Why Governance and Communication Drive Post-IPO Value

2 hrs ago

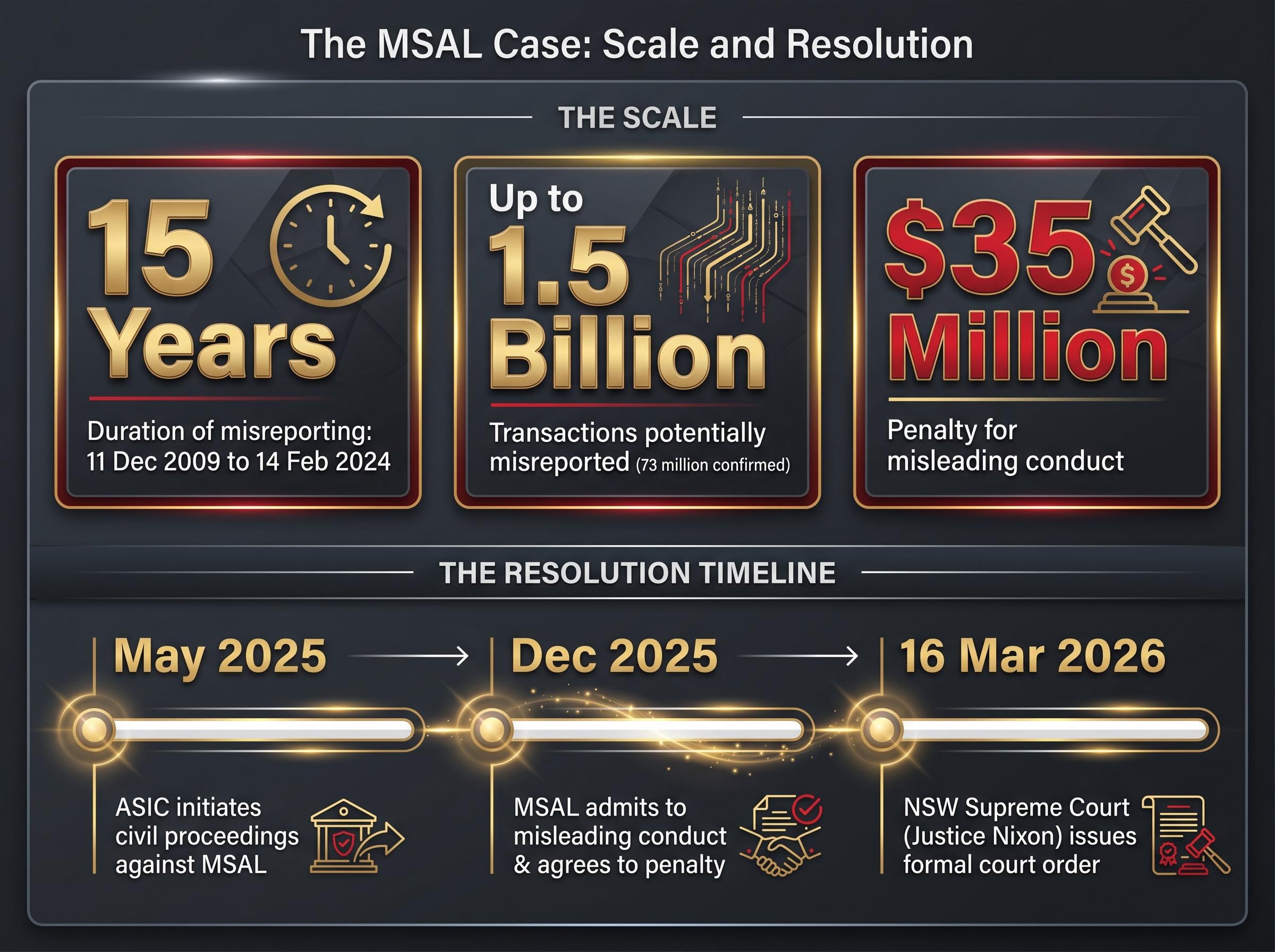

Between December 2009 and February 2024, Macquarie Securities Australia Limited filed short sale reports that were wrong, potentially up to 1.5 billion times. The NSW Supreme Court’s March 2026 ruling, imposing a $35 million penalty, made one thing clear: in Australian markets, the data behind short selling is not a back-office formality.

Short selling is a legal, widely used investment strategy in Australia. It operates inside a regulatory architecture that depends entirely on accurate, timely reporting. When that reporting fails, the consequences extend well beyond the firm responsible, affecting market surveillance, investor sentiment signals, and public trust in the integrity of price discovery.

This article explains what short selling is, how Australia’s reporting rules work, why the accuracy of that data matters far beyond compliance checklists, and what the MSAL case reveals about the real cost of getting it wrong.

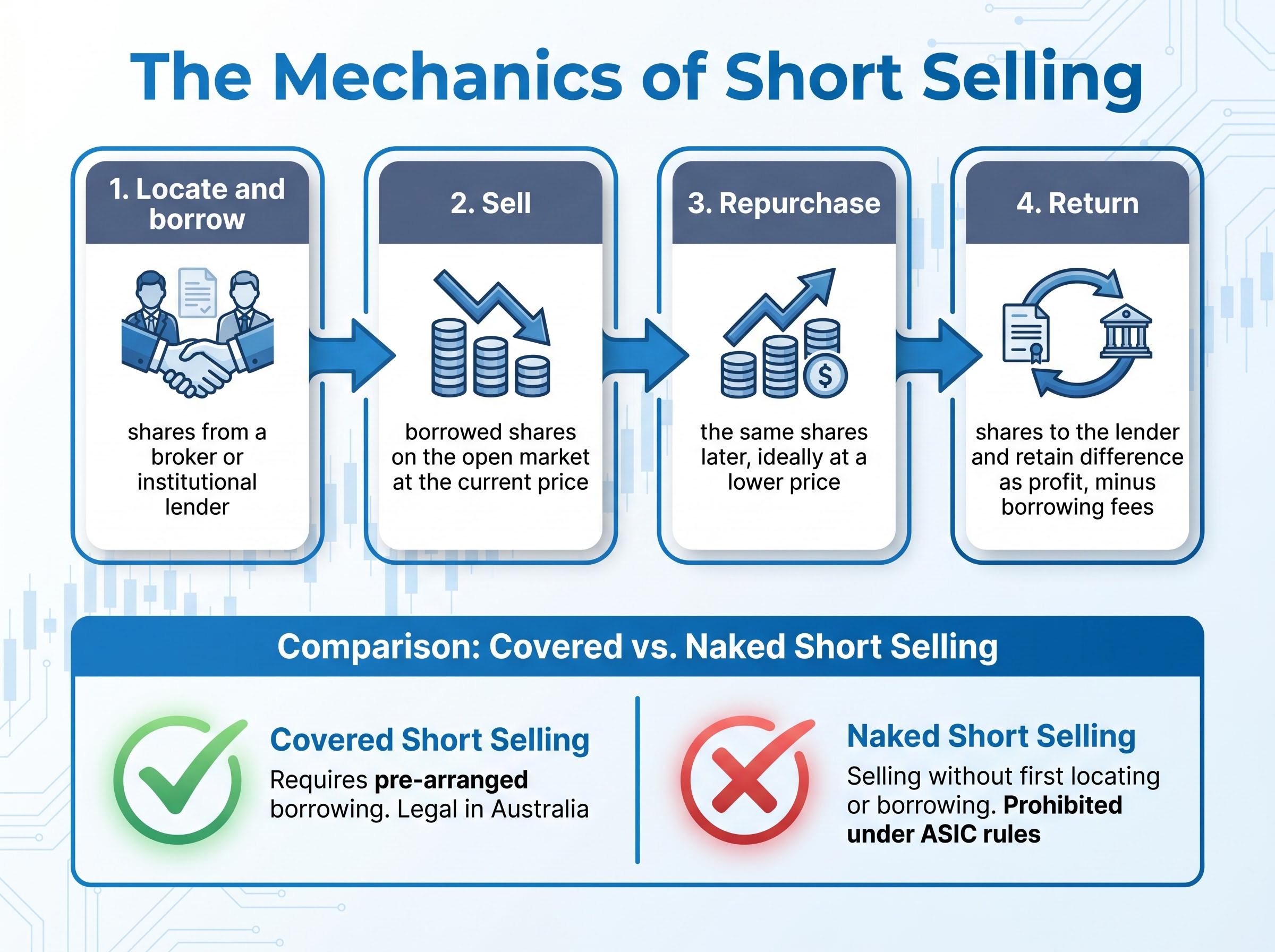

Short selling starts with a counterintuitive premise: it is possible to profit when a stock falls. Where conventional investing relies on buying low and selling high, short selling reverses the sequence. A short seller sells shares they do not own, borrowed from a broker, with the intention of repurchasing them later at a lower price.

The mechanics follow a four-step sequence:

Not all short selling is treated equally under Australian law. The distinction between covered and naked short selling is the foundation of the entire regulatory framework:

Retail investors who wish to short sell must hold a margin account with an ASIC-licensed broker and comply with all covered short requirements.

Retail investors who wish to short sell must hold a margin account with an ASIC-licensed broker, and the mechanics of margin lending in Australia sit at the centre of that requirement: variable rates now exceeding 10% per annum mean leveraged positions must generate consistently strong returns before any net benefit is realised.

The risk profile of short selling is fundamentally asymmetric. On a long position, the worst possible outcome is losing the amount invested; a stock can only fall to zero. On a short position, there is no ceiling. A stock price can theoretically rise without limit, meaning losses on a short trade are theoretically unlimited.

The unlimited loss distinction is the single most important risk factor for retail investors considering short selling. A stock purchased for $10 can only lose $10 per share. A stock shorted at $10 can rise to $50, $500, or higher, and the short seller remains obligated to buy it back.

That asymmetry attracts regulatory attention for good reason. A short squeeze, where rising prices force short sellers to buy urgently, can accelerate a stock’s climb and compound losses across multiple participants simultaneously. Margin calls add further pressure: brokers require additional funds when losses exceed the margin threshold, and failure to meet those calls triggers forced position closures.

Borrowing costs also erode returns. Even when the directional bet is correct, the fees paid to borrow shares reduce the net profit on every trade.

Short selling does, however, serve legitimate market functions. Portfolio managers use short positions to hedge long holdings against sector-wide declines. Short sellers also contribute to price discovery by identifying overvalued securities. During the COVID-19 period, ASIC monitored elevated short interest in discretionary retail stocks on the ASX, where short selling activity helped signal weakening fundamentals before earnings confirmed the trend.

Short sellers also contribute to price discovery by identifying overvalued securities, and tracking the most shorted ASX stocks has emerged as an early warning tool for retail investors: institutional participants built positions in Lotus Resources and Generation Development Group weeks before both stocks fell sharply, with short interest signalling the deteriorating outlook before earnings confirmed it.

| Strategy | Profits from | Maximum loss | Australian regulatory notes |

|---|---|---|---|

| Long (buy) position | Price increase | Amount invested | Standard; no special reporting |

| Short selling | Price decrease | Theoretically unlimited | Must be covered; daily reporting required |

| Put options | Price decrease | Premium paid | Separate derivatives framework |

Australia’s reporting regime was not designed to generate paperwork. It was designed to generate market intelligence. Every short sale report filed by a market participant feeds into the aggregate data that ASIC uses for surveillance, that portfolio managers use for sentiment analysis, and that retail investors can access freely through public dashboards.

The regulatory architecture rests on several layers. ASIC Regulatory Guide 196 (RG 196), last substantively revised in 2018, provides the principal framework for short sale disclosure obligations. ASX Operating Rule 7.11 governs on-market short sale reporting for ASX-listed securities, while Cboe Australia’s Chapter 9 rules provide the equivalent framework for Cboe-listed securities. The legislative foundation sits in the Corporations Act 2001.

ASIC Regulatory Guide 196 sets out the covered short selling framework that applies to all ASX and Cboe-listed securities, including the prohibition on naked short selling, the real-time order tagging requirement, and the aggregate reporting obligations that feed public dashboards.

The reporting timeline is tight. Daily aggregate short sale data must be submitted by T+1 at 9:30 AM AEST through ASX and Cboe portals. Individual orders must be tagged in real time at the point of trade execution.

What distinguishes Australia’s system from international peers is its granularity. There is no minimum position threshold for reporting. All on-market short sales must be disclosed regardless of size, making the Australian regime more transaction-granular than either the US or UK systems.

| Aspect | Australia | US | UK |

|---|---|---|---|

| Daily reporting | All on-market shorts; T+1 aggregate | Daily to FINRA (private); weekly public aggregates | Daily to FCA for significant positions |

| Position thresholds | No minimum; all reportable | No position reporting minimum; 0.5% for close-out rules | 0.2% net short position triggers public disclosure |

| Public disclosure | Weekly ASX/Cboe dashboards (free) | Bi-monthly short interest (settlement-based) | Daily net short positions above 0.5% published on FCA site |

| Structural focus | Transaction-focused; granular | Position-oriented; fails-to-deliver emphasis | Position-based with rapid public transparency |

Aggregated data flows from ASX and Cboe portals into weekly public dashboards, freely accessible to anyone. Retail investors can use this data to observe which stocks carry elevated short interest and draw inferences about market sentiment, whether institutional participants are positioning for price declines in specific sectors or individual securities.

Retail investors can use this data to observe which stocks carry elevated short interest and draw inferences about market sentiment, and current ASX short interest data as of late April 2026 shows Telix Pharmaceuticals carrying the highest short position on the exchange at 16.10%, with Generation Development Group and Lotus Resources posting the sharpest weekly buildups across the reporting period.

Individual trader positions are not disclosed. The public data is aggregate-level, showing total short sale volumes rather than the identities or positions of specific participants.

The mechanics of reporting are one thing. What happens when reporting goes wrong is another entirely.

ASIC uses aggregate short sale data as a live surveillance input. It is one of the tools the regulator relies on to detect unusual activity, monitor volatility risks, and identify patterns consistent with potential market manipulation. The ASIC Corporate Plan 2025-26, published 27 August 2025, identifies short selling under market integrity priorities, with short sale data specifically flagged as a tool for detecting volatility risks.

Investors and portfolio managers also rely on public short interest data to interpret sentiment. When the aggregate figures are wrong, the signals they generate are systematically misleading. A stock that appears lightly shorted may in reality carry significant short interest, or vice versa.

The downstream consequences of inaccurate data compound across every user of the system:

The MSAL case brought this chain of consequences into sharp relief. MSAL acknowledged during NSW Supreme Court proceedings that its inaccurate reporting caused potential disruption to ASX and Cboe markets.

“MSAL acknowledged that inaccurate data could mislead traders, investors, companies, regulators, and the general public.”

Between 298 million and 1.5 billion MSAL transactions were potentially misreported across the relevant period, with a minimum of 73 million short sales confirmed incorrectly reported.

The scale of the MSAL case is difficult to overstate. Misreporting ran from 11 December 2009 to 14 February 2024, a period spanning more than 15 years during which multiple internal reviews failed to detect the problem. This was not a single coding error or one quarter of faulty data. It was a systemic failure that compounded with every passing year.

The case progressed through three stages:

This was ASIC’s first major enforcement action specifically targeting short sale misreporting. The fact that the first case involved violations spanning more than a decade underscored just how long systemic failures can persist undetected when internal controls are inadequate.

ASIC enforcement penalties issued through the Federal Court have followed a consistent calibration logic in 2026: the $10 million penalty against Binance Australia Derivatives for retail client misclassification, handed down just weeks before the MSAL ruling, applied the same general deterrence framing that Justice Nixon used in sizing the $35 million short sale penalty.

Risk management analysis published by Protecht Group on 10 April 2026 catalogued the root causes:

In addition to the $35 million penalty, MSAL was required to retain an independent expert to review its short sale and regulatory reporting systems. The court also ordered MSAL to pay ASIC’s legal costs.

Justice Nixon explicitly framed the $35 million penalty around general deterrence. The ruling was not sized solely to punish MSAL; it was calibrated to set a standard for all market participants. The message was that systemic, long-duration reporting failures will attract penalties proportionate to their market impact, not merely to the cost of the compliance failure itself.

The court found that MSAL engaged in misleading conduct, a finding that carries weight beyond technical non-compliance. Misleading conduct carries reputational consequences and signals to other firms that inadequate reporting infrastructure is not a defensible position.

Industry analysis following the ruling anticipates that ASIC may push for RG 196 updates requiring automated real-time validation, though no confirmed consultation had been announced as of May 2026.

ASIC’s post-ruling position, consistent with the Corporate Plan 2025-26, is that all market participants must ensure their systems, controls, and governance frameworks are sufficiently robust to meet reporting obligations continuously, not just at point of implementation.

ASIC expects that systems and governance frameworks are “sufficiently robust to meet regulatory obligations.”

The MSAL case has shifted industry expectations. Compliance professionals have identified three categories of action that firms should prioritise in response:

The reactive nature of ASIC’s current enforcement model means firms cannot assume that the absence of regulatory inquiry signals compliance. MSAL’s misreporting persisted for 15 years before proceedings were initiated.

For retail investors, the practical takeaway is direct. The short interest data visible on ASX and Cboe dashboards is only as reliable as the firm-level reporting that feeds it. Enforcement of reporting obligations is not an abstract regulatory concern; it is a retail investor protection issue. When the data is wrong, every investor reading the public dashboards is working from a distorted picture.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Short selling is a legal, valuable market function in Australia when conducted within the covered short framework and supported by accurate reporting. The strategy contributes to price discovery, supports hedging, and provides a counterweight to speculative overvaluation.

The chain of dependency is straightforward. Accurate firm-level reporting feeds aggregate public data. That aggregate data informs investor decisions, regulator surveillance, and market confidence. When one link breaks, as it did across 15 years of MSAL misreporting, the entire chain is compromised.

The $35 million penalty and court-ordered independent review have recalibrated what the industry understands as acceptable. The next phase of regulatory activity will test whether that message has landed across the sector.

Retail investors seeking to track short interest can access ASIC’s freely available public dashboards on the ASX and Cboe Australia websites. Those wanting to understand the specific obligations that apply to licensed market participants can consult ASIC’s Regulatory Guide 196 directly.

Forward-looking statements regarding potential regulatory changes are speculative and subject to change based on ASIC’s future consultation outcomes and policy decisions.

Short selling is a legal investment strategy where a trader borrows shares and sells them on the open market, intending to repurchase them later at a lower price and return them to the lender, keeping the price difference as profit minus borrowing fees.

Covered short selling requires the seller to have pre-arranged borrowing of securities before executing the sale and is legal in Australia, while naked short selling involves selling securities without first locating or borrowing them and is prohibited under ASIC rules due to settlement risk.

Under ASIC Regulatory Guide 196, all on-market short sales must be tagged in real time at execution and daily aggregate data submitted by T+1 at 9:30 AM AEST through ASX and Cboe portals, with no minimum position threshold, making Australia's regime more granular than equivalent US or UK systems.

Macquarie Securities Australia Limited filed inaccurate short sale reports between December 2009 and February 2024, with between 298 million and 1.5 billion transactions potentially misreported, resulting in a $35 million penalty imposed by the NSW Supreme Court in March 2026 following ASIC civil proceedings.

The short interest data visible on public ASX and Cboe dashboards is only as reliable as the firm-level reporting that feeds it, meaning inaccurate reporting distorts market sentiment signals and causes every investor reading those dashboards to base decisions on a misleading picture of actual short positions.