How to Position for the Most Event-Dense Week of July 2026

6 hrs ago

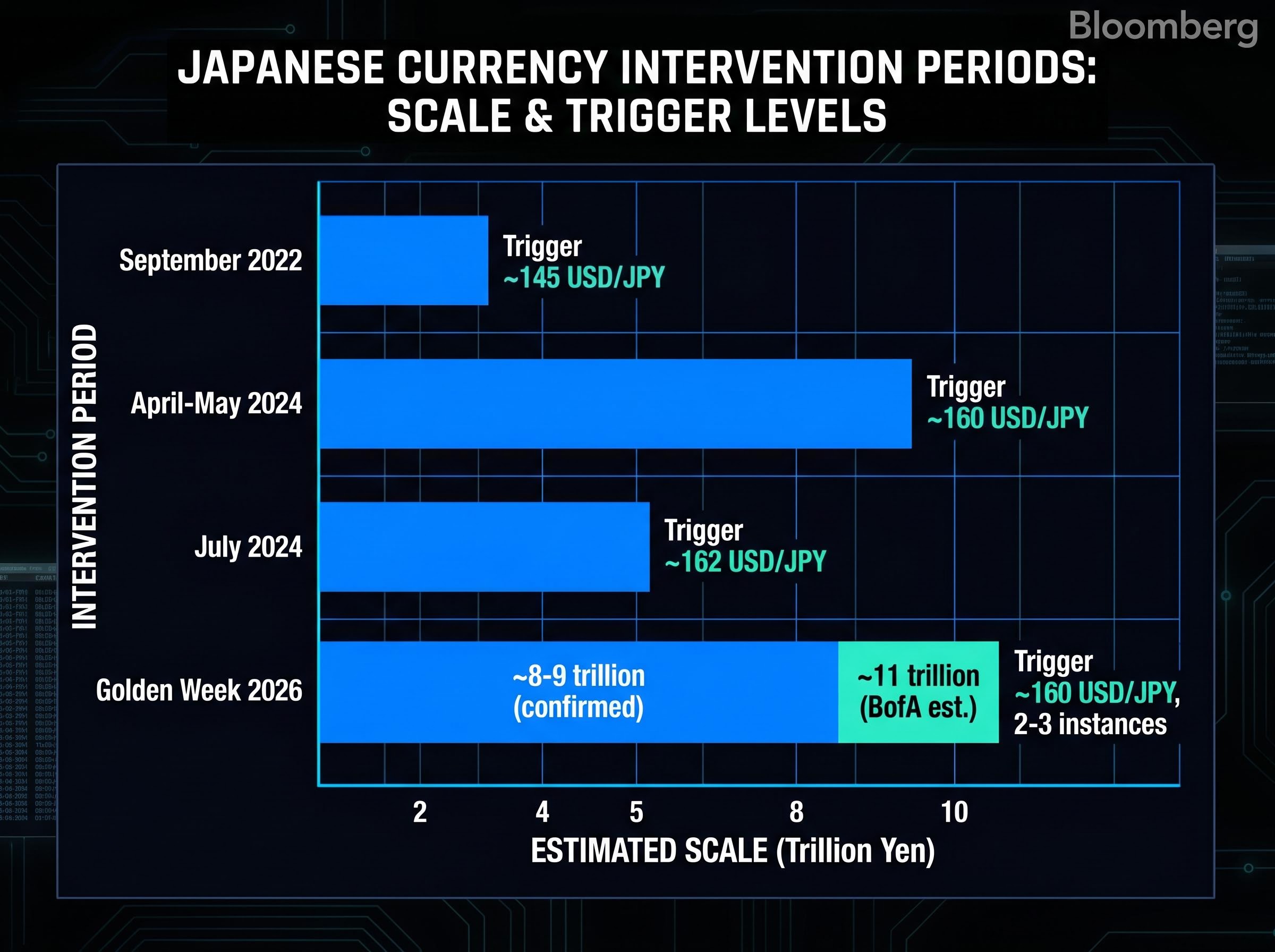

Japan’s Ministry of Finance is believed to have deployed up to 9 trillion yen across multiple operations during the Golden Week holiday window, a scale of currency intervention not seen since 2022. The campaign, concentrated between 29 April and 6 May 2026, targeted the 160 USD/JPY threshold that had come to represent a line in the sand for Japanese policymakers. Thin holiday liquidity amplified both the yen’s weakness and the government’s response, with each trillion deployed carrying outsized price impact as major Tokyo participants sat on the sidelines.

The operation raises immediate questions across asset classes. An implied sell-down of U.S. Treasury holdings to fund the intervention, estimated at $40-$50 billion, has placed bond investors on alert. The Bank of Japan’s rate path remains uncertain, with a June hike priced at roughly 40% probability. What follows covers the scale of the intervention, how the mechanics work, the Treasury market spillover, IMF compliance constraints, the BoJ policy backdrop, and a forward-looking watch list for investors tracking what comes next.

The first confirmed operation landed on or around 1 May, when Bank of Japan current account data, as reported by Bloomberg, indicated the Ministry of Finance (MoF) had sold approximately 5.4 trillion yen (roughly $34.5 billion) in a single intervention. That figure alone would rank among the largest single-day currency operations in Japanese history.

Bank of America strategist Shusuke Yamada has extrapolated a broader campaign estimate of approximately 11 trillion yen (around $72 billion), applying a rule-of-thumb of roughly 1 yen of USD/JPY movement per 1 trillion yen deployed. That figure remains unconfirmed. The Ministry of Finance has not released official totals as of 7 May 2026.

Vice Finance Minister Atsushi Mimura characterised the yen’s decline as driven by “speculative” forces and warned that the government stood ready to take further action. His statement, issued on 1 May, stopped short of confirming specific intervention amounts.

Japan’s foreign exchange reserves stand at approximately $1.4 trillion, providing substantial capacity for continued operations, though each intervention draws down that buffer.

The table below places the Golden Week campaign in the context of prior episodes:

| Period | Estimated Scale (trillion yen) | Trigger Level (USD/JPY) | Duration |

|---|---|---|---|

| April-May 2024 | ~9.8 | ~160 | Multiple days |

| July 2024 | ~5.5 | ~162 | 2-3 days |

| September 2022 | ~2.8 | ~145 | 1 day |

| Golden Week 2026 | ~8-9 (confirmed); ~11 (BofA est.) | ~160 | 2-3 instances |

Yen intervention follows a specific chain of command. The Ministry of Finance makes the decision to intervene, then issues an execution order to the Bank of Japan, which acts as the government’s agent in foreign exchange markets. The BoJ sells U.S. dollars and buys yen in spot markets, drawing on Japan’s pool of foreign exchange reserves to fund the operation.

Those reserves are predominantly held in dollar-denominated assets, primarily U.S. Treasuries and other fixed-income instruments. To raise the dollars needed for sale, the BoJ liquidates or uses these assets as collateral. The purchased yen then flows into the market, strengthening the currency against the dollar.

The step-by-step sequence:

Golden Week, Japan’s longest holiday period, removes the majority of Tokyo-based institutional participants from the market. Liquidity drops sharply. BofA’s analysis applies a ratio of approximately 1 yen of USD/JPY movement per 1 trillion yen deployed under normal conditions, but thin holiday volumes mean each operation punches harder.

The government’s choice to act during this window was both tactical and risky: tactical because reduced liquidity amplified impact, risky because it also amplified the potential for disorderly price action.

The most consequential cross-asset implication sits in the U.S. bond market. If Japan liquidated reserve assets to fund the intervention, the implied Treasury sales could range from $40-$50 billion, a figure derived from the assumption that intervention cash was raised through selling existing holdings rather than through maturing securities or investment returns.

This figure is a derived estimate and has not been confirmed by the Ministry of Finance, the U.S. Treasury, or any publicly available data. No U.S. Treasury International Capital (TIC) data covering the intervention window has been published as of 7 May 2026.

Vice Finance Minister Mimura confirmed “extremely close contact” with U.S. counterparts on market conditions, a statement analysts have interpreted as a deterrent signal aimed at speculative positioning rather than evidence of formal coordination on Treasury sales.

To help readers assess the information tiers in this section:

For bond investors, even the possibility of a supply injection of this scale matters for duration pricing and yield levels at a time when the U.S. Treasury market is already sensitive to issuance volumes.

Treasury yield implications of a large reserve liquidation are complicated by a structural factor that Wolfe Research’s yield decomposition highlights: roughly half of the 40-basis-point yield surge since the Iran conflict began is attributable to growth repricing rather than the geopolitical shock itself, meaning even a resolution of the Hormuz closure would not fully reverse the yield environment into which any Japan reserve sales land.

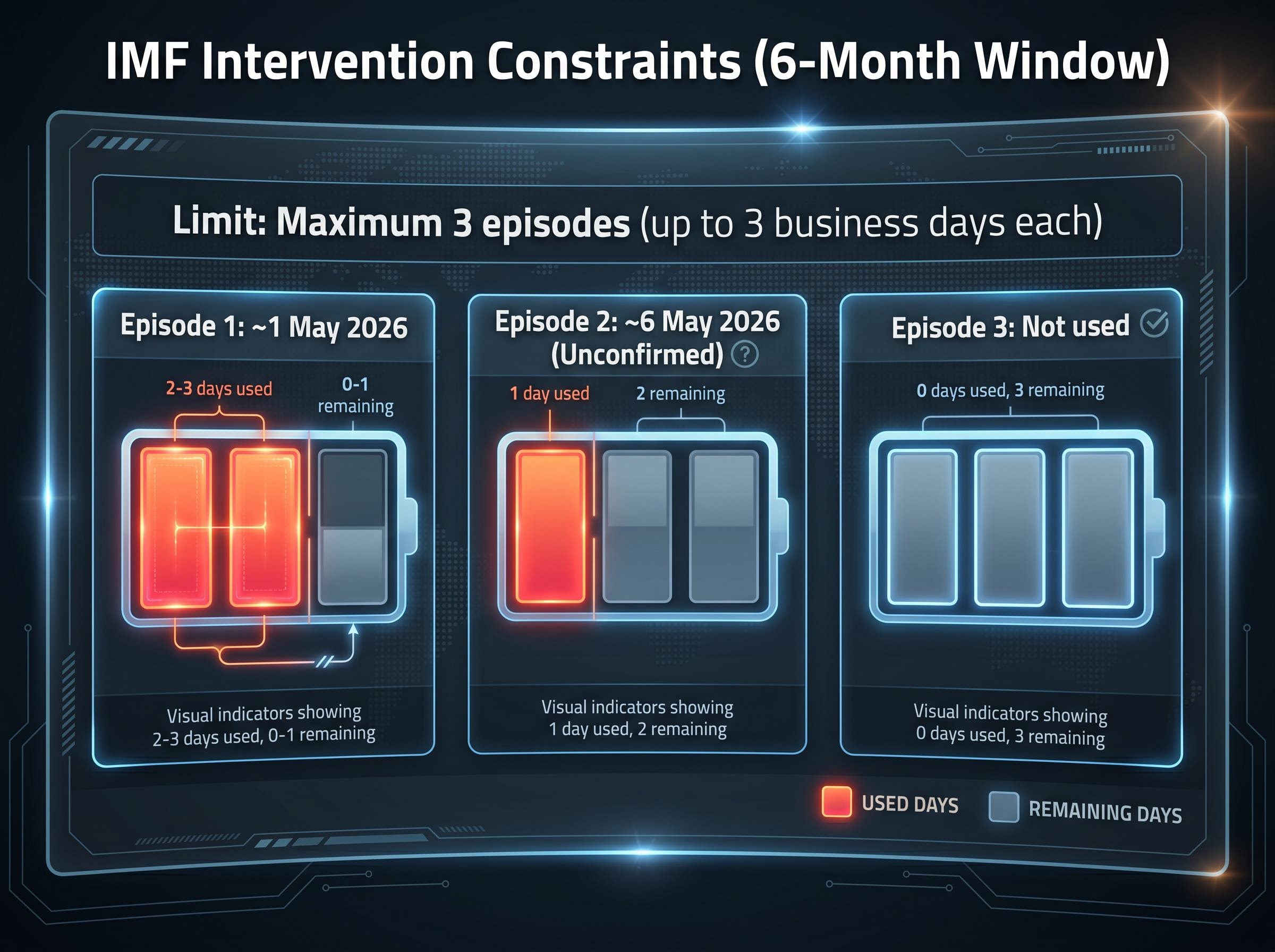

The International Monetary Fund (IMF) classifies the yen as a free-floating currency. Maintaining that classification requires Japan to limit intervention to a maximum of three episodes, each lasting up to three business days, within any six-month rolling window. Breaching this threshold could trigger a reclassification review, a scenario no major economy courts willingly.

The IMF free-floating classification criteria define a free-floating regime as one where intervention occurs only exceptionally, capped at three instances within any six-month period with each lasting no more than three business days, the precise framework that determines how much runway Japan retains before a reclassification review becomes a live risk.

The Golden Week operations appear to constitute one or possibly two distinct episodes. Trading behaviour on 6 May was flagged by analysts as a possible start of a second episode, and BofA identified 7 May and 8 May as potential continuation dates. No new interventions were confirmed on either day.

| Episode Number | Approximate Start Date | Business Days Used | Business Days Remaining |

|---|---|---|---|

| Episode 1 | ~1 May 2026 | 2-3 | 0-1 |

| Episode 2 (unconfirmed) | ~6 May 2026 | 1 (if confirmed) | 2 (if confirmed) |

| Episode 3 | Not used | 0 | 3 |

The IMF framework is the structural ceiling on Japan’s intervention capacity. With one to two episodes potentially consumed, the runway is narrowing. Each additional day of intervention carries compliance risk alongside market impact.

Intervention is a pressure-relief valve. It absorbs speculative momentum and resets the exchange rate for a period of days or weeks. It does not resolve the structural forces pulling the yen lower.

The market-implied probability of a BoJ rate hike at the June 2026 meeting sits at approximately 40%, a figure that reflects mixed analyst sentiment rather than conviction. The Golden Week interventions do not appear to have materially shifted monetary policy expectations.

Three structural drivers sustain yen weakness regardless of intervention:

BoJ-Fed policy divergence is not simply a matter of headline rate levels; the April 2026 FOMC meeting produced a historic four-way internal dissent, reflecting a committee genuinely torn between a 3.5% PCE reading and rising unemployment, a dynamic that makes Fed rate cuts far less predictable than market pricing implies and keeps the interest rate gap wider for longer than the yen needs.

BofA characterised a scenario in which intervention drove the June hike probability to approximately 40% as a “strategic opportunity” for JPY-positive positioning, framing it as a tactical entry point rather than a signal of policy change.

USD/JPY closed at 156.2680 on 7 May, stabilising within the 155-157 range following the intervention campaign. The pair had surged approximately 3% in the immediate aftermath of the first operation before trimming gains.

With the holiday window closed and no new interventions confirmed on 7 May or 8 May, attention now shifts to a sequence of signals that will arrive on a defined timeline:

Japanese capital repatriation estimates as high as $500 billion have been cited by JPMorgan as a compounding stress factor in U.S. credit markets, a figure that contextualises the Golden Week reserve liquidation not as an isolated event but as one tranche of a broader, structurally-driven capital flow reversal that bond and equity markets are still pricing in.

The 160 USD/JPY level has now been defended across three separate intervention campaigns: April-May 2024, and now Golden Week 2026. Each defence reinforces its significance as a psychological threshold. Whether that threshold holds without active intervention in the weeks ahead is the most informative test of the campaign’s lasting impact.

The Golden Week campaign was historically large. The confirmed single-operation figure of approximately 5.4 trillion yen and the broader campaign estimate of 8-9 trillion yen place it alongside the most aggressive Japanese currency interventions on record. Three things are now clearer: the approximate scale, the derived Treasury spillover risk of $40-$50 billion (unverified), and the IMF compliance position, with one to two episodes consumed and the runway narrowing.

None of this addresses the policy divergence driving yen weakness. The BoJ June meeting remains the next structural inflection point. How USD/JPY behaves in the 155-160 range over the coming sessions will indicate whether the intervention has shifted market psychology or simply delayed the next test of the threshold.

Investors tracking the bond market spillover from reserve liquidation will find our full explainer on the 5% Treasury yield threshold useful, as it covers BofA’s Hartnett framework for what a breach of that level would trigger across mortgages, corporate borrowing costs, and equity valuations, with the 12 May CPI release identified as the most immediate catalyst.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements regarding BoJ policy, exchange rate movements, and Treasury market impacts are speculative and subject to change based on market developments.

Japan yen intervention is when the Ministry of Finance orders the Bank of Japan to sell U.S. dollars and buy yen in spot currency markets, using Japan's foreign exchange reserves (primarily U.S. Treasuries) to fund the operation and push the yen higher against the dollar.

The Ministry of Finance is estimated to have deployed approximately 8-9 trillion yen across multiple operations between 29 April and 6 May 2026, with Bank of America estimating the total could reach around 11 trillion yen, though official figures had not been released as of 7 May 2026.

To fund yen intervention, Japan liquidates dollar-denominated reserve assets including U.S. Treasuries; the Golden Week 2026 campaign implies an estimated $40-$50 billion in Treasury sales, which could add supply pressure to an already yield-sensitive bond market, though this figure remains unverified.

The IMF classifies the yen as a free-floating currency, which caps Japan at a maximum of three intervention episodes, each lasting no more than three business days, within any six-month rolling window; breaching this could trigger a currency regime reclassification review.

The 160 USD/JPY level has now been defended across three separate Japanese intervention campaigns, including April-May 2024 and Golden Week 2026, making it a widely recognised psychological threshold that market participants and policymakers treat as a line the Ministry of Finance will act to defend.