Apple’s A-series and M-series chips have been TSMC’s to manufacture, almost without exception, for over a decade. That near-monopoly may be starting to crack.

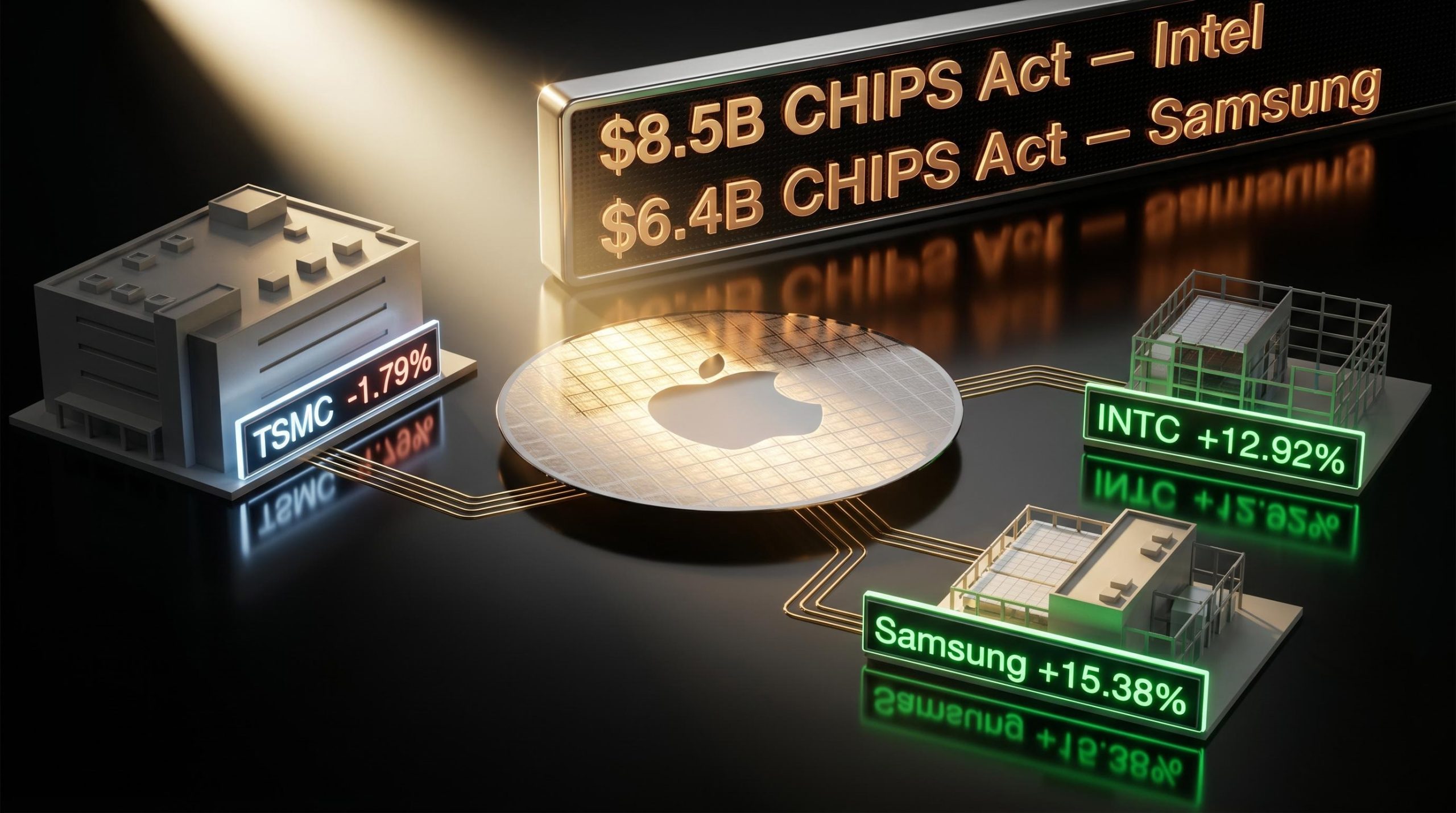

Bloomberg reported on 4-5 May 2026 that Apple has entered early-stage discussions with both Samsung Foundry and Intel Foundry Services about manufacturing central processors at US-based facilities. The report landed days after Apple’s Q2 2026 earnings call flagged supply chain constraints, and it immediately moved markets across the global semiconductor sector. Intel surged 12.92%. Samsung Electronics jumped roughly 15.38%. TSMC slipped 1.79%. Apple itself dipped, then recovered.

What follows is a breakdown of what Apple is actually pursuing, why the talks are happening now, what the manufacturing realities mean for any realistic shift, and what investors in all four companies should make of the market reaction and the road ahead.

What Apple is reportedly exploring with Samsung and Intel

The core claim in Bloomberg’s reporting is straightforward: Apple has held exploratory discussions with Samsung Foundry and Intel Foundry Services about manufacturing A-series and M-series processors at US-based fabrication plants. Apple executives visited Samsung’s facility under construction in Taylor, Texas, and held separate conversations with Intel’s foundry division.

Every credible outlet that covered the initial report reinforced the same constraint on interpretation:

- 9to5Mac (4 May 2026): “Talks still in early stages… no orders in place.”

- Reuters (4 May 2026): “Discussions remain at early stages as neither effort has resulted in any orders.”

- MacRumors (5 May 2026): “The talks are said to be preliminary, and no orders have been made.”

- Engadget (5 May 2026): “No orders have been placed so far and talks… are still preliminary.”

No follow-up developments, confirmations, or denials have emerged from any of the four companies as of 6 May 2026. The significance here sits not in the operational details but in the strategic direction Apple has signalled by initiating the conversations at all.

When big ASX news breaks, our subscribers know first

Why Apple is pushing to reduce its TSMC dependency now

This is not a reactive decision. Three compounding pressures converged in early 2026, each building over years but reaching a decision point within the same quarter:

- Geopolitical concentration risk. TSMC’s manufacturing base in Taiwan represents a single point of failure that China-Taiwan tensions make increasingly uncomfortable for Apple’s board and supply chain leadership.

- AI-driven capacity competition. The artificial intelligence boom has intensified demand for advanced node capacity across the industry, squeezing the supply of the very production slots Apple requires.

- CHIPS Act financial incentives. US policy now subsidises domestic semiconductor production at a scale that changes the cost equation. Intel has received $8.5 billion in CHIPS Act grants for its US fabs. Samsung’s Taylor facility has $6.4 billion allocated under the same programme.

AI capacity competition across the advanced node market intensified sharply in 2026 as four hyperscalers committed a projected $650 billion in infrastructure capital expenditure, concentrating demand for 3nm and 2nm production slots at precisely the fabs Apple relies on and narrowing the margin for error in Apple’s own capacity planning.

The CHIPS Act funding allocations for domestic semiconductor manufacturing represent a structural shift in the cost economics of US-based fabrication, with Intel receiving $8.5 billion and Samsung’s Taylor facility awarded $6.4 billion in direct grants, underwriting precisely the facilities Apple is now evaluating as alternatives to TSMC.

CHIPS Act context: The combined $14.9 billion allocated to Intel and Samsung under the CHIPS Act represents the largest US government investment in foundry capacity since the programme’s inception, directly underwriting the facilities Apple is now evaluating.

The timing is also telling. Apple’s Q2 2026 earnings call on 30 April 2026 explicitly flagged supply chain constraints and “limited flexibility,” language that suggests internal conversations about diversification were already well underway before the Bloomberg report surfaced. This is a resilience strategy, not a replacement strategy, and the structural pressures behind it are not going away.

For investors wanting to understand the full financial context behind the supply chain disclosures, our dedicated guide to Apple’s Q2 2026 earnings report covers the record $111.2 billion revenue result alongside the specific supply chain language Tim Cook used on the call, the $100 billion buyback authorisation, and the forward guidance signals that set the stage for these foundry discussions.

Can Samsung and Intel actually build chips Apple would accept?

The gap between strategic intent and manufacturing reality is where this story gets complicated. The node-level data tells the story more honestly than any headline.

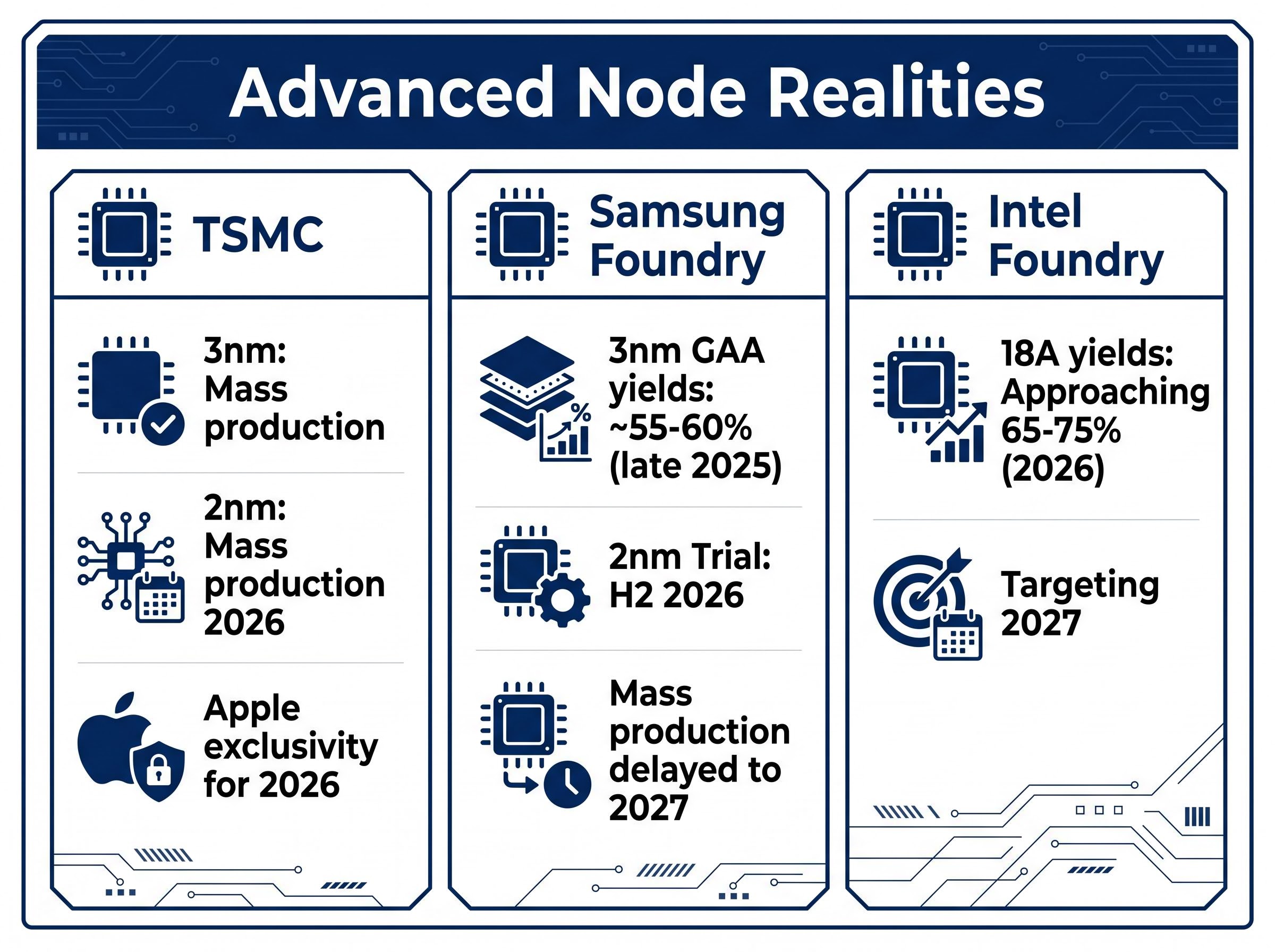

TSMC currently mass-produces Apple’s iPhone 17/A18 chips on its 3nm process (N3E/N3P). For the iPhone 18/A20, Apple holds exclusivity on TSMC’s 2nm node (N2) for the 2026 launch. That exclusivity alone makes any near-term shift for flagship chips structurally impossible.

Samsung Foundry’s 3nm gate-all-around (GAA) process is in production, but yields of approximately 55-60% in late 2025 lagged TSMC’s performance. Trial production at 2nm is targeted for H2 2026, with mass production delayed to 2027. The Taylor fab is not yet at production volume.

Intel’s foundry position

Intel’s 18A node (sub-2nm equivalent) has shown yield improvements approaching 65-75% in 2026, but it remains entirely unproven at the volumes Apple would require, even for a limited tranche. The foundry pivot itself is nascent, with Intel Foundry Services reporting losses as it builds external customer relationships.

| Foundry | 3nm Status | 2nm Timeline | Apple Shift Realism |

|---|---|---|---|

| TSMC | Mass production; strong yields; Arizona Fab 21 ramping | N2 mass production 2026; Apple exclusivity for A20 | Baseline partner; no shift required |

| Samsung Foundry | 3nm GAA in production; yields ~55-60% | Trial H2 2026; mass production delayed to 2027 | Low for 2026; possible limited backup by 2027 |

| Intel Foundry | Intel 3 yielding; 18A improvements noted | 18A (sub-2nm) targeting 2027; unproven at scale | Very low near-term; scale untested for external customers |

Bloomberg sources stated directly that “Intel and Samsung can’t reliably offer the type of production and scale” that TSMC provides.

Any initial volume shift would likely be capped at less than 10% of Apple’s total chip volume, directed at non-flagship components rather than the primary A-series or M-series processors. The manufacturing gap is the reason investors should not read this as a TSMC displacement story.

How markets priced the Apple supply chain news on May 5

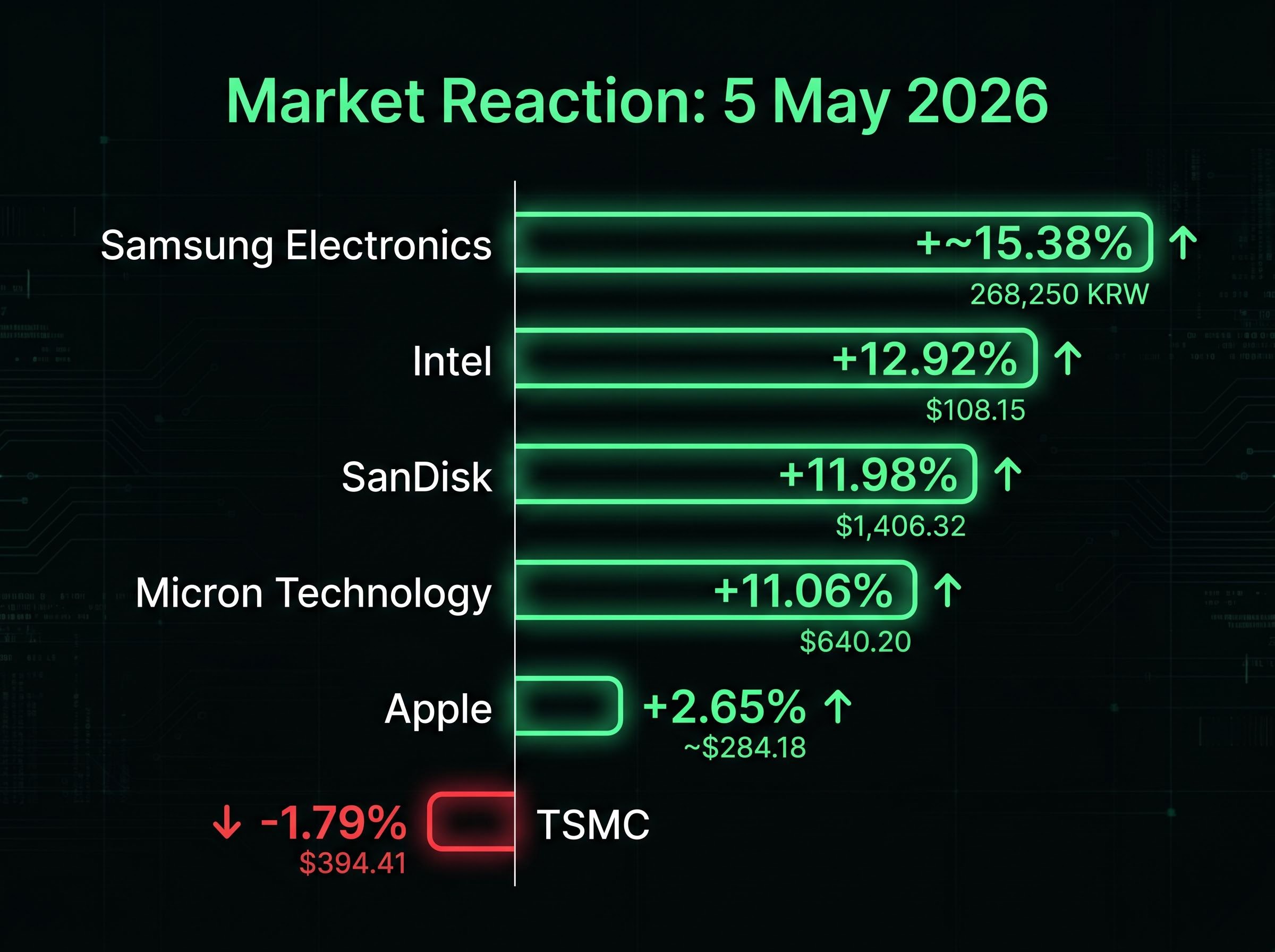

The same Bloomberg report produced four very different stock reactions on 5 May 2026, and the divergence reveals where institutional capital is placing its bets.

| Company | Ticker | May 5 Close | 1-Day Move | Analyst Read |

|---|---|---|---|---|

| Intel | INTC | $108.15 | +12.92% | Foundry credibility validation |

| Samsung Electronics | 005930.KS | 268,250 KRW | +~15.38% | Foundry strategy gaining traction |

| Apple | AAPL | ~$284.18 | +2.65% (after -1.18% on May 4) | Diversification re-priced as resilience |

| TSMC | TSM | $394.41 | -1.79% | Theoretical risk, not immediate threat |

| Micron Technology | MU | $640.20 | +11.06% | Broader semiconductor rally |

| SanDisk | SNDK | $1,406.32 | +11.98% | Broader semiconductor rally |

Intel’s surge, on volume of approximately 185.59 million shares, reflected the commercial credibility that even an exploratory Apple relationship confers on its foundry turnaround. Apple dipped on 4 May as supply chain uncertainty was priced in, then recovered on 5 May as investors reframed diversification as a net positive. TSMC’s modest decline suggests the market acknowledges theoretical risk to exclusivity without viewing it as an immediate threat.

Intel’s foundry credibility received an unusual market test on the day the Bloomberg report landed: while the current article records a 12.92% surge in INTC on 5 May, a separate trading session earlier in the week saw Intel shares fall approximately 3.85% as investors priced execution risk and capital costs rather than treating exploratory Apple interest as guaranteed accretive revenue.

The Micron and SanDisk rallies on the same day indicate part of Intel’s move was sector-wide momentum rather than purely Apple-specific. The overall market narrative treated these discussions as validating the US semiconductor buildout thesis.

What TSMC’s foundry dominance actually looks like for Apple investors

Before calibrating the disruption risk, the baseline relationship deserves scrutiny. TSMC’s position as Apple’s chip manufacturer extends well beyond volume. It includes:

- Packaging co-development: InFO and SoIC advanced packaging technologies, developed in partnership and tuned specifically for Apple silicon.

- Custom process optimisation: TSMC tunes its process nodes for Apple’s specific design requirements, a co-engineering depth no alternative foundry currently replicates.

- Long-term capacity agreements: Multi-year commitments that guarantee Apple priority access to TSMC’s most advanced nodes ahead of competitors.

TSMC controls more than 60% of the global advanced node market. No other foundry operates at comparable scale.

TSMC’s Arizona Fab 21 is ramping to approximately 100 million Apple chips in 2026, representing meaningful US-based production but still a fraction of Apple’s total global chip demand.

The 2nm exclusivity lock-in for the A20 processor provides TSMC investors with a concrete near-term protection. The 5 May decline of 1.79% may warrant monitoring as a potential overreaction given the structural depth of this relationship.

What investors should watch as Apple’s chip strategy develops

The story will either fade or escalate based on three specific milestones, listed in order of likely sequencing:

- Samsung Taylor fab reaching production-ready yields. Trial production is targeted for H2 2026, with mass production pushed to 2027. Whether yields meet Apple’s quality thresholds will be the first tangible test.

- Intel 18A proving at external-customer scale. The node improvements are noted, but no external customer has tested Intel Foundry Services at the volumes Apple would demand, even for a limited tranche.

- Apple product roadmap signals for non-flagship chip sourcing. Any indication that Apple is designing a lower-tier product around a non-TSMC chip would be the clearest evidence that exploratory talks have progressed to engineering evaluation.

A notable absence remains: no named sell-side analyst from Goldman Sachs, Morgan Stanley, JP Morgan, or Wedbush has published post-5 May volume allocation projections for Intel or Samsung. The sub-10% initial volume estimate circulating in coverage is directional, not a confirmed projection. The market’s best analysts are not yet willing to put numbers on this.

The framing question for investors is not whether Samsung or Intel will replace TSMC. It is what the value of even a small Apple volume commitment would mean for Intel’s or Samsung’s foundry credibility and forward order pipeline.

Semiconductor stock vulnerabilities extend beyond the Apple-TSMC relationship: if hyperscalers revise their $635-700 billion FY 2026 infrastructure capital expenditure commitments downward as inference economics remain unprofitable, the advanced node capacity that Intel and Samsung are building to attract customers like Apple could face a demand shortfall at exactly the moment those fabs reach production scale.

Apple’s supply chain pivot is a signal, not yet a shift

Apple is clearly motivated to diversify, and the policy environment is supportive. The manufacturing gap, however, is real. Yields at both Samsung and Intel remain below TSMC’s performance at the nodes Apple requires, and the 2nm exclusivity commitment locks flagship production to TSMC through at least the iPhone 18 launch cycle.

The market on 5 May priced possibility. Operational reality remains constrained by yield and scale gaps that are unlikely to close before 2027 at the earliest.

The investor question is not whether TSMC loses Apple. It is how quickly and at what volume Apple builds a credible alternative, and what that process does to the competitive dynamics and valuations of all four companies over a multi-year horizon. Supply chain diversification stories often move markets before they move manufacturing. The evidence to watch has been identified; the confirmation cycle has not yet begun.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. These forward-looking assessments are speculative and subject to change based on market developments and company performance.