What a Random ASX Backtest Reveals About Managing Market Risk

2 hrs ago

Hedge fund exposure to global information technology equities hit an all-time high as of the week ending 25 May 2026, surpassing every prior level recorded since Goldman Sachs Prime Brokerage began tracking these positions a decade ago. The record arrives against an unlikely backdrop: Iran conflict-related macroeconomic pressures that might ordinarily prompt institutional de-risking. Instead, hedge funds accelerated their technology purchases at the fastest pace in nearly three months, pushing collective tech weightings relative to the MSCI World Index to a five-year high.

The divergence between geopolitical stress and institutional conviction is the signal worth examining. What follows breaks down what is driving the surge, which technology sub-sectors are attracting the most concentrated interest versus facing selling pressure, and what the positioning data means for readers tracking institutional momentum in AI and semiconductor equities.

The numbers carry their own weight. According to Goldman Sachs Prime Brokerage, aggregate hedge fund exposure to global IT equities reached an all-time high during the reporting week ending approximately 25 May 2026. That figure exceeds every prior level since the firm began tracking institutional positioning in 2016, a full ten-year window that includes the pandemic tech rally, the 2022 rate-shock sell-off, and every AI-driven accumulation wave since.

Goldman Sachs Prime Brokerage characterised aggregate hedge fund exposure to global information technology equities as having reached an all-time high, surpassing all levels recorded since tracking began in 2016.

What makes the milestone sharper is the speed at which it arrived. The buying pace was the swiftest in nearly three months, indicating acceleration rather than a gradual drift upward. Funds were not simply holding existing positions; they were adding to them with urgency.

Three headline metrics frame the scale of this positioning shift:

Institutional positioning at record extremes is one of the more reliable indicators of directional conviction in professional markets. The fact that all three metrics aligned in the same reporting week is uncommon, and it sets the context for understanding where, specifically, that conviction is being deployed.

SEC Form 13F disclosure requirements mandate that institutional investment managers with more than 100 million dollars in qualifying assets report their long equity holdings quarterly, making the 13F filing cycle one of the few public windows into the directional positioning that prime brokerage reports capture on a more frequent basis.

The all-time high in aggregate tech exposure masks a sharper story underneath. Not every corner of the technology sector is attracting the same interest, and the gap between what hedge funds are accumulating and what they are offloading reveals where conviction is genuinely concentrated.

Semiconductors and chip manufacturers attracted the highest speculative interest among all technology sub-sectors during the reporting week, according to Goldman Sachs. The buying was not one-dimensional: it comprised both short-covering (the unwinding of existing bearish bets) and fresh long initiation (new directional positions). That combination is notable. Short-covering alone can reflect forced repositioning rather than conviction. When paired with new longs, it points to a broader reassessment of forward value.

The semiconductor sector surge running through 2026 has been underpinned by a specific demand narrative: hyperscalers including Microsoft, Google, Amazon, and Meta have committed a combined approximately $725 billion in 2026 capex guidance directed toward agent-driven inference infrastructure, creating compounding procurement demand across memory, logic, and interconnect components that extends well beyond any single chip vendor.

Software companies formed the second accumulation cluster, also receiving net inflows. The AI linkage runs through both sub-sectors: semiconductor firms supply the compute infrastructure, and software firms build the applications that sit on top of it.

Communications equipment makers and IT services firms sat on the opposite side of the ledger, facing net selling pressure during the same week. The contrast is direct and needs little embellishment.

| Sub-Sector | Flow Direction | Primary Driver |

|---|---|---|

| Semiconductors | Net buying | Short-covering and fresh long initiation |

| Software | Net buying | AI-linked demand and speculative interest |

| Communications equipment | Net selling | Institutional de-risking |

| IT services | Net selling | Institutional de-risking |

The divergence suggests hedge funds are not making a blanket bet on “tech.” They are making a specific bet on AI-adjacent hardware and software, while reducing exposure to sub-sectors with weaker structural tailwinds.

The Iran conflict has introduced sustained macroeconomic headwinds throughout 2026, the kind of geopolitical pressure that historically prompts institutional risk reduction across growth-sensitive sectors. Technology equities, with their elevated valuations and sensitivity to discount rate expectations, would ordinarily sit near the front of any de-risking queue.

The recurring divergence between geopolitical risk and market behaviour follows a documented pattern: equity markets process conflict events as probability-adjusted inputs to future earnings rather than proportional headline shocks, which is why consensus predictions have repeatedly overestimated the equity damage from major disruptions. The structural mechanisms that absorb supply-side shocks, including spare production capacity, strategic reserves, and reroutable logistics, tend to limit economic transmission well before institutional portfolio managers feel compelled to reduce risk.

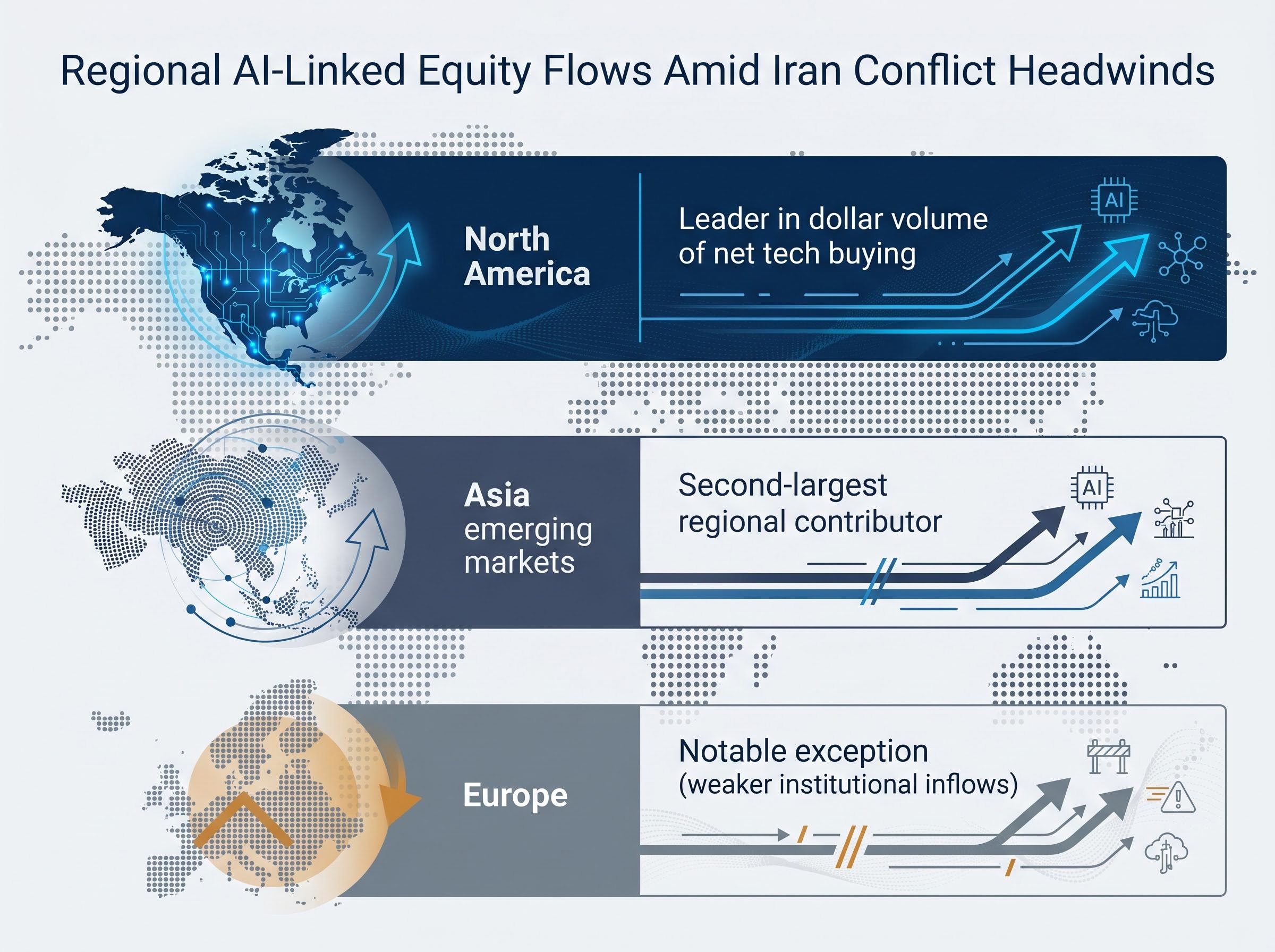

That has not happened. According to Goldman Sachs Prime Brokerage, AI-linked equities maintained their upward trajectory and sustained momentum despite the broader conflict-related pressures. The buying spanned most major global regions, with North America and Asia emerging markets leading in dollar volume.

Goldman Sachs Prime Brokerage noted that AI-linked equities maintained momentum through macroeconomic headwinds associated with the Iran conflict, with buying activity persisting across most major global regions.

The resilience appears rooted in structural demand drivers. AI compute requirements, data centre buildouts, and enterprise software adoption cycles operate on multi-year procurement timelines that do not pause for geopolitical disruption in the same way that consumer discretionary or commodity-linked equities might. The fact that buying included both short-covering and fresh long initiation across regions suggests broad conviction rather than a single tactical move by a handful of funds.

Record positioning data carries analytical value, but only if readers understand what it measures and where its limits sit.

Hedge fund prime brokerage positioning data functions as a momentum signal, not direct investment guidance. When Goldman Sachs reports that aggregate tech exposure has reached an all-time high across its ten-year tracking history (since 2016), it captures the net directional positioning of hundreds of institutional portfolios in a single reading.

The distinction between short-covering and fresh long initiation matters for interpreting signal strength. Short-covering reflects the closing of bearish positions, a reduction in negativity rather than an expression of bullishness. Fresh long initiation represents new capital being deployed in the direction of rising prices. When both occur simultaneously, as they did in the most recent reporting week, the combined signal is stronger than either component alone.

The MSCI World Index relative weighting measure provides a standardised benchmark for gauging whether positioning is stretched. A five-year high in that ratio suggests hedge funds are not merely keeping pace with the index; they are meaningfully overweight.

The MSCI World Index sector weighting methodology establishes how constituent securities are weighted and rebalanced across sectors, which determines the benchmark denominator used to calculate whether hedge fund tech allocations represent a genuine overweight relative to the index or simply track its own elevated tech composition.

Prime brokerage reports are institutional-access documents. Retail readers typically encounter the findings through financial media coverage with some delay, meaning the positioning data may already be partially reflected in prices by the time it becomes publicly visible.

Record positioning can also reflect two very different conditions: strong forward conviction built on durable demand drivers, or a crowded trade approaching the point where any catalyst for reversal would trigger amplified selling. The data alone does not distinguish between the two.

The crowded trade signals visible in the Goldman Sachs Prime Brokerage data align with independent survey evidence: the May 2026 BofA Fund Manager Survey identified long global semiconductors as the single most crowded institutional position at 73% conviction, with cash levels compressing to 3.9% and the Bull and Bear Indicator one step below the 8.0 threshold that triggers a second independent sell signal simultaneously.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

The ten-year tracking window that underpins the all-time high characterisation began in 2016. That baseline captures a full market cycle: the late-stage bull market of 2017-2019, the pandemic crash and recovery of 2020-2021, the aggressive rate-tightening sell-off of 2022, and the AI-driven rebound from 2023 onward.

Against that full arc, the current positioning stands out on multiple dimensions:

The five-year high in MSCI World relative weighting is not simply a reflection of strong absolute returns; it also captures a period when international developed markets including Europe and Japan are trading at roughly a 50-55% forward price-to-earnings discount to the S&P 500 IT sector, a valuation spread near multi-decade extremes that historically has preceded rotations away from the dominant cohort.

Prior periods of elevated hedge fund tech concentration have preceded both sustained rallies and sharp reversals. The data does not offer a single directional reading. What makes the current record notable rather than routine is its context: it arrived during an active geopolitical conflict that has not yet resolved, against macroeconomic conditions that would historically have prompted de-risking rather than accumulation.

The tension between record conviction and unresolved risk is the defining feature of this positioning moment.

Hedge fund technology exposure has reached a level that no prior period in the past decade has matched, concentrated specifically in semiconductors and AI-linked software names. That positioning has persisted, and accelerated, through a geopolitical environment that has historically prompted institutional risk reduction.

The sub-sector divergence is the most instructive finding. Institutional capital is not flowing into technology broadly; it is flowing into the AI compute supply chain while actively reducing exposure to communications equipment and IT services. That specificity distinguishes the current positioning from a generic risk-on rotation.

The structural question the data leaves open is whether this reflects durable conviction built on multi-year AI demand fundamentals, or a crowded trade that has not yet been tested by a more severe geopolitical shock. Subsequent Goldman Sachs Prime Brokerage releases and the next 13F filing cycle will provide the first data points for tracking whether this record holds or begins to reverse.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

An all-time high in hedge fund tech exposure means that, across the full tracking history measured by Goldman Sachs Prime Brokerage since 2016, institutional portfolios collectively hold more weight in global IT equities than at any prior recorded point, including the pandemic-era tech rally and every AI accumulation wave since.

As of the week ending 25 May 2026, hedge funds were net buyers of semiconductors and software, driven by AI-linked demand and a combination of short-covering and fresh long initiation, while communications equipment makers and IT services firms faced net selling pressure.

Short-covering refers to funds closing existing bearish bets, which reduces negativity but does not necessarily signal bullishness, while fresh long initiation means new capital is being deployed in the direction of rising prices; when both occur simultaneously, the combined signal indicates stronger conviction.

Retail investors can monitor quarterly SEC Form 13F filings, which require institutional managers with over $100 million in qualifying assets to disclose long equity holdings, and follow financial media coverage of prime brokerage reports from firms like Goldman Sachs for more frequent directional signals.

AI compute requirements, data centre buildouts, and enterprise software adoption cycles operate on multi-year procurement timelines that are less sensitive to geopolitical disruption than consumer or commodity-linked sectors, which appears to be sustaining institutional conviction even as macroeconomic headwinds persist.