Stock-Bond Correlation Hits 30-Year Extreme, Rattling 60/40 Investors

13 mins ago

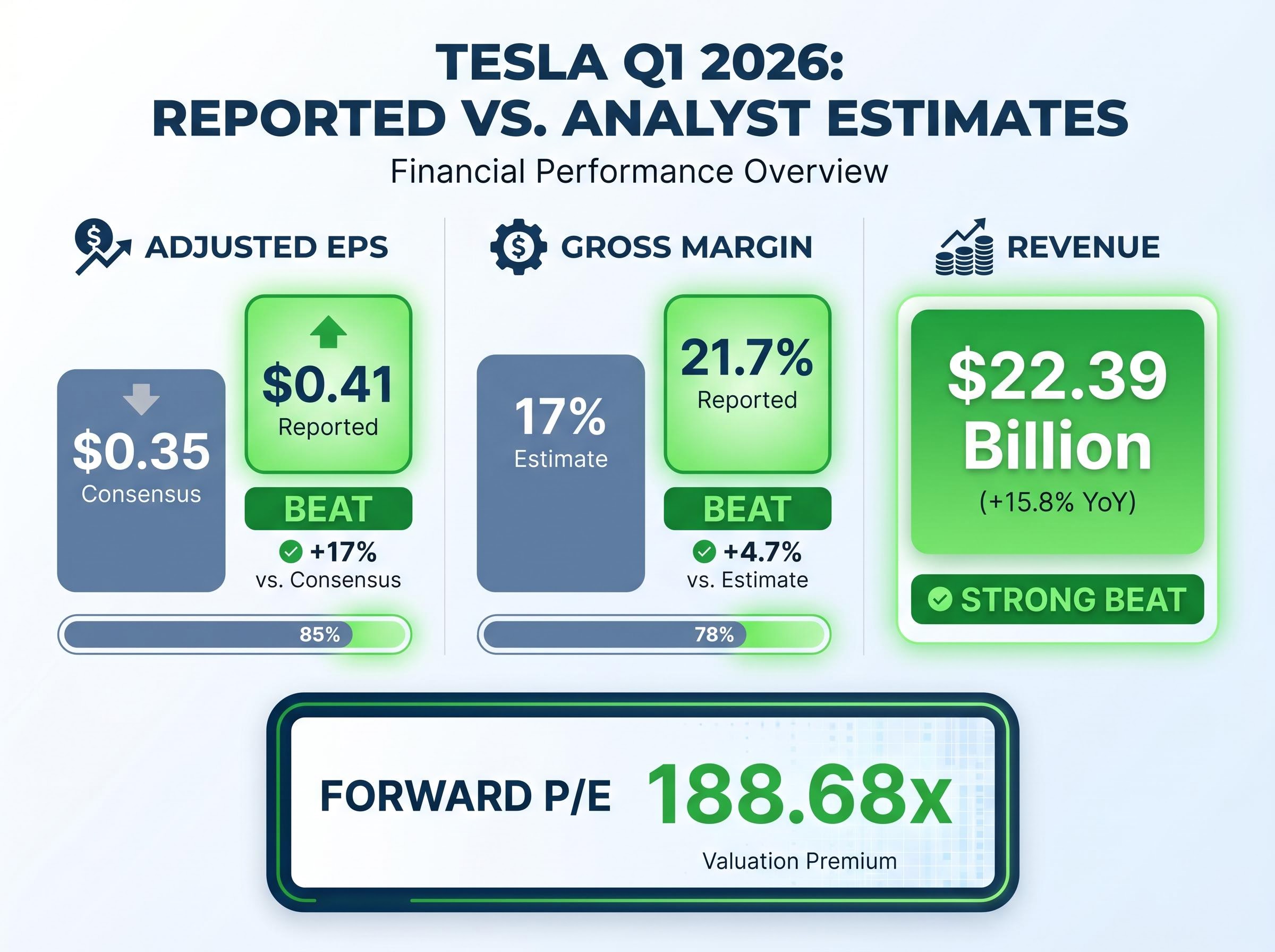

Tesla reported Q1 2026 earnings that beat Wall Street on every headline metric, and the stock’s 188x forward price-to-earnings ratio still has almost nothing to do with cars. On 22 April 2026, the company posted $22.39 billion in revenue (up 15.8% year-over-year), adjusted earnings per share of $0.41 against a $0.35 consensus estimate, and gross margins of 21.7%, well above the 17% analysts had modelled. By any conventional automotive measure, the quarter was a genuine positive surprise. But the earnings call itself barely dwelt on vehicles. The bulk of management’s narrative capital went to Optimus production ramp-ups, Fremont facility conversions, robotaxi city expansions, and a proprietary AI chip called AI5. The automotive business now functions as the funding mechanism; the AI and robotics transition is the investment thesis. This analysis separates what Tesla has concretely committed to from what remains aspirational, examines where the regulatory and competitive ground is shifting, and stress-tests whether the current share price near $390 prices in a probability of AI execution that the operational evidence actually supports.

The headline numbers were strong across every metric that matters for the automotive business:

At 188x forward earnings, Tesla is priced as an AI platform company that also happens to sell cars.

The problem is arithmetic. Tesla’s 2026 consensus EPS sits at approximately $2.25, with revenue estimates near $108.9 billion. A $1.47 trillion market capitalisation against those earnings implies almost none of the current valuation premium is explained by the car business, no matter how strong the quarter. Solid execution on the legacy automotive operation provides the cash flow that funds the transformation. It cannot independently justify the share price. Investors who treat the earnings beat as confirmation of the valuation thesis are conflating two stories that operate on entirely separate tracks.

The same analytical tension appears across multiple Musk-connected ventures: extreme valuation multiples that price in decades of future execution create asymmetric downside when timelines slip, a dynamic that SpaceX’s reported 250x EBITDA target illustrates as sharply as Tesla’s 188x forward P/E.

The earnings call laid out three categories of operational progress, each with a meaningfully different level of commitment attached.

| Category | Announcement | Current Status | Projected Milestone |

|---|---|---|---|

| Fremont / Optimus | Model S and X lines retired; facility repurposed for Optimus production | Physical conversion underway | External commercial availability projected for 2027 |

| Robotaxi | Expansion to Dallas and Houston alongside Austin; fully driverless operation | Operational in three Texas cities; autonomous miles nearly doubled in Q1 2026 | Geographic expansion timeline not specified |

| AI Infrastructure | AI5 chip in final design phase | Pre-production | No public production date confirmed |

The retirement of the Model S and Model X production line at Fremont and its repurposing as an Optimus facility is the clearest evidence of committed capital toward robotics. This is a physical, irreversible allocation decision, not a slide in a presentation. The long-term production ambition remains tens of millions of Optimus units annually, with third-party commercial availability projected for 2027.

Tesla is reportedly withholding Optimus design details because competitors have been reverse-engineering from publicly released footage. That secrecy signals both competitive pressure and genuine internal conviction about the product.

The robotaxi programme now operates across Austin, Dallas, and Houston, all fully unsupervised with no in-vehicle safety operators. Autonomous vehicle miles nearly doubled in Q1 2026 compared to the same period a year earlier. The Texas expansion is commercially operational, but it remains geographically constrained to a single state.

The investment thesis for Tesla’s AI premium often implicitly assumes first-mover dominance in both robotics and autonomy. The competitive field as of mid-2026 no longer supports that assumption without qualification.

Waymo has operated commercial driverless ride-hailing across multiple U.S. cities for several years and holds approved status from both the CPUC and California DMV, permits that Tesla does not have. The real-world data advantage accumulated over that period is substantial and difficult to replicate quickly.

The robotics field has moved from concept demonstrations to production commitments:

Two architectural philosophies are emerging. Tesla pursues vertical integration, controlling hardware, software, and deployment end-to-end. NVIDIA is building a platform-based ecosystem, partnering across manufacturers. Neither approach has proven dominant yet, but the existence of a well-funded alternative architecture means Tesla’s path is not the only viable one. Microsoft, Google, and Amazon hold financial resources that could rival Tesla’s if they choose to enter high-margin robotics or autonomous vehicle markets at scale.

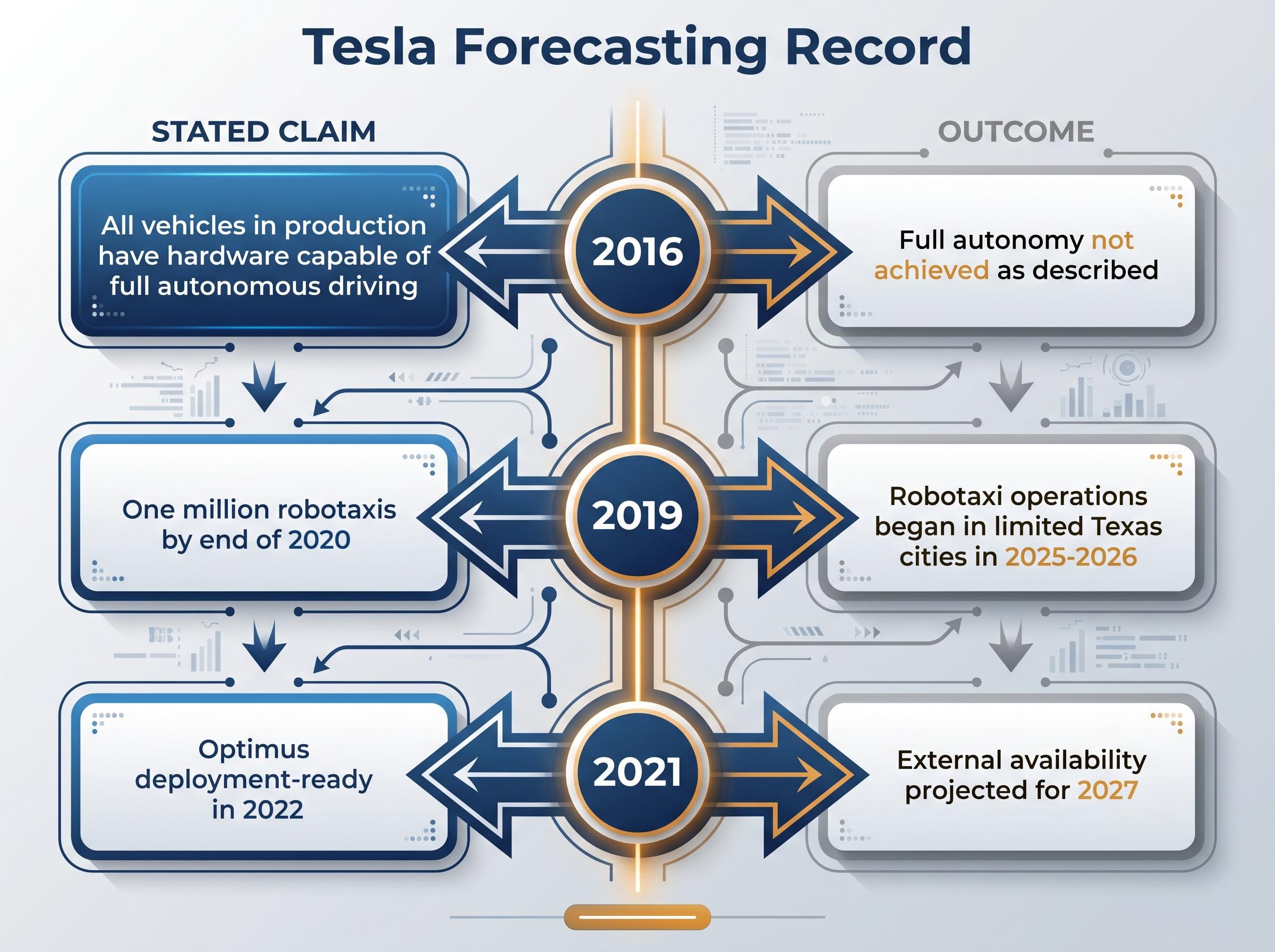

Investors evaluating a 188x forward P/E are, by definition, assigning high probability to forward projections materialising on something close to the stated timeline. That probability assignment should be calibrated against the available data, and the most relevant data set is Elon Musk’s own forecasting record on these specific technologies.

The concept at work is what institutional investors sometimes call a “credibility discount”: the degree to which stated executive timelines should be adjusted based on a documented pattern of optimistic forecasting. This is not a judgement on whether the vision eventually materialises; it is a method for weighting the timeline probability embedded in the current price.

Academic research on CEO overconfidence and management forecasting, including the Hribar and Yang study published in Contemporary Accounting Research, establishes that overconfident chief executives systematically issue more optimistic forward guidance and are more likely to miss their own projections, providing empirical grounding for the credibility discount framework applied to technology executives.

| Year of Claim | Claim Made | Projected Date | Actual Outcome |

|---|---|---|---|

| 2016 | All Tesla vehicles in production have hardware capable of full autonomous driving | Implied near-term capability | Full autonomy not achieved as described |

| 2019 | One million robotaxis operating on public roads | End of 2020 | Not met; robotaxi operations began in limited Texas cities in 2025-2026 |

| 2021 | Optimus would be deployment-ready | 2022 | Did not occur on schedule; external availability now projected for 2027 |

The counterpoint is fair: Tesla has delivered products that the broader industry considered implausible, often on compressed timelines relative to competitors, even when slipping against Musk’s own stated dates. The question for investors at current prices is not whether these visions eventually materialise. It is whether $390 per share embeds a timeline probability that the historical record suggests is too optimistic.

The three Texas cities represent genuine operational progress. California represents a documented absence.

As of May 2026, neither the California DMV nor the CPUC has issued Tesla a permit for commercial driverless vehicle operations.

The regulatory facts are straightforward:

Waymo, by contrast, has been operating commercial driverless ride-hailing in multiple U.S. cities for several years, accumulating a substantial real-world data advantage in the process. California is the largest U.S. auto and technology market. The absence of a California deployment path creates a material constraint on the robotaxi revenue timeline, and it is not a regulatory detail the earnings call addressed.

The valuation debate reduces to two scenario frameworks, and the spread between them tells investors what the current price is actually purchasing.

| Scenario | Revenue Growth | Net Margin | Valuation Multiple | Projected 10yr Return |

|---|---|---|---|---|

| Bull Case | 20-35% | 20-30% | 25-35x | 11-35% annualised |

| Bear Case | 6-12% | 8-14% | 18-22x | Negative at current prices |

The bull case carries an estimated probability of 5-10%. At approximately $375-$390 per share, every projected return outcome under the bear case is negative.

A $225 spread between Goldman Sachs and Wedbush price targets signals genuine disagreement about whether Tesla’s AI optionality is worth paying for at current prices.

Wedbush’s Dan Ives maintains a $600 target, emphasising AI potential as the primary valuation driver. Morgan Stanley holds $415 with an Equalweight rating, citing capex concerns. Goldman Sachs sits at $375 with a neutral stance. Bernstein has expressed scepticism on the profitability outlook for autonomous driving operations.

The capex constraint sharpens the tension. CFO guidance of over $25 billion in 2026 capital expenditures is expected to generate substantial negative free cash flow, creating a funding pressure at precisely the moment execution proof is needed. At $390, buyers are not paying for the automotive business. They are paying for a 5-10% probability scenario to deliver a much larger-than-modelled payoff. That is a legitimate investment logic, but it requires clear-eyed understanding of what is actually being purchased.

The operational evidence is genuine. The Fremont conversion is a committed capital allocation. Three Texas cities are running fully driverless operations. Autonomous vehicle miles nearly doubled in Q1 2026.

Confirmed operational progress:

Documented execution gaps:

The investor’s decision at $390 is not whether Tesla’s AI transformation will happen eventually. It is whether the current share price correctly embeds the timeline and probability of that transformation materialising in a way that generates positive returns from this entry point. Buyers who accumulated shares near $100 a few years ago and buyers entering at $390 today are making fundamentally different bets, even if the bull case thesis they cite is identical. The forward EPS consensus of approximately $2.25 for 2026, with analyst projections implying roughly 5x growth from current levels over the medium term, underscores how much future execution is already priced in.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Tesla's forward price-to-earnings ratio stands at approximately 188x, meaning the stock is priced as an AI and robotics platform company rather than a conventional automaker. At this multiple, almost none of the valuation premium is explained by the automotive business alone.

Tesla reported Q1 2026 revenue of $22.39 billion (up 15.8% year-over-year), adjusted EPS of $0.41 against a $0.35 consensus estimate, and gross margins of 21.7%, well above the 17% analysts had modelled.

Optimus is Tesla's humanoid robot, with Tesla having physically converted its Fremont facility to produce it. External commercial availability is projected for 2027, though Tesla has a documented history of timeline slippage on major product announcements.

As of May 2026, neither the California DMV nor the California Public Utilities Commission has issued Tesla a permit for commercial driverless vehicle operations, creating a material constraint on its robotaxi revenue timeline given California is the largest U.S. auto and technology market.

Analyst price targets range from $375 (Goldman Sachs, neutral) and $415 (Morgan Stanley, Equalweight) on the cautious end, to $600 (Wedbush) on the bullish end, with the $225 spread reflecting deep disagreement about whether Tesla's AI optionality justifies its current valuation at around $390 per share.