EOS Shares Jump 4% as MARSS Wins €102M Counter-Drone Deal

2 hrs ago

Commonwealth Bank of Australia posted a $2.7 billion cash net profit for the three months ending 31 March 2026, with business lending expanding 12.5% year-on-year, a pace reportedly faster than the broader market. The result lands as Australian households and businesses absorb the combined pressures of a higher Reserve Bank of Australia (RBA) cash rate, persistent cost-of-living strains, and global macroeconomic uncertainty following the RBA’s May 2026 increase to 4.35%. CBA’s quarterly update provides the clearest real-time snapshot of how the nation’s largest lender is navigating these conditions. What follows is a breakdown of where the growth is coming from, what the credit quality signals reveal about financial stress in the economy, and what the result suggests for the bank’s near-term trajectory.

CBA’s Q3 FY26 cash net profit rose 4% year-on-year, the bank’s strongest quarterly comparison since the start of the current rate cycle.

The headline numbers tell a two-directional story. According to CBA’s quarterly update, CBA reported a cash net profit of $2.7 billion and a statutory net profit of $2.6 billion for Q3 FY26, representing a 4% improvement on the same quarter a year earlier.

Against the first half of FY26, the picture softens slightly. Q3 cash profit came in approximately 1% below the per-quarter average of H1 FY26, a marginal step back rather than a trend break.

Total operating income held flat across the quarter. CBA attributed the result to lending and deposit volume growth being offset by the impact of two fewer calendar days in the period. For investors, the year-on-year gain signals sustained earnings momentum; the quarter-on-quarter softness is a prompt to look past the headline and examine what is driving volume versus what is compressing margin.

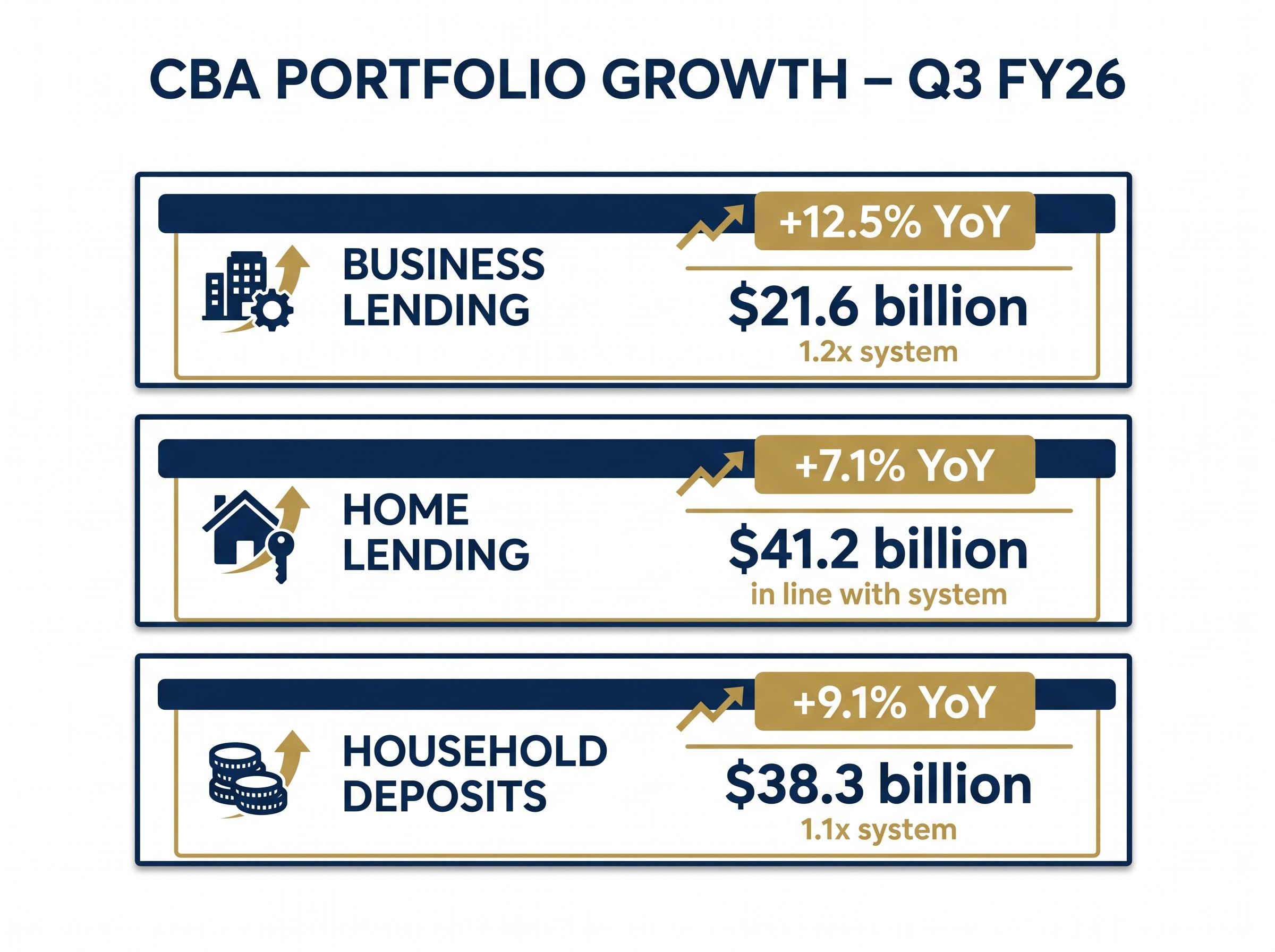

The standout number in the quarterly update is business lending growth of 12.5% year-on-year, representing $21.6 billion in additional loans and a pace 1.2 times the broader loan market. This is not a rising-tide result. It is a market share story.

Home lending grew 7.1% year-on-year ($41.2 billion), broadly in line with system growth. The asymmetry between the two segments is striking: CBA’s business book is expanding nearly twice as fast as its mortgage book.

Household deposits rose 9.1% year-on-year ($38.3 billion), reinforcing the strength of CBA’s funding base.

| Segment | YoY Growth | Volume |

|---|---|---|

| Business Lending | +12.5% (1.2x system) | $21.6 billion |

| Home Lending | +7.1% (in line with system) | $41.2 billion |

| Household Deposits | +9.1% (1.1x system) | $38.3 billion |

Operating expenditure rose modestly, driven by three factors in order of materiality:

These increases were partially offset by the shorter quarter and efficiency measures. Business lending growth at 1.2 times the market rate is the single most commercially significant data point in the result, suggesting CBA is actively gaining share in a segment that typically carries higher margins than retail home lending.

Australian major banks release quarterly trading updates rather than full earnings results. These updates disclose volume metrics, credit quality data, and headline profit figures, but they do not include full income statements, divisional breakdowns, or comprehensive margin analysis. Understanding what the update contains, and what it omits, matters for interpreting the numbers accurately.

The two profit figures CBA reported serve different purposes:

The $100 million gap between the two figures in Q3 FY26 reflects those non-recurring adjustments. For investors tracking CBA’s operational trajectory, cash profit is the more informative measure.

Interest income accrues daily. A quarter with two fewer calendar days mechanically reduces income even if the underlying loan book is growing. CBA disclosed that volume growth in lending and deposits offset this calendar effect, keeping operating income flat rather than negative.

Flat operating income in this context represents underlying growth when annualised, not stagnation. The 4% year-on-year cash profit comparison, which smooths for calendar effects, offers a more accurate reading of the bank’s earnings trajectory.

The growth story has a counterweight. CBA’s credit quality data reveals that volume momentum and financial stress are co-existing inside the same balance sheet.

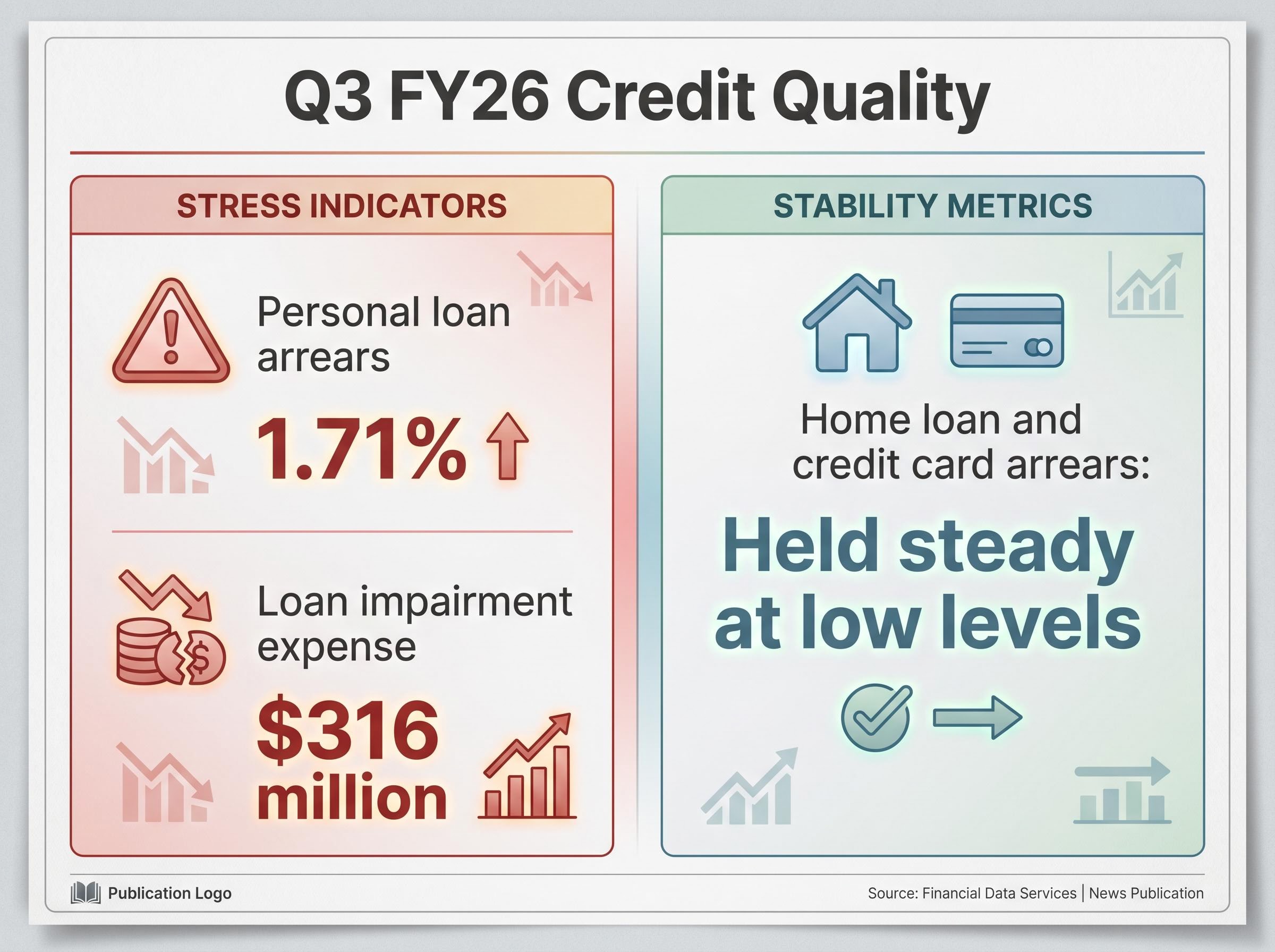

The divergence is telling. Secured lending, backed by property, remains stable. Unsecured lending, where borrowers have fewer buffers, is where rate and cost-of-living pressures are biting hardest. CBA characterised overall portfolio credit quality as remaining sound despite the personal loan movement.

Corporate insolvency rates reaching their highest level since the 1990–91 recession sit in direct tension with CBA’s business lending growth of 12.5%, and that tension is precisely what the collective provision expense is designed to absorb: lending volumes can expand while the pool of stressed borrowers widens simultaneously.

Collective provisions are a forward-looking buffer set against anticipated but not yet realised losses. They represent a bank’s judgment about the probability of future defaults across its loan book, rather than write-offs on loans already in distress.

According to CBA’s quarterly update, elevated collective provisions reflect “geopolitical and macroeconomic uncertainty” and broader global economic conditions.

The underlying net interest margin (NIM) remained broadly stable excluding non-recurring tailwinds, suggesting the margin compression story is one to watch in coming quarters rather than an immediate concern.

RBA monetary policy guidance indicates that the transmission of rate increases to household budgets typically operates with a lag of two to four quarters, meaning the full effect of the current 4.35% cash rate on borrower repayment capacity may not be fully visible in arrears data until late FY26 or early FY27.

CBA’s forward guidance was measured. The bank identified three macroeconomic headwinds expected to pressure household consumption and business activity:

The RBA’s May 2026 rate decision passed with eight of nine Board members voting for the hike, and forward guidance language that explicitly preserved full policy optionality, neither committing to a pause nor signalling a fourth move, leaving the trajectory of the cash rate dependent on Q2 CPI and labour market data due before the July meeting.

CBA stated its intent to “adapt strategic settings as conditions evolve,” language consistent with a bank preparing for multiple scenarios rather than committing to a single trajectory.

The Federal Budget delivered on 12 May 2026 introduces a further policy variable. Budget measures affecting housing, energy costs, and SME financing may shape demand for investor and household loans through FY27, though their impact on CBA’s lending volumes will only become visible in subsequent quarters.

For existing shareholders, the Q3 result offers reassurance: 4% year-on-year profit growth and above-system business lending momentum in a tightening environment. For prospective investors, the question is whether CBA’s premium valuation relative to dividend yield alternatives on the ASX already prices in this resilience.

Structural buying pressure on CBA shares from ASX 200 index weighting, compulsory superannuation inflows, and SMSF familiarity bias creates a persistent mechanical bid that analysts argue sustains the premium regardless of whether near-term earnings growth justifies a 28x multiple.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

The Q3 FY26 result presents two competing signals. On one side: business lending outperformance at 1.2 times the market rate and 4% year-on-year profit growth. On the other: personal loan arrears rising to 1.71% and a $316 million provision expense reflecting management’s caution about what lies ahead.

Whether Q4 FY26 represents an improvement or a step back depends on three variables that investors and market watchers should track closely:

CBA’s next scheduled disclosure will determine which side of this tension defines the FY26 full-year story.

For investors wanting to situate CBA’s Q3 result within the broader sector picture, our detailed coverage of Big Four analyst consensus ratings examines which banks carry buy versus sell majorities, how capital adequacy compares across the four, and why analyst price targets are not the primary concern driving bearish positions on CBA specifically.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Cash net profit excludes non-recurring items such as hedging and treasury adjustments, making it the preferred measure for comparing CBA's core performance across quarters. Statutory net profit is the IFRS-compliant figure that includes all one-off items and can be distorted by factors unrelated to ongoing business operations.

CBA reported a cash net profit of $2.7 billion and a statutory net profit of $2.6 billion for the three months ending 31 March 2026, representing a 4% improvement on the same quarter a year earlier.

CBA's business lending grew 12.5% year-on-year, which is 1.2 times the broader market rate, while home lending grew 7.1% broadly in line with system growth, suggesting CBA is actively gaining market share in a segment that typically carries higher margins than retail mortgages.

Personal loan arrears rising to 1.71% in Q3 FY26 indicates that unsecured borrowers are feeling the most pressure from higher interest rates and cost-of-living strains, while secured home lending remains stable. CBA set aside a $316 million loan impairment expense as a forward-looking buffer against potential future losses.

The RBA's rate increase to 4.35% in May 2026 adds pressure to household budgets and business activity, with the full effect on borrower repayment capacity potentially not visible in arrears data until late FY26 or early FY27 due to the typical two-to-four quarter transmission lag.