Three ASX stocks now carry short interest above 14%, with Telix Pharmaceuticals attracting more bearish institutional positioning than any other company on the exchange. Short selling data published by Market Index on 4 May 2026, covering the week to 28 April 2026, reveals a market where pharmaceutical and consumer discretionary names dominate the most shorted list, while oil, gas, and gold miners saw meaningful short covering. The data reflects positions as of 28 April but carries a four-business-day reporting lag under ASIC’s mandatory disclosure rules. What follows is the full top-ten ranking, the week-on-week and month-on-month shifts driving the biggest moves, and what the data signals about institutional sentiment heading into May.

Telix, Domino’s and Polynovo hold the top three positions

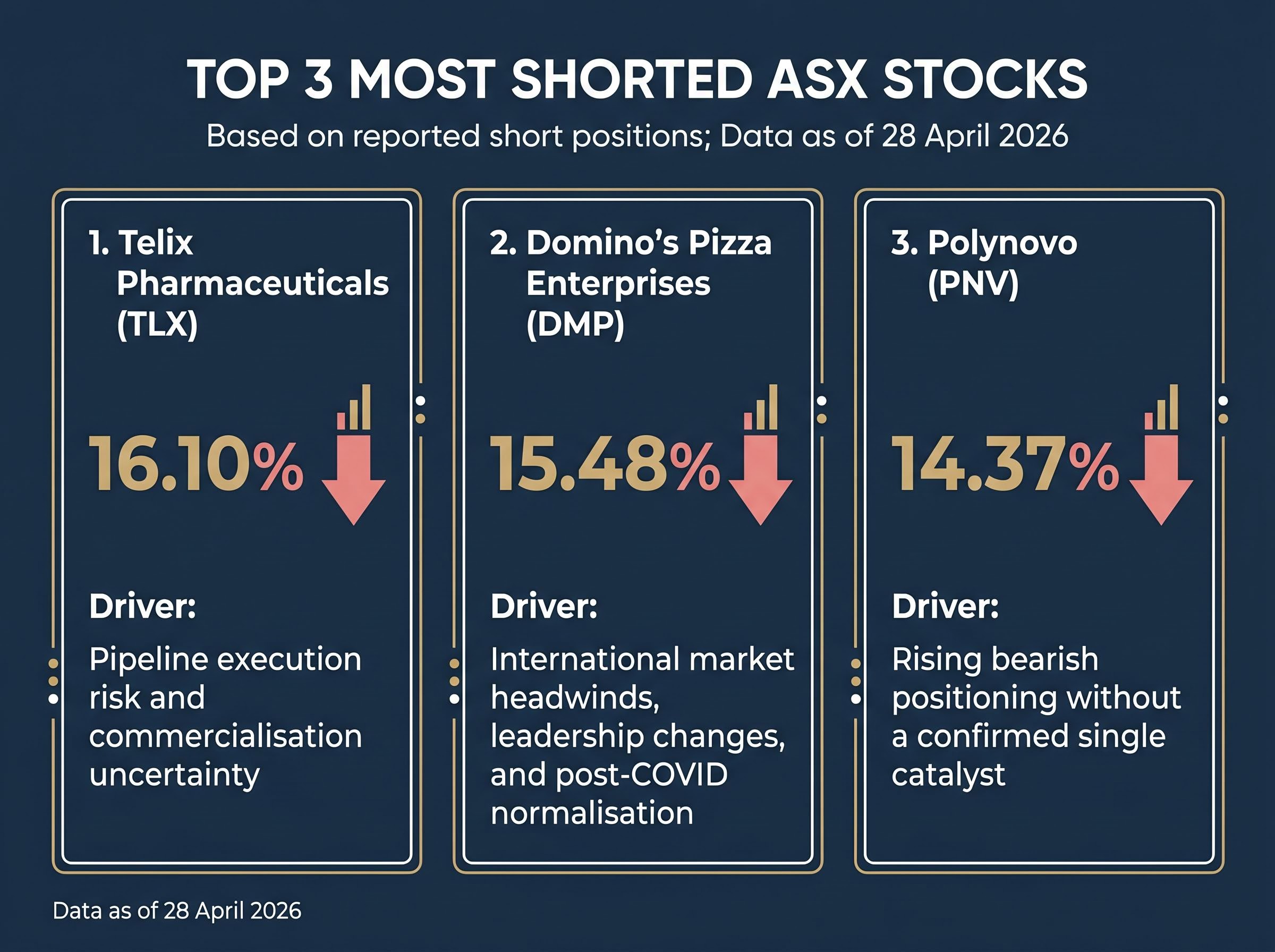

Telix Pharmaceuticals (TLX) holds the number-one position with 16.10% short interest, the highest of any ASX-listed stock as of 28 April 2026.

That figure dipped just 0.06% week-on-week but has climbed 2.35% over the past month, up from approximately 11.10% at the start of the calendar year. The trajectory suggests building institutional conviction rather than a one-off spike.

Domino’s Pizza Enterprises (DMP) sits second at 15.48%, slipping 0.07% for the week and 0.54% for the month. Shares remain down roughly 80% from COVID-era peaks and approximately 34% over the past year.

Polynovo (PNV) rounds out the top three at 14.37%, and unlike DMP, the direction is moving against the company. Short interest rose 0.29% week-on-week and 1.59% month-on-month, positioning PNV as the stock where bearish bets are actively expanding.

| Stock | Short Interest (%) | Week-on-Week Change (%) | Month-on-Month Change (%) |

|---|---|---|---|

| TLX | 16.10 | -0.06 | +2.35 |

| DMP | 15.48 | -0.07 | -0.54 |

| PNV | 14.37 | +0.29 | +1.59 |

| TWE | 13.24 | +0.27 | -1.41 |

| GYG | 12.08 | -1.81 | -1.41 |

| ZIP | 11.76 | -0.14 | +4.35 |

| FLT | 11.68 | -0.77 | +2.00 |

| LOT | 11.54 | +0.53 | +5.67 |

| CAR | 9.89 | +0.64 | +5.30 |

| GDG | 9.40 | +1.99 | +4.75 |

When big ASX news breaks, our subscribers know first

What is driving short interest in the top-ranked stocks

The numbers tell part of the story. The thesis behind each position fills in the rest.

TLX‘s short interest has climbed from roughly 11.10% to 16.10% since the start of 2026. The bearish positioning does not appear to be a revenue story; the company reported strong FY2025 figures. Instead, institutional scepticism centres on execution risk in its radiopharmaceutical pipeline and uncertainty around the commercialisation trajectory at scale.

Telix’s FY2025 revenue figures showed US$804 million at the full-year mark, with 46% Q4 growth driven by the Gozellix launch and 19 European marketing authorisations, a commercial track record that makes the bear case almost entirely dependent on whether the therapeutic pipeline delivers.

DMP‘s persistent position near the top of the table reflects concerns about international market execution, a leadership overhaul, and ongoing post-COVID normalisation pressures in discretionary food spending. With shares down approximately 34% over the past year, bears continue to question whether a sustained recovery is achievable.

PNV‘s rising short interest sits in the medical devices and wound care segment. No single confirmed catalyst has publicly emerged to explain the buildup; bears appear to be building positions into the stock’s current valuation without a clear event trigger.

- TLX: Pipeline execution risk and commercialisation uncertainty despite strong revenue

- DMP: International market headwinds, leadership changes, and post-COVID normalisation

- PNV: Rising bearish positioning without a confirmed single catalyst

Treasury Wine Estates (TWE), the next name in the table at 13.24%, reported a $649.4 million net loss for H1 FY2026 and suspended its interim dividend, providing clear fundamental context for sustained bearish conviction.

The biggest weekly movers: where short interest surged and where it covered

Two distinct movements played out in the same week. In one corner, bearish positioning accelerated sharply into several names. In the other, short sellers retreated from commodity-linked stocks.

Where short interest rose most sharply

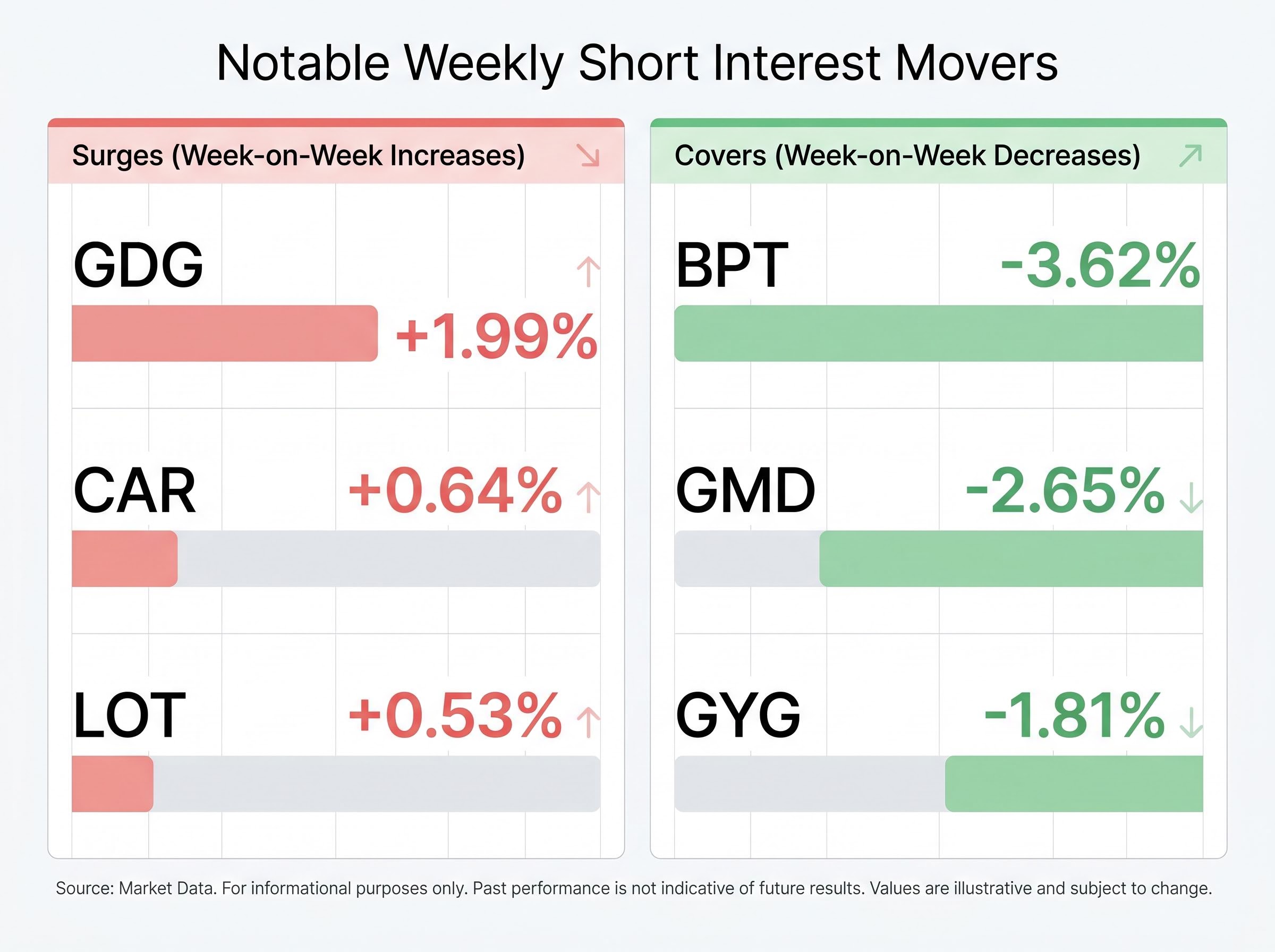

Generation Development Group (GDG) delivered the most striking move. Short interest climbed from approximately 4% in late March to 9.40% by 28 April 2026, a rise of 1.99% for the week alone and 4.75% for the month. The buildup followed a 22.6% single-session share price drop on 22 April 2026, despite the company reporting funds under management (FUM) of $34.8 billion at end of the March quarter, representing 0.8% quarterly growth.

Lotus Resources (LOT) carries 11.54% short interest, up 0.53% for the week and 5.67% for the month. On 30 April 2026, a fire-related production halt at its Kayelekera uranium mine caused the share price fall. Shares fell 34% on that day.

Zip Co (ZIP) sits at 11.76%, with a monthly increase of 4.35%, and 4DMedical (4DX) rose to 5.31% on a 5.01% monthly climb.

- GDG: +1.99% weekly, +4.75% monthly; shares fell 22.6% on 22 April

- LOT: +0.53% weekly, +5.67% monthly; data retraction event on 30 April

- ZIP: +4.35% monthly

- 4DX: +5.01% monthly

Where short sellers covered their positions

The resource sector saw the week’s most pronounced covering activity.

The same-week 52-week highs data shows the mirror image of this covering activity: lithium and materials names including Liontown Resources, Pilbara Minerals, and Mineral Resources hit new annual highs, with lithium carbonate averaging $15,000 per tonne in April 2026 providing the fundamental basis for a sector-level divergence from the bearish positioning concentrated in healthcare and consumer names.

Beach Energy (BPT) recorded the largest single-week short cover in the oil and gas segment, falling 3.62% week-on-week to 4.89%. Genesis Minerals (GMD) dropped 2.65% weekly to 2.93%, while PLS Group (PLS) eased 1.31% to 5.49% and Cochlear (COH) fell 1.06% to 4.66%.

Guzman y Gomez (GYG) also saw covering, with short interest declining 1.81% week-on-week to 12.08%. The covering appeared tied to a 36% share price surge between 2 and 10 April 2026, following Q3 Australian comparable sales growth of 6.6% against an estimated 5.1%.

- BPT: -3.62% weekly

- GMD: -2.65% weekly

- PLS: -1.31% weekly

- COH: -1.06% weekly

- GYG: -1.81% weekly

How to read ASX short selling data: what the numbers actually mean

Short interest is expressed as a percentage of a company’s issued shares held in short positions by institutional investors and hedge funds. A figure of 16.10%, as seen with TLX, implies that a meaningful share of the company’s stock is being borrowed and sold by institutions expecting the price to fall.

The data carries a built-in delay. The process works as follows:

- A short trade is executed on the ASX.

- The trade is reported to ASIC within three business days, as required under mandatory disclosure rules.

- ASIC publishes the aggregated data, which reaches platforms like Market Index with a four-business-day lag.

ASIC’s short selling disclosure rules require holders of net short positions above the relevant threshold to report those positions within three business days of the trade, with aggregated data published on a four-business-day lag, which is why the 4 May release captures positions only as of 28 April.

This means data published on 4 May 2026 reflects positions as of 28 April 2026. Any event occurring after that date, such as the LOT data retraction on 30 April, will not appear until the following week’s release.

High short interest reflects institutional bearish conviction. It does not guarantee a price decline. Positions can be held for months, and short sellers can be wrong. Rapidly building short interest, such as GDG‘s doubling in weeks, warrants monitoring rather than immediate action.

Resources for verifying short data include ASIC’s short position reports and ShortMan.com.au, which provides days-to-cover metrics.

The broader market picture: sector patterns in this week’s short data

Stepping back from individual names, the sector-level view reveals where institutional money is expressing the most concentrated scepticism.

The concentration of short interest in healthcare and consumer discretionary names aligns with ASX market breadth data for the same week, where those two sectors produced the most new 52-week lows as consumer confidence posted its steepest monthly decline since the COVID-19 pandemic, reinforcing that institutional short positioning and broader equity weakness are pointing in the same direction.

Healthcare and pharmaceuticals carry the heaviest aggregate short positioning, led by TLX at 16.10% and PNV at 14.29%. Consumer discretionary and food services follow closely, with DMP at 15.48% and GYG at 12.08%.

The retail sector saw building bearish activity across multiple names. Bapcor (BAP) rose to 9.50% (up 1.15% weekly), Myer (MYR) reached 6.59% (up 0.89% weekly), and CAR Group (CAR) climbed to 9.89% (up 0.64% weekly, 5.30% monthly). Zip (ZIP) at 11.76%, with a 4.35% monthly increase, added a buy-now-pay-later name to the list of stocks attracting growing bearish positioning.

On the other side, oil, gas, gold, and lithium names saw the most meaningful short covering. Woodside (WDS) fell to 2.12% (down 0.91% weekly), Evolution Mining (EVN) dropped to 2.53% (down 1.04% weekly), and PLS eased to 5.49% (down 1.31% weekly). Flight Centre (FLT) at 11.68% (down 0.77% weekly but up 2.00% monthly) remains elevated despite the weekly dip.

- Healthcare/pharma: Heaviest aggregate short interest (TLX, PNV)

- Consumer discretionary/food: Persistent bearish positioning (DMP, GYG)

- Retail: Building short interest (BAP, MYR, CAR)

- Fintech/BNPL: Rising bearish bets (ZIP)

- Resources (oil, gold, lithium): Most meaningful short covering (WDS, EVN, PLS)

Short sellers are watching the same stocks they watched last month

The top three names, TLX, DMP, and PNV, have held their positions with limited structural change, suggesting institutional conviction in these shorts remains firm rather than being driven by short-term event trading.

The two situations that warrant the closest attention in the coming weeks are Lotus Resources and Generation Development Group. LOT’s data retraction on 30 April 2026, which sent shares down 34%, occurred after the 28 April measurement date. That means the current data does not yet capture any positioning changes prompted by the event. GDG’s short interest has risen from approximately 4% to 9.40% in under six weeks, a pace that stands out against the rest of the table.

Watch list for the next data release: LOT (first data to capture post-retraction positioning) and GDG (monitoring whether the rapid short buildup continues or stabilises).

The next weekly data release will be the first to reflect any market positioning changes from after 28 April 2026. Updated short positions can be accessed via Market Index and ASIC’s published short position reports.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.