On 5 May 2026, Bloomberg reported that Apple held preliminary discussions with both Intel and Samsung about manufacturing its custom chips in the United States. Within hours, three of the most closely watched semiconductor stocks were moving in three different directions. The news arrives at a moment when U.S. supply chain resilience is a live strategic concern and both Intel and Samsung are building out domestic foundry capacity that needs anchor customers to validate billions in capital expenditure. What follows breaks down what the talks actually involve, why each stock moved the way it did, and what investors watching Apple semiconductor stocks need to understand before drawing conclusions from early-stage headlines.

What Apple is actually doing, and what it is not doing yet

Bloomberg’s report, published on 5 May 2026 and referencing events from the prior day, confirmed that Apple has engaged in preliminary discussions with Intel and Samsung about U.S.-based chip manufacturing. The sourcing described the talks as early-stage, with no agreements reached and no production timelines disclosed.

Three facts are confirmed:

- Bloomberg reported the discussions, citing unnamed sources familiar with the matter

- Apple executives visited Samsung’s under-construction facility in Taylor, Texas

- No contracts, memoranda of understanding, or formal commitments have been announced

How far along are the talks, really?

The descriptors “preliminary” and “early-stage” are the exact terms Bloomberg’s sources used. No party has disclosed a timeline for decision-making, and no formal proposals have been reported.

For investors, the distinction matters. A site visit and a signed contract sit at opposite ends of the supply chain commitment spectrum. Stock prices can move sharply on the former, but portfolio decisions are better anchored to the latter.

When big ASX news breaks, our subscribers know first

Why Apple wants an alternative to TSMC

TSMC has been Apple’s longstanding primary chip production partner, manufacturing the custom processors that power the iPhone, iPad, and Mac product lines. That relationship has served Apple well on performance, but it concentrates manufacturing risk in a single supplier operating primarily in East Asia.

The concentration is not unique to Apple. TSMC dominates leading-edge chip production globally, and most major technology companies face similar exposure. Apple’s outreach to Intel and Samsung reflects a structural vulnerability the industry shares, not a sudden operational failure.

Apple’s supply chain dependencies are most visible when read against the company’s revenue composition: iPhone revenue of $56.99 billion accounted for the majority of Apple’s record $111.2 billion Q2 2026 result, meaning any disruption to chip production flows directly into the company’s single largest revenue line.

Bloomberg’s reporting framed the discussions around Apple “reducing reliance on a single chip fabrication partner,” positioning the talks as a diversification effort rather than a replacement strategy.

The distinction is financially material for investors holding TSMC shares:

- Diversification scenario: Apple splits future orders across multiple foundries. TSMC retains the majority of volume but loses exclusivity. Revenue impact is moderate and gradual.

- Full transition scenario: Apple migrates primary production away from TSMC entirely. Revenue impact is severe. Bloomberg’s reporting does not support this interpretation at present.

Any transition would constitute what sources described as a “meaningful transformation” of Apple’s supply chain approach, a process measured in years rather than quarters.

Intel and Samsung’s foundry readiness, and why it matters for the thesis

Whether Apple’s discussions convert to contracts depends on whether either company can manufacture leading-edge chips at the volume and yield Apple requires. The readiness data paints two different pictures.

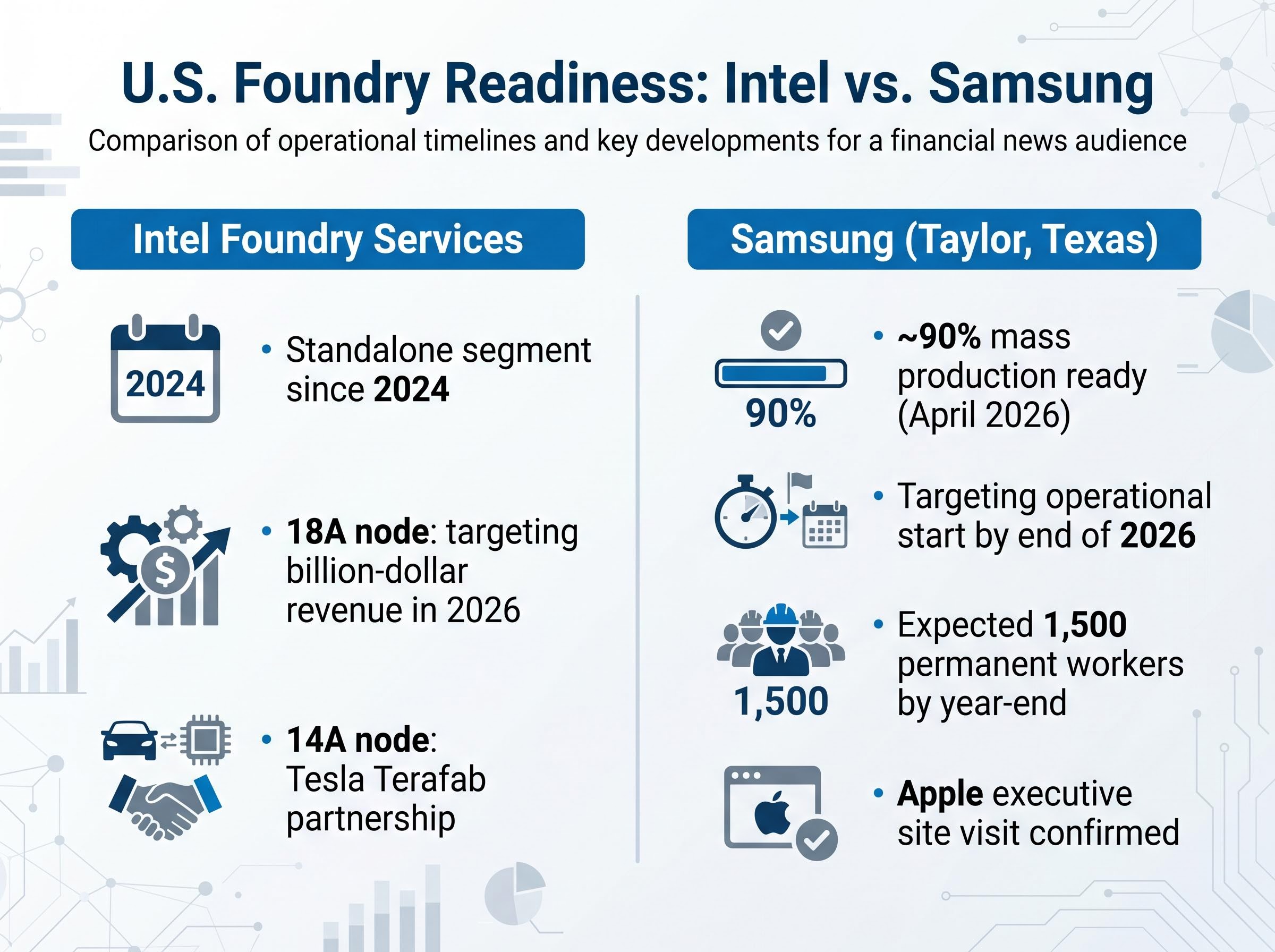

Intel Foundry Services

Intel Foundry Services (IFS), which has operated as a standalone business segment since 2024, is pursuing an aggressive turnaround. The unit reported approximately $7 billion in losses in 2023, reflecting the scale of investment required to build a competitive external foundry.

Intel’s 18A process node is progressing toward what the company expects will be billion-dollar revenue in 2026, a milestone that would signal commercial viability. Separately, Intel secured a partnership with Tesla for the Terafab project using Intel’s 14A process node, providing the first high-profile external customer validation.

Some analysts have characterised IFS as a potential “turnaround of the decade,” though the gap between foundry ambition and current financial performance remains wide.

Samsung’s Texas buildout

Samsung’s Taylor, Texas facility is further along in physical readiness. Mass production capability stood at approximately 90% as of April 2026, with an operational start targeted by the end of the year. The facility is expected to employ 1,500 permanent workers by year-end.

Apple executives visiting the Taylor plant is the most concrete act of engagement confirmed by Bloomberg’s reporting.

| Company | Facility location | Key process node | Operational status | Notable customer deal |

|---|---|---|---|---|

| Intel Foundry Services | U.S. (multiple sites) | 18A (leading-edge), 14A (next-gen) | 18A targeting billion-dollar revenue in 2026 | Tesla Terafab (14A node) |

| Samsung | Taylor, Texas | Advanced node (undisclosed specifics) | ~90% mass production ready; operational by end of 2026 | Apple executive site visit confirmed |

Investors treating this as a near-term revenue event for either company should weigh the readiness data carefully. Yield capability at leading-edge nodes remains the single largest execution risk in foundry manufacturing.

How the market read the news, and what the moves actually tell you

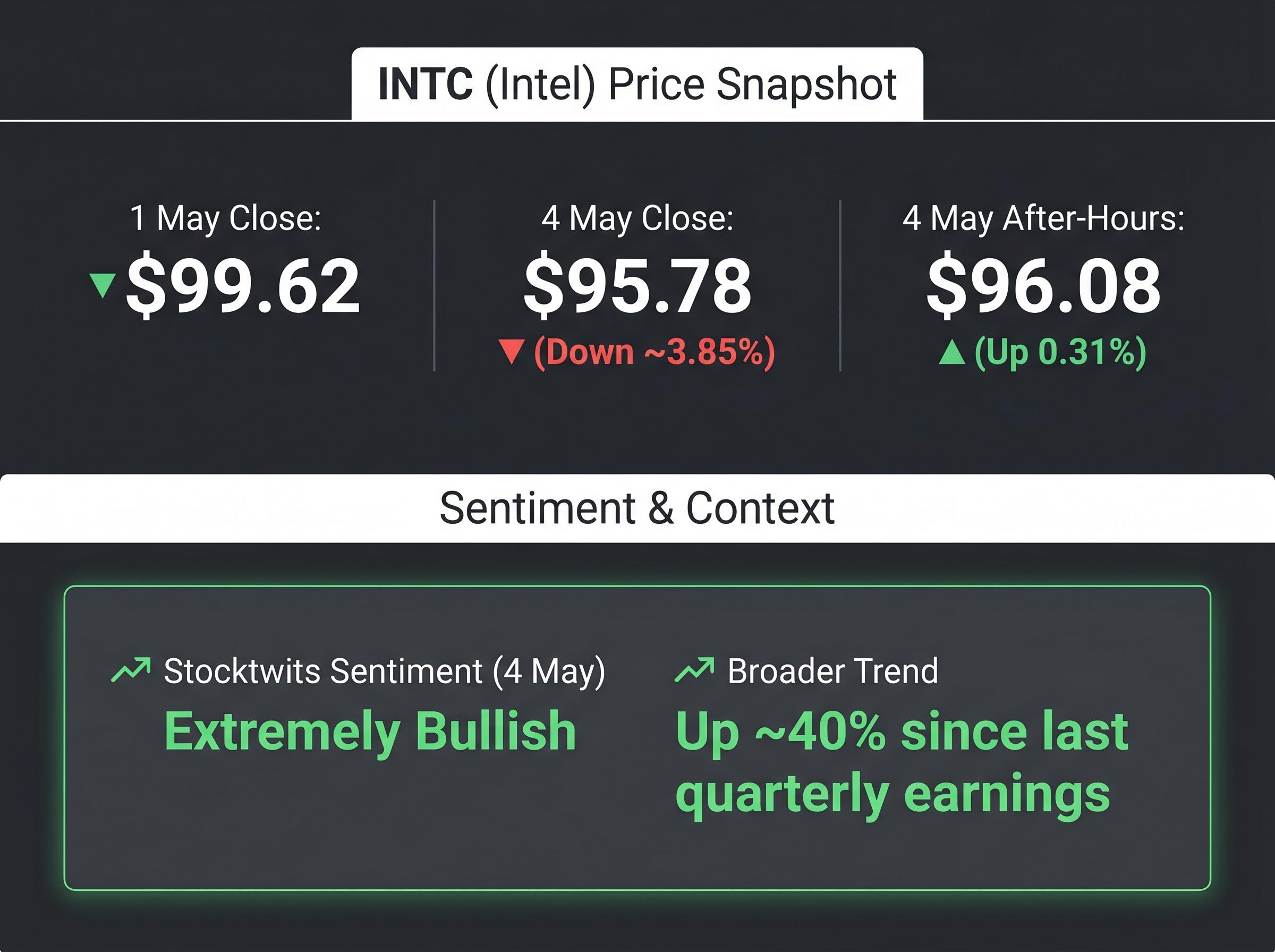

The stock movements on 4 May 2026 did not follow the script a headline reader might expect. INTC closed at $95.78, down approximately 3.85% from its $99.62 close on 1 May. After-hours trading nudged the price up 0.31% to $96.08, but the day’s direction was unmistakably negative.

A stock falling nearly 4% on the day an Apple partnership is reported is a signal worth interrogating. The decline suggests the market may be pricing in execution risk, the capital intensity of foundry buildouts, or margin compression that comes with serving a customer as demanding as Apple, rather than simply celebrating a potential new contract.

The pattern of investors selling on record results is not unique to this news cycle: Apple’s own Q2 2026 earnings saw shares fall approximately 1.3% in extended trading despite simultaneous all-time records for revenue, iPhone sales, and EPS, as the market focused instead on unresolved AI monetisation and leadership succession questions.

Stocktwits sentiment for INTC was rated “extremely bullish” as of 4 May 2026, amid high message volume. Shares were up approximately 40% since the last quarterly earnings report, suggesting the broader rally predates the Apple news.

| Stock | May 4 price movement | Directional interpretation | Data availability |

|---|---|---|---|

| INTC | $95.78 close, down ~3.85% | Market pricing execution risk and investment costs | Confirmed (Yahoo Finance) |

| TSM | Not independently verified | Diversification risk, but no displacement signal | Not confirmed for this specific news event |

| Samsung | Not independently verified | Potential anchor customer validation | Not confirmed for this specific news event |

The absence of verified same-day data for TSM and Samsung limits the conclusions that can be drawn about how the broader market digested the news. For Intel, the reaction suggests that investors are distinguishing between “potential customer interest” and “accretive revenue,” a distinction the early-stage status of these talks reinforces.

What this means for the semiconductor supply chain, and the investor framing that holds up

No formal analyst ratings changes or price target revisions had been published as of 5 May 2026 in connection with the Apple discussions. The market’s full analytical response is still forming.

For investors already holding semiconductor names, the immediate question is whether this news changes the thesis for any position. For those considering entry based on the headline, the question is whether preliminary talks constitute a sufficient catalyst.

Three unresolved variables will determine whether these discussions become material supply chain changes:

- Foundry yield capability: Can Intel or Samsung manufacture Apple’s chips at the defect rates and volumes Apple requires? Intel’s 18A billion-dollar revenue milestone, expected in 2026, would sharpen this question considerably.

- Apple’s timeline pressure: How urgently does Apple need a second source? No timeline has been disclosed, and urgency drives negotiating leverage.

- Policy environment: U.S. policy support for domestic chip manufacturing could accelerate or complicate these discussions depending on subsidy structures and trade conditions.

What to watch as this story develops

Two near-term milestones would signal whether talks are accelerating. Samsung Taylor’s operational start, targeted for late 2026, would demonstrate production-ready capacity. Intel’s 18A revenue milestone would demonstrate commercial viability. Until one or both arrive, the story remains on the watch list rather than the action list.

For investors wanting to stress-test the bullish foundry thesis against the downside scenario, our full explainer on semiconductor vulnerability to capex deceleration examines what happens to Intel and Samsung’s foundry economics if hyperscalers revise 2027 infrastructure spending downward, including the specific margin and revenue exposure that makes preliminary Apple discussions a necessary but not sufficient anchor.

The bigger picture behind Apple’s supply chain reset

Apple’s outreach is consistent with a broader industry-wide push toward U.S.-based chip manufacturing capacity. Both Intel and Samsung have committed billions to domestic foundry buildouts, but those investments need anchor customers to justify the capital expenditure.

The CHIPS Incentives award to Intel, announced by the U.S. Department of Commerce in November 2024, committed federal funding to support Intel’s domestic semiconductor manufacturing buildout across multiple U.S. states, making the policy tailwinds behind Intel Foundry Services concrete rather than aspirational.

Three parties have distinct interests in how this story resolves:

The AI capital expenditure cycle provides the structural backdrop that makes Apple’s foundry discussions legible as more than a bilateral supply chain move: with four hyperscalers collectively forecasting $650 billion in 2026 AI infrastructure spending, Intel and Samsung need large-volume anchor customers partly because that same spending wave is creating intense competition for leading-edge chip capacity across the industry.

- Apple: Seeks supply resilience and reduced concentration risk across its most important product lines

- Intel and Samsung: Need high-volume, high-profile external customers to validate their foundry investment theses and attract further demand

- U.S. policy environment: Domestic chip manufacturing capacity has become a strategic priority, and Apple’s participation would provide the highest-profile endorsement of that effort

For long-term investors in either Intel or Samsung, Apple becoming a production customer would be a foundational demand signal, one that extends beyond Apple’s own supply chain and into the viability of U.S. domestic semiconductor production as an investment category.

No formal analyst commentary or ratings revisions had been published specifically in response to these discussions as of 5 May 2026. The analytical consensus is still catching up to the headline.

Reading the Apple-Intel-Samsung talks without getting ahead of the data

The story as reported is definitively early-stage. No agreements have been reached, no timelines disclosed, and no analyst consensus has formed. The strategic logic on all sides is genuine: Apple wants supply resilience, Intel and Samsung want anchor customers, and the U.S. policy environment favours domestic production. But logic and execution are separated by years of manufacturing validation.

Intel’s 18A billion-dollar revenue milestone and Samsung Taylor’s late 2026 operational start remain the two concrete events that would convert this from a watch-list story to an investable development. INTC’s 3.85% decline on the day the news broke is a reminder that market reactions to supply chain headlines are rarely as straightforward as the headlines themselves.

The most useful habit for investors tracking this story is the simplest one: distinguishing between “talks have begun” and “a deal is done.” That distinction applies here, and it applies to every supply chain diversification headline that follows.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. These statements are speculative and subject to change based on market developments and company performance.