What Social Media Stock Promotions Actually Do to Prices

2 hrs ago

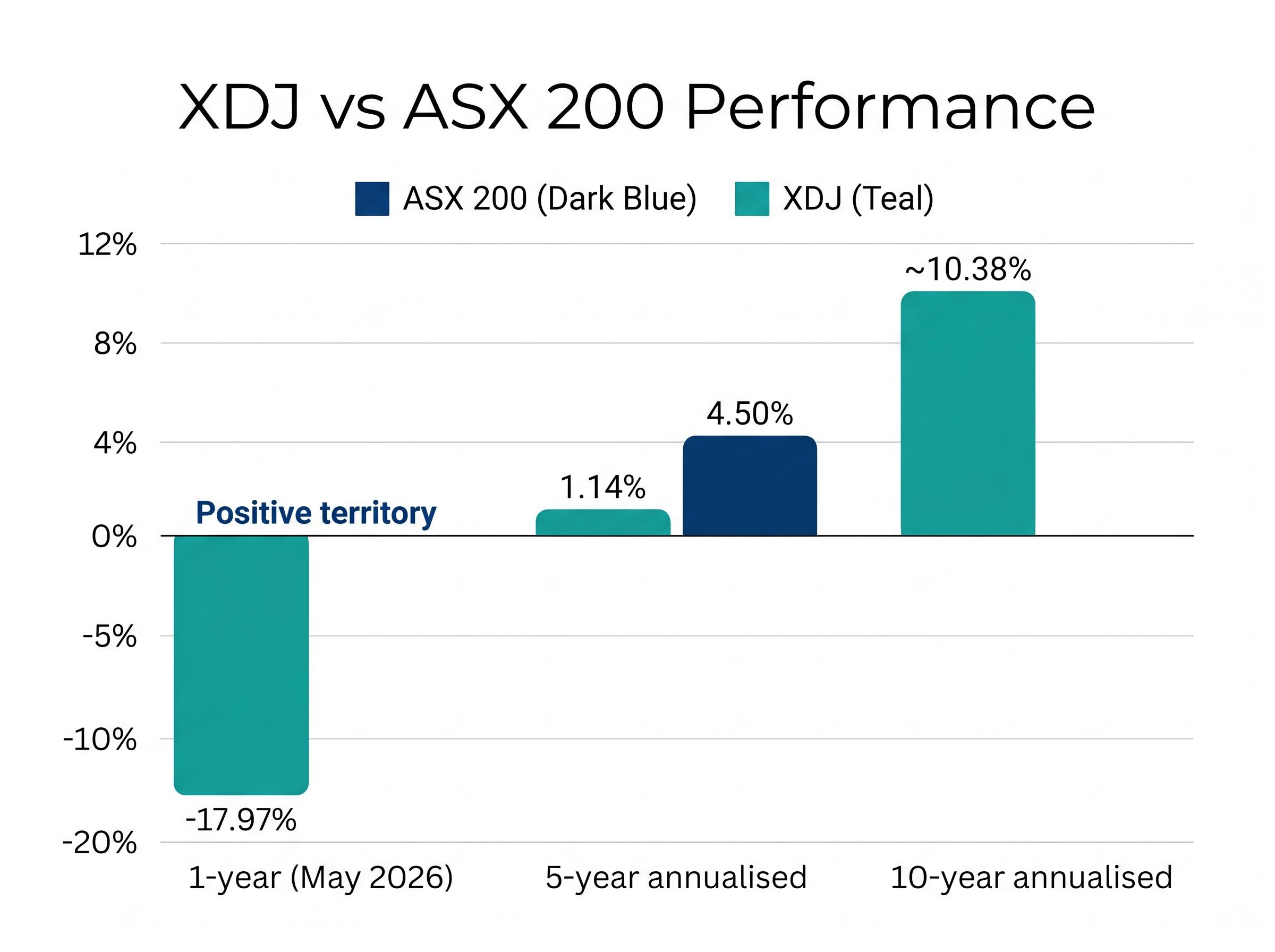

The ASX Consumer Discretionary Index has returned just 1.14% per year over the past five years, while the broader ASX 200 delivered 4.50% annually over the same period. For investors drawn to familiar household-name retailers, that gap deserves an explanation.

Australian retail investors frequently gravitate toward recognisable consumer brands on the ASX, assuming that a business they shop at is a business worth owning. The appeal is intuitive. But the sector’s structural relationship with interest rates, cost-of-living conditions, and dividend variability creates risks that are easy to underestimate when the brand feels familiar. This article explains what consumer discretionary stocks actually are, why they have structurally underperformed the broader ASX in recent years, and what practical factors Australian investors should assess before buying into the sector.

Consumer discretionary stocks are companies that sell non-essential goods and services. Retailers, entertainment businesses, restaurants, and leisure operators all fall into this category. The distinction from consumer staples, which sell essentials such as groceries and household products, is straightforward: if a household can delay or skip the purchase without immediate consequence, the company selling it is discretionary.

ASX consumer staples such as Coles and Woolworths recorded a maximum drawdown of approximately -9% in 2025 compared to approximately -15% for the broader ASX 200, a gap that illustrates why institutional investors treat the two consumer sectors as structurally different portfolio tools rather than interchangeable income sources.

That distinction carries a structural implication. Because these businesses depend on what consumers choose to do with extra income, their revenues expand and contract with the economic cycle. This is not a quirk of individual management teams or product quality. It is built into the business model.

The S&P/ASX 200 Consumer Discretionary Index (XDJ) includes 23 companies, with major constituents including Wesfarmers (WES), Aristocrat Leisure (ALL), JB Hi-Fi (JBH), Harvey Norman (HVN), Super Retail Group (SUL), and Domino’s Pizza (DMP). Notably, Wesfarmers straddles both discretionary (Kmart, Target, Officeworks) and home improvement (Bunnings), illustrating that sector classification is not always clean-cut.

Five structural forces govern the sector’s ups and downs:

Understanding what separates a discretionary business from a defensive one is the foundational insight that explains everything else in this article.

The headline figures are stark.

The XDJ returned 1.14% annualised over five years, compared with 4.50% annualised for the ASX 200 over the same period.

That gap translates into meaningful compounding differences for investors who held discretionary-heavy portfolios. The more recent picture is sharper still: the XDJ’s one-year return sat at -17.97% as of 11 May 2026, with the index trading within a 52-week range of 3,294-4,621.

Individual stocks reflect the pressure. JB Hi-Fi’s share price declined 25.7% from the start of 2025 to 12 May 2026, a company-level illustration of what sector-wide weakness looks like in a portfolio.

ASX sector rotation in May 2026 revealed the two-speed nature of the current market: while consumer discretionary fell 16% year to date and healthcare fell 27% as the rate cycle intensified, materials, energy, financials, and utilities were simultaneously recording new highs, a pattern that underscores how cyclical pressure concentrates in specific sectors rather than distributing evenly across the index.

| Timeframe | XDJ Return | ASX 200 Return |

|---|---|---|

| 1-year (as of May 2026) | -17.97% | Positive territory |

| 5-year annualised | 1.14% | 4.50% |

| 10-year annualised | ~10.38% | — |

The 10-year annualised figure of approximately 10.38% provides a longer-term frame of reference. The sector is not structurally broken. But recent years have tested investors who entered without accounting for the cycle.

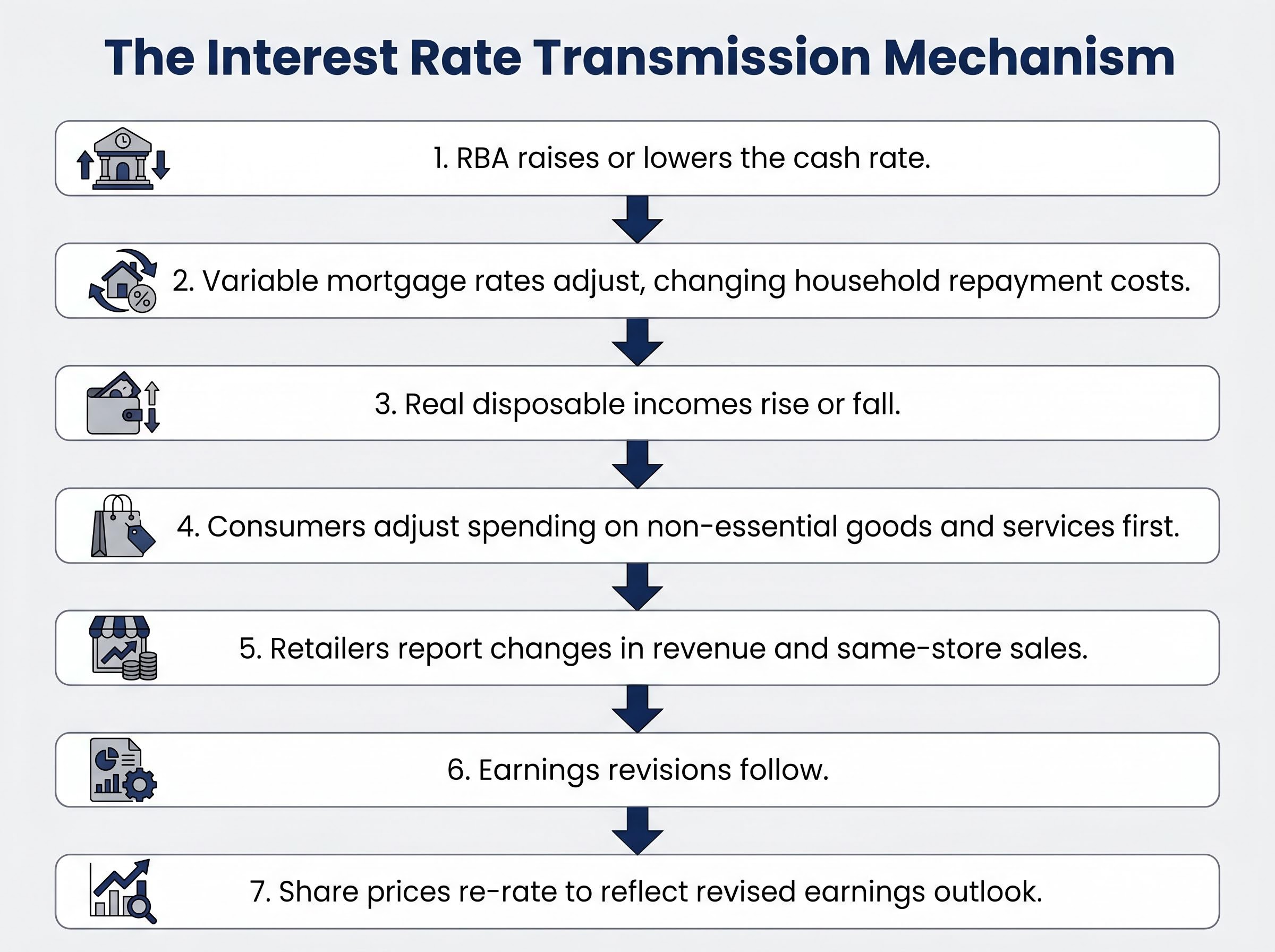

The transmission mechanism is direct. Higher RBA rates increase mortgage repayments, reduce real disposable incomes, and the first spending category households cut is non-essential goods and services. That reduction flows straight into retailer revenues and, from there, into earnings.

Bell Potter attributed the XDJ’s 4.28% monthly decline between 31 October and 24 November 2025 to “interest rate concerns,” a period in which the consumer staples index rose 0.09%. The divergence between the two indices captured a defensive rotation in real time.

The sector retains upside sensitivity to rate expectations as well. In April 2026, the XDJ recorded a brief gain of +0.32% ahead of an RBA decision, a reminder that the same mechanism works in both directions.

The path from an RBA decision to a retailer’s profit margin follows a traceable chain. Understanding each link allows investors to read rate decisions as forward signals for the sector, rather than reacting after the share price has already moved.

RBA analysis of household consumption and income since the pandemic documents how variable mortgage rates transmit directly into real disposable incomes, with non-essential spending adjusting faster and more sharply than essential categories when repayment burdens rise.

What makes this mechanism particularly relevant for discretionary stocks is that markets price forward-looking changes, not just actual rate movements. Rate expectations alone can move the sector.

The evidence appeared clearly in November 2025.

The Westpac/Melbourne Institute Consumer Sentiment Index surged 12.8% to 103.8, the first reading above 100 since May 2022 and a seven-year high excluding COVID-era readings.

Westpac economist Matthew Hassan linked the improvement directly to rate cut expectations. Bell Potter cited improving non-food spending and identified Harvey Norman (HVN) and Universal Store (UNVL) as seasonal recovery picks for the Christmas 2025 period. The sentiment shift was not a response to an actual rate cut. It was a response to the expectation of one, and it was already influencing analyst positioning.

Many larger ASX consumer discretionary companies have established dividend-paying histories. For income-oriented investors, headline yield figures from familiar retailers carry intuitive appeal.

That appeal is real, but it comes with a structural caveat. Discretionary dividends are tied to the same earnings cycle that pressures share prices. When household spending contracts, retailer revenues fall, earnings compress, and dividends are often reduced or cut. This makes yield figures less reliable as forward indicators than yields from sectors with more stable cash flows.

Consider the contrast:

JB Hi-Fi illustrates how dividend dynamics play out at the company level. The stock’s current dividend yield sits at approximately 4.8% as of May 2026, compared with a five-year average yield of approximately 5.2%. The decline reflects both share price movements and earnings variability.

JB Hi-Fi achieved average annual revenue growth of 2.5% over three years despite the high-rate environment, demonstrating that individual companies within the sector can show resilience even when the index struggles. Its price-to-sales ratio of 0.82x sits above its five-year average of 0.70x, which investors should factor into income expectations alongside the yield figure.

Share valuation methods including price-to-sales, DCF, and EV/EBITDA each produce different intrinsic value estimates for the same stock, and the gap between them often reveals whether a retailer’s apparent cheapness reflects genuine value or cyclically depressed earnings that will compress margins further as the rate cycle plays out.

No single metric, including yield or price-to-sales, is sufficient for an investment decision. The case study illustrates why investors building income assumptions around discretionary stocks need to assess the full earnings cycle, not just one year’s payout.

The 1.14% versus 4.50% five-year return gap quantifies the cost of entering this sector without a framework. Three factors, approached as sequential questions, provide a practical starting point for retail investors evaluating discretionary opportunities.

Assessing the RBA’s published forward guidance alongside economist commentary provides a timing frame that is more relevant for discretionary stocks than for most other ASX sectors, because the sector’s earnings are unusually sensitive to changes in the household cash flow that rate decisions directly control.

These three factors translate the sector’s structural characteristics into a pre-investment filter that does not require professional-grade analytical tools, but does require discipline.

The past five years have been unkind to discretionary investors. The 1.14% annualised return against the ASX 200’s 4.50% is difficult to ignore. But the ten-year picture tells a different story.

The XDJ’s 10-year annualised return of approximately 10.38% indicates a sector that rewards patient, cycle-aware investors over longer holding periods.

Consumer discretionary is not a structurally weak sector. It is a cyclical one. The difference matters. The XDJ sits near the lower end of its 52-week range of 3,294-4,621 as of May 2026, and the Westpac/Melbourne Institute Consumer Sentiment Index reading of 103.8 in November 2025 was the kind of turning-point signal analysts monitor before the next phase of the cycle begins.

The central argument remains straightforward: familiarity with a brand is a useful starting point for research, but the sector’s cyclical nature means investors need to layer in rate awareness, dividend scrutiny, and valuation discipline before committing capital. Those who do may find that the same forces that produced five years of underperformance are the forces that create the next opportunity. Those who do not risk repeating the gap.

For investors wanting to translate cycle awareness into portfolio action, our dedicated guide to positioning for RBA rate cuts examines which ASX sectors have historically moved first and fastest when the RBA eases, including how the deposit-to-equity rotation creates a structural demand bid for dividend-paying stocks that directly benefits discretionary names in the early recovery phase.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.

Consumer discretionary stocks are companies that sell non-essential goods and services, such as retailers, restaurants, entertainment businesses, and leisure operators. The S&P/ASX 200 Consumer Discretionary Index (XDJ) includes 23 companies, with major constituents such as Wesfarmers, JB Hi-Fi, Harvey Norman, and Aristocrat Leisure.

The sector returned just 1.14% annualised over five years compared to 4.50% for the ASX 200, largely because higher RBA interest rates increased mortgage repayments, reduced household disposable incomes, and caused consumers to cut non-essential spending first, which flowed directly into lower retailer revenues and earnings.

When the RBA raises rates, variable mortgage repayments increase, real disposable incomes fall, and consumers reduce spending on non-essential goods first, compressing retailer revenues and earnings before share prices re-rate downward. Rate expectations alone can move the sector, as shown when the XDJ gained 0.32% ahead of the April 2026 RBA decision.

Discretionary dividends are tied to the same earnings cycle that pressures share prices, meaning payouts can be reduced or cut when household spending contracts and retailer revenues fall. For example, JB Hi-Fi's dividend yield sat at approximately 4.8% in May 2026, below its five-year average of approximately 5.2%, reflecting earnings variability over the rate cycle.

Investors should assess where interest rates are in the cycle and where they are heading, whether the company maintained or grew its dividend through previous downturns, and whether their familiarity with the brand extends to the balance sheet, competitive position, and earnings outlook rather than just the shopfront experience.