EOS Shares Jump 4% as MARSS Wins €102M Counter-Drone Deal

1 hr ago

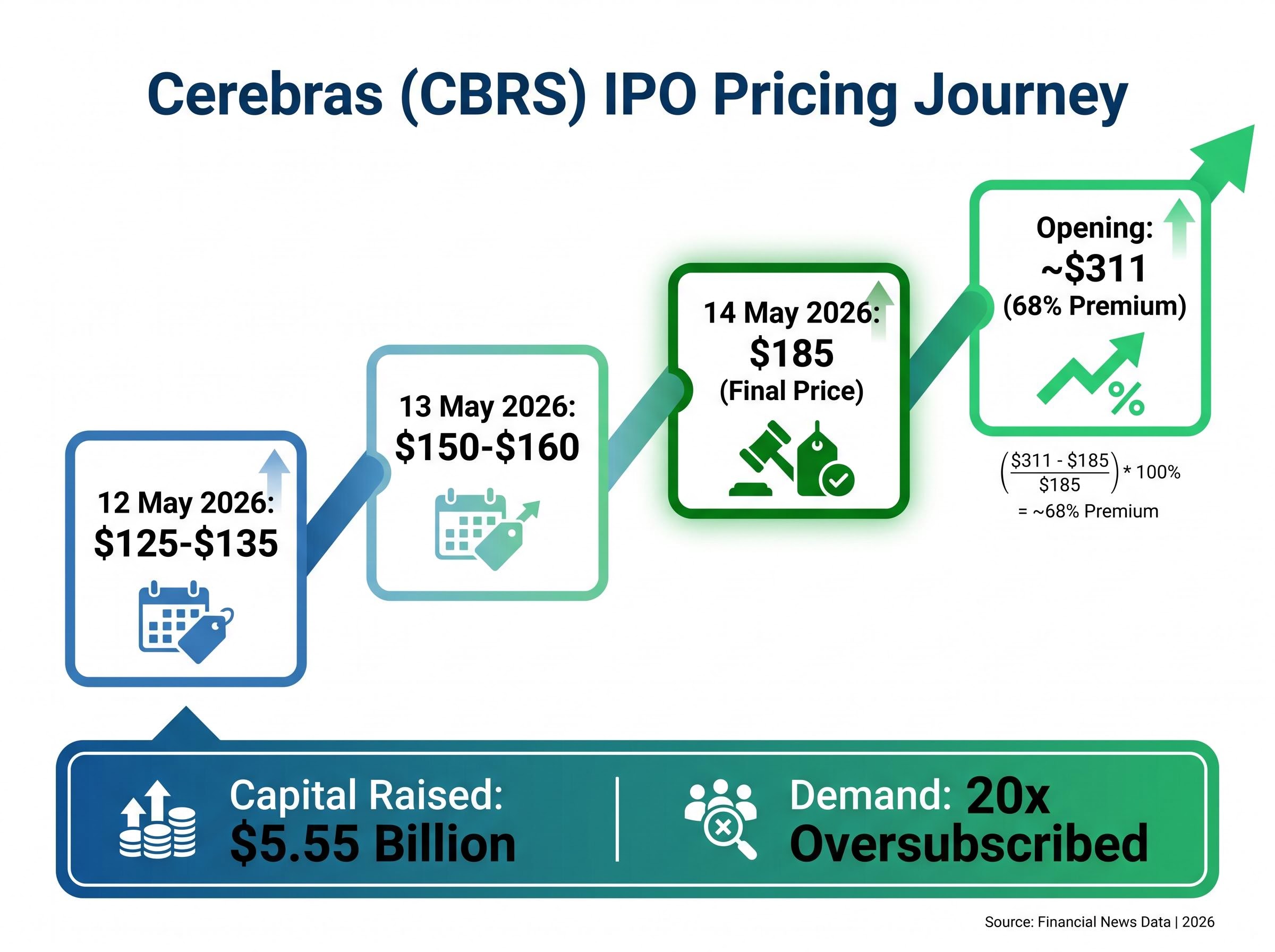

Cerebras Systems priced its IPO at $185 per share on 14 May 2026. By the close, shares were trading at approximately $311, a 68% first-day premium that implied a $95 billion company had arrived on public markets in a single session. The Cerebras IPO landed on a day already charged with AI momentum: the S&P 500 notched its 18th record close of the year, Nvidia extended a multi-session rally, and Cisco raised its AI hyperscaler order target to $9 billion. Cerebras did not merely benefit from that backdrop; it amplified it. What follows unpacks the mechanics of the debut, the company’s financials and technology, the valuation debate now splitting early commentary, how related stocks moved on the session, and what the listing signals about where AI infrastructure capital is flowing in 2026.

The final terms tell the story of demand outrunning every estimate the roadshow put forward. Cerebras listed on the ticker CBRS, raised approximately $5.55 billion, and opened at roughly $311 per share, 68% above the $185 issue price.

The pricing journey was itself a signal. The range moved three times in three days:

Each revision reflected institutional appetite the underwriters had underestimated. The deal was reportedly 20x oversubscribed during book-building, a figure that forced the repeated upward adjustments and that placed it comfortably as the largest US IPO of 2026.

The AI investment cycle now absorbs a record 4.9% of US GDP in IT spending, a level that surpasses both the dot-com era peak of approximately 4.2% and the cloud buildout peak, providing the macro foundation that allowed a single AI chip debut to attract 20x oversubscription during book-building.

The 68% first-day premium on $5.55 billion raised implied a post-IPO market capitalisation of approximately $95 billion, making Cerebras the most valuable pure-play AI hardware company to debut on US exchanges this year.

Analysts have cautioned, however, that oversubscription at the IPO price does not indicate conviction at $300+ aftermarket levels. The gap between allocation demand and secondary-market staying power will only become visible in the weeks ahead.

Most AI compute relies on clusters of individual graphics processing units (GPUs) wired together across server racks. Cerebras took a different approach. Its wafer-scale engine (WSE) is a single chip that spans an entire silicon wafer, delivering substantially higher transistor density and memory bandwidth than a conventional GPU cluster occupying the same footprint.

That architectural difference matters most for inference, the stage of AI computation where a trained model processes new inputs and delivers outputs in real time. Inference workloads reward low latency and high throughput, not just raw training horsepower, and the WSE’s unified memory architecture is designed to serve those priorities without the inter-chip communication bottlenecks that GPU clusters face.

Nvidia’s CUDA software ecosystem remains deeply entrenched at the model-training layer, where most AI spending still concentrates. Cerebras is betting that inference at scale creates a second competitive front where architectural differentiation can win customers that GPU-only solutions cannot serve as efficiently.

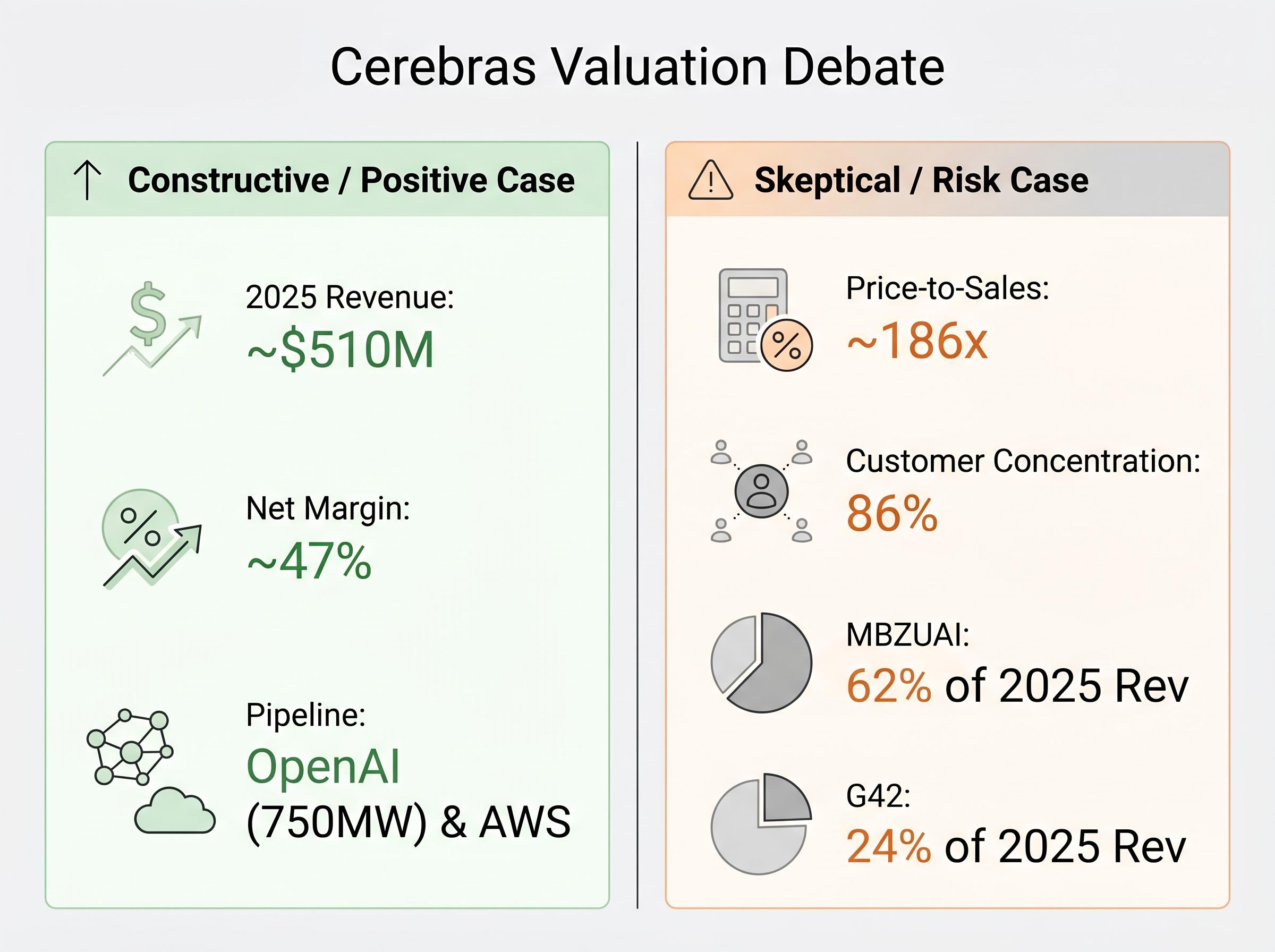

The company’s 2025 revenue reached approximately $510 million, with a net margin of roughly 47%, a level of profitability that few pre-IPO AI hardware vendors have demonstrated. Its forward pipeline includes:

CoreWeave, which IPO’d in March 2026 at a $23 billion valuation while not yet profitable, is the nearest public comparable, though it operates as a GPU cloud infrastructure provider rather than a chip designer. The distinction matters: Cerebras is selling silicon; CoreWeave is renting it.

At approximately $95 billion in implied market capitalisation on $510 million in 2025 revenue, Cerebras is trading at roughly 186x trailing sales. That multiple sits well above even Nvidia’s elevated AI-era valuation and has split early market commentary into two sharply opposed camps.

Valuation frameworks for AI stocks, including the Shiller CAPE ratio at 40.11, Minsky’s financing stages, and behavioural sentiment indicators, collectively suggest elevated but not yet indiscriminate speculative conditions, a reading that sits uncomfortably alongside a debut multiple of 186x trailing sales.

The constructive case rests on profitability, differentiation, and pipeline. TradingKey (writing on 12 May 2026) framed the 47% net margin and the OpenAI deal as justification for a strategic infrastructure premium, noting that Cerebras is profitable at scale where CoreWeave was not at its own IPO. If the backlog converts, the multiple compresses quickly.

The sceptical case focuses on what the revenue base actually looks like today.

Benzinga, writing on 14 May 2026, argued investors are “paying a growth premium for a business that has not yet demonstrated it can grow profitably” beyond its current customer base.

That current customer base is concentrated to a degree that cuts across both bull and bear narratives:

Combined, 86% of revenue sits with two UAE-linked entities, neither of which is the OpenAI or AWS name featured in forward-looking pipeline disclosures. The geopolitical and regulatory dimensions of that concentration add a layer of risk that the headline growth figures do not capture on their own.

The SEC prospectus risk disclosures filed with the Cerebras S-1 enumerate the customer concentration exposure in formal regulatory language, identifying MBZUAI and G42 by name as the sources of the 86% revenue concentration and flagging the geopolitical dimensions of those relationships as a material risk factor.

| Metric | Cerebras (CBRS) | Nvidia (NVDA) | CoreWeave |

|---|---|---|---|

| Market cap | ~$95B (post-IPO) | Approaching $6 trillion | ~$23B (March 2026 IPO) |

| 2025 revenue | ~$510M | Multi-tens of billions | Not disclosed |

| Net margin (2025) | ~47% | High (established) | Not profitable at IPO |

| Price-to-sales | ~186x | Elevated but far lower | N/A |

| Key risk | Customer concentration (86%) | Regulatory / export controls | Revenue scale / path to profit |

Nvidia’s rally on 14 May 2026 drew from two reinforcing catalysts. The Cerebras debut validated AI infrastructure spending at a scale the market had not yet priced into a single-day IPO event, while the US Commerce Department cleared sales of H200 chips to approximately 10 Chinese technology firms, including Alibaba, Tencent, ByteDance, and JD, with each buyer capped at 75,000 chips.

The clearance arrived during Nvidia’s seventh consecutive session of gains, a run that had already pushed the company’s market capitalisation toward $6 trillion. The Cerebras listing added momentum to an already-extended move rather than initiating it.

The Cerebras debut did not land in isolation. Four corroborating data points hit the tape on the same session:

Each of these, independently, would have moved sector sentiment. Together, they formed the fundamental scaffolding that gave the Cerebras valuation room to breathe on its first day of trading.

The S&P 500 closed at 7,501 on 14 May 2026, up 0.77%, marking its 18th record close of the year and the first time the index crossed the 7,500 level. The Information Technology sector led all sectors with a 1.85% gain.

The 18th record close in a single calendar year places 2026 on pace with the long-run historical average of approximately 18.5 record closes annually since 1957, suggesting the AI-driven rally is sustaining a historically normal pace of new highs rather than producing an anomalous frequency.

The broader indices confirmed the session’s risk-on character:

The VIX declined 3.41% to 17.26, and Bitcoin recovered above $80,000 with an approximately 3% gain on the session. The cryptocurrency move suggested risk appetite extended beyond equities, with AI optimism functioning as a broader catalyst across speculative asset classes.

Materials was the weakest sector, down 0.80%, a divergence that reinforced the theme-specific nature of the session’s strength. This was an AI infrastructure day, not a broad cyclical rally.

CoreWeave entered public markets in March 2026 at a $23 billion valuation without demonstrating profitability. It was, briefly, the benchmark for AI infrastructure IPOs. Cerebras has reset that benchmark by a factor of four, delivering a $95 billion debut with 47% net margins and a $5.55 billion capital raise.

Financial commentary suggests smaller AI chip startups and RISC-V accelerator vendors may pull forward IPO timelines in response to the demand signal Cerebras provided. As of mid-May 2026, however, no named US AI chip company had formally cited the Cerebras debut in SEC documents. The pipeline acceleration remains anticipatory rather than confirmed.

The Cerebras debut generated a valuation; it did not generate a complete informational picture. Three categories of data remain unavailable:

Until these arrive, the only price discovery mechanism for CBRS is the open market itself, which opened 68% above issue price and has not yet been tested by a sustained risk-off session.

The session of 14 May 2026 delivered a rare convergence. Cerebras debuted at a $95 billion valuation. The S&P 500 crossed 7,500 for the first time. Cisco beat and raised. Applied Materials guided semiconductor equipment growth above 30%. TSMC revised its chip market forecast upward by $500 billion. Nvidia extended its rally toward a $6 trillion market capitalisation.

Each data point reinforced the others. Together, they validated AI infrastructure as the dominant capital allocation theme of the year.

The tension sits beneath the surface. The Cerebras valuation is a bet on pipeline execution: the OpenAI 750MW agreement and the AWS relationship converting into diversified revenue before the concentrated 2025 customer base becomes a liability. Investors who bought at $311 are pricing in that conversion.

Three forward markers will determine whether the premium proves prescient or premature:

The AI infrastructure trade is intact. The Cerebras debut made it larger, louder, and more expensive. Whether it also made it more fragile depends entirely on what happens when the contracts behind the $95 billion price tag start producing, or fail to produce, actual revenue.

Investors deciding how to position around the Cerebras debut and the broader AI infrastructure trade will find our comprehensive walkthrough of AI infrastructure stock allocation, which covers the three-layer hardware, cloud, and software framework, specific ticker-level examples at each layer, and the concentration and multiple-compression risks that determine how much AI infrastructure exposure is appropriate for a given portfolio.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Cerebras Systems is an AI chip company that went public on 14 May 2026, pricing its IPO at $185 per share under the ticker CBRS and raising approximately $5.55 billion in the largest US IPO of 2026.

A wafer-scale engine (WSE) is a single chip that spans an entire silicon wafer, delivering higher transistor density and memory bandwidth than a conventional GPU cluster; Cerebras uses this architecture to target AI inference workloads where low latency and high throughput matter most.

Cerebras shares opened at approximately $311 on their first day of trading, a 68% premium above the $185 IPO price, implying a post-IPO market capitalisation of approximately $95 billion.

86% of Cerebras' 2025 revenue came from two UAE-linked entities: MBZUAI (62%) and G42 (24%), creating significant concentration risk that is flagged in the company's SEC prospectus as a material risk factor.

Underwriter coverage from banks including Morgan Stanley, Citi, Barclays, and UBS is restricted for approximately 25-30 days post-IPO, meaning the first formal analyst ratings and price targets are expected no earlier than mid-June 2026.