces a comparable or better outcome for the specific asset; or rebalance toward new residential stock to access the policy advantage.

The decision sequence investors should work through:

The asymmetry of risk in waiting is worth noting. The grandfathering mechanics are clear in principle, but transitional rule detail remains unlegislated as of May 2026. Late movers may find themselves unable to act before the deadline if legislative complexity creates planning delays. Both BDO Australia and K&L Gates have framed the grandfathering boundary as an active planning deadline requiring immediate attention.

The proposed 30% tax on discretionary trusts from 1 July 2028 represents a distinct but related decision with its own planning horizon. Investors using trust structures to hold property assets face both the July 2027 CGT deadline and the July 2028 trust tax deadline as simultaneous planning priorities. The two deadlines compound rather than cancel each other, and advisers are treating them as a paired exercise.

The CGT reform shifts who benefits from property investment in ways that are city-specific and investor-specific. It will produce a period of market recalibration rather than collapse. Its housing supply ambitions are limited by state planning capacity that the federal government does not control.

What the government has right: taxing only real gains is defensible in principle, the new-build carve-out is a logical supply incentive, and the intergenerational fairness framing reflects genuine structural problems in Australian housing. The honest constraint is that the decade-long impact the government has pointed to depends on states and territories moving in parallel, and that alignment is not yet in evidence.

Investors should consult a qualified tax adviser to model the indexation versus flat discount outcome for their specific portfolio before the legislative detail is finalised.

Investors wanting to understand how the CGT changes sit within the broader policy package will find our full explainer on Australia’s three-pillar investment tax reform, which covers the negative gearing ring-fence, the CGT discount replacement, and the discretionary trust minimum tax in sequence, including major bank economist assessments of which measure carries the largest behavioural consequence.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

From 1 July 2027, Australia will replace the 50% capital gains tax discount for assets held longer than 12 months with a cost base indexation model, meaning only the real inflation-adjusted gain is taxed, subject to a 30% minimum rate.

For properties purchased before 1 July 2027 but sold after that date, gains are apportioned by accrual date, so pre-cutoff gains retain the 50% discount while gains accruing from 1 July 2027 fall under the new indexation regime.

No. Superannuation funds and SMSFs are explicitly carved out of the new framework, preserving their existing CGT treatment in full.

Investors should calculate the inflation-adjusted gain on each asset, model the tax outcome under indexation versus the flat 50% discount, assess eligibility for the new-build exemption, and review any discretionary trust structures before the separate July 2028 deadline.

Sydney investors have generally benefited more from the flat 50% discount due to strong price growth, while Melbourne investors with subdued returns relative to inflation may find indexation comparable or better; Brisbane investors face a higher likelihood of a larger taxable gain under indexation given recent strong price growth.