Hormuz Prices Have Normalised. Geopolitical Inflation Risk Has Not.

49 mins ago

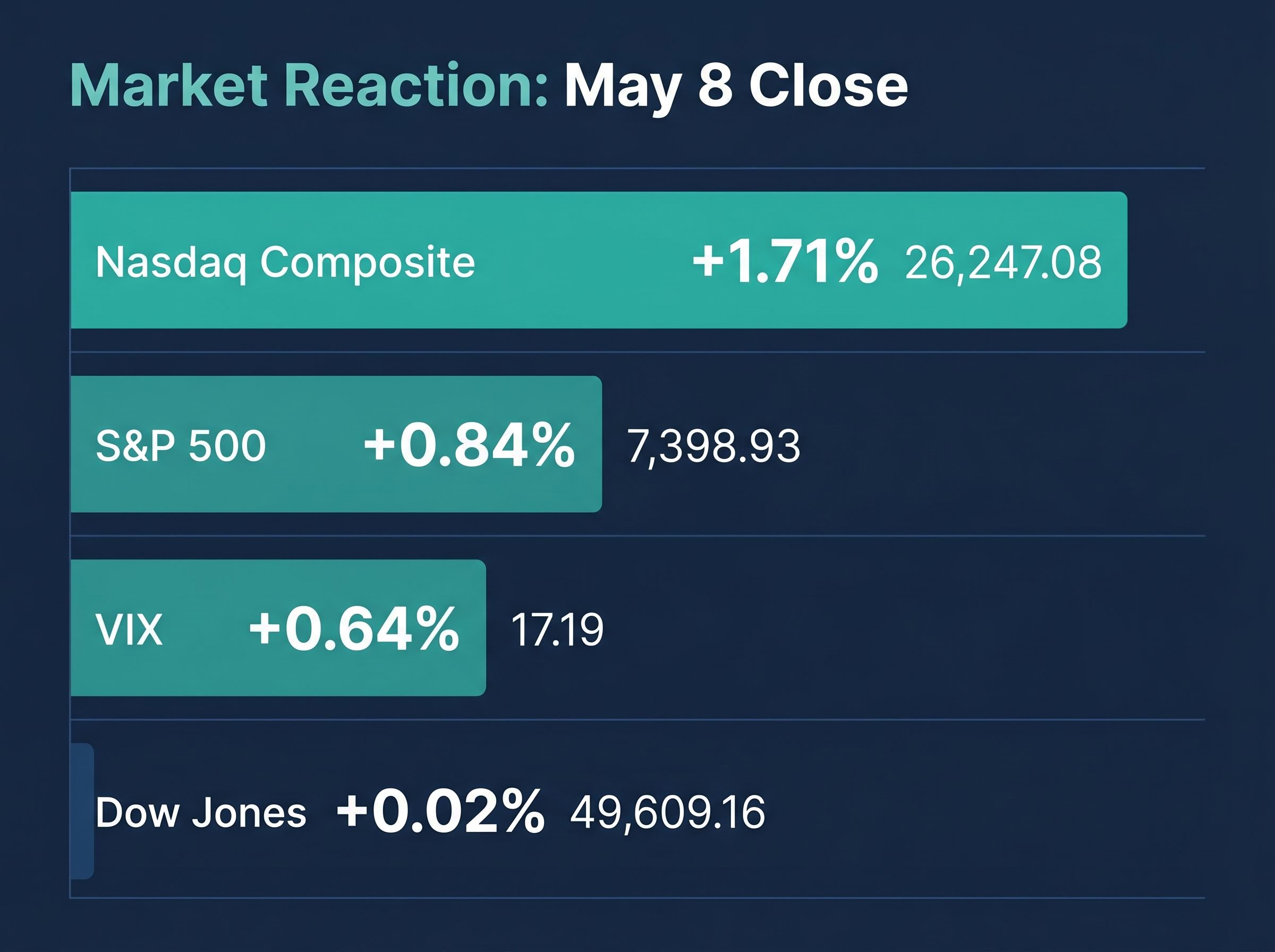

Two federal courts have now struck down the legal pillars of the Trump administration’s sweeping tariff programme within three months of each other. The Supreme Court invalidated tariffs imposed under the International Emergency Economic Powers Act (IEEPA) on 20 February 2026. The Court of International Trade (CIT) followed on 8 May 2026, striking down Section 122-based duties. Together, these rulings dismantle the two broadest statutory authorities the executive branch had used to impose US tariff policy unilaterally, yet the S&P 500 closed above 7,398 on the day of the second ruling, and the VIX barely moved.

The gap between the legal significance and the market’s response is the story worth unpacking. What follows is an analysis of the legal double-blow to executive tariff authority, why equity markets responded with restraint rather than a relief rally, and what the rulings mean for investors watching trade risk in the months ahead.

The two rulings did not chip away at tariff authority. They removed its load-bearing walls.

Legal analysis from Skadden Arps, published 26 February 2026, characterised the IEEPA ruling as a foundational shift:

“The Supreme Court’s application of the major questions doctrine to IEEPA amounts to a constitutional reset of executive trade authority.”

K&L Gates warned in a 9 May 2026 assessment that Section 301, the remaining statutory tool the administration has used for targeted tariffs, now faces heightened litigation risk given the pattern of judicial pushback. WilmerHale trade analyst Simon Lester described the combined rulings as a “one-two punch” that leaves the executive with significantly narrowed unilateral options.

Section 301 tariff exposure has already produced concrete winners and losers at the sectoral level, with domestic battery materials producers such as Novonix absorbing demand previously captured by Chinese suppliers now facing combined duties exceeding 160%, a preview of the kind of industrial reshaping that accelerates when tariff authority shifts from executive orders to legislatively-grounded, longer-cycle instruments.

Lawfare’s major questions doctrine analysis of the Learning Resources ruling argues that the Court’s logic extends beyond IEEPA, placing Section 232 and other statutes conferring broad executive trade discretion on uncertain constitutional footing if challenged in litigation.

The muted reaction was not indifference. It was prior pricing.

Through 2025, the S&P 500 experienced a 5-7% drawdown at peak tariff escalation, functioning as the market’s real-time absorption of trade policy risk. By the time the CIT ruled on 8 May, the volatility premium had already been extracted.

| Index | May 8 Close | Daily Change |

|---|---|---|

| S&P 500 | 7,398.93 | +0.84% |

| Dow Jones | 49,609.16 | +0.02% |

| Nasdaq Composite | 26,247.08 | +1.71% |

| VIX | 17.19 | +0.64% |

The divergence between the Nasdaq’s 1.71% gain and the Dow’s near-flat close is telling. Technology-heavy names, which carry less direct tariff exposure on physical goods, rallied. Industrial and manufacturing-heavy Dow components, still processing supply chain restructuring costs, did not.

Goldman Sachs, in a 9 May note, characterised the rulings as ending the “tariff bluff era,” arguing that the policy uncertainty premium embedded in valuations had been the larger drag, and its removal was already underway before the gavel fell.

Goldman Sachs described the rulings as ending the “tariff bluff era,” reducing the policy uncertainty premium that had weighed on equity valuations throughout 2025.

Investors who interpret the restrained move as complacency may be misreading the signal. The market had already done this work.

The resilience of global recession buffers matters directly to how investors should read the muted equity response: BCA Research’s seven-factor framework identifies IT investment at a record 4.9% of GDP in Q1 2026 as the most durable cushion, suggesting that the tariff uncertainty premium was being absorbed against a backdrop of genuine structural strength rather than complacency.

With IEEPA and Section 122 off the table, three pathways remain for the administration to pursue tariff policy:

USTR Jamieson Greer signalled in a 9 May interview that the administration is exploring “national security relabeling” of existing duties to bring them under Section 232 authority, a workaround that legal experts expect to face its own litigation.

The White House responded to the CIT ruling directly: “Courts can’t stop America First, Congress will act.”

That statement reflects a genuine shift in mechanism. Any legislative grant of tariff authority requires passage through both chambers of Congress, introducing a longer and less predictable timeline than executive orders.

The White House has reportedly pushed for explicit statutory authority, with some reporting referencing a “Trade Security Act,” though no confirmed bill text or hearing schedule has been verified as of 9 May 2026. Congressional dynamics introduce partisan negotiation variables entirely absent from the executive order model investors had been pricing around.

While the legal drama plays out domestically, the more durable market story is the structural trade rerouting that has accelerated regardless of courtroom outcomes.

| Trading Partner | Immediate Reaction | Longer-Term Repositioning |

|---|---|---|

| European Union | Welcomed ruling; suspended approximately €4 billion in retaliatory tariffs | Firms including Volkswagen exploring refund claims on previously paid duties |

| China | No new countermeasures; state media framed ruling as “US self-sabotage” | ASEAN export rerouting up approximately 12% year-to-date |

| Canada | Halted CUSMA dispute escalation per 8 May joint statement | Lumber and steel order volumes stabilised |

| Mexico | Continued nearshoring momentum | Top US import source at approximately 16.3-16.9% share, overtaking China at 6.6-7.5% |

The pattern across all four partners is consistent: immediate relief combined with continued diversification. Supply chain rerouting that began as a tactical response to tariff volatility has become structural. A reversal of US tariff policy may not restore prior trade patterns, even if executive authority is eventually restored through legislation.

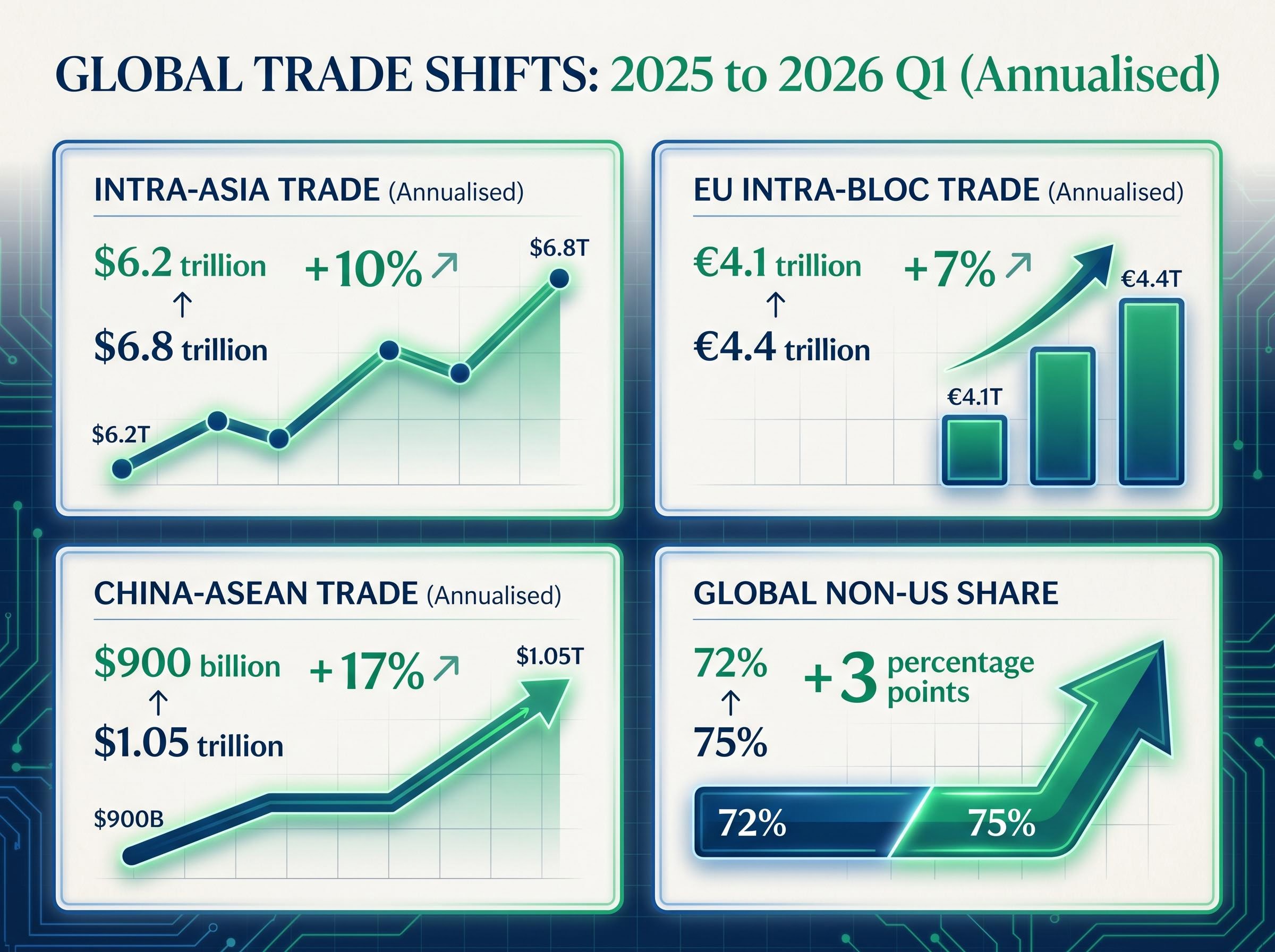

The volume figures tell the story more precisely than any single ruling can.

| Trade Corridor | 2025 Volume | 2026 Q1 (Annualised) | Change |

|---|---|---|---|

| Intra-Asia | $6.2 trillion | $6.8 trillion | +10% |

| EU Intra-Bloc | €4.1 trillion | €4.4 trillion | +7% |

| China-ASEAN | $900 billion | $1.05 trillion | +17% |

| Global Non-US Share | 72% | 75% | +3 percentage points |

Global non-US trade share rising from 72% to 75% in a single year is not a cyclical fluctuation. Global container volumes on ex-US routes climbed approximately 8% year-over-year, reinforcing the pattern. Commerce has not contracted; it has rerouted.

These figures are drawn from WTO, Eurostat, China Customs, and UNCTAD directional reporting, though exact report editions have not been independently verified. The directional trend is consistent across sources.

For investors with concentrated US equity exposure, the data suggests a policy-driven reduction in US trade activity does not translate directly into a global trade contraction. Sectors with high import exposure, particularly electronics and automobiles, face continued price adjustment risk regardless of court outcomes, given supply chain restructuring timelines of 12-18 months. Tariff removals could lower consumer prices by 1-2% in those categories, while the 15% nearshoring-driven increase in auto sector imports from Mexico indicates the structural shift is already well advanced.

Structural supply chain repricing is not unique to trade policy: the Hormuz oil risk premium demonstrates the same pattern of rerouting becoming permanent even when the original disruption resolves, with VLCC daily hire rates near $110,000 and a projected two-year recovery timeline that mirrors the 12-18 month restructuring lag the current article identifies for tariff-exposed manufacturing sectors.

The rulings do not end tariff risk. They change its speed and its mechanism.

The Brookings Institution, in a 9 May 2026 assessment, framed the shift directly:

“The rulings transfer tariff authority from the executive to Congress, slowing the pace of ‘overnight’ tariff imposition without ending tariffs as a policy tool entirely.”

Three pathways remain, ranked by legal defensibility and speed of execution:

JPMorgan’s 8 May prediction of a flatter yield curve as trade risks fade aligns with the 10-year Treasury yield reading near 4.39-4.42%, well below the historical average of approximately 5.8%. The bond market, like equities, is pricing a world where tariff shocks arrive more slowly.

The appropriate investor response is calibration, not capitulation. Tariff risk has migrated from a binary executive shock model to an extended legislative uncertainty model, which is, by its nature, more priceable by markets and more manageable within diversified portfolios.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements regarding trade policy outcomes are speculative and subject to change based on legislative, judicial, and executive developments.

The International Emergency Economic Powers Act (IEEPA) is a federal statute that grants the president broad authority to regulate international commerce during a national emergency. The Trump administration used it to impose sweeping tariffs, but the Supreme Court struck down this use on 20 February 2026, ruling that IEEPA's language does not extend to tariff imposition without explicit congressional authorisation.

After the invalidation of IEEPA and Section 122 tariff authority, the administration retains three main pathways: Section 232 national security tariffs, the Trading with the Enemy Act (though its peacetime applicability is untested), and any new legislative grant from Congress. Section 232 is considered the most legally defensible remaining tool.

Markets responded with restraint rather than a sharp relief rally: the S&P 500 gained 0.84% to close at 7,398.93, the Nasdaq rose 1.71%, and the Dow finished nearly flat on 8 May 2026. Analysts attributed the muted reaction to the fact that trade policy uncertainty had already been priced into valuations through 2025.

Major partners including the EU, Canada, China, and Mexico responded with a mix of immediate relief measures and continued long-term supply chain diversification. The EU suspended roughly 4 billion euros in retaliatory tariffs, Canada halted CUSMA dispute escalation, and Mexico consolidated its position as the top US import source, reflecting structural rerouting that analysts say is unlikely to reverse even if US tariff policy changes.

Unlike executive orders, any new congressional grant of tariff authority requires passage through both chambers of Congress, introducing a longer and less predictable timeline subject to partisan negotiation. This means tariff risk has shifted from a model of rapid overnight policy shocks to a slower legislative process that markets can price more gradually.