Why Most Wealth-Building Strategies Aren’t Built for You

6 hrs ago

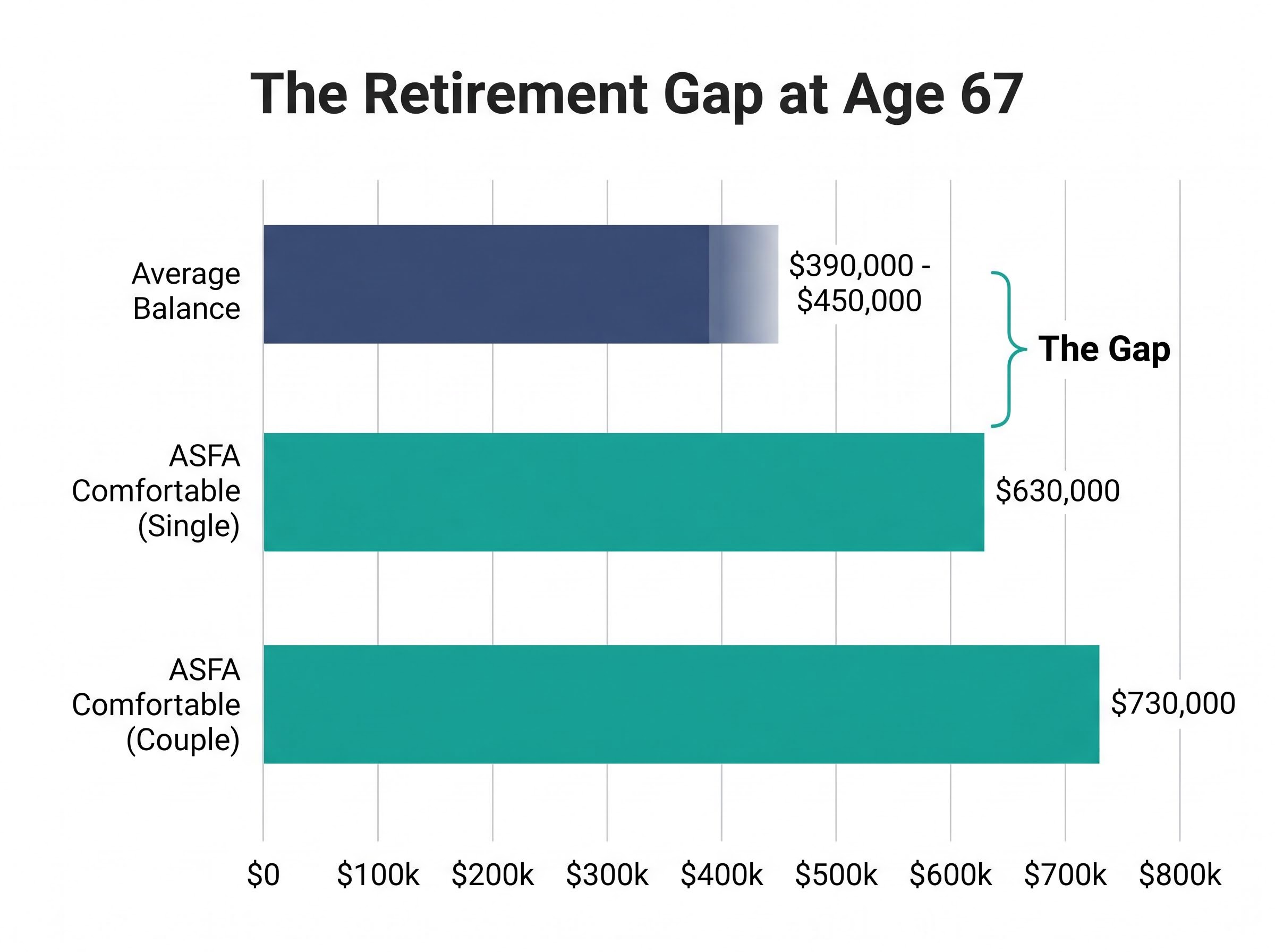

The average Australian in their early fifties has roughly $200,000 in superannuation. The Association of Superannuation Funds of Australia (ASFA) says a single person needs $630,000 by age 67 for a comfortable retirement. That is not a savings failure. It is a mathematics failure most Australians have never been taught to see.

This article is not about earning more money. It is about understanding why $500 a month, sustained over time, produces an outcome that feels arithmetically impossible until the numbers are laid out decade by decade. Anchored to the Australian context, using balanced super fund returns, ASX benchmarks, and a realistic 8% blended annual return, the sections that follow explain exactly how compound interest works in Australia, why the final ten years of an investment horizon matter more than the first twenty, and what the two main vehicles available to Australian investors offer in terms of tax efficiency and access.

The gap between where Australians stand and where they need to be is not abstract. It is specific, and it widens with every year of inaction.

| Age Group | Average Super Balance | Gap to ASFA Comfortable Target ($630,000) |

|---|---|---|

| 30-34 | ~$51,138 | ~$578,862 |

| 45-54 | ~$196,223 | ~$433,777 |

| At retirement (67) | ~$390,000-$450,000 | ~$180,000-$240,000 |

According to Rest Super data published in March 2026, the average super balance for men aged 30-34 is $55,690; for women, $46,586. By ages 45-54, the combined average reaches approximately $196,223. Even at retirement age, data from Motley Fool and the Australian Retirement Trust suggests most Australians arrive at 67 with between $390,000 and $450,000, well short of the ASFA comfortable retirement benchmark of $630,000 for a single person or $730,000 for a couple.

The ASFA Retirement Standard benchmarks are updated quarterly and represent the most widely cited official reference for retirement adequacy in Australia, with the February 2026 release confirming the comfortable retirement lump sum targets of $630,000 for singles and $730,000 for couples that underpin national superannuation planning guidance.

The Australian Retirement Trust stated in May 2025 that “many people’s super balances are falling behind what they should be.”

The instinct is to blame low incomes. But for a significant portion of working Australians, the issue is not what they earn. It is that they do not intuitively understand how growth compounds over time, which makes the shortfall feel permanent when it is not. The gap between financially stressed and financially comfortable retirees often traces back to consistent monthly habits rather than six-figure salaries.

The shortfall is not evenly distributed across life stages: super balance benchmarks by age reveal that the gap between actual balances and the ASFA target widens sharply in the decade between 45 and 55, precisely when many Australians assume they still have time to catch up.

The first few years of consistent investing feel flat. A $500 monthly contribution into a balanced fund does not produce dramatic results in year one or year three. The balance grows, but it grows at the pace of the contributions themselves, and the returns on those contributions are modest because there is simply not enough accumulated capital for compounding to accelerate.

This is where most people disengage. The impression is that investing is not working. In reality, the mechanism underneath is building momentum that will not become visible for a decade or more.

Compounding means returns are earned not only on the original contributions but on all previously accumulated returns. Each cycle of growth enlarges the base on which the next cycle operates. The effect is self-reinforcing: small in the early years, and then progressively larger as the capital base expands.

The 8% annual return benchmark used here reflects the AustralianSuper Balanced option’s ten-year return of 8.17% per annum (to March 2026, per SuperRatings), which aligns with historical balanced super fund averages.

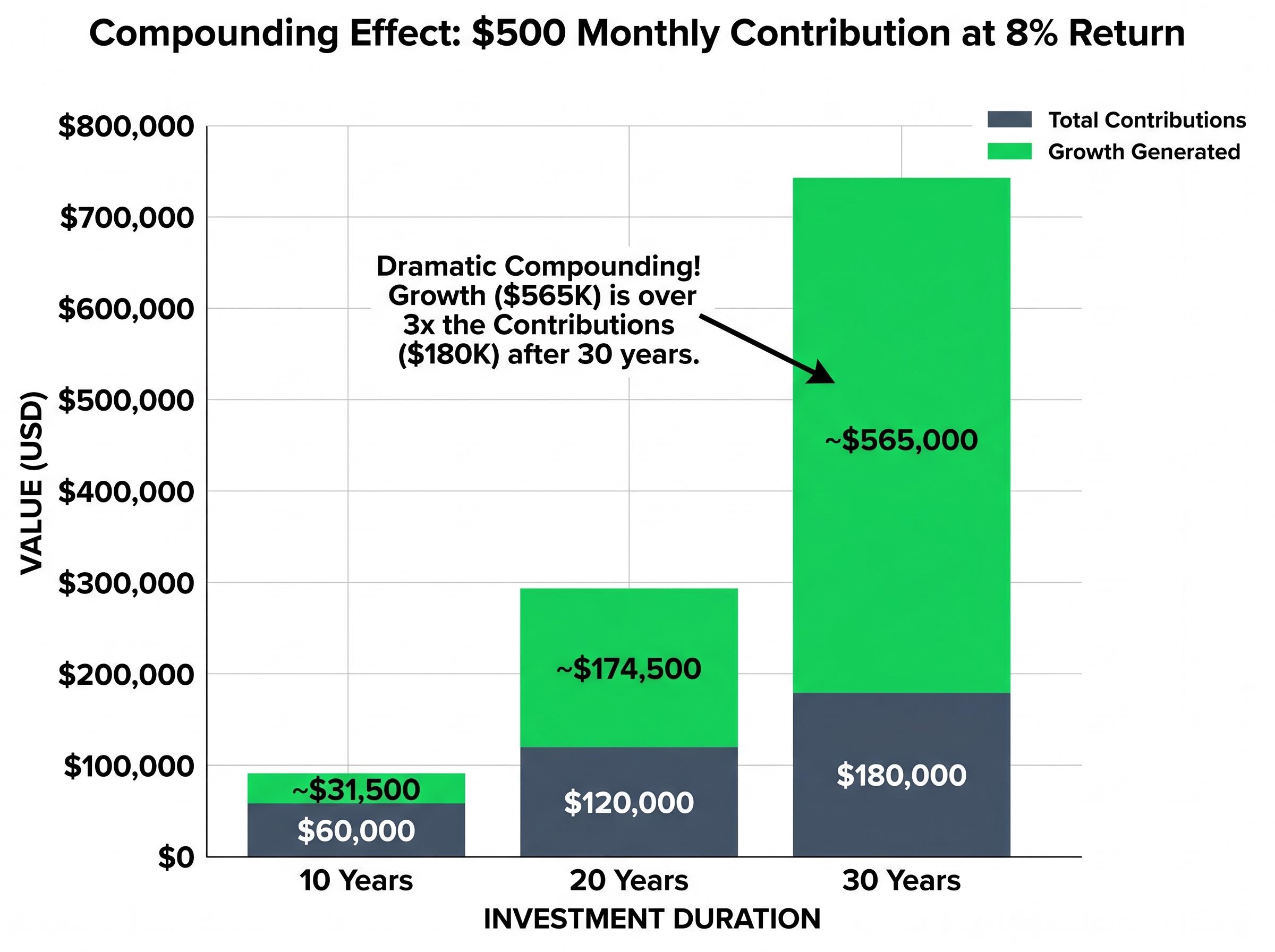

| Time Horizon | Total Contributions | Projected Balance at 8% | Growth Generated |

|---|---|---|---|

| 10 years | $60,000 | ~$91,500 | ~$31,500 |

| 20 years | $120,000 | ~$294,500 | ~$174,500 |

| 30 years | $180,000 | ~$745,000 | ~$565,000 |

$180,000 in personal contributions, compounded at 8% over 30 years, grows to approximately $745,000. More than $565,000 of that balance is generated by the compounding itself, not by the investor’s contributions.

The contrast between years 20 and 30 is where the mechanism becomes undeniable. In the first 20 years, growth generated approximately $174,500. In the final 10 years alone, growth added roughly $390,500, more than double what the preceding two decades produced, with identical monthly contributions throughout. No extra effort. No increased risk. The only variable was time.

This is also why early withdrawal destroys disproportionately more wealth than the amount withdrawn. Every dollar pulled out in year 15 loses all the compounding it would have produced during the high-acceleration final decade. At the ASX long-term historical average of approximately 10%, the same contributions exceed $1.1 million over 30 years.

The cost of delay is not a vague motivational concept. It is a specific number, and it grows larger with every decade postponed.

| Start Age | Investment Horizon (to age 65) | Total Contributed | Projected Balance at 8% |

|---|---|---|---|

| 25 | 40 years | $240,000 | ~$1,745,000 |

| 35 | 30 years | $180,000 | ~$745,000 |

| 45 | 20 years | $120,000 | ~$294,500 |

| 55 | 10 years | $60,000 | ~$91,500 |

A 25-year-old contributing $500 per month at 8% reaches approximately $1,745,000 by age 65. The same contribution starting at age 35 reaches approximately $745,000, still exceeding the ASFA comfortable retirement target of $630,000 for a single person at age 67. Waiting until 45 reduces the projected balance to approximately $294,500, and starting at 55 yields roughly $91,500.

Each ten-year delay costs more than the one before it, because the lost decade is always the one closest to the high-acceleration zone of the curve.

That said, the 20-year projection still represents $174,500 in growth on $120,000 contributed. For someone starting in their mid-forties, this is a real and meaningful outcome, not a reason to give up but a reason to start immediately. Two relevant bookends frame the Australian compounding timeline: preservation age at 60 (when super becomes accessible) and Age Pension eligibility at 67 (per ATO and Australian Retirement Trust guidelines). The distance between those two dates offers additional compounding runway even after a late start.

Understanding compounding is the first step. Choosing where to apply it is the second, and in Australia, the decision sits between two primary vehicles: salary sacrifice into superannuation and investment in ASX-tracking exchange-traded funds (ETFs). Neither is universally superior. The right answer depends on age, income, and how soon the money needs to be accessible.

Salary sacrifice into superannuation is the most tax-efficient option for most working Australians. Contributions made through salary sacrifice are taxed at 15% rather than the individual’s marginal income tax rate. For someone earning $80,000 per year, salary sacrificing $500 per month means those contributions attract 15% tax instead of the 32.5% marginal rate applicable to that income bracket, a meaningful difference compounded over decades.

The concessional contribution cap is $30,000 per year (ATO, 2025/26). The Superannuation Guarantee (SG) rate stands at 11.5% in 2025/26, rising to 12% from July 2026. Funds remain locked until preservation age, which is fixed at 60 for all individuals born on or after 1 July 1964.

ASX-tracking ETFs offer the alternative for capital that needs to remain accessible before age 60. Management fees on broad index funds often sit below 0.2% per year. The trade-off is tax efficiency: dividends and capital gains are taxed at the investor’s marginal income tax rate, not the concessional super rate.

| Feature | Salary Sacrifice (Super) | ASX ETF | Hybrid Approach |

|---|---|---|---|

| Tax on contributions | 15% | Marginal rate (post-tax income) | Split across both |

| Tax on earnings/growth | 15% within fund | Marginal rate on dividends and CGT | Lower blended rate |

| Access before age 60 | No (preservation rules) | Yes (full liquidity) | Partial (ETF portion accessible) |

| Suitable for | Long-term retirement savings | Pre-retirement goals, flexibility | Most working-age Australians |

For most working-age Australians, the practical recommendation is a hybrid: use salary sacrifice for the long-term compounding advantages within super’s low-tax environment, and supplement with ETFs for pre-retirement flexibility. The split between the two depends on individual circumstances, specifically age, income level, and how many years remain before preservation age.

Structuring $500 a month across both vehicles requires calculating available salary sacrifice room net of existing employer Superannuation Guarantee contributions, then directing the remainder into a low-cost ASX index ETF for liquidity needs that cannot wait until preservation age.

The biggest threat to a 30-year compounding strategy is not a market crash. It is treating the monthly contribution as a decision rather than an automated commitment. When $500 per month remains discretionary, it competes with every other spending impulse, and spending impulses win more often than most people admit.

The daily-spend reframe makes the figure feel achievable. A daily outlay of approximately $16.50 is equivalent to a monthly contribution of $500, comparable to a single food delivery order or a couple of takeaway coffees and a snack each day.

A daily spend of $16.50 is equivalent to $500 per month, which at 8% over 30 years grows to approximately $745,000.

Contribution abandonment most commonly occurs between years four and seven of an investment journey. This is precisely the period when the compounding curve is still flat and the emotional return on patience feels lowest. Pulling out at year five forfeits the high-acceleration final decade where the vast majority of wealth is generated.

Market drawdowns of 20-30% are normal within long-horizon investment journeys. The balance decline is temporary, but the compounding loss from pausing contributions or withdrawing capital is permanent. Investors who continued contributing through downturns historically purchased more units at lower prices, accelerating the recovery and amplifying long-term returns.

Three behavioural interventions protect compounding from its most common saboteur:

The retirement savings shortfall facing most Australians is a mathematical education gap, not an income gap. A single $500 monthly contribution, sustained over 30 years at 8%, produces a balance of approximately $745,000, exceeding the ASFA comfortable retirement target of $630,000 for a single person.

Superannuation alone, at the current 11.5% SG rate, will not close this gap for most workers. Voluntary contributions through salary sacrifice or ETFs remain the practical lever available to working-age Australians who want to reach the comfortable retirement benchmark rather than fall short of it.

For Australians who have career gaps, variable income years, or a Total Super Balance below $500,000, our comprehensive walkthrough of carry-forward super strategies covers exactly how to access up to five years of unused concessional cap space in a single financial year, including the hard 30 June 2026 deadline for FY2020-21 cap amounts that expire permanently.

The action is straightforward: pick a start date within the next seven days, automate the first $500 contribution, and let the compounding mechanism do the work that no amount of market timing or stock selection can replicate.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Compound interest means returns are earned not only on your original contributions but also on all previously accumulated returns, creating a self-reinforcing growth effect. In an Australian context, this applies to both superannuation and ASX-tracking ETFs, where an 8% annual return on $500 monthly contributions can grow to approximately $745,000 over 30 years.

The Association of Superannuation Funds of Australia (ASFA) sets the comfortable retirement target at $630,000 for a single person and $730,000 for a couple, as confirmed in the February 2026 ASFA Retirement Standard update. Most Australians currently retire with between $390,000 and $450,000, falling short of this benchmark.

Salary sacrifice contributions are taxed at 15% rather than your marginal income tax rate, making super the more tax-efficient option for long-term retirement savings, while ASX ETFs offer full liquidity and flexibility before age 60. A hybrid approach using both vehicles suits most working-age Australians depending on their age, income, and access needs.

Starting at 35 instead of 25 reduces the projected balance at age 65 from approximately $1,745,000 to approximately $745,000 at an 8% annual return, with $60,000 less contributed in total. Each decade of delay costs more than the previous one because the lost years are always closest to the high-acceleration phase of the compounding curve.

The three most effective interventions are automating contributions immediately after each pay cycle, reframing market dips as discounted unit purchases rather than losses, and reviewing your portfolio annually rather than weekly. Contribution abandonment most commonly occurs between years four and seven, precisely when the compounding curve is still flat but before the high-growth final decade begins.