Apple posted $111.2 billion in quarterly revenue, beat Wall Street on both headline metrics, and claimed the top spot in global smartphone shipments for the first time in an opening calendar quarter. The fiscal Q2 2026 Apple earnings report, released on 30 April 2026, arrived against a backdrop that should have made those numbers difficult: a global memory chip shortage compressing margins across the smartphone sector, Samsung delaying its flagship Galaxy S26, and overall shipments falling between 4% and 6% depending on the research firm. Apple moved the other direction. What follows is an analysis of what drove the record, what the memory chip crunch means for the broader industry, and whether the conditions that produced this quarter are durable or temporary.

A record quarter built on iPhones, but the numbers tell a more layered story

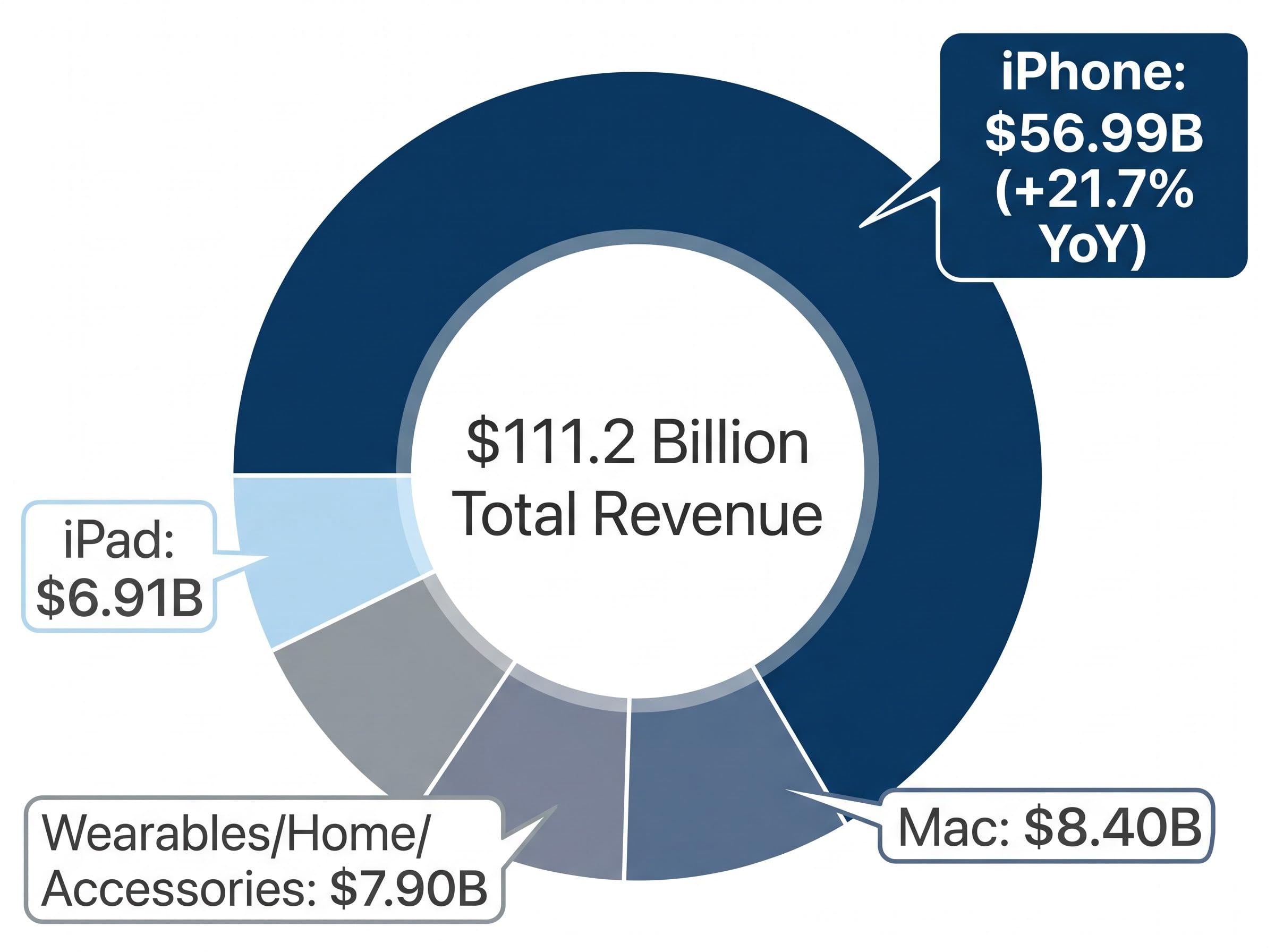

Apple reported earnings per share of $2.01 against a consensus estimate of $1.96, and revenue of $111.2 billion against a $108.9 billion consensus. Both beats were clean. But the structural story underneath is concentrated in a single segment.

iPhone revenue reached $56.99 billion, up 21.7% year on year. That figure carried the quarter. Without it, the remaining segments delivered solid but unremarkable growth:

- Mac revenue: $8.40 billion

- iPad revenue: $6.91 billion

- Wearables, Home, and Accessories revenue: $7.90 billion

Net income came in at $29.6 billion. Management authorised a $100 billion share repurchase programme, a signal of balance sheet confidence that aligns with forward guidance projecting 14-17% year-on-year revenue growth in Q3.

| Segment | Revenue | YoY Change |

|---|---|---|

| iPhone | $56.99B | +21.7% |

| Mac | $8.40B | — |

| iPad | $6.91B | — |

| Wearables/Home/Accessories | $7.90B | — |

The takeaway for investors tracking Apple: this was not a broad-based acceleration across the product portfolio. It was an iPhone quarter, and the durability of the result depends on whether that segment’s momentum holds through the memory supply crunch ahead.

When big ASX news breaks, our subscribers know first

The Factors Behind Apple’s Unprecedented Q1 Global Smartphone Share

Apple held 21% of global smartphone shipments in Q1 2026, according to Counterpoint Research, marking the first time in history the company has led shipments in any opening calendar quarter. The achievement is worth pausing on because Q1 has traditionally been Samsung’s strongest period, with new Galaxy launches and seasonal demand patterns favouring the Android ecosystem.

The gap was not narrow. Samsung fell to 20% share, down 6% year on year. Xiaomi dropped to 13%, absorbing a 13% shipment decline that hit its entry-level portfolio hardest. The broader market contracted to 289.7 million units shipped, down 4.1% year on year per IDC.

| Vendor | Market Share | YoY Shipment Change | Key Note |

|---|---|---|---|

| Apple | 21% | +5% | First-ever Q1 lead |

| Samsung | 20% | -6% | Galaxy S26 delayed |

| Xiaomi | 13% | -13% | Entry-level hit hardest |

Three operational decisions made this possible. Apple concentrated iPhone 17 Pro demand in the premium tier, where memory cost sensitivity is lower. Trade-in programme uptake accelerated upgrade cycles. And the company frontloaded inventory shipments to the US ahead of anticipated US-China tariff escalation, a move that simultaneously solved two problems: tariff exposure and memory component access.

China, India, and Japan: the geographic engine behind the share gain

Apple’s China market share reached approximately 19%, according to Reuters citing regional data, with analysts attributing the performance to trade-in programme strength and iPhone 17 demand. India and Japan served as additional growth contributors, extending the geographic base beyond the company’s traditional US and European strongholds. The combination of premium product concentration and geographic diversification suggests the share lead was structural rather than a single-product anomaly.

What a memory chip shortage actually means for smartphone economics

The global smartphone shipment decline did not happen in isolation. It traces directly to a supply-side decision made by memory chip manufacturers.

DRAM and NAND memory suppliers, the companies that produce the storage and processing memory in every smartphone, redirected manufacturing capacity toward AI data centre infrastructure during 2025 and into 2026. AI servers require far more memory per unit than consumer devices, and memory producers followed the higher-margin opportunity. The result was a supply shortfall for smartphone and consumer electronics manufacturers. Here is how that propagates through the industry:

- Memory suppliers shift capacity toward AI data centres

- DRAM and NAND supply tightens for consumer electronics

- Bill-of-materials (BOM) costs rise for smartphone manufacturers

- OEMs either absorb the cost (compressing margins) or pass it through to consumers as higher retail prices

- Entry-level and mid-range devices, where pricing sensitivity is highest, see the steepest volume declines

The impact was not uniform across the market. Premium-tier manufacturers like Apple, with pricing power and pre-secured supply agreements, absorbed the shock more effectively. Entry-level and mid-range producers bore the heaviest burden. Xiaomi’s 13% shipment decline, the steepest among top vendors, illustrates the point. Tariff-related BOM cost increases of 5-10% compound the pressure for manufacturers without comparable mitigation strategies.

Samsung disclosed that profitability in its mobile and network division is projected to decline in 2026, with the memory shortage expected to persist through late 2027.

For investors evaluating the smartphone sector, understanding which OEMs have built operational buffers against the shortage, and which remain structurally exposed, is the clearest lens for assessing relative positioning into 2027.

Samsung versus Apple: two responses to the same structural pressure

Samsung and Apple faced the same memory supply environment in Q1 2026. Their responses diverged sharply, and the results reflect the cost of each strategic bet.

Samsung delayed the Galaxy S26 launch, reduced its entry-level portfolio to protect margins, and raised consumer prices to offset BOM cost inflation. The outcome: 20% market share, down 6% year on year, with margin pressure expected to persist through the year. Xiaomi absorbed an even steeper 13% decline, confirming that the entry-level exposure Samsung partially shares was the quarter’s primary vulnerability.

Apple made three operational moves that Samsung did not:

- Secured memory component supply ahead of the shortage peak through proactive procurement

- Frontloaded inventory shipments to the US before tariff escalation, hedging both cost and availability risks simultaneously

- Concentrated the entire product mix in premium-only tiers, eliminating exposure to the entry-level margin compression that hit competitors hardest

Management disclosed that these tariff mitigation efforts offset approximately 2% of margin pressure that would otherwise have flowed through. The result: 21% market share, up 5% year on year, in a quarter where the broader market contracted.

Google and the outliers gaining ground in the disruption

The disruption created openings beyond the top two. Google recorded 14% shipment growth in mature markets, with AI and computational photography features cited as differentiators. Nothing posted 25% growth on the strength of its Phone (4a) launch. Neither represents a near-term threat to Apple’s position, but both illustrate that the supply disruption is reshuffling share at every tier.

Leadership transition, Apple Intelligence, and the revenue gap still to close

The quarterly numbers were clean. The strategic picture underneath them is less settled.

Tim Cook attributed approximately 20% of Services revenue growth in fiscal Q2 2026 to AI features integrated into iPhone 17, framing Apple Intelligence as a proven demand driver.

On the earnings call, Cook characterised AI as contributing approximately 20% of Services revenue growth in the quarter, positioning it as a material factor in iPhone 17’s demand performance.

That figure establishes something important: AI is already selling hardware. The unresolved question is whether Apple can convert that demand contribution into a durable, high-margin software revenue stream.

Approximately ten days before the earnings report, Apple announced that Cook would transition to a chairman role, with John Ternus named as incoming CEO. The succession adds a layer of strategic uncertainty to the AI monetisation timeline.

Three questions remain open:

- What monetisation model will Apple adopt: premium subscription tiers, bundled services, or a hybrid approach?

- When will a premium AI tier roll out, and at what pricing?

- How does Apple’s AI hardware integration compete with Google’s AI-driven shipment growth in mature markets?

The market’s initial reaction captured both the optimism and the uncertainty. AAPL rose as much as 5.35% in after-hours trading on 30 April, then reversed to approximately -1.3% in extended trading. The average analyst price target moved to approximately $303 post-earnings. Q3 guidance of 14-17% year-on-year revenue growth suggests management confidence, but the AI revenue gap between demand contribution and monetisation remains the most consequential open question for investors evaluating Apple’s premium valuation.

Apple’s record sets a high watermark, but the memory crunch will test whether it holds

The record is real. Apple posted historic revenue, claimed its first Q1 shipment lead, and demonstrated that supply chain positioning can be a competitive weapon in a constrained environment. The execution in fiscal Q2 2026 was genuine.

Several of the tailwinds that produced it, however, are either temporary or diminishing. Inventory frontloading is a one-time hedge. Competitor delays created a window that closes when the Galaxy S26 reaches market (early pre-order demand for the S26 Ultra has been described as strong). Tariff mitigation offsets require sustained operational effort.

Three forward-looking pressure points merit monitoring:

- Memory shortage persistence: expected to continue through late 2027, with no new capacity agreements announced

- Tariff risk: potential 5-10% BOM cost increase without continued mitigation measures

- AI monetisation progress: the gap between AI’s demonstrated demand contribution and a formalised revenue model remains unresolved

Q3 guidance implies approximately 15.5% year-on-year revenue growth at the midpoint, a strong figure that nonetheless assumes continued iPhone demand resilience in a tightening supply environment. Whether the Q1 market share lead holds or narrows will depend on the same structural variables that created it.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements, including management guidance and analyst price targets, are subject to change based on market conditions and various risk factors.