Crude Drops 4% on Hormuz Hopes, but the Deal Isn’t Done

9 hrs ago

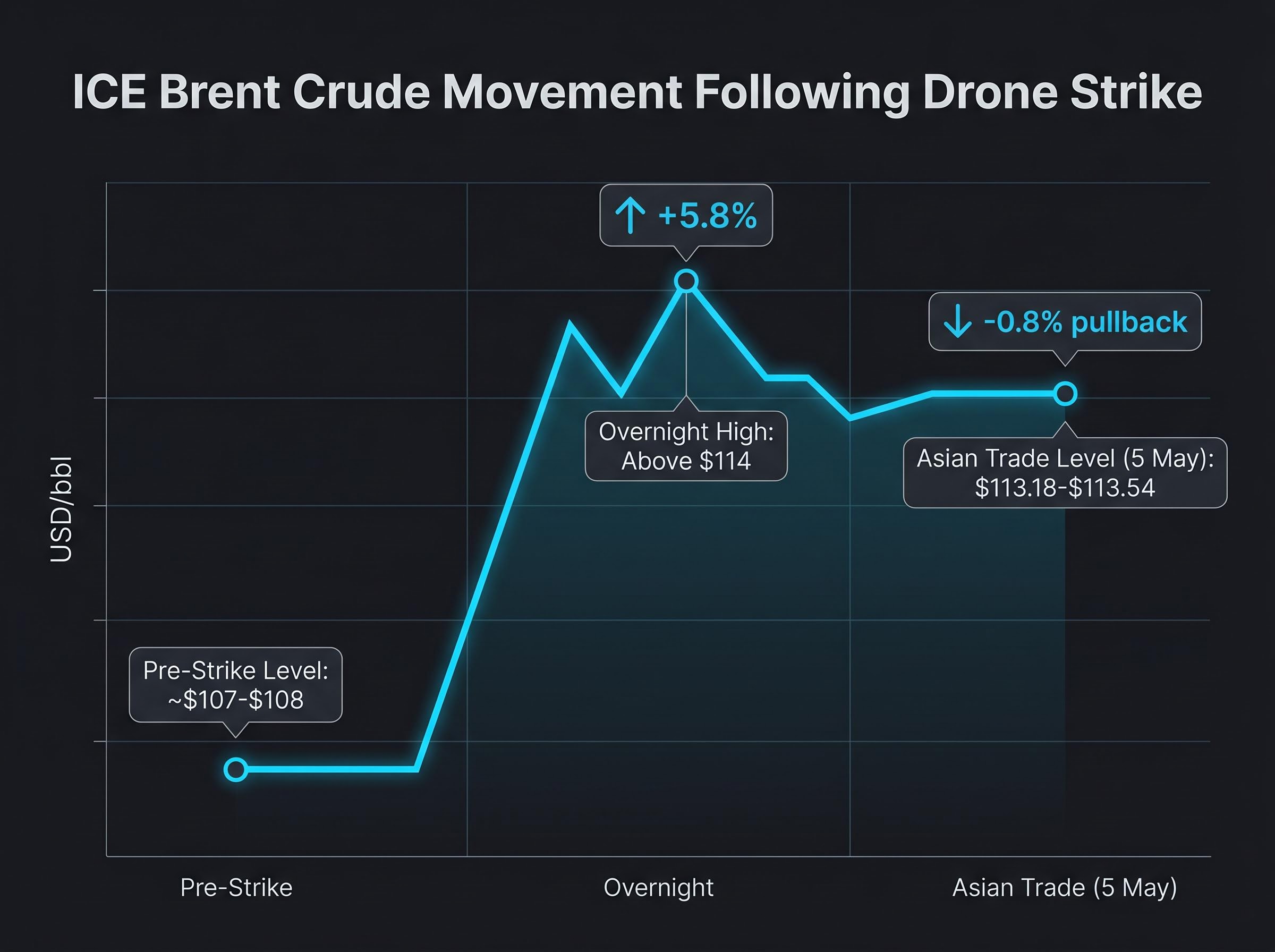

Overnight, a single drone strike on the UAE’s primary Hormuz-bypass oil hub sent Brent crude above $114 per barrel for the first time since the Gulf crisis escalated, putting Australian energy investors and mortgage holders on alert in the same session. The Fujairah Oil Industry Zone exists for one reason: to route Gulf oil exports without passing through the Strait of Hormuz, which has been functionally disrupted since February 2026. Striking Fujairah closes the escape hatch, and markets priced that in immediately.

What follows walks through the strike itself, why the oil price spike partially unwound during Asian trade, how the move rippled into ASX energy stocks and bond yields, and what the Reserve Bank of Australia’s (RBA) own language about “persistent energy price effects through the remainder of 2026” means for portfolios right now.

Fujairah sits on the Gulf of Oman, outside the Strait of Hormuz. Its entire function is to allow UAE crude exports to bypass the chokepoint Iran has leveraged as a weapon since February 2026. When suspected Iranian drones ignited a fire at the Fujairah Oil Industry Zone on 4-5 May, the target was not a peripheral pipeline. It was the contingency plan itself.

The UAE’s response was immediate:

The UAE condemned the strike as “unacceptable aggression.”

Three Indian nationals sustained moderate injuries. No fatalities were confirmed at the facility. Iran denied involvement, attributing regional instability to US “military adventurism,” leaving the diplomatic path forward unclear.

ICE Brent crude futures surged 5.8% overnight, breaking above $114 per barrel as traders absorbed the strategic implications of Fujairah being hit directly. The move reflected the market’s instant verdict: losing the bypass route is a different category of risk than losing a single export terminal.

The oil price trajectory from a pre-conflict baseline near $72-$74 per barrel to an intraday peak of $126 on 30 April illustrates how quickly supply risk can compound once a chokepoint closes; Minneapolis Fed President Kashkari cited industry estimates of roughly six months for supply chains to normalise even if the Strait reopened immediately, a timeline that frames the RBA’s ‘persistent through the remainder of 2026’ language as a conservative rather than an alarmist read.

During Asian trade on 5 May, Brent eased to approximately $113.18-$113.54 USD per barrel, a pullback of roughly 0.8% from the overnight peak. That partial reversal came from position squaring and the absence of a confirmed escalation announcement, not from a reassessment of the underlying supply threat.

| Metric | Pre-Strike Level (approx) | Overnight High | Asian Trade Level |

|---|---|---|---|

| ICE Brent Crude (USD/bbl) | ~$107-$108 | Above $114 | $113.18-$113.54 |

Goldman Sachs had already raised oil price forecasts citing Middle East supply disruption risks prior to the strike. JPMorgan has gone further.

JPMorgan analysts flag persistent supply losses and inflation stemming from the Iran conflict as signals of further oil price upside risk, recommending portfolio diversification to manage energy price volatility through 2026.

The partial pullback does not mean the risk premium has evaporated. A price correction is not risk resolution.

The Fujairah Oil Industry Zone was purpose-built to solve a single problem: what happens when the Strait of Hormuz becomes unreliable. Its functions include:

Partial Hormuz blockage since February 2026 had already elevated Fujairah from important to irreplaceable. The US military has been assisting merchant vessel transit and countering Iranian interdiction efforts, but the strike on Fujairah itself shows the threat has moved beyond the chokepoint and into the alternatives.

The Fujairah strike did not occur in isolation; it is the latest extension of a supply disruption that had already reached structural severity before any drone crossed UAE airspace, with the Hormuz triple lock of US naval blockade operations, Iranian toll enforcement on non-US vessels, and the near-total collapse of commercial war risk insurance combining to remove roughly 13 million barrels per day from global circulation at its peak.

The UAE withdrew from OPEC+ effective 1 May 2026, just four days before the strike. Gulf production coordination is fracturing precisely when the region is under military pressure.

No emergency OPEC+ output response has been confirmed as of 5 May 2026. The combination of a fractured producer alliance and a burning bypass facility leaves the global supply picture with fewer safety nets than at any point since the crisis began.

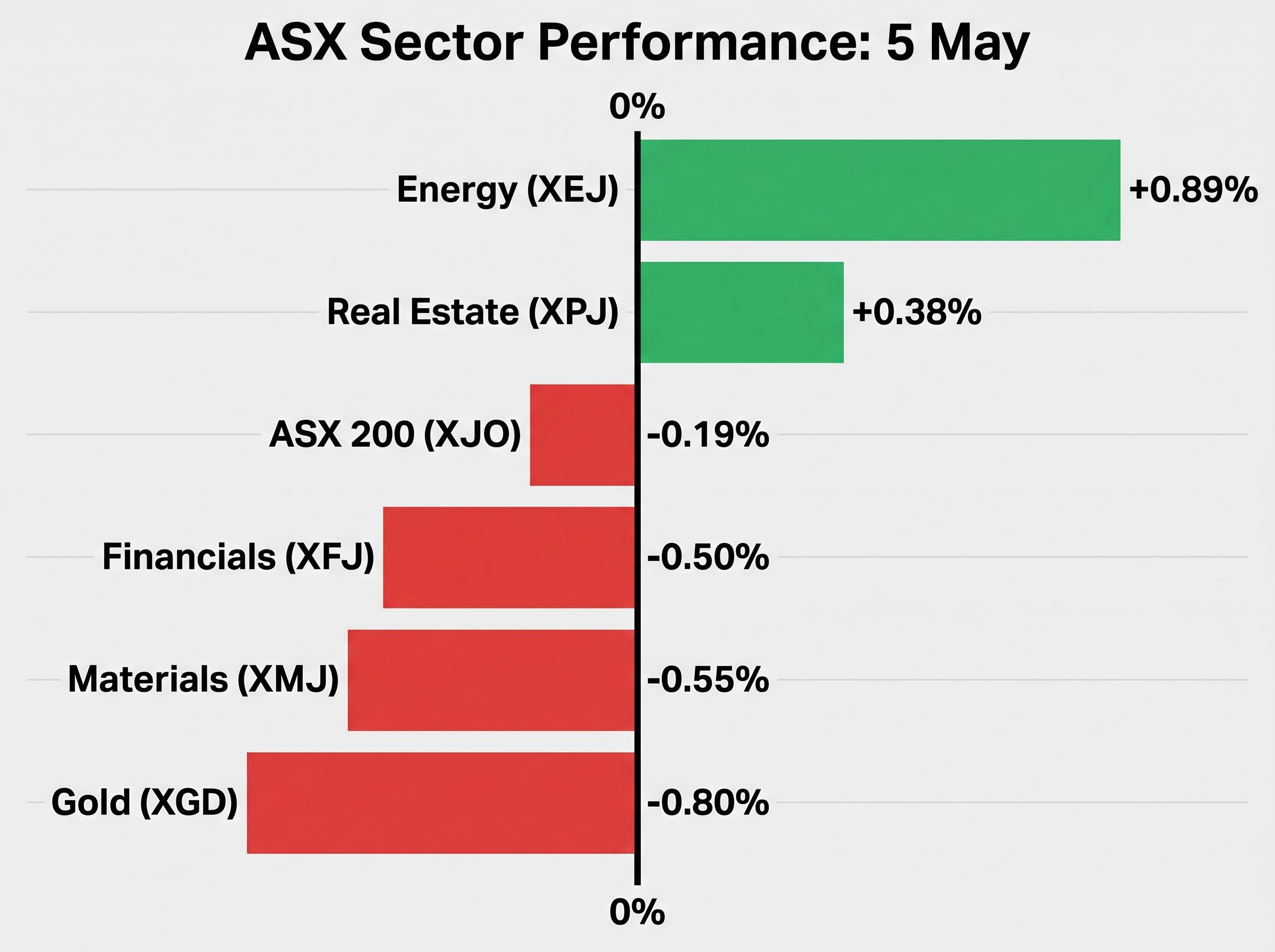

The ASX Energy sector (XEJ) gained 0.89% to close at 10,932.4 on 5 May, making it the session’s standout performer. The Brent crude surge translated directly into energy equity gains.

The broader ASX 200 (XJO) told a different story, closing at 8,680.5, down 0.19% (16.6 points). Energy gains were not enough to offset pressure elsewhere, and Chinese markets were closed for Labour Day, removing commodity pricing signals for resource stocks.

| Sector | Index Code | Change (%) | Close Level |

|---|---|---|---|

| Energy | XEJ | +0.89% | 10,932.4 |

| Gold | XGD | -0.80% | n/a |

| Materials | XMJ | -0.55% | 22,974.3 |

| Financials | XFJ | -0.50% | 9,470.8 |

| ASX 200 | XJO | -0.19% | 8,680.5 |

The gold sector’s decline despite a geopolitical shock deserves a two-part explanation:

An oil price shock does not lift all boats on the ASX. The cross-asset mechanics matter for investors positioning across energy, materials, and rate-sensitive sectors simultaneously.

The ASX sector rotation triggered by sustained crude prices above $110 has produced asymmetric outcomes: energy producers including Woodside and Santos gained roughly 40% year-to-date on oil-indexed LNG revenues while Qantas absorbed an estimated A$800 million increase in its fuel bill, a divergence that makes sector selection, rather than broad index exposure, the more consequential variable for Australian portfolios navigating the current shock.

The RBA raised the cash rate by 25 basis points to 4.35% on 5 May 2026. Australian economists have widely dubbed it the “Hormuz hike” for its explicit link to oil-driven inflation. An 80% market probability of the hike had been priced in ahead of the decision.

Governor Michele Bullock signalled that even if the Middle East conflict resolved quickly, the economic effects on Australia were expected to persist through the remainder of 2026. The RBA is not treating this oil surge as transitory. RBA forecasts show Australian GDP growth declining to approximately 1.1%, which Governor Bullock characterised as “very weak,” describing current monetary policy settings as “a bit restrictive.”

Governor Bullock acknowledged the rate rise “would create genuine hardship for Australian households.”

Bond markets pared rate rise expectations after the press conference, lifting the Real Estate sector (XPJ) by 0.38%.

The compounding pressure on Australian households is arriving through two channels simultaneously:

NAB expects a pause after the May hike to assess ongoing energy price impacts. Some economists argue the petrol price spike is already acting as a de facto rate rise on household budgets, meaning the formal hike adds a second layer of demand destruction on top of fuel costs already tightening consumer wallets.

For borrowers trying to model how long elevated repayments will last, our dedicated guide to the RBA rate plateau ahead examines all four major bank forecasts, including Westpac’s projection of a further path to 4.85% by August 2026, and explains how second-round oil price effects through freight and construction costs are expected to keep trimmed mean inflation sticky well into Q3 2026.

Two unresolved structural conditions will keep the oil risk premium elevated:

US Non-Farm Payrolls for April (forecast +60,000, sharply down from +178,000 in March) are due Friday 8 May and will intersect with oil price dynamics to shape global risk appetite entering the following week.

JPMorgan Asset Management recommends portfolio diversification to mitigate energy price volatility through 2026. That recommendation carries weight given the ASX Energy sector’s two-session performance: most energy stocks remain lower across two sessions despite the 5 May single-session gain, a caution against reading one day as a directional signal.

JPMorgan oil price research covering Middle East supply disruption scenarios identifies persistent inflation pass-through as the primary channel through which elevated Brent crude levels translate into sustained portfolio risk, particularly for economies with high household debt serviceability exposure like Australia.

JPMorgan Asset Management recommends portfolio diversification to mitigate energy price volatility through 2026, noting that persistent supply losses and inflation from the Iran conflict present ongoing risk to concentrated portfolios.

Three forces are compounding in the same session: a geopolitical supply shock that sent Brent above $114, a domestic rate rise to 4.35%, and a structural Hormuz disruption that has been building since February 2026. The RBA’s own language, “persistent through the remainder of 2026,” closes the door on any expectation that this will resolve quickly for Australian households or portfolios.

Brent crude levels, ASX Energy sector moves, and any OPEC+ emergency response are the primary indicators to watch as this situation evolves. For Australian investors, the week ahead will test whether a single-session energy rally holds, or whether the dual squeeze of rates and fuel costs pulls the broader market lower.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The Fujairah Oil Industry Zone is a UAE facility on the Gulf of Oman that allows crude exports to bypass the Strait of Hormuz. It became the primary alternative route after Hormuz was partially disrupted in February 2026, so a strike on Fujairah directly threatens the last major escape hatch for Gulf oil exports.

The RBA raised the cash rate by 25 basis points to 4.35% on 5 May 2026, a move widely called the 'Hormuz hike' because it was explicitly linked to oil-driven inflation stemming from the Iran conflict. Governor Michele Bullock indicated the economic effects on Australia are expected to persist through the remainder of 2026, signalling the RBA is not treating the oil surge as temporary.

The ASX Energy sector (XEJ) gained 0.89% to close at 10,932.4 on 5 May, making it the session's top performer. The broader ASX 200 fell 0.19%, as gains in energy were offset by declines in gold, materials, and financials.

ICE Brent crude surged 5.8% overnight to above $114 per barrel after suspected Iranian drone strikes ignited a fire at the Fujairah Oil Industry Zone on 4-5 May 2026. During Asian trade on 5 May, Brent eased slightly to approximately $113.18-$113.54 USD per barrel as traders squared positions, though the underlying supply risk remained unresolved.

Australian mortgage holders face a dual squeeze: higher repayments from the RBA's 25bp rate rise to 4.35%, and elevated petrol and energy costs flowing directly into household budgets from the oil price surge. Some economists note the fuel price spike is already acting as a de facto additional rate rise on consumer spending power.