A fund charging 0.07% per year and a fund charging 0.93% per year can both receive a Bronze Morningstar Medalist Rating. Yet from April 2026, the gap between those fees directly determines which one might be upgraded to Gold and which one risks falling to Neutral. The methodology update, announced in December 2025 and rolled out through March and April 2026, introduced a formal Price Score that quantifies fee competitiveness relative to category peers and feeds it directly into the five-tier Gold, Silver, Bronze, Neutral, Negative designation system. For Australian investors evaluating ETFs and managed funds, the change is more than cosmetic. It reshapes which products carry the highest ratings on adviser platforms, comparison tools, and research portals. This article explains exactly how the Price Score works, why it carries more weight for index funds than for active strategies, what the scoring formula produces in practice, and what the update means for anyone using the Medalist Rating to assess funds listed on the ASX.

The rating system behind the medal: what the Morningstar Medalist Rating actually measures

The Medalist Rating is a forward-looking assessment. It evaluates a fund’s probability of outperforming its category benchmark over a full market cycle, not its recent track record. That distinction matters: the rating is not a reward for past returns but a projection of whether a fund is structured to deliver competitive results after fees over time.

Three analytical pillars have historically formed the core of the assessment:

- People: The quality and stability of the investment team managing the fund

- Process: The coherence and repeatability of the investment strategy

- Parent: The governance, culture, and stewardship record of the asset manager

The rating applies to both managed funds and ETFs available to Australian investors, including those listed on the ASX. Its five-tier scale communicates a clear signal:

The Medalist Rating applies equally to both managed funds and ETFs listed on the ASX, and readers new to the structure of these products will find that ASX ETF basics cover important distinctions in how units are created, redeemed, and priced relative to the underlying basket of securities.

- Gold: High conviction that the fund will outperform its benchmark after fees over a full cycle

- Silver: Strong conviction in benchmark outperformance after fees

- Bronze: Moderate conviction in benchmark outperformance after fees

- Neutral: Roughly even odds of matching or modestly underperforming the benchmark

- Negative: Material barriers to delivering competitive long-term returns

What changed in April 2026

The December 2025 announcement introduced the Price Score as a fourth input, formalising what had previously been an implicit consideration: how a fund’s fees compare to those of its category peers. The phased rollout through March and April 2026 means the effects are now visible across Australian fund ratings. The following sections explain the mechanics in full.

When big ASX news breaks, our subscribers know first

How the Price Score works: the formula, the scale, and what it actually measures

The Price Score is a single number between -2.5 and +2.5. A fund at the cheapest end of its category scores near +2.5. A fund at the most expensive end scores near -2.5. The foundation of the metric is peer-relative comparison: it benchmarks a fund’s fees against the median fee of comparable funds in the same investment category, not against an absolute standard.

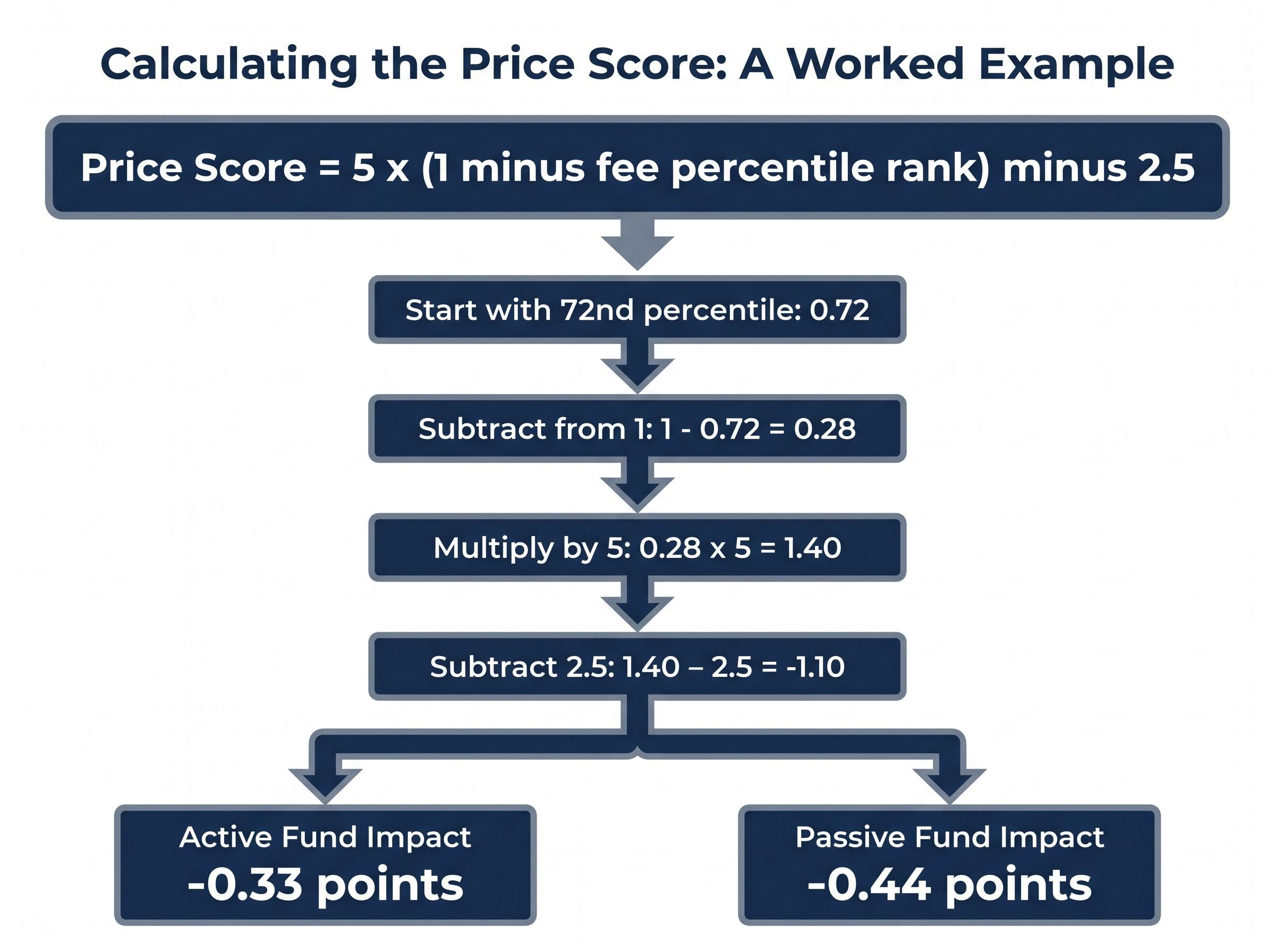

The Formula: Price Score = 5 x (1 minus fee percentile rank) minus 2.5

The scale is continuous, not bucketed, meaning even marginal fee differences that compound over a long investment horizon are captured. Here is how the formula works in practice, using a fund ranked at the 72nd percentile for fees (meaning 72% of peers charge less):

- Start with the fee percentile rank: 0.72

- Subtract from 1: 1 minus 0.72 = 0.28

- Multiply by 5: 0.28 x 5 = 1.40

- Subtract 2.5: 1.40 minus 2.5 = -1.10

That fund receives a Price Score of -1.10, placing it on the costly side of its peer group. The consequence of that score differs depending on whether the fund is active or passive: it reduces an active fund’s overall rating by 0.33 points and a passive fund’s rating by 0.44 points.

The table below illustrates how the formula distributes scores across the peer group:

| Fee Percentile Rank | Price Score |

|---|---|

| 10th (cheaper than 90% of peers) | +2.00 |

| 30th (cheaper than 70% of peers) | +1.00 |

| 50th (category median) | 0.00 |

| 72nd (more expensive than 72% of peers) | -1.10 |

| 90th (more expensive than 90% of peers) | -2.00 |

For investors who have long struggled to determine whether a fund’s fee is genuinely competitive, the Price Score provides an answer grounded in peer comparison rather than intuition.

Why passive funds feel the Price Score more than active ones

For an index-tracking strategy, the fund’s entire purpose is to replicate a benchmark as closely as possible. Security selection is not the value proposition; precision and low cost are. The management fee becomes one of the very few variables an investor can control and a manager can meaningfully influence. Under that logic, weighting fees heavily in the rating makes analytical sense.

Active funds operate under a different thesis. The claim is that manager skill in security selection can generate returns that offset higher fees. It is analytically reasonable, then, to weight pricing somewhat lower while still treating it as a material factor.

The weighting figures reflect this distinction:

- Passive funds: the Price Score carries a 40% weighting in the overall Medalist Rating

- Active funds: the Price Score carries a 30% weighting

For passive funds, the Price Score is the single largest input in the rating calculation, exceeding any individual pillar.

The asymmetric weighting does not exempt active funds from fee scrutiny. A Price Score of -1.10 still reduces an active fund’s overall Medalist Rating by 0.33 points, enough to push a borderline Bronze fund down to Neutral.

| Factor | Passive Funds | Active Funds |

|---|---|---|

| Price Score weighting | 40% | 30% |

| Rating impact of a -1.10 score | -0.44 points | -0.33 points |

| Rationale | Fee is the primary controllable variable; no alpha thesis to offset cost | Manager skill thesis justifies partial offset, but fees remain material |

For Australian ETF investors, this weighting structure explains why low-fee index products have seen the most dramatic rating upgrades since April 2026.

The Price Score in practice: what it means for Australian ETFs and managed funds

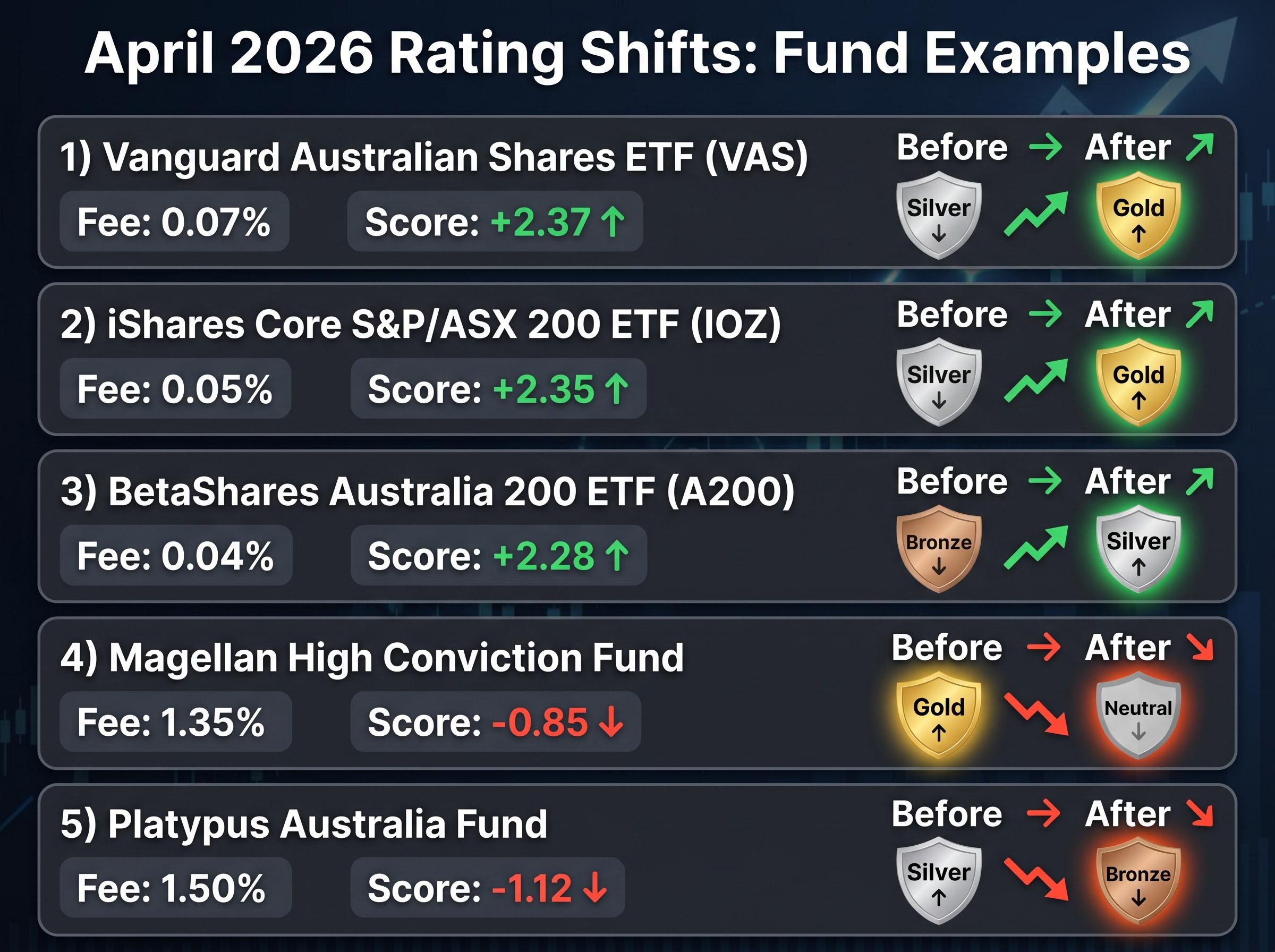

The Vanguard Australian Shares ETF (VAS) provides the clearest illustration. Its management fee of 0.07% sits against a category median of 0.93%, producing a Price Score of +2.37, near the top of the scale. That score was sufficient to move VAS from a Silver to a Gold Medalist Rating.

The pattern repeats across low-fee products. iShares Core S&P/ASX 200 ETF (IOZ), with a management fee of 0.05%, holds a Gold rating as of April 2026. BetaShares Australia 200 ETF (A200), which cut its fee to 0.04% (as of May 2026), was upgraded from Bronze to Silver with a Price Score of +2.28.

| Fund/ETF | Fee | Price Score | Pre-Update Rating | Post-Update Rating |

|---|---|---|---|---|

| Vanguard Australian Shares ETF (VAS) | 0.07% | +2.37 | Silver | Gold |

| iShares Core S&P/ASX 200 ETF (IOZ) | 0.05% | +2.35 | Silver | Gold |

| BetaShares Australia 200 ETF (A200) | 0.04% | +2.28 | Bronze | Silver |

| Magellan High Conviction Fund | 1.35% | -0.85 | Gold | Neutral |

| Platypus Australia Fund | 1.50% | -1.12 | Silver | Bronze |

Approximately 15% of rated Australian funds were affected by the methodology change overall, with passive ETFs seeing net upgrades and higher-fee active funds experiencing net downgrades.

Active funds under pressure

The Magellan High Conviction Fund, with a management fee of 1.35%, moved from Gold to Neutral. Its Price Score of -0.85 created a headwind that the fund’s People, Process, and Parent pillar scores could not fully offset. The Platypus Australia Fund, charging 1.50% against a category median of approximately 0.95%, dropped from Silver to Bronze with a Price Score of -1.12.

These downgrades reflect a structural headwind rather than a performance judgement. The pillar assessments for these funds did not necessarily deteriorate; the new fee metric simply formalised a cost penalty that was previously implicit.

Why fees predict performance, and what the Price Score formalises

The Price Score rests on an empirical foundation rather than an editorial preference. Multiple studies, including Morningstar’s own research, have consistently identified fund fees as one of the most reliable predictors of future investment outcomes across fund categories.

The reasoning is straightforward:

Active versus passive performance data from Australia’s own fund universe reinforces the empirical foundation the Price Score draws on: approximately 88% of active global equity funds in Australia failed to beat their benchmarks over 15 years, a finding that helps explain why Morningstar now weights fees at 30-40% of the overall Medalist Rating.

- Annual drag: Fees are charged every year regardless of market performance, creating a guaranteed headwind to returns

- Compounding effect: A seemingly small difference between 0.07% and 0.93% amounts to 0.86% per year; over a decade or more, that gap compounds into a substantial return difference

- No alpha offset for passive strategies: Index funds, by design, cannot generate excess returns to compensate for higher fees

- Peer-relative cost position: A fee that looks modest in isolation may be expensive relative to peers offering comparable exposure in the same category

The annual fee difference between the cheapest and most expensive peers in the same category can erode years of investment gains over a long horizon.

ASIC’s Moneysmart fee guidance quantifies how even small annual cost differences compound into materially different outcomes for Australian investors over a 10-20 year horizon, providing a regulatory-backed frame for evaluating whether a fund’s fees represent genuine value.

The practical challenge the Price Score addresses is one of scale. With hundreds of ETFs now listed on the ASX, evaluating each fund’s fee in isolation is difficult. An investor might use an informal personal rule, such as excluding products above 0.25% per annum total cost ratio, as a screening heuristic. The Price Score replaces that kind of rough filter with a precise, category-relative measurement embedded directly into the rating system.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

What this means for Australian investors evaluating funds today

The Price Score is best treated as a diagnostic tool. A strong positive score confirms that a fund’s fees are competitive within its category. A negative score signals that the fund needs to justify its cost through demonstrably superior People, Process, or Parent pillar scores to maintain a positive overall rating.

The cheapest fund in a category does not automatically receive the highest overall rating. A fund with a Price Score of +1.8 but weak People and Process assessments can still receive a Neutral or Negative designation. The overall Medalist Rating requires reading all pillar scores in context.

When reviewing a fund’s rating under the new methodology, consider the following steps:

The Price Score is one input in a broader managed fund due diligence process; readers applying a structured approach to fund selection will also need to review the Product Disclosure Statement, verify the manager’s AFS licence, and assess redemption and liquidity terms before committing capital.

- Check the Price Score to understand whether the fund’s fee is an advantage or a headwind relative to category peers

- Review individual pillar scores (People, Process, Parent) to see whether the rating is driven by fee advantage or by conviction in the investment team and strategy

- Compare against category peer ratings to assess whether similarly priced funds carry higher or lower overall designations

- Consider the scale of the fund manager, recognising that large providers such as Vanguard, BetaShares, and iShares benefit structurally from economies of scale that support ultra-low fees

Where the Price Score has limits

Large providers are structurally advantaged by the Price Score. Their scale supports fees that smaller or newer fund managers cannot match, regardless of investment quality. SMSF trustees and investors comparing managed funds should factor this in when evaluating emerging or niche strategies.

A high Price Score alone does not guarantee a positive overall rating. The Financial Advice Association Australia (FAAA) has flagged a related concern: the methodology could drive unintended herding toward lowest-fee homogeneity in active fund categories, potentially reducing the diversity of active strategies available to Australian investors.

The Price Score as a signal, not a verdict

Before April 2026, fees influenced Medalist Ratings indirectly through their effect on outperformance probability. Now, the Price Score makes that influence explicit, quantified, and category-relative.

The methodology does create a genuine tension. Weighting fees at 30-40% of the overall rating places structural pressure on active managers, and whether that pressure improves or reduces the quality of active strategies available to Australian investors remains an open question as the system matures.

Fees were always a factor in Medalist Ratings. The Price Score is the first time they have been given a precise, published, category-relative score that directly determines rating outcomes.

The broader context reinforces the shift. Fee compression in the Australian ETF market continues to accelerate: large-cap equity ETF average management expense ratios sat around 0.15% in 2025-2026, down from approximately 0.20% previously. The BetaShares A200 fee of 0.04% as of May 2026 marks how far that compression has gone. The Price Score is both a product of this trend and, through its influence on ratings and platform visibility, an accelerant of it.

The Medalist Rating still requires interpretation across all its components. What has changed is that fee competitiveness can no longer be overlooked or underweighted in that interpretation. For Australian investors, that clarity is the update’s most durable contribution.

For investors wanting to understand how the broader shift toward low-cost index products is reshaping what Australian retail portfolios actually look like, our deep-dive into Australian ETF portfolio trends for 2026 examines asset allocation data by generation, inflow patterns across domestic and international categories, and the behavioural tensions between long-term accumulation and reactive trading that emerge during volatile markets.