Brent Falls to $99, but the Strait of Hormuz Is Still Closed

32 mins ago

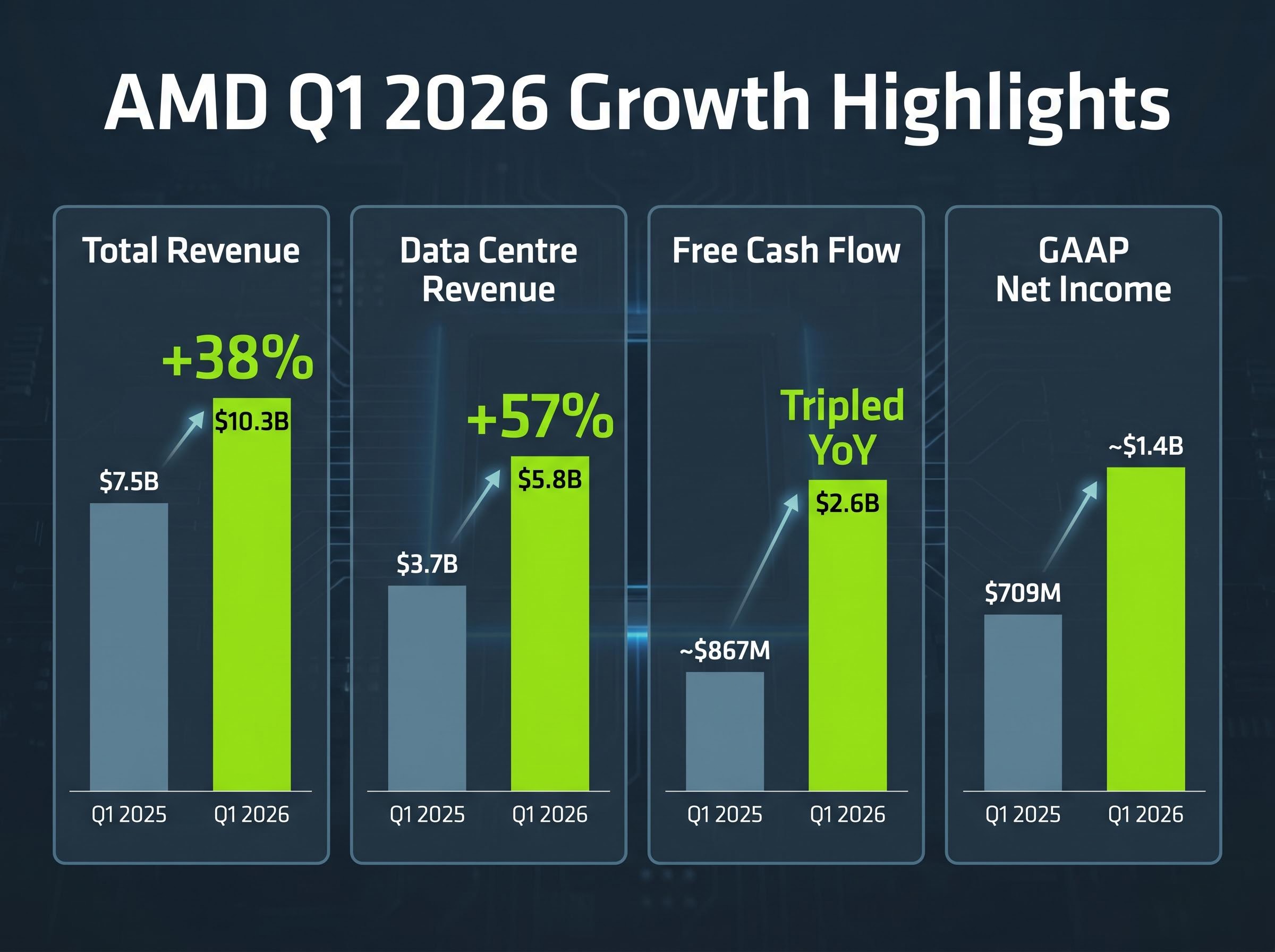

AMD’s free cash flow tripled year-over-year to a record $2.6 billion in Q1 2026. That single figure, more than the revenue beat or the earnings surprise, signals the company has crossed a threshold: profitability is now scaling faster than the top line, and the AI infrastructure buildout is generating cash, not just consuming it.

The results, reported on 5 May 2026, landed against a backdrop of cautious optimism across technology earnings. Nasdaq 100 futures climbed 0.7% the following morning as investors processed a strong reporting season, and AMD’s numbers added fuel to the momentum. They also raised the stakes for Nvidia’s own earnings report later this month. What follows is a breakdown of what AMD’s quarter actually delivered, where the growth is concentrated inside the business, how Wall Street repriced the stock overnight, and what remains genuinely unresolved about AMD’s competitive position in the race to supply AI infrastructure.

The top line came in at $10.3 billion, up 38% year-over-year and above the high end of management guidance. Non-GAAP earnings per share of $1.37 beat the analyst consensus range of $1.25-$1.29, a gap of roughly 6-10% that forced immediate re-evaluation of forward estimates.

GAAP net income nearly doubled to approximately $1.4 billion, up from $709 million in Q1 2025. Free cash flow tripled to $2.6 billion, a company record that underscores the operating leverage now embedded in the business model.

The number that matters most sits inside the data centre segment: $5.8 billion in revenue, up 57% year-over-year. That division alone now accounts for more than half of AMD’s total revenue, a structural shift from a company that was, until recently, defined by its PC processor rivalry with Intel.

| Metric | Q1 2026 Result | Q1 2025 Comparison | Analyst Consensus |

|---|---|---|---|

| Revenue | $10.3B | $7.5B | Below $10.3B |

| Non-GAAP EPS | $1.37 | N/A | $1.25-$1.29 |

| GAAP Net Income | ~$1.4B | $709M | N/A |

| Free Cash Flow | $2.6B | ~$867M | N/A |

| Data Centre Revenue | $5.8B | $3.7B | N/A |

CEO Lisa Su described the quarter as “outstanding,” citing “accelerating demand for AI infrastructure” as the primary growth catalyst.

The $5.8 billion data centre figure is not the product of a single chip cycle. It reflects two distinct product lines working in parallel, each serving different layers of the AI infrastructure stack.

The breadth matters. A single product dependency would make 57% growth fragile. A multi-product platform shift makes it structurally harder to reverse.

CEO Lisa Su noted on the earnings call that customer engagement with the MI450 GPU series is “strengthening,” with forecasts exceeding initial expectations. Management indicated server growth is expected to “accelerate meaningfully” going forward.

The Advancing AI 2026 Event, scheduled for July 2026, represents AMD’s next major product strategy disclosure. It is not an earnings event but a roadmap presentation where the MI450 ramp timeline and next-generation product details are expected to take shape. For investors evaluating near-term revenue visibility, that event is the next concrete milestone.

AMD’s 57% data centre revenue growth arrived on top of an already elevated prior-year base, and it illustrates a demand dynamic that differs from the server refresh cycles that historically drove semiconductor earnings.

Hyperscalers and cloud providers are building AI infrastructure at a pace that exceeds traditional procurement patterns. The demand splits into two categories worth understanding:

The demand environment AMD is benefiting from is anchored in hyperscaler AI capital expenditure that reached $130 billion in Q1 2026 alone across Amazon, Microsoft, Alphabet, and Meta, with full-year 2026 combined projections at $725 billion and a trajectory toward $1 trillion annually by 2027.

AMD’s data centre segment now accounts for more than half of total company revenue: $5.8 billion of $10.3 billion in Q1 2026.

The distinction between training and inference demand matters because it means the market is not dependent on a single phase of AI development. Training drove the initial wave; inference is broadening it. Intel’s stronger-than-expected Q1 CPU results provide a parallel signal that the infrastructure buildout is lifting multiple semiconductor companies, not just AI GPU specialists. Nasdaq 100 futures rising 0.7% on 6 May partly reflected this broader AI earnings optimism.

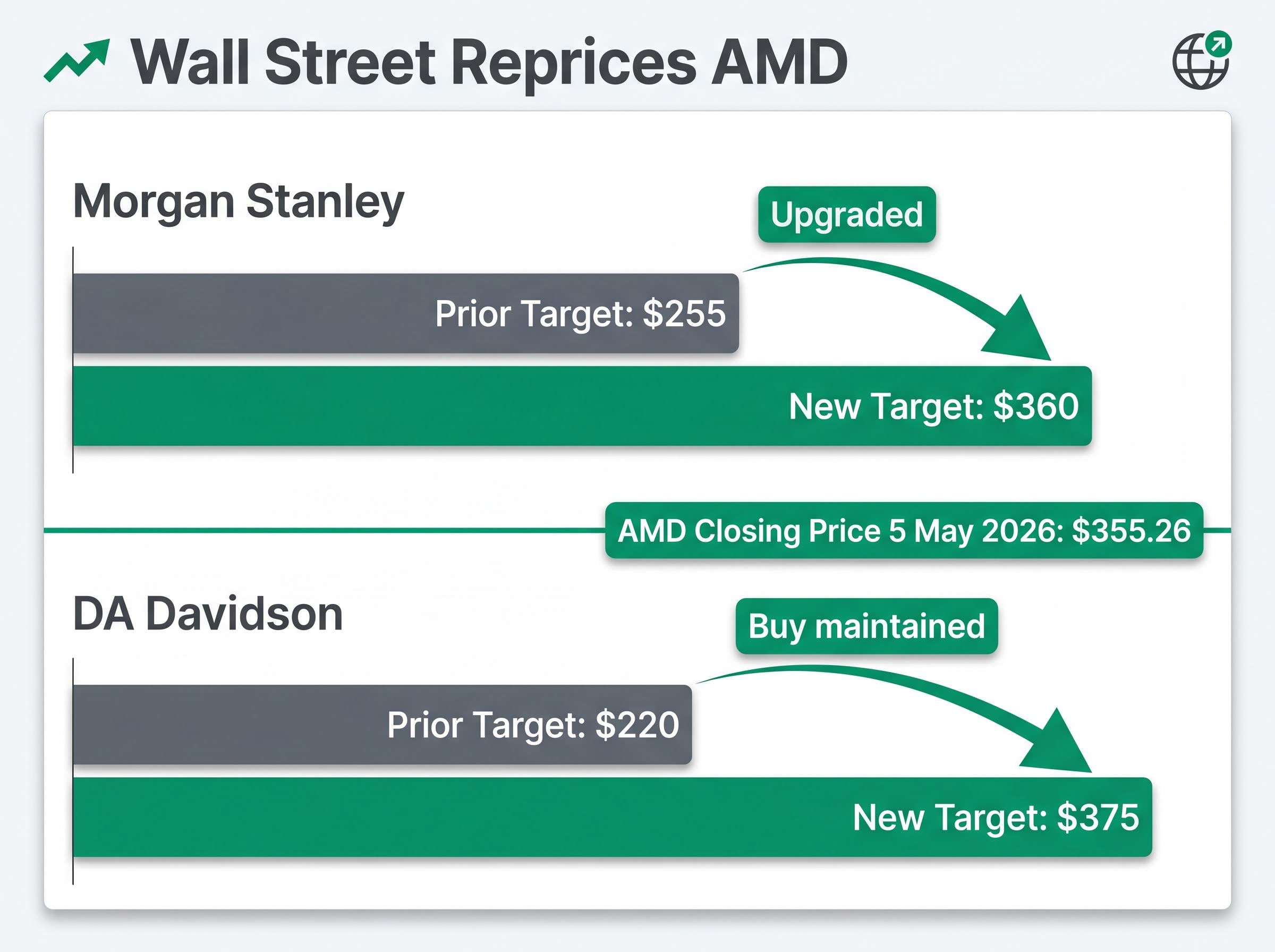

AMD closed at $355.26 on 5 May 2026, up 4.02% on the regular session before the earnings release. The after-hours reaction was substantially larger, with the stock surging in the range of approximately 15%-18% across various reports (specific figures varied, with no single number definitively confirmed, but the direction and magnitude reflected strong institutional validation).

The analyst community moved quickly. Morgan Stanley raised its AMD price target to $360 from $255, a 41% increase. DA Davidson went further, lifting its target to $375 from $220, a 70% revision, while maintaining a Buy rating.

Two details from the earnings report that carry significant forward weight are the Q2 guidance and Meta supply deal: AMD guided Q2 revenue to approximately $11.2 billion, clearing analyst consensus by $700 million, while a separate $60 billion Meta chip supply agreement covering five years of MI300X and MI325X GPU shipments provides contractually anchored revenue visibility that extends the growth story well beyond any single quarter.

| Analyst Firm | Prior Price Target | New Price Target | Rating |

|---|---|---|---|

| Morgan Stanley | $255 | $360 | Upgraded |

| DA Davidson | $220 | $375 | Buy (maintained) |

BofA Securities characterised AMD’s execution positively but flagged a specific uncertainty: how chip market share will ultimately be distributed among rivals supplying OpenAI’s infrastructure. That question remains open, and it is the primary reason the analyst community has not converged on a single view of AMD’s forward valuation.

AMD has secured seats at the most visible AI infrastructure tables. The question investors have not yet answered is how large those seats will be.

The highest-profile proof point is the AMD-OpenAI strategic partnership, announced in October 2025:

A separate partnership expansion with Meta, announced on 24 February 2026, involves GPU supply at scale and reinforces AMD’s presence in hyperscaler procurement.

BofA’s caution is worth holding alongside that optimism. Nvidia and Broadcom are competing for the same infrastructure contracts, and the distribution of chip supply across OpenAI’s buildout has not been publicly disclosed. Seat presence and contract volume are not the same thing.

Nvidia and Broadcom valuations illuminate the competitive context around AMD: Nvidia trades at approximately 24x forward earnings despite $193.7 billion in FY2026 data centre revenue, while Broadcom commands a higher 37x multiple on the back of locked-in multi-year ASIC contracts with Google and Meta, a valuation spread that reflects how differently the market prices GPU-scale volume against contract-backed predictability.

Nvidia’s earnings report, expected later in May 2026, will function as a competitive benchmark. It will help investors determine whether AMD’s data centre growth represents genuine market share gains or participation in an expanding market that is lifting all suppliers. The comparison will shape how the market interprets AMD’s Q1 results in hindsight.

AMD’s results are not isolated. They are one data point in a cluster that is forcing the semiconductor sector to reprice its role in AI infrastructure.

Samsung Electronics crossed the $1 trillion market capitalisation milestone on 6 May 2026, driven partly by AI-related memory chip demand. Samsung’s stock has more than doubled year-to-date, a signal that the AI buildout is creating value across the semiconductor supply chain, from GPUs to memory.

Samsung Electronics crossed $1 trillion in market capitalisation on 6 May 2026, with the stock more than doubling year-to-date on AI memory chip demand.

Intel’s stronger-than-expected Q1 CPU results add another layer. The AI infrastructure cycle is generating returns not just for the accelerator chip designers but for the broader ecosystem of semiconductor companies supplying the buildout.

Three catalysts will test whether Q1’s momentum holds:

AMD’s Q1 2026 results are unambiguous. Revenue growth of 38%, data centre expansion of 57%, record free cash flow of $2.6 billion, and analyst price target revisions of 41-70% leave little room for debate about the quarter itself.

What remains open is the competitive question. The OpenAI supply share distribution among AMD, Nvidia, and Broadcom has not been settled. Nvidia’s May earnings will provide the next comparative reading. AMD’s July roadmap event will reveal whether the MI450 ramp can sustain the data centre trajectory.

Inference cost sustainability is the structural challenge that could eventually slow the hyperscaler procurement cycle: escalating inference costs are making generative AI applications fundamentally unprofitable at current margins, and if that dynamic persists, it creates a ceiling on how long hyperscalers can justify $725 billion annual capex commitments regardless of near-term demand signals.

Investors following this story should treat those catalysts as the next chapters, not the final word.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

AMD reported Q1 2026 revenue of $10.3 billion, up 38% year-over-year, with non-GAAP EPS of $1.37 beating analyst consensus of $1.25-$1.29, and record free cash flow of $2.6 billion, triple the prior year figure.

An AI accelerator is a specialised chip, typically a GPU, designed to handle the mathematical operations required by artificial intelligence workloads; AMD's Instinct MI series GPUs compete directly in this market and are a primary driver of the company's 57% data centre revenue growth in Q1 2026.

Morgan Stanley raised its AMD price target by 41% to $360, while DA Davidson lifted its target by 70% to $375, and AMD's stock surged approximately 15%-18% in after-hours trading following the results.

Three key catalysts follow the Q1 results: the AMD Advancing AI 2026 Event in July, which will detail the MI450 GPU ramp; Nvidia's May 2026 earnings report, which will clarify market share dynamics; and the first AMD-OpenAI deployment of 1 gigawatt of computing power planned for H2 2026.

AMD has a $60 billion chip supply agreement with Meta covering five years of MI300X and MI325X GPU shipments, providing contractually anchored revenue visibility that extends well beyond any single quarter.