Why 30% Recession Odds Are Harder to Trade Than 60%

8 hrs ago

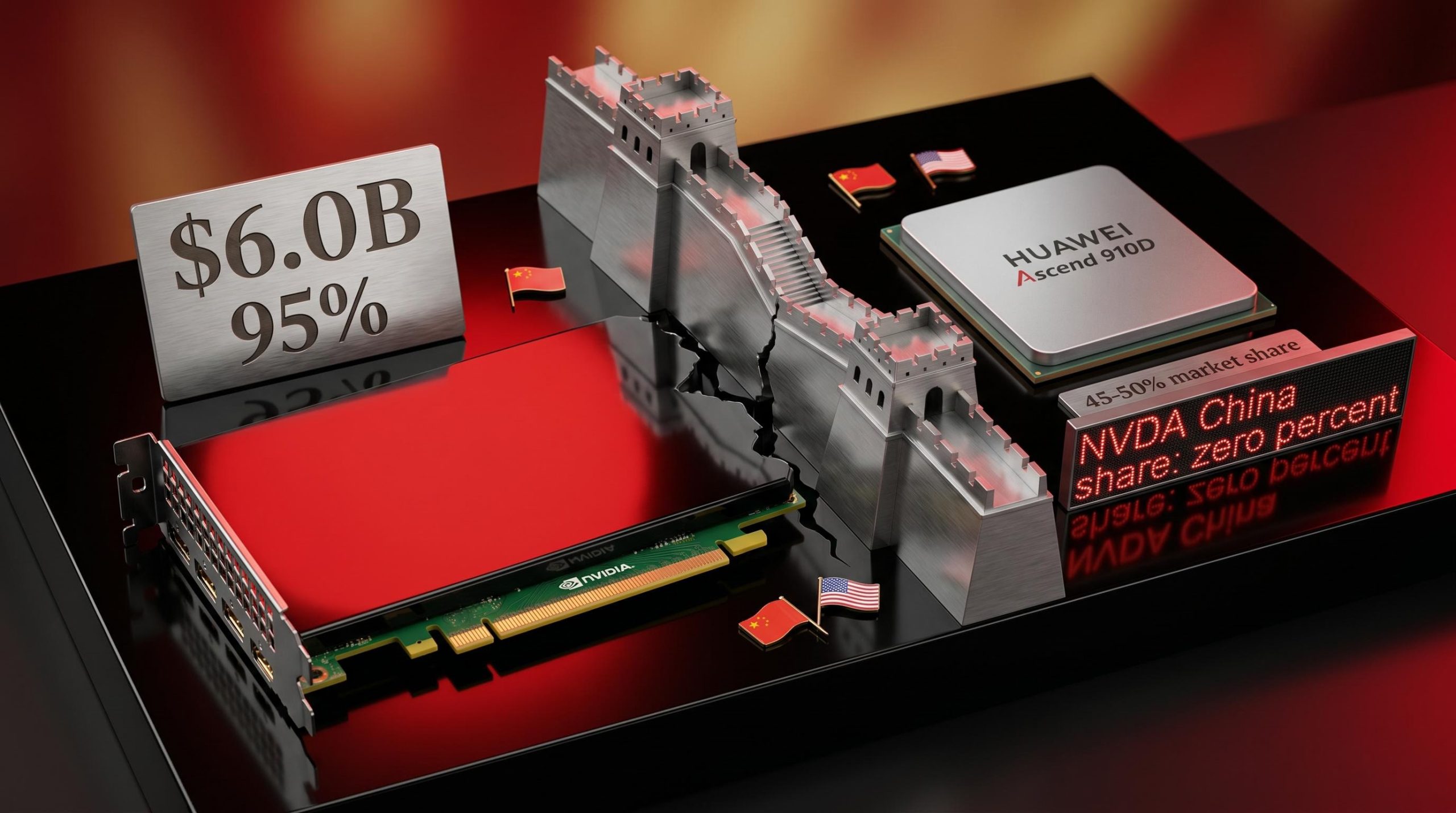

Before U.S. export controls reshaped the competitive map, Nvidia held roughly 95% of China’s advanced AI chip market. That figure, cited publicly by CEO Jensen Huang, represented not just commercial dominance but structural dependency: Chinese hyperscalers, AI laboratories, and cloud providers had no credible domestic alternative for frontier AI training workloads. On 14 May 2026, as Huang joined President Trump’s diplomatic summit in Beijing with Chinese President Xi Jinping, Reuters reported that approximately ten Chinese firms had received U.S. government authorisation to purchase Nvidia’s H200 chip, each capped at 75,000 units. Nvidia shares climbed roughly 1.8% in premarket trading. The premarket move, however, is the least interesting part of this story.

What follows traces the full arc: what Nvidia once held in China, how it lost it, who filled the gap, where the H200 licensing framework stands after the summit, and what institutional investors actually assume about China’s role in the long-term Nvidia investment thesis. The framework is designed to help readers evaluate Nvidia’s China exposure as a commercial opportunity with measurable constraints, rather than a headline risk that demands reactive positioning.

Pre-restriction dominance: Nvidia supplied an estimated 95% of China’s advanced AI accelerator market before export controls tightened, according to Jensen Huang’s public statements.

That figure was not a market-share footnote. It meant every major Chinese hyperscaler, from Alibaba to ByteDance, ran its most performance-intensive AI training workloads on Nvidia hardware. No domestic alternative could match H100-class performance, and the switching costs were embedded in software ecosystems built around CUDA.

The revenue was substantial:

Without a clear picture of this baseline, the $50 billion China AI market figure that Huang now cites has no frame of reference. The revenue Nvidia is trying to recover was not marginal. It was a structural monopoly that funded a meaningful share of the company’s R&D trajectory.

The revenue collapse was not a single event. It was a regulatory escalation that removed one layer of access after another, each step foreclosing the compliance path Nvidia had used to navigate the previous restriction.

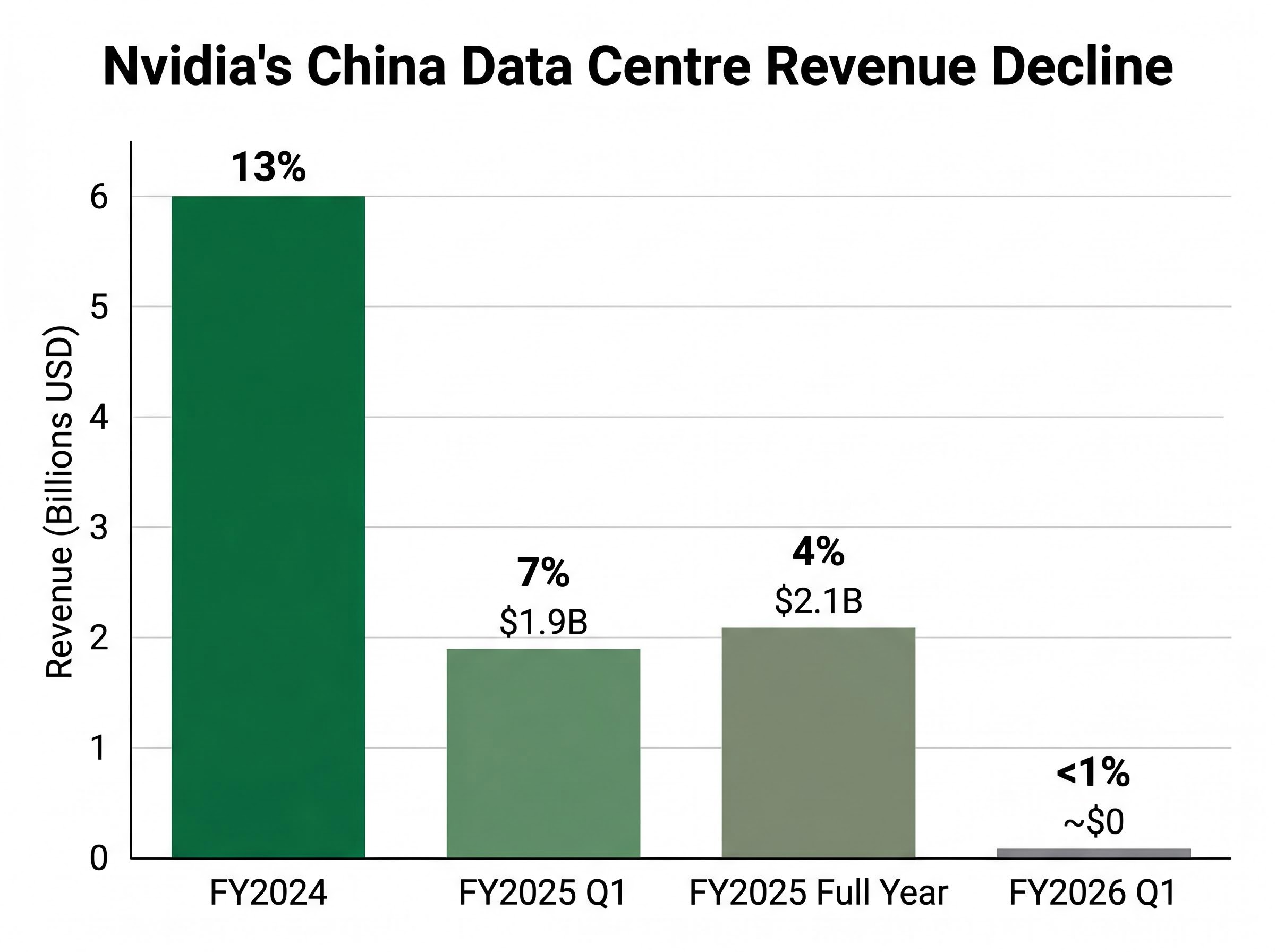

The initial H100 and A100 export bans prompted Nvidia to develop downgraded variants, the H800 and A800, designed to fall below the Bureau of Industry and Security’s performance thresholds. Those chips sustained a compliant revenue stream through FY2025 Q1 (February to April 2025), when China data centre revenue still reached $1.9 billion, approximately 7% of total data centre revenue.

Then the thresholds tightened again. H800 and A800 chips were restricted. Nvidia pivoted to the H200 licensing framework, which the BIS granted in December 2025 for approximately ten Chinese firms. But the commercial value of those licenses was immediately constrained from two directions.

| Period | China Data Centre Revenue | % of Total Data Centre Revenue |

|---|---|---|

| FY2024 (ended Jan 2024) | $6.0B | 13% |

| FY2025 Q1 (Feb–Apr 2025) | $1.9B | 7% |

| FY2025 Full Year (ended Jan 2026) | $2.1B | 4% |

| FY2026 Q1 (Feb–Apr 2026) | ~$0 | <1% |

In April 2026, five additional Chinese AI labs were added to the U.S. entity list. H100 and H800 chips remain fully banned. No approvals exist for Blackwell architecture (GB200) chips.

The squeeze was not one-sided. China imposed 100% retaliatory tariffs on U.S. legacy chips in March 2026 (Wall Street Journal, 15 March 2026), and Beijing issued informal directives pressuring domestic firms to avoid Nvidia purchases entirely.

ByteDance cancelled H200 orders (Reuters, 22 April 2026). Alibaba similarly halted purchases. The H200 licenses granted in December 2025 were, in practice, commercially neutralised before most transactions could close. Bernstein estimated approximately $1 billion per quarter in indirect smuggled chip sales as of March 2026, but these figures are not reflected in Nvidia’s official revenue.

The CNAS research on AI chip smuggling identifies the performance gap between legally available chips and frontier hardware as the primary driver of illicit procurement networks, which explains why Bernstein’s estimated $1 billion per quarter in indirect smuggled chip sales persists even when compliant licensing pathways nominally exist.

The dynamic operates independently of U.S. licensing decisions. Even where a licence exists, Beijing’s buyer pressure creates a structural barrier that no export approval alone can remove.

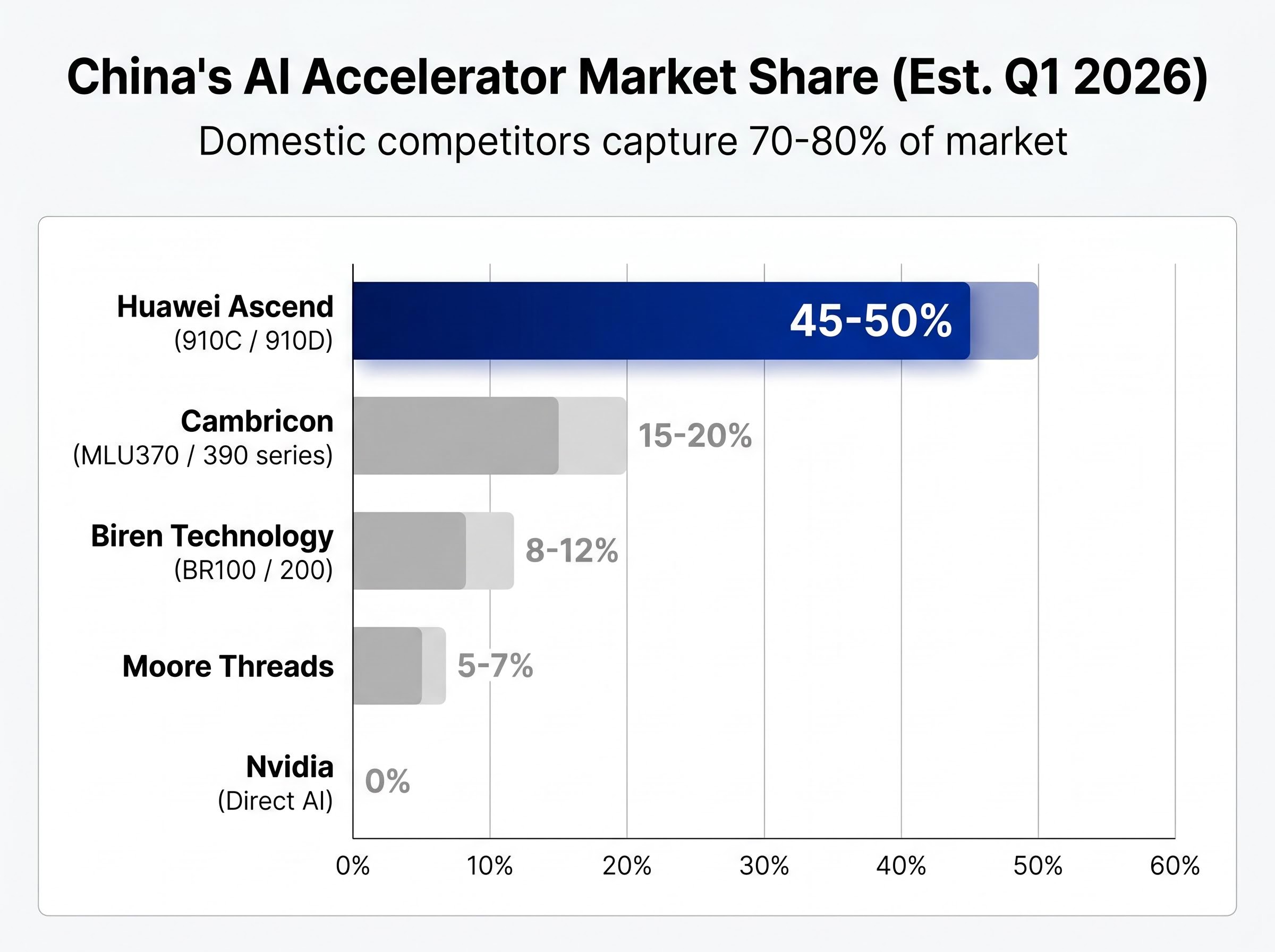

A common assumption is that export controls left a vacuum in China’s AI chip market. By Q1 2026, that vacuum had largely closed, faster than most Western analysts anticipated.

Domestic competitors, led by Huawei Ascend, collectively held approximately 70-80% of China’s AI accelerator market by Q1 2026, according to Bernstein. The shift was concentrated in a three-year window.

| Company | Key Products | Est. Q1 2026 China Market Share |

|---|---|---|

| Huawei Ascend | 910C / 910D (7nm-class) | 45-50% |

| Cambricon | MLU370 / 390 series | 15-20% |

| Biren Technology | BR100 / 200 (GPU-like) | 8-12% |

| Moore Threads | Various | 5-7% |

Performance parity claim: Bernstein reported that Huawei’s 910D matches approximately 80% of H100 performance at lower cost, materially reducing Chinese buyers’ incentive to pursue Nvidia products even if restrictions were eased.

China’s AI accelerator market is now estimated at $30-40 billion in 2026. Huang’s $50 billion figure encompasses broader AI infrastructure beyond accelerators alone, which explains why the opportunity appears large while the addressable share for Nvidia remains disputed.

The competitive displacement is the most underappreciated element of Nvidia’s China risk. Even a full diplomatic resolution would not restore the pre-2023 position. Chinese customers now have functioning domestic alternatives with government backing, and the software ecosystems built around those chips deepen with each quarter of adoption.

The same institutional capital rotation that displaced Nvidia in China is beginning to register in equity markets: Asian semiconductor alternatives, including SK Hynix with an estimated 52-70% of Nvidia’s HBM orders and Samsung approaching $1 trillion in market capitalisation, are attracting record foreign inflows even as U.S. chip stocks absorb the volatility from ongoing export control uncertainty.

The H200 licence framework, granted in December 2025, authorised approximately ten Chinese firms to purchase up to 75,000 units each through 2027 (Bloomberg, 5 January 2026). Approved buyers include:

No approvals have been granted for Blackwell architecture chips. The licences cover H200 units only.

Jensen Huang was personally invited by President Trump to join the Beijing summit delegation, added mid-journey during a stop in Alaska. The summit, running from 11 to 14 May 2026, saw Huang publicly advocating for expanded market access alongside Trump’s “open up” rhetoric (EM360Tech, 13 May 2026). The Financial Times reported a “tentative deal” for expanded H200 sales as of 14 May 2026, though outcomes remained pending and existing licence holders had not yet completed transactions.

The framing matters for interpreting any Nvidia-related headline from Beijing: summit communiques cannot govern chip export controls because those restrictions are set through agency rulemaking and executive orders, meaning symbolic gestures at the diplomatic level, however prominent Jensen Huang’s presence in the delegation, do not alter the legal framework that determines whether H200 or Blackwell shipments can proceed.

Jensen Huang stated on 28 April 2026 that Nvidia’s direct AI accelerator market share in China is now “zero percent”, as reported by Tom’s Hardware on 2 May 2026.

Nvidia shares rose approximately 1.8% in premarket trading on 14 May 2026. The premarket move reflects optimism about the diplomatic signal, but the structural constraints on H200 commercialisation, including Beijing’s buyer pressure and the absence of Blackwell approvals, limit the near-term revenue impact of any expanded licence framework.

The gap between the $50 billion headline and institutional base-case assumptions is where most valuation errors occur. Sell-side analysts and buy-side institutions largely treat China as a peripheral variable, not a thesis driver.

| Firm / Analyst | Stance | China Framing | Price Target |

|---|---|---|---|

| UBS (Timothy Arcuri) | Buy | “Summit could add $2-3B revenue, neutral to thesis” | $1,200 |

| Goldman Sachs (Toshiya Hari) | Hold | “Model excludes >5% China revenue” | $950 |

| Bernstein (Harlan Sur) | Neutral | “Domestic rivals are permanent fixtures” | N/A |

The consensus average price target sits at approximately $1,100 (Reuters poll, 13 May 2026). Summit-related news contributed to a 17% Nvidia stock drop in April 2026 (EM360Tech), illustrating how China headlines move the stock price even when analysts model China as peripheral.

Nvidia’s forward earnings multiple of approximately 24x reflects a notable compression from prior peak valuations, driven partly by China revenue uncertainty and partly by investor concern about custom ASIC competition from hyperscalers, with Broadcom’s locked-in multi-year contracts with Google and Meta providing a contrasting valuation benchmark that helps contextualise where Nvidia’s multiple sits relative to the broader AI chip investment landscape.

The three largest institutional positions represent three distinct poles of opinion.

BlackRock frames China as less than 3% of revenue and is monitoring the summit without adjusting positioning (Q1 2026 letter, Bloomberg). Vanguard models a base case of 0% direct China AI sales (Seeking Alpha, 5 May 2026). ARK Invest’s Cathie Wood argues that diplomacy could unlock the full $50 billion total addressable market (Financial Times, 10 May 2026).

Nvidia’s geographic risk is partially de-risked through fabrication partnerships in Taiwan and Malaysia, which some institutions cite when characterising China as a revenue risk rather than a supply-chain risk. The distinction matters for portfolio construction.

Bernstein’s Harlan Sur estimated in March 2026 that even under optimistic H200 approval scenarios, Nvidia’s ceiling in China sits at 10-15% market share. Goldman Sachs placed post-H200 recapture at approximately 20% of pre-ban revenue levels, constrained by Huawei’s dominance (January 2026).

Sam Bresnick at Georgetown’s Center for Security and Emerging Technology (CSET) stated that “full market recapture is impossible amid the broader U.S.-China technology rivalry” (WIRED, 29 January 2026).

For meaningful China market share recovery, four conditions would need to be met simultaneously:

Each condition is independently difficult. Together, they define a scenario that no major institutional model currently prices as a base case. China upside functions as a call option on geopolitical resolution, not a revenue driver that belongs in a base-case model for any long-term Nvidia position.

The analyst consensus buy rating with an average price target of approximately $1,100 reflects confidence in a thesis that does not require China revenue to materialise. The drivers that institutional models treat as the thesis foundation sit elsewhere:

China represented less than 1% of direct AI revenue in FY2026 Q1. The broader global data centre demand driving Nvidia’s revenue growth operates independently of diplomatic outcomes in Beijing. UBS’s Timothy Arcuri framed it directly: the summit “could add $2-3B revenue,” but remains “neutral to thesis.”

Nvidia’s fabrication partnerships in Taiwan and Malaysia provide additional geographic diversification, reducing the existential framing that some headlines attach to the China situation (BlackRock Q1 2026 letter).

The $50 billion China AI market figure is real, and Huang is right to pursue it. But investors who anchor their Nvidia thesis to Beijing outcomes are optimising for the wrong variable. Future China headlines are worth monitoring as updates on a call option. They do not redefine the structural case.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements regarding diplomatic outcomes, market share projections, and revenue estimates are speculative and subject to change based on regulatory developments and geopolitical conditions.

The H200 licensing framework, granted by the U.S. Bureau of Industry and Security in December 2025, authorises approximately ten Chinese firms to purchase up to 75,000 Nvidia H200 units each through 2027. No approvals have been granted for Nvidia's newer Blackwell architecture chips.

Nvidia CEO Jensen Huang stated on 28 April 2026 that Nvidia's direct AI accelerator market share in China is now zero percent, down from an estimated 95% before U.S. export controls tightened.

Domestic Chinese competitors, led by Huawei Ascend with an estimated 45-50% market share, collectively held approximately 70-80% of China's AI accelerator market by Q1 2026, according to Bernstein research.

Most major institutional investors treat China as a peripheral variable rather than a thesis driver, with Goldman Sachs excluding more than 5% China revenue from its model and Vanguard modelling a base case of 0% direct China AI sales as of early 2026.

Analysts identify four simultaneous requirements: a freeze on entity list expansions, U.S. approval of Blackwell architecture exports, Beijing lifting informal buyer pressure that neutralises existing H200 licences, and sustained underperformance by domestic rivals like Huawei.