Citi Puts Memory Supply Above Chip Design in AI Stock Rankings

1 hr ago

While retail and institutional investors have spent much of the past year chasing AI-driven semiconductor stocks higher, at least one global asset manager is quietly rotating capital in the opposite direction, toward supermarket shelves, beer bottles, and dishwashing liquid. Australian consumers in May 2026 are absorbing a 4.35% RBA cash rate and 4.6% annual CPI inflation, conditions that have battered household budgets and pressured branded goods companies across the ASX. Markets have responded by de-rating the consumer staples sector relative to technology, leaving valuations at or near multi-year lows on a global basis. That same environment, however, is precisely what Morningstar Investment Management and Franklin Templeton are treating as an opportunity signal rather than a warning. What follows is an examination of the contrarian case for beaten-down consumer staples and household goods stocks, how institutional investors identify value when sentiment is weakest, and the real risks that separate genuine mispricing from a value trap.

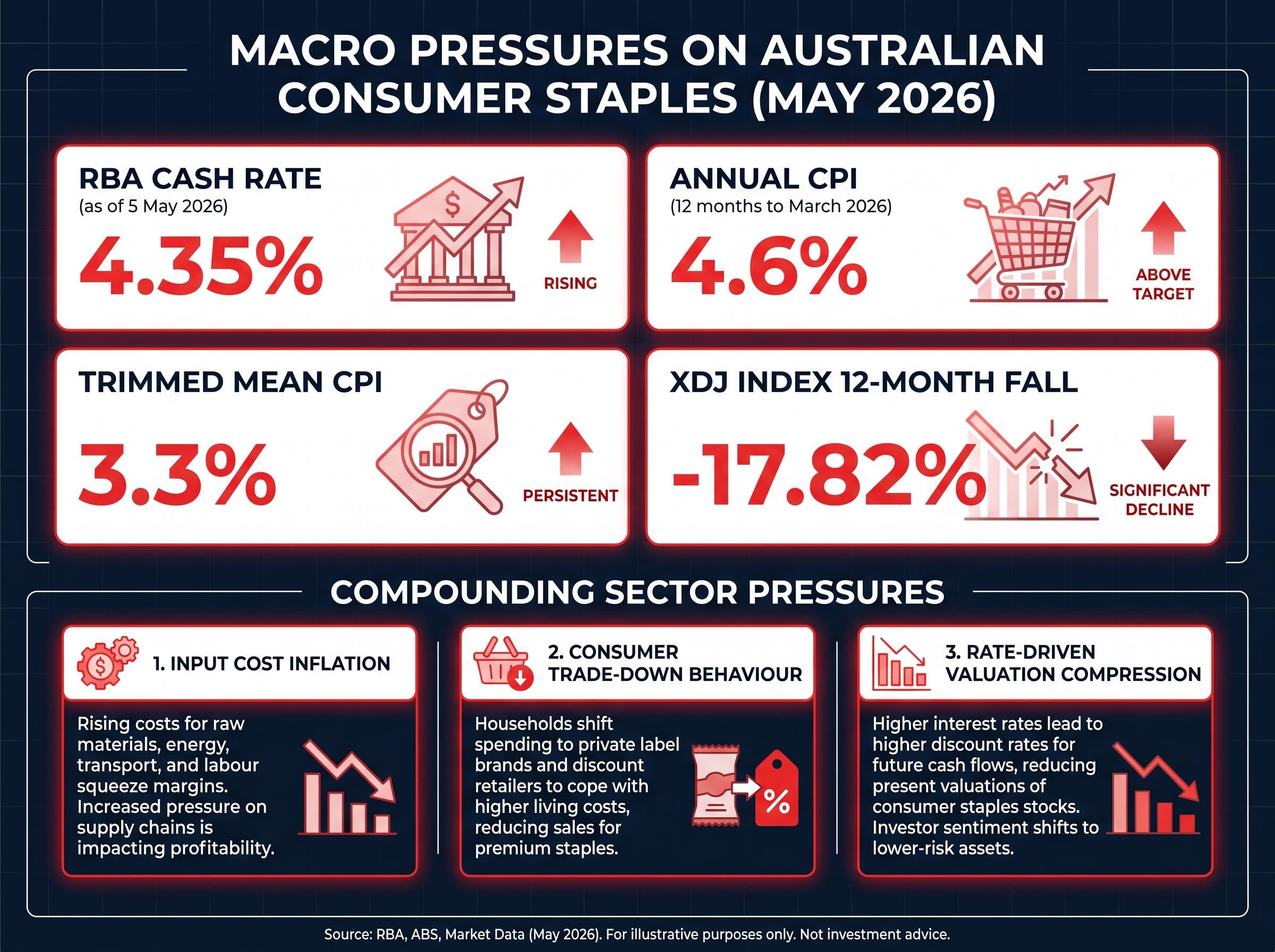

The macro backdrop facing Australian consumer staples companies is blunt. The Reserve Bank of Australia holds the cash rate at 4.35% as of 5 May 2026. Annual CPI reached 4.6% in the 12 months to March 2026, with trimmed mean inflation at 3.3%, according to the Australian Bureau of Statistics. Household budgets are under sustained compression, and the spending response has been predictable: consumers are trading down.

Trimmed mean inflation at 3.3% is the RBA’s preferred underlying measure precisely because it strips out volatile components like energy prices, making it the more reliable signal for assessing whether input cost pressures facing staples producers are likely to persist or moderate in coming quarters.

RBA monetary policy decisions confirm the cash rate has been held at 4.35% since late 2023, a sustained restrictive stance that has progressively compressed household disposable income and weighed on consumption-sensitive sectors including branded consumer goods.

Three compounding pressures are weighing on the sector simultaneously:

Against that backdrop, the AI-driven semiconductor rally has pulled investor attention, and capital, toward technology names. The ASX Consumer Discretionary index (XDJ) fell approximately 17.82% over the 12 months to May 2026, a related but distinct signal of how rate-sensitive consumer sectors have suffered.

Franklin Templeton noted in March 2026 that consumer staples relative price-to-earnings multiples sit near multi-year lows globally, a level of valuation discount not seen for an extended period.

That valuation gap is the precondition for any contrarian thesis. It is not, on its own, evidence the thesis is correct.

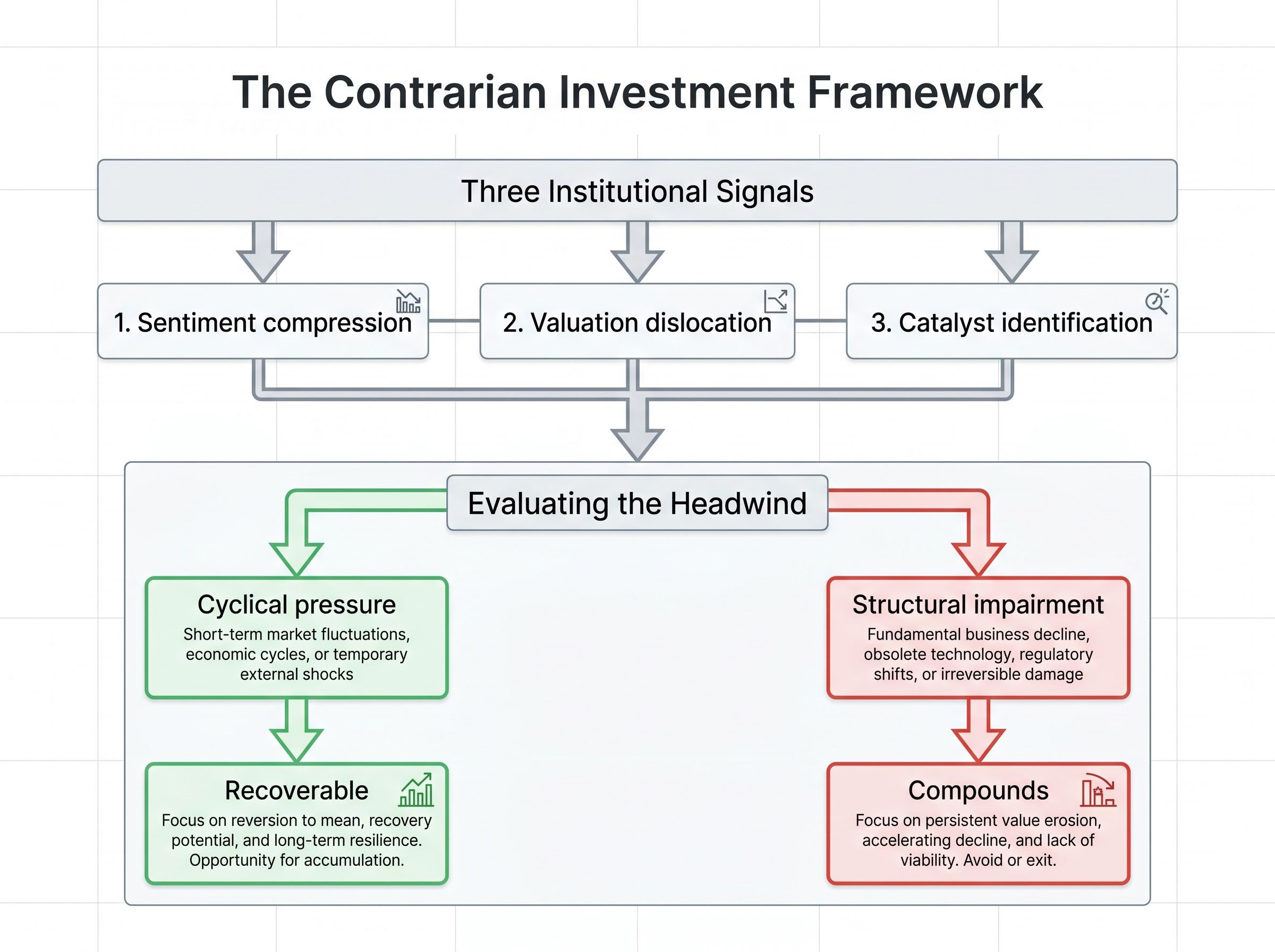

Contrarian investing is frequently misunderstood as simply buying whatever the market dislikes. The actual discipline is narrower and more demanding: it involves buying assets where prevailing sentiment has driven valuations below long-term intrinsic value, and where the reasons for that sentiment are identifiable, temporary, and recoverable.

The distinction the thesis depends on is between cyclical headwinds and structural impairment. The former is recoverable. The latter compounds.

Institutional managers typically look for three signals before building a contrarian position:

Sentiment compression, where extreme pessimism in survey data coincides with equity market resilience, has historically marked contrarian entry points rather than the onset of sustained declines, a pattern visible in the April 2026 University of Michigan reading hitting record lows while the S&P 500 held near all-time highs.

Morningstar Investment Management’s Dennis Li, Associate Portfolio Manager, stated in May 2026 that the firm’s preference is for sectors where market sentiment is weak and valuations already price in significant negative expectations. Franklin Templeton characterised re-rating potential in consumer staples as dependent on an earnings recovery outlook materialising. Separately, DNR Capital has been cited as describing “developing but not fully mature” contrarian conditions in Australian equities, though this characterisation could not be independently verified and is noted here as directional context only.

A company losing volume because consumers are trading down during a cost-of-living crisis is experiencing cyclical pressure. The behaviour reverses when real incomes recover. A company losing volume because its category has been permanently displaced by a substitute, say a physical product replaced by a digital alternative, is experiencing structural impairment. That loss does not reverse.

The contrarian investment strategy only applies to the former. The question for Australian consumer staples is which description fits the current environment.

Franklin Templeton confirmed in March 2026 that multiple strategies within the firm have been selectively increasing consumer staples exposure. The rationale rests on three pillars:

Franklin Templeton attributes the broader rotation from technology toward defensives partly to fears of overstretched technology valuations and concerns about AI disruption to corporate earnings more broadly.

ASX capital rotation in May 2026 has not been uniform: while healthcare and consumer discretionary absorbed the sharpest de-ratings, materials, energy, financials, and utilities recorded simultaneous new highs during the same period, illustrating that the institutional defensive pivot toward staples is one expression of a broader portfolio repositioning across the market.

Morningstar Investment Management has identified out-of-favour consumer sectors, including beverages and branded household goods, as potentially undervalued. Dennis Li noted that the market may be applying overly short-term assumptions while underweighting long-term cash flow generation potential in these sectors.

Commentary from Wilson Asset Management and TAMIM Asset Management on Australian staples was present in available research, with Wilson’s Matt Haupt reportedly identifying Woolworths as a selective value opportunity and TAMIM characterising inflationary pressures as manageable cyclical challenges. Neither position could be independently verified, however, and both are noted here as directional context rather than confirmed institutional stances.

Institutional interest is a necessary condition for a valid contrarian thesis. It is not a sufficient one.

Moving from the abstract to the specific clarifies what the contrarian framework demands at the company level. Woolworths Group (ASX: WOW) and Orora Limited (ASX: ORA) offer contrasting illustrations.

Woolworths represents the cleaner contrarian candidate. Australia’s largest supermarket operator faces an active ACCC court case, initiated in 2024 and ongoing as of 2 May 2026, accusing the company of misleading discount practices. The regulatory and reputational overhang has weighed on the stock. The contrarian reading: the ACCC case is identifiable, its resolution (whether through settlement or court outcome) is a potential catalyst, and the underlying business, which sells food to a growing population, is not structurally impaired.

Within the broader staples universe, the alcoholic beverages sub-sector has been flagged in available commentary as a contrarian opportunity where the market may be conflating cyclical volume pressure with permanent structural decline. Trade tariff concerns and moderation trends have weighed on the category.

| Company | Primary Contrarian Thesis | Key Risk / Complication | Analyst Data Availability |

|---|---|---|---|

| Woolworths (WOW) | Regulatory noise depressing valuation of a structurally sound essential goods business | ACCC case outcome uncertain; adverse ruling could introduce material liability | Forward EPS, price targets, consensus ratings not verified for May 2026 |

| Orora (ORA) | Acquisition-driven earnings reset creating apparent valuation discount | Saverglass facility halted; FY26 guidance revised downward; exogenous operational disruption | Post-downgrade consensus and recovery timeline not verified for May 2026 |

Orora illustrates the opposite outcome. The company’s acquisition of French glass packaging manufacturer Saverglass introduced material operational risk. As of April 2026, a Saverglass production facility has been halted due to disruption linked to Middle East conflict. Earnings have been reset and FY26 guidance revised downward.

A stock can appear cheap because earnings have been legitimately impaired, not because the market has over-discounted temporary noise. Orora’s situation shows how an exogenous disruption, geopolitical and operational in nature, can transform what looked like a contrarian opportunity into a deteriorating fundamental story. The discount is real; the question is whether it reflects opportunity or accurate repricing of diminished prospects.

Readers should consult Morningstar Australia, Refinitiv, or Bloomberg consensus data before drawing investment conclusions on either stock. Specific forward earnings estimates, analyst price targets, and consensus ratings for both WOW and ORA as of May 2026 were not available in this analysis.

A contrarian thesis that cannot survive scrutiny of its own risks is not a thesis. Three categories of risk bear directly on the consumer staples case.

Macro risks:

Company and sector-specific risks:

The “depressed valuation” argument at the ASX sector level cannot be fully confirmed for May 2026. Current ASX 200 consumer staples P/E and price-to-book data relative to the broader index were not independently verified in available research. The thesis rests partly on global relative P/E data from Franklin Templeton (March 2026) that may not translate directly to ASX-listed companies. Readers should consult S&P Global, Morningstar Direct, or ASX sector data portals for verification.

The structural advantage a long-term investor holds in a contrarian position is time. Short-term sentiment can remain wrong, or at least unresolved, longer than most investors are willing to hold. The return, if it materialises, accrues to those who maintain conviction through the period of maximum negativity.

Morningstar Investment Management’s broader investment discipline, as articulated by Dennis Li in commentary on geopolitical volatility, centres on focusing on company fundamentals rather than political or sentiment headlines. Franklin Templeton framed re-rating potential in consumer staples as conditional on an earnings recovery trajectory, not as an immediate event.

DNR Capital’s characterisation of “developing but not fully mature” contrarian conditions, while unverified, suggests the opportunity may still be building rather than at full expression. Patience, in this context, is not passive waiting. It is the active discipline of monitoring catalysts: ACCC case resolution for Woolworths, CPI normalisation reducing RBA rate pressure, and earnings recovery in staples companies outperforming depressed consensus estimates.

For investors wanting to model the specific scenarios under which input cost normalisation might occur, our full explainer on the RBA rate path to 2026 maps the Q2 CPI triggers, the Federal Budget implications, and the futures-market-implied terminal rate of approximately 4.68%, providing the rate timeline that determines when the earnings recovery catalyst the contrarian thesis depends on becomes plausible.

Before committing capital, Australian investors should follow a structured due diligence process:

Several institutional views referenced in this analysis, including those attributed to Wilson Asset Management, TAMIM Asset Management, and DNR Capital, could not be independently verified. These should be confirmed through primary sources before being incorporated into any personal investment rationale.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The confirmed analytical pillars are straightforward: global consumer staples relative valuations sit near multi-year lows, according to Franklin Templeton’s March 2026 analysis. Institutional accumulation is underway. The macro environment, a 4.35% cash rate and 4.6% CPI, is creating temporary headwinds for a sector whose products remain non-discretionary.

What remains unresolved is equally clear: ASX-specific valuation confirmation, the timing of any earnings recovery, and individual stock outcomes, from Woolworths’ litigation to Orora’s facility resumption, are open questions.

The contrarian investment strategy for Australian consumer staples is intellectually coherent and institutionally supported. It is not, however, a buy signal. It is a framework for identifying where to direct deeper due diligence, one that requires patient capital, verified data, and rigorous stock selection rather than a blanket bet on a beaten-down sector. The crowd may be looking the wrong way. That does not automatically mean looking the other way is right. It means it is worth investigating.

A contrarian investment strategy involves buying assets where prevailing negative sentiment has driven valuations below long-term intrinsic value, with the expectation that the reasons for that pessimism are temporary and recoverable rather than permanent and structural.

Consumer staples stocks are near multi-year valuation lows due to three compounding pressures: elevated input cost inflation squeezing margins, consumer trade-down behaviour toward private-label alternatives, and higher discount rates mechanically reducing the present value of defensive earnings streams.

Franklin Templeton confirmed in March 2026 that multiple strategies within the firm have been selectively increasing consumer staples exposure, while Morningstar Investment Management has identified out-of-favour consumer sectors including beverages and branded household goods as potentially undervalued.

The key distinction is between cyclical headwinds, where volume or earnings pressure reverses when macro conditions improve, and structural impairment, where a business has been permanently displaced by a substitute or irreversible trend; Orora is cited in the article as an example where exogenous disruption transformed an apparent contrarian opportunity into a deteriorating fundamental story.

Potential re-rating catalysts include resolution of the ACCC court case against Woolworths, normalisation of input cost inflation as CPI trends lower, a reduction in RBA rate pressure, and earnings results that outperform depressed consensus estimates across the sector.