RBC Raises S&P 500 Target to 8,150, Warns of 10% Pullback Risk

2 hrs ago

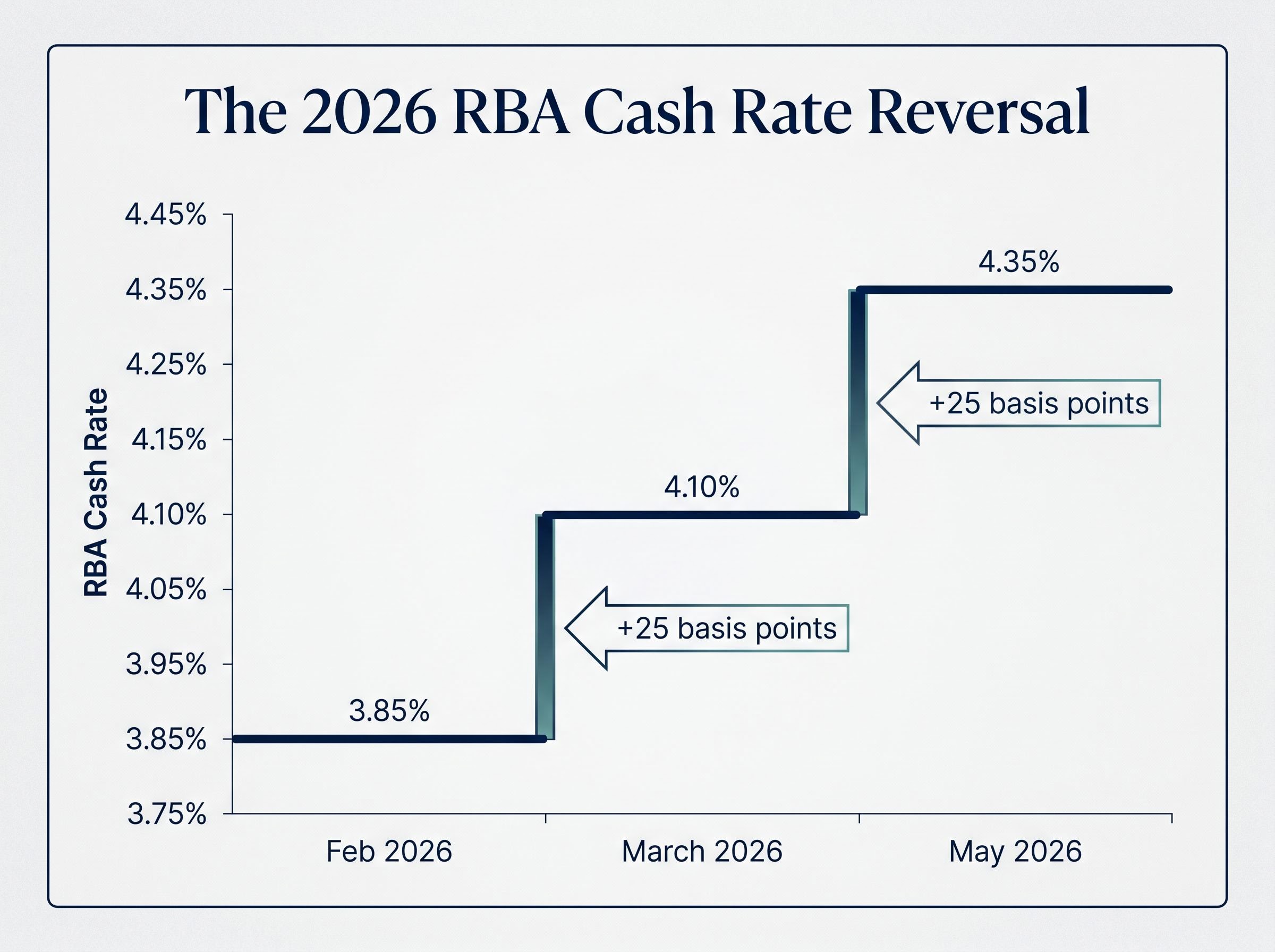

Australia’s cash rate has returned to 4.35%, the same peak reached during the prior tightening cycle in early 2024. The Reserve Bank of Australia lifted the rate by 25 basis points on 5 May 2026, its third consecutive hike this year, reversing nearly all of the easing delivered across 2025. The decision landed one week before the Federal Budget, in an environment where headline consumer price inflation has climbed to 4.6% and global energy pressures show no sign of abating. For mortgage holders, superannuation investors, and anyone watching the trajectory of borrowing costs, the question is no longer what happened but what it means for the months ahead. This article explains the data behind the decision, maps the conditions under which the RBA might hike again or pause, and identifies the specific dates and releases that will determine which way policy moves next.

The Board’s 5 May decision brought the cash rate from 4.10% to 4.35%, completing a three-step reversal that began in February. The sequence tells its own story:

Each move was 25 basis points. Together, they have unwound the bulk of the rate relief delivered during 2025 and returned borrowing costs to the level the Board held through most of 2024.

The RBA May 2026 monetary policy decision confirmed that the Board raised the cash rate by 25 basis points to 4.35%, citing elevated inflation, capacity pressures, and the transmission of Middle East conflict into domestic fuel and energy costs as the primary factors driving the move.

The full vote breakdown has not yet been published. Board meeting minutes are expected around 19 May, and those will reveal the degree of internal consensus. What is already clear is the direction: the inflation data left limited room for any other outcome.

Governor Michele Bullock described the current policy stance as “a bit restrictive,” a signal that the Board is tightening deliberately but remains conscious of the cumulative pressure being applied to households and businesses.

That characterisation matters. It tells borrowers the Board is not on autopilot; it is watching the data at each meeting. But the data, so far, has pointed one way.

Two numbers dominated the Board’s deliberations, and neither offered grounds for a pause.

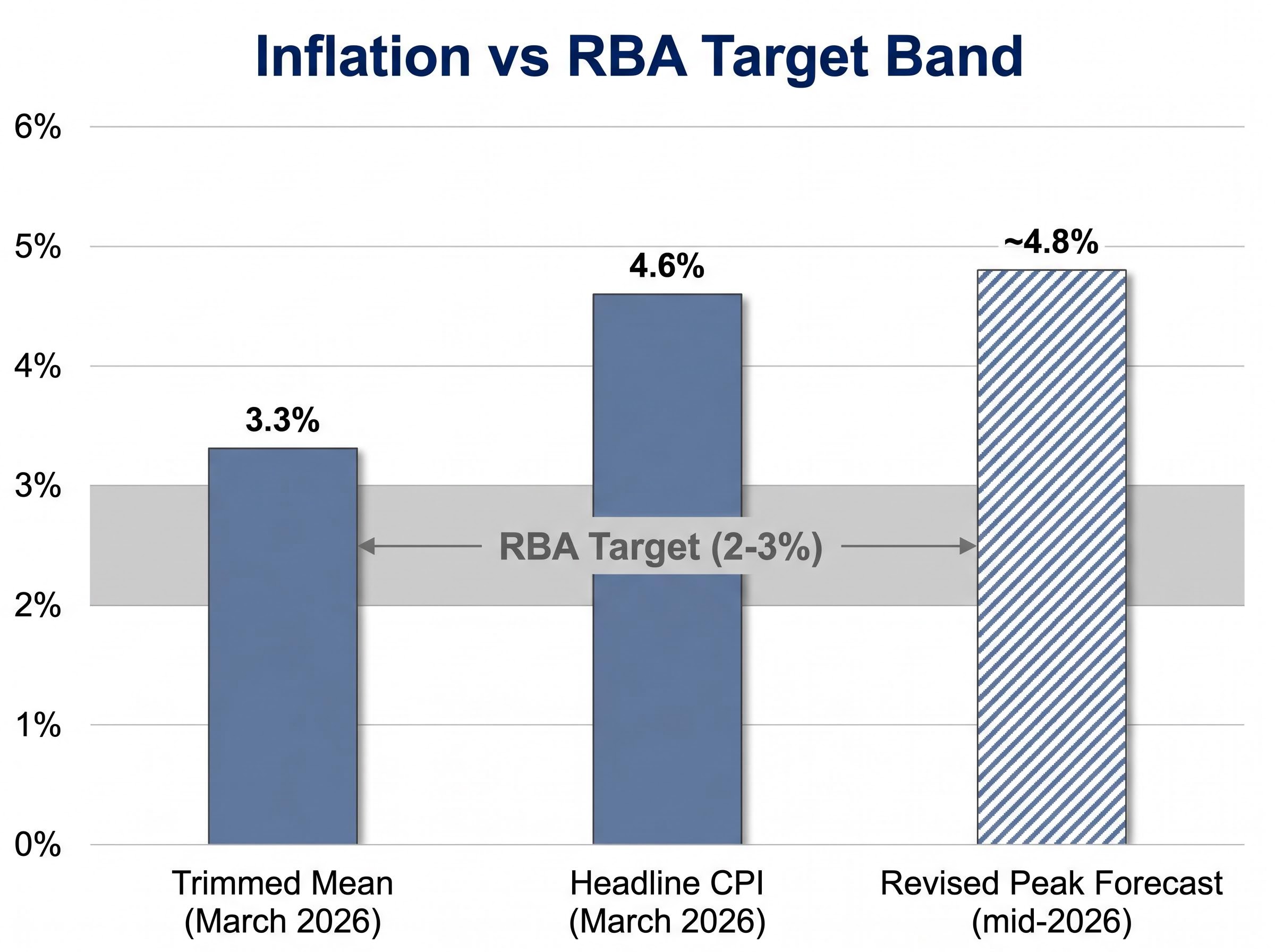

Headline CPI came in at 4.6% for the year to March 2026, the highest reading since 2023. Trimmed mean inflation, the underlying measure that strips out volatile items, printed at 3.3% over the same period. The RBA’s target band sits at 2-3%. Both measures remain above it.

The ABS CPI data for March 2026 confirmed headline inflation at 4.6% over the year and trimmed mean inflation at 3.3%, both sitting above the RBA’s 2-3% target band and providing the statistical foundation for the Board’s decision to tighten.

The distinction between the two readings is itself informative. Headline CPI captures everything consumers pay for, including fuel and fresh food. Trimmed mean excludes the most volatile components to reveal the underlying trend. When both are elevated, the Board has little room to argue that inflation is merely a temporary supply-side problem.

The RBA’s own forecasts shifted materially after the decision. Before 5 May, the Bank had projected headline inflation peaking near 4.2% around mid-2026. The revised projection now places the peak at approximately 4.8%, with underlying inflation expected to remain above 3% through late 2027.

| Measure | March 2026 actual | RBA target | RBA revised peak forecast |

|---|---|---|---|

| Headline CPI | 4.6% | 2-3% | ~4.8% (mid-2026) |

| Trimmed mean | 3.3% | 2-3% | Above 3% through late 2027 |

The quarterly trimmed mean came in slightly below expectations, providing marginal reassurance that domestic price pressures were not independently re-accelerating. That sliver of good news was not enough to change the outcome.

The second inflation driver is external. Middle East conflict has kept global energy costs elevated, and those costs flow into Australian consumer prices through three channels: fuel, transport, and manufacturing inputs.

The RBA flagged this transmission as a specific concern. What began as a temporary pass-through from higher oil prices is beginning to embed into broader pricing decisions. Businesses facing persistently higher energy and freight costs are passing them on rather than absorbing them, and that behaviour, once established, is difficult to reverse without tighter monetary conditions.

The energy cost pass-through mechanism runs further than the petrol pump: elevated Brent crude prices lift transport and freight costs, which then flow into the price of goods that depend on energy-intensive supply chains, meaning a sustained oil shock compounds itself across the CPI basket over successive quarters.

The Board is therefore fighting two overlapping problems: a global energy shock it cannot control, and a domestic pricing response it needs to contain before it becomes self-reinforcing.

The cash rate is the interest rate on overnight loans between commercial banks. The RBA sets this rate, and it serves as the anchor for borrowing costs across the economy. When it moves, the effects cascade outward in a sequence that typically takes weeks for the first step and months for the full impact:

The cumulative effect of three hikes in 2026 represents a significant reversal. Most of the rate cuts delivered during 2025 have now been unwound, meaning variable-rate borrowers are paying repayments close to where they sat at the prior cycle peak.

Market rates reflect this tightening. The 10-year Australian government bond yield sat at approximately 4.94-4.97% on 5-6 May 2026, while the 3-year yield was approximately 4.58-4.64%. Both are well above the cash rate, indicating that bond markets are pricing in the possibility of further tightening or a prolonged hold at elevated levels.

Understanding this transmission chain helps readers interpret future RBA signals accurately, rather than waiting for a decision announcement to adjust financial planning.

The Board’s next moves depend on a handful of specific data releases and events. Rather than speculating on the direction, readers can track the same inputs the Board will be watching.

The late May monthly CPI release is the single most important near-term data point. A trimmed mean reading moving toward 3% would strengthen the case for a pause at the next meeting. An upward surprise could bring forward the timing of a fourth hike.

Two labour market reports follow. The 21 May and 25 June releases will show whether unemployment, currently at 4.3% as of March 2026, is holding firm or softening. Persistent strength at or below 4.3% reinforces the tightening case; any material rise could shift the Board’s calculus toward patience.

The Federal Budget on 12 May is the wildcard. A stimulatory fiscal stance would complicate the RBA’s task, effectively adding demand while the Board is trying to cool it. A fiscally conservative budget may give the Board grounds to pause at the June or July meeting.

The federal budget fiscal conflict introduces a genuine policy tension: personal income tax cuts, energy rebates, and a potential fuel excise reduction each add demand at the margin, directly counteracting the RBA’s effort to cool spending through higher borrowing costs.

| Date | Event | What it means for rates |

|---|---|---|

| 12 May 2026 | Federal Budget | Stimulatory measures raise hike odds; restraint supports a pause |

| Late May 2026 | Monthly CPI release | Trimmed mean near 3% supports pause; higher reading accelerates fourth hike |

| 21 May 2026 | Labour force data | Unemployment at or below 4.3% reinforces tightening case |

| 25 June 2026 | Labour force data | Continued strength or softening shapes the Board’s June/July deliberation |

| Sep/Oct 2026 | Next most probable hike window | Market pricing implies one further 25bp move in this timeframe |

Futures markets, as measured by the ASX Rate Tracker on 5 May 2026, imply a terminal cash rate of approximately 4.68% by December 2026, consistent with one further 25 basis point hike from the current 4.35%.

The immediate market reaction to the decision was muted. The ASX 200 closed at 8,680.50 on 5 May, down just 0.19%. A high probability of the hike had already been priced in. The structural repricing across asset classes, however, is ongoing.

The sector-level logic differs materially. Banks benefit from wider net interest margins as the spread between deposit rates and lending rates expands, but they face rising credit quality risk as cumulative hikes pressure heavily indebted borrowers. Real estate investment trusts face the most direct headwinds: higher discount rates reduce the present value of future rental income, and REIT income yields become less competitive against risk-free government bond yields approaching 5%. Resources and energy stocks carry relative shelter because the same geopolitical factors driving inflation also support commodity prices.

For investors concerned about persistent price rises through late 2027, inflation-linked bonds offer a direct hedge. ETFs such as ILB on the ASX provide exposure to bonds whose returns adjust with inflation.

| Asset class | Rate environment impact | Relevant ASX ETF examples |

|---|---|---|

| Banks | Wider margins offset by credit risk from stretched borrowers | MVB |

| REITs / Property | Most direct headwind from higher discount rates and competing yields | VAP |

| Resources / Energy | Relative shelter; commodity prices supported by same geopolitical factors | QRE, OZR |

| Inflation-linked bonds | Direct hedge against persistent inflation through late 2027 | ILB |

| Gold | Traditional store of value during prolonged inflationary periods | QAU, GHLD |

GDP growth in the December 2025 quarter exceeded the RBA’s estimate of potential growth, supporting the view that the economy is not yet in distress. The AUD/USD was trading around 0.726 as of 6 May 2026, reflecting relative stability rather than stress.

Investors wanting to act on the asset class analysis above will find our full explainer on ASX inflation investment strategy covers six specific ETFs, including ILB, AAA, and ISEC, with portfolio tilts mapped to three different investor goals: capital preservation, income generation, and inflation-adjusted growth through a prolonged tightening environment.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.

A rate cut in 2026 is considered unlikely under current conditions. A pause, however, is achievable if the incoming data moves in the right direction.

Three conditions could enable the Board to hold at its next meeting rather than deliver a fourth hike:

Of these, the external factor carries the most leverage. A material decline in energy costs would lower headline CPI quickly and give the Board room to pause sooner than the September or October window currently priced by markets.

The RBA’s own signalling suggests one additional hike remains the central expectation embedded in its revised projections, with the Board indicating it will remain data-dependent rather than pre-committed to a fixed path. Governor Bullock’s description of policy as “a bit restrictive” reinforces this: the Board is aware it is applying pressure and is watching for the point at which tightening has done enough.

The Board meeting minutes, expected around 19 May 2026, will be the next source of detailed forward guidance before the late May CPI release. Readers tracking the rate path should watch for the language around inflation risk and the Board’s assessment of fiscal policy interactions.

The path to relief exists, but it is narrow and conditional. The dates and data points outlined above are the same inputs the Board will use to make its next call. Knowing them makes the RBA’s direction legible rather than opaque.

The RBA cash rate is the interest rate on overnight loans between commercial banks, and it anchors borrowing costs across the economy. When the RBA raises the cash rate, banks reprice variable-rate loans, which directly increases mortgage repayments for borrowers on variable rates.

The RBA raised the cash rate by 25 basis points to 4.35% on 5 May 2026 because headline CPI inflation reached 4.6% and trimmed mean inflation was 3.3%, both above the 2-3% target band, with global energy pressures from Middle East conflict compounding domestic price rises.

The most critical near-term releases are the late May monthly CPI print, labour force data on 21 May and 25 June, and the Federal Budget on 12 May; a trimmed mean CPI moving toward 3% or rising unemployment above 4.3% would strengthen the case for a pause rather than a fourth hike.

Futures markets, as measured by the ASX Rate Tracker on 5 May 2026, implied a terminal cash rate of approximately 4.68% by December 2026, consistent with one further 25 basis point hike from the current 4.35% level.

Banks can benefit from wider net interest margins but face rising credit risk from indebted borrowers, while REITs face the most direct headwinds because higher discount rates reduce the present value of future rental income and their yields become less competitive against government bonds approaching 5%.