ATEC is marketed as Australia’s only pure-play Australian technology ETF. It is a compelling pitch, and with approximately $581 million in assets under management as of May 2026, investors have clearly bought it. Yet only 56% of the fund’s underlying index falls within the technology sector under standard industry classification. The remaining holdings include an industrials company, a healthcare name, and a cluster of communications services stocks.

That gap between label and composition explains a pattern of investor confusion that has persisted through 2025 and into 2026: the ETF does not behave like a concentrated tech fund, particularly during sharp selloffs and recoveries. Understanding why requires looking past the product name and into the index it tracks. This article breaks down exactly what ATEC owns, how the S&P/ASX All Technology Index selects its constituents, and what the cross-sector design means for investors weighing this fund against narrower technology exposure.

The one label doing a lot of heavy lifting

When investors hear “technology ETF,” most picture a fund filled with software companies, cloud platforms, and IT services businesses. ATEC, managed by BetaShares with a management fee of 0.48% per annum, is genuinely the only ASX-listed ETF offering exclusive exposure to Australian technology-related companies. That market positioning is accurate. The phrase “technology-related,” however, is doing significant definitional work.

ATEC tracks the S&P/ASX All Technology Index, not the S&P/ASX 200 Information Technology Index. The distinction matters more than most investors realise. The All Technology Index holds 45 companies as of May 2026, drawn from across multiple sectors of the economy.

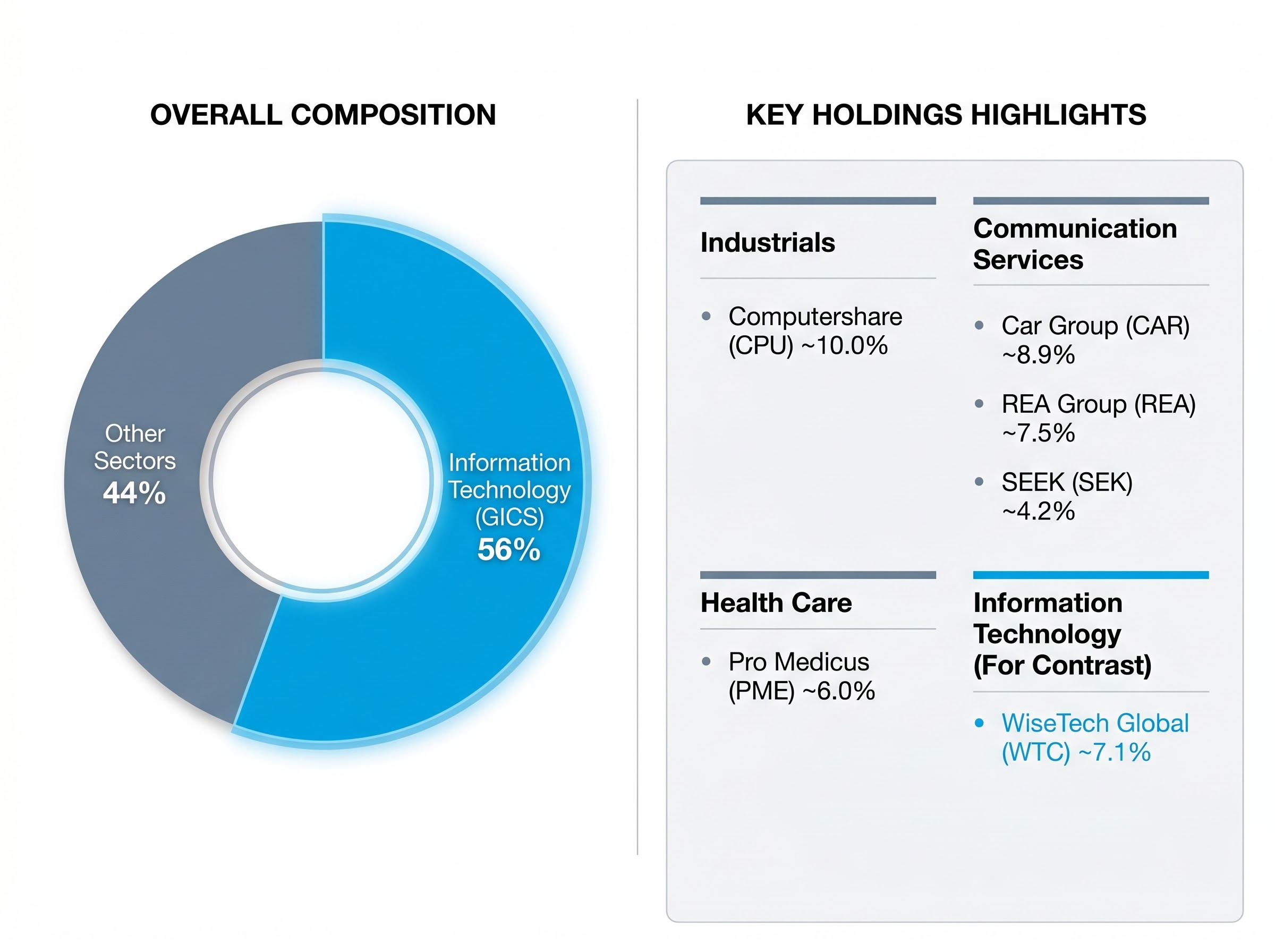

Only 56% of the S&P/ASX All Technology Index’s constituents are classified within the Information Technology sector under the Global Industry Classification Standard (GICS), the system used by index providers worldwide to categorise companies by their primary business activity.

Investors who purchase ATEC expecting the concentrated, high-beta behaviour of a pure IT index are operating on an assumption the index was never designed to deliver. Correcting that assumption starts with the index methodology itself.

When big ASX news breaks, our subscribers know first

What the S&P/ASX All Technology Index actually selects for

The cross-sector composition is not a labelling error by BetaShares or an oversight by S&P Dow Jones Indices. It is a deliberate design choice built into the index methodology.

The S&P/ASX All Technology Index uses a “technology-enabled business model” criterion as its primary filter rather than GICS sector classification. A company does not need to sit within the Information Technology sector to qualify. It needs to operate a business model that S&P considers technology-driven. The index’s stated scope covers four categories:

- Information technology

- Consumer electronics

- Online retail

- Medical technology

That scope is broader than a pure IT index by design. It reflects a specific editorial judgment by S&P about what “Australian technology” means in a market where many of the largest tech-enabled businesses happen to be classified under adjacent GICS sectors.

Eligibility criteria that shape what gets in

Beyond the scope definition, the index applies screening criteria that are more restrictive than a simple sector-membership test.

New entrants must demonstrate two prior years of positive earnings per share before they can be added. This profitability screen filters out early-stage, pre-revenue technology companies that might otherwise qualify on a business-model basis alone.

Constituents must also meet liquidity and size thresholds to remain in the index. Rebalancing occurs quarterly, with buffers in place to reduce unnecessary turnover. Foreign-domiciled companies listed on the ASX are eligible for inclusion.

S&P announced enhancements to the broader S&P/ASX index series in September 2025, though no specific structural overhaul to the All Technology Index has been confirmed. Quarterly rebalances have continued with incremental additions and removals reflecting changes in constituent eligibility and relative performance.

Meet the non-tech names inside Australia’s “tech ETF”

The 56% figure becomes far more concrete when individual holdings are examined. Several of ATEC’s most heavily weighted positions sit outside the Information Technology sector entirely.

Computershare (ASX: CPU), classified as Industrials under GICS, has historically been one of the fund’s largest holdings. The company operates a technology-enabled registry and corporate administration business. Its inclusion reflects the index’s business-model criterion: the technology infrastructure underpinning Computershare’s operations qualifies it, even though its GICS classification does not.

Car Group (ASX: CAR), REA Group (ASX: REA), and SEEK (ASX: SEK) are all classified under Communications Services. Each operates a digital marketplace platform, in automotive, property, and employment respectively. These are genuinely technology-driven businesses. The surprise is not that they use technology; it is that their GICS classifications place them outside the IT sector.

Pro Medicus (ASX: PME) falls under Health Care. It develops and sells medical imaging software, a product that is unambiguously technological. Yet under GICS conventions, its primary revenue classification keeps it in the healthcare bucket.

For contrast, WiseTech Global (ASX: WTC) at approximately 7.1% weighting is classified as Information Technology, sitting squarely where most investors would expect a tech ETF constituent to sit.

| Company | ASX Code | GICS Sector | Approx. Weight (%) |

|---|---|---|---|

| Computershare | CPU | Industrials | ~10.0 |

| Car Group | CAR | Communication Services | ~8.9 |

| REA Group | REA | Communication Services | ~7.5 |

| Pro Medicus | PME | Health Care | ~6.0 |

| SEEK | SEK | Communication Services | ~4.2 |

| WiseTech Global | WTC | Information Technology | ~7.1 |

Selected ATEC holdings by GICS sector (May 2026). WiseTech included for contrast as a pure IT constituent.

How this composition shaped ATEC’s behaviour in the recent tech rout

The structural characteristics described above are not abstract. They showed up clearly in ATEC’s performance during the extended technology selloff that ran through late 2025 and into early 2026.

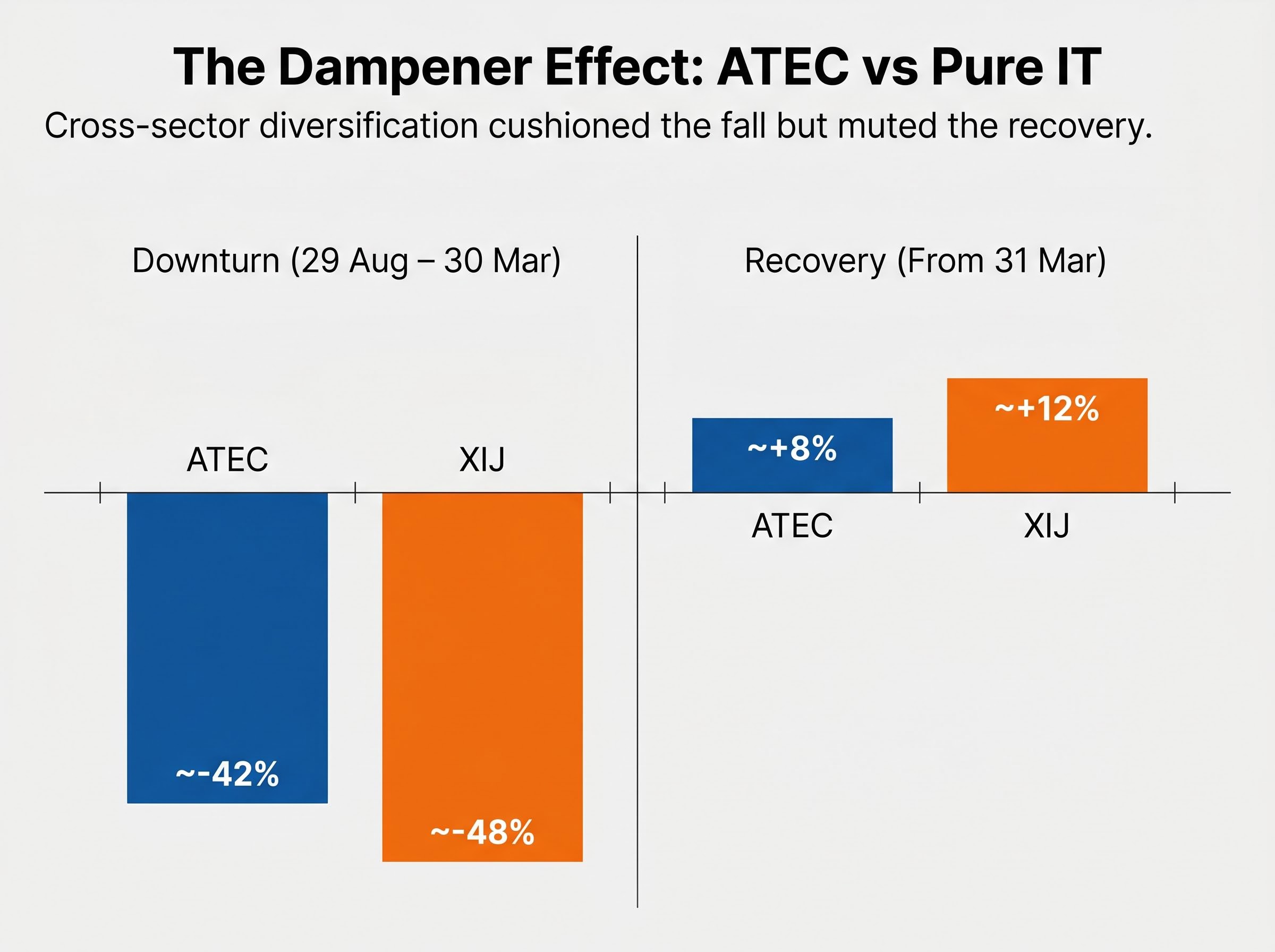

Between 29 August and 30 March, ATEC declined approximately 42%. Over the same window, the S&P/ASX 200 Information Technology Index (XIJ) fell approximately 48%. The non-IT holdings in ATEC’s portfolio, spanning industrials, communications services, and healthcare, provided a partial buffer. These companies are not pure-beta technology plays, and their share prices did not fall as aggressively as the concentrated IT names.

The other side of that coin arrived with the recovery. From 31 March onward, ATEC recovered approximately 8%, while the XIJ rebounded approximately 12%. The same cross-sector diversification that cushioned the fall also muted the snapback.

| Metric | ATEC | XIJ (ASX 200 IT Index) |

|---|---|---|

| Downturn decline (29 Aug – 30 Mar) | ~-42% | ~-48% |

| Post-trough recovery (from 31 Mar) | ~+8% | ~+12% |

| 1-year return (as of May 2026) | ~-20.58% | — |

The dispersion within XIJ’s own constituents was extreme. WiseTech fell approximately 64% with no meaningful recovery at the measurement date. Megaport surged approximately 79% in the recovery phase. Elsight gained approximately 242% during the rout itself, moving against the broader trend entirely. A concentrated IT index carries that kind of individual-stock variance; ATEC’s broader composition smooths it.

Despite the difficult performance environment, BetaShares reported $193.7 million in year-to-date inflows into ATEC as of April 2026, suggesting that investor demand has persisted even as returns have compressed.

ATEC’s cross-sector design functions as a structural smoother. It is not a downside protector, and it is not an upside enhancer. It is a dampener in both directions. Investors who felt the fund “didn’t fall enough” and those who felt it “didn’t bounce enough” were both experiencing the same design feature from different vantage points.

The two Australian tech indices compared: what each one is actually measuring

The confusion around ATEC often stems from a single false equivalence: treating the S&P/ASX All Technology Index and the S&P/ASX 200 Information Technology Index as interchangeable. They answer the same question, “what is Australian technology?”, but they arrive at very different answers.

The All Technology Index casts a wide net across 45 constituents, selecting companies based on whether their business model is technology-enabled, regardless of GICS classification. The 200 Information Technology Index is narrower, comprising only companies within the GICS Information Technology sector that are members of the ASX 200, weighted by market capitalisation.

The practical consequence is concentration. The IT Index is heavily weighted toward names like Xero and WiseTech Global, both classified as pure Information Technology. That concentration produces higher volatility in both directions. Investors seeking closer alignment with global technology indices such as the NASDAQ-100 will find the IT Index’s composition more familiar. Investors who want broader exposure to Australia’s digital economy, including its marketplaces, its med-tech names, and its tech-enabled industrials, may find the All Technology Index’s scope more appropriate.

Neither index is wrong. They are measuring different things.

| Feature | S&P/ASX All Technology Index | S&P/ASX 200 IT Index |

|---|---|---|

| Constituents | 45 | Varies (ASX 200 IT-sector members) |

| Selection criterion | Technology-enabled business model | GICS IT-sector membership |

| Sector scope | IT, communications, health care, industrials | Information Technology only |

| Volatility profile | Lower (cross-sector dampening) | Higher (concentrated IT exposure) |

| Primary ETF | ATEC (BetaShares) | No standalone ASX-listed ETF |

One notable gap in the current ASX ETF market: no standalone ETF tracks the S&P/ASX 200 Information Technology Index directly. Investors who want that specific, narrower exposure do not have a single-product solution available on the ASX today.

What investors should actually expect when they buy ATEC

Everything in the preceding sections points to a single practical reframing: ATEC is a diversified Australian digital economy fund, not a high-concentration pure-technology play. Evaluating it on the terms of a narrow IT index will produce consistent disappointment in both directions.

The two most common retail investor complaints, that ATEC didn’t fall as much as feared and that it didn’t bounce as much as hoped, are not signs of a broken product. Both outcomes are structurally expected given the index design. The cross-sector composition is working as intended.

Investors considering ATEC should calibrate their expectations accordingly:

- ATEC is a broad-based fund capturing Australia’s technology-enabled economy across IT, communications, healthcare, and industrials

- ATEC is not a concentrated high-beta IT fund comparable to a NASDAQ-100 tracker

- ATEC tends to outperform narrower IT indices during selloffs, because its non-IT holdings provide a partial cushion

- ATEC tends to lag narrower IT indices during sharp recoveries, because the same diversification dampens the rebound

BetaShares’ positioning of the fund as offering exposure to “technology-related” companies is accurate under the All Technology Index’s own methodology. The 0.48% management fee is reasonable for a sector fund with this breadth. The fund’s since-inception return of approximately 8.59% per annum provides context for its long-run performance through multiple market cycles.

Investors who want pure IT exposure will need to look elsewhere. Options include global technology ETFs (including NASDAQ-100 trackers and thematic AI or cybersecurity funds available on the ASX), BetaShares’ own global tech ETF lineup, or a self-constructed basket of ASX-listed IT stocks. No competing ASX-listed ETF currently tracks the narrower S&P/ASX 200 Information Technology Index directly.

ATEC is a digital economy fund with a tech-sector label, and that distinction matters

ATEC’s composition is intentional, not accidental. The S&P/ASX All Technology Index’s cross-sector design reflects a deliberate view that Australia’s technology story lives across multiple GICS classifications, from digital marketplaces classified as Communications Services to medical imaging platforms classified as Health Care.

That design choice has real consequences for portfolio behaviour, and investors who understand those consequences are better positioned to use the product appropriately. Reading the product disclosure statement and reviewing the full holdings list before assuming any ETF’s sector label is a complete description of its portfolio remains sound practice.

The practical takeaway is straightforward. ATEC suits investors who want diversified exposure to Australia’s digital economy. A different vehicle is needed for investors who want pure Information Technology concentration.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.