On 5 May 2026, Brent crude was trading near $113-$114 per barrel, having surged more than approximately 5.8% the prior session before easing as US-Iran strikes resumed across the Gulf. Within the same 48-hour window, the White House announced Project Freedom, and daily Strait of Hormuz transits sat at roughly nine vessels, less than half the waterway’s normal throughput.

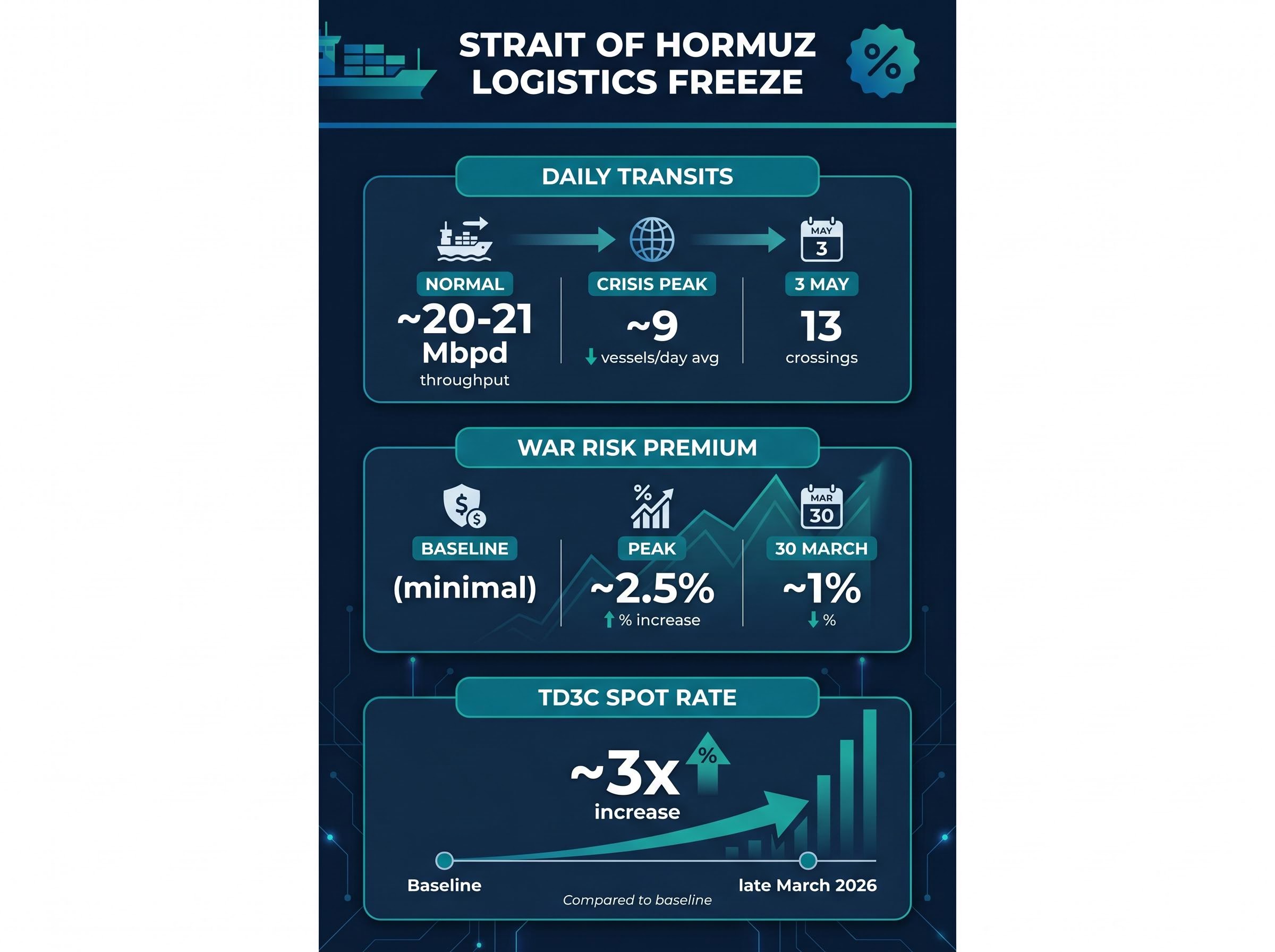

The Strait of Hormuz carries roughly 20-21 million barrels per day under normal conditions. Since late March 2026, a combination of Iranian interdiction threats, a collapsed ceasefire, and surging war risk premiums has effectively frozen commercial shipping confidence. Project Freedom is Washington’s logistical answer to that freeze.

What follows is an assessment of what Project Freedom actually does operationally, what price relief it has delivered so far, and why analysts argue that a military guidance programme cannot resolve the geopolitical fault line still driving energy market volatility.

What Project Freedom actually does on the water

The distinction that matters is between “military escort” and “military guidance.” Project Freedom does not provide formal one-to-one warship escorts for individual tankers. Instead, the US military is actively guiding stranded commercial vessels through the Strait under a broader regional defensive posture.

President Trump characterised the initiative as humanitarian, framing it around the plight of stranded vessels and crews. In the same announcement, he warned that interference would “have to be dealt with forcefully.” That dual-register tone, humanitarian rationale paired with a military threat, defines the programme’s diplomatic positioning.

Three confirmed operational elements anchor the initiative:

- Guidance posture: Active US military coordination of commercial vessel transits, not formal individual escorts.

- Humanitarian framing: The programme is publicly justified by the stranded vessel crisis, not as a combat operation.

- Launch timeline: Announced 3-4 May 2026, with operations commencing Monday morning Middle East time on 5 May.

What the asset claims do and do not tell us

Early reporting cited significant US military assets deployed to support the programme, including guided-missile destroyers, over 100 aircraft, multi-domain unmanned platforms, and approximately 15,000 service members. These figures remain unverified by independent sources.

The analytical significance is straightforward. Inflated perceived deterrence and actual deterrence capacity are not the same thing. Markets are pricing a perception of restored security. If Iranian interdiction attempts resume and the deployed force proves thinner than claimed, the confidence gap could reverse sharply.

When big ASX news breaks, our subscribers know first

The shipping freeze that made Project Freedom necessary

The collapse in Strait of Hormuz traffic did not arrive overnight. Outbound crude shipments began falling in March 2026 as war risk insurance premiums spiked, and by late April, daily transits had thinned to an average of roughly nine vessels per day.

The transmission mechanism ran through insurance and freight costs. War risk premiums peaked at approximately 2.5% before easing to approximately 1% as of 30 March 2026, according to S&P Global Platts and HowdenRe’s Strait of Hormuz report dated 27 March 2026. Even at the lower level, premiums remained elevated enough to freeze marginal operators out of the route entirely.

Spot shipping rates on the TD3C benchmark (Middle East to Asia) nearly tripled by late March 2026, driven by surging war risk premiums and widespread avoidance of the Strait.

The result was a logistics crisis. Vessels that were willing to transit could not afford to. Vessels that could afford to lacked insurance coverage at commercially viable terms. That is the stranded-vessel problem Trump’s humanitarian framing is built around, and it is real.

The shipping freeze did not arise from a single cause; the Hormuz triple lock of US naval blockade operations, Iranian toll enforcement on non-US and non-Israeli vessels, and near-total withdrawal of commercial war risk insurance converged to make the route commercially unnavigable for most operators well before transit volumes collapsed to single-digit daily counts.

| Metric | Pre-Crisis Level | Crisis Peak | As of 5 May 2026 |

|---|---|---|---|

| Daily Strait transits | ~20-21 Mbpd throughput | ~9 vessels/day avg | 13 crossings (3 May) |

| War risk premium | Baseline (minimal) | ~2.5% | ~1% (30 March) |

| TD3C spot rate | Baseline | ~3x increase | Elevated |

How oil markets responded, and why the numbers are messy

The price sequence across 4-5 May 2026 resists a clean reading. Brent crude dropped to approximately $107.53 on 4 May, then surged more than approximately 5.8% the prior session before settling around $113.93 by 20:10 ET on 5 May, according to Investing.com. WTI dropped approximately 1.2% to $105.05 per barrel on 5 May.

The problem is attribution. At least three concurrent variables were moving oil prices simultaneously:

- Project Freedom launch: The guidance programme’s announcement introduced downside pressure on crude by signalling improved transit prospects.

- OPEC+ output increase: A modest production increase announced in early May 2026 coincided with the initiative, adding supply-side pressure unrelated to the Strait.

- UAE OPEC+ exit: The UAE’s departure from the alliance in early May 2026 shifted its production decisions to a sovereign footing, introducing an independent volume variable.

Any single-cause reading of the price moves in this environment is analytically incomplete. The cross-source variance in Brent figures alone, ranging from approximately $104 to $114 depending on the source and timestamp, underscores the difficulty of isolating Project Freedom’s specific contribution.

The Project Freedom announcement on 4 May produced a 1.69% single-session drop in both Brent and WTI, with J.P. Morgan’s forecast trajectory illustrating just how rapidly geopolitical risk can override supply fundamentals: the bank shifted its 2026 Brent outlook from $60 per barrel to a warning above $150 in under five weeks.

The currency market signal

Forex analysis from Forex.com noted that Project Freedom’s announcement delivered downside pressure on USD/CAD by boosting risk appetite. This is a sentiment indicator, not a supply indicator. It measures perceived improvement in energy market security, not realised improvement.

The distinction matters for positioning. Currency markets can reprice sentiment in minutes. Freight rates and insurance premiums take weeks. The gap between the two is where misaligned trades live.

What history says about military escort programmes and market stability

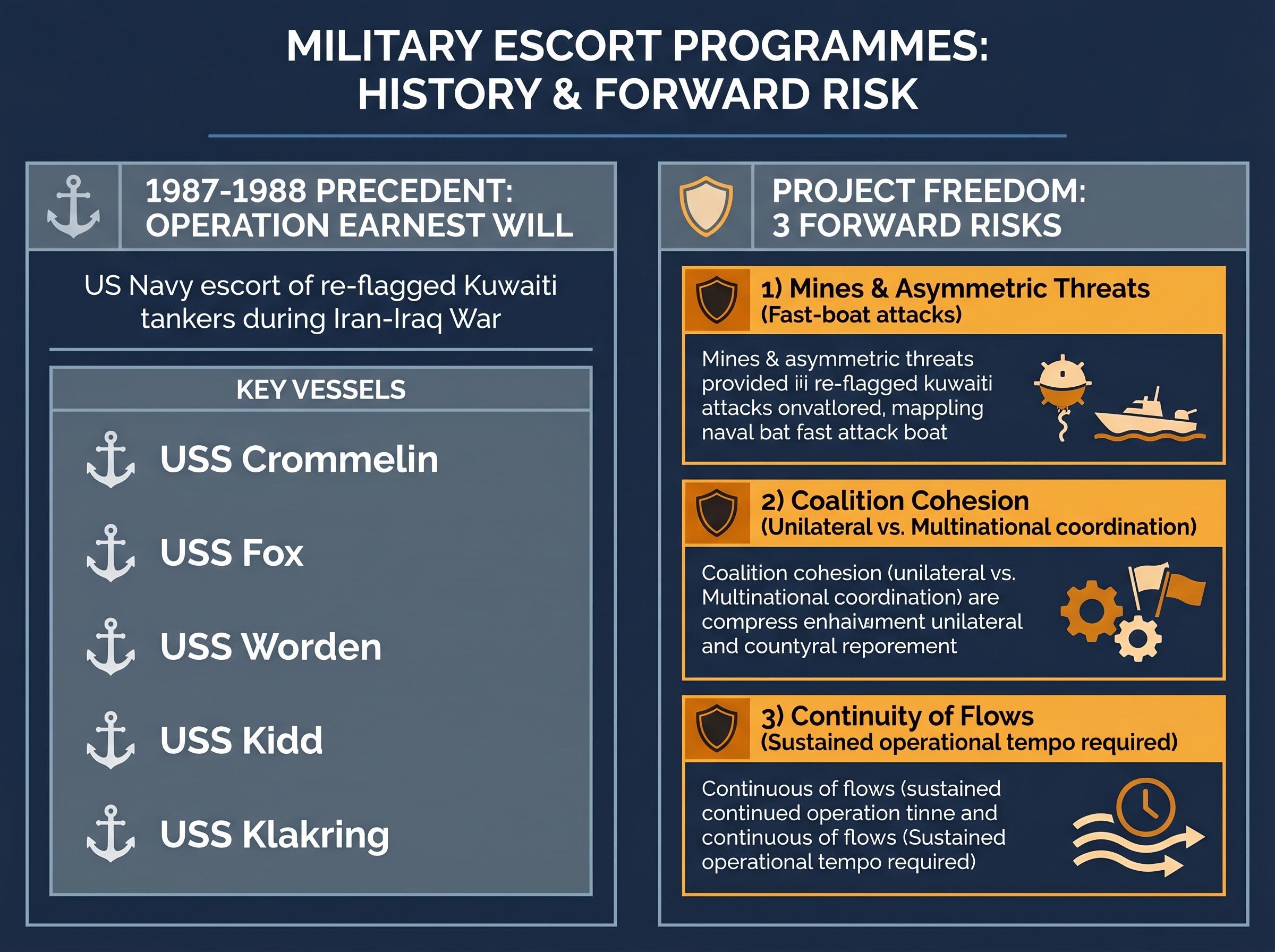

The correct historical precedent for Project Freedom is Operation Earnest Will (1987-1988), a US Navy operation that escorted re-flagged Kuwaiti tankers through the Strait during the Tanker War phase of the Iran-Iraq War. Key vessels included the USS Crommelin, USS Fox, USS Worden, USS Kidd, and USS Klakring.

Earnest Will delivered initial market relief. Shipping confidence recovered in the near term as tankers moved under military protection. Then the complications arrived.

Three lessons from Earnest Will map directly onto Project Freedom’s forward risks:

HowdenRe’s Strait of Hormuz war risk analysis documented premium surges reaching up to 5% of vessel value for certain routes, with the compression from that peak to approximately 1% representing a meaningful but incomplete normalisation that still excluded marginal operators from commercial viability.

- Mines and asymmetric threats: Iran deployed mines and fast-boat attacks that escort forces struggled to suppress consistently. Project Freedom faces the same category of threat in a more technologically advanced form.

- Coalition cohesion: Multinational coordination proved difficult to sustain as the operation extended. Project Freedom’s current posture appears predominantly unilateral, which simplifies command but limits burden-sharing.

- Continuity of flows: Escort programmes require sustained operational tempo. Any interruption, whether from political pressure, operational fatigue, or escalation, risks a rapid reversal of confidence gains.

Analysis from RSIS and CSIS indicates that naval escort and guidance programmes can restore shipping confidence in the near term, but their durability depends on political sustainability and Iranian restraint. The 1987-1988 precedent shows initial market relief followed by persistent volatility until a broader diplomatic resolution was reached.

For energy investors, the implication is direct. If the Earnest Will pattern repeats, short-term price relief is plausible, but positioning should account for continued premium volatility absent a diplomatic framework.

The structural gap Project Freedom cannot close

Project Freedom addresses logistics. It does not address the underlying Iran-US geopolitical conflict that caused the shipping freeze. That distinction is the analytical core of this assessment.

Analyst commentary drawn from the research is direct: Project Freedom may address certain logistical obstacles, but it does not resolve the root geopolitical conflict driving energy market volatility.

The evidence that the conflict is widening, not de-escalating, arrived on the same weekend the programme launched. Renewed US and Iranian strikes in the Gulf on 4-5 May effectively ended a tenuous ceasefire arrangement. War risk insurance premiums remain elevated relative to pre-crisis levels even after easing from their 2.5% peak.

The Fujairah attack as a market signal

Iranian strikes extended to UAE energy infrastructure, including the Fujairah port oil terminal, reported on 4 May 2026. This is the single most important data point in this analysis.

The Fujairah Oil Industry Zone had been functioning as one of the only active pipeline bypass routes that avoided the Strait entirely, meaning Iranian strikes on the facility directly compounded the existing supply bottleneck rather than introducing a separate, isolated disruption to Gulf energy infrastructure.

The Fujairah attack represents a geographic expansion of risk beyond the Strait itself. Project Freedom’s operational posture is Hormuz-focused. Iranian escalatory options, however, now extend to supply chain nodes across the Gulf that no single corridor-specific military programme can protect. The conflict is not contained to one chokepoint, and energy investors should price accordingly.

Military logistics versus market risk: what investors should actually watch

The next four to six weeks will determine whether Project Freedom’s initial confidence effect holds or unravels. The leading indicators split into two categories.

Signals that Project Freedom is working:

- Daily Strait transit volumes recovering toward pre-crisis throughput levels

- War risk insurance premiums declining toward baseline

- TD3C spot rates (Middle East to Asia) stabilising or falling

Signals that structural risk is re-escalating:

- Iranian interdiction attempts resuming despite military guidance operations

- War risk premiums re-widening after initial compression

- Fujairah-style attacks on Gulf energy infrastructure outside the Strait corridor

Freight rate and insurance premium normalisation is expected to lag shipping traffic recovery by several weeks, according to research assessments. That makes daily transit volume the earliest available signal.

The UAE supply wildcard

The UAE’s exit from OPEC+ means its production decisions are now sovereign and unconstrained by alliance quotas. Algeria, Russia, and Kazakhstan reaffirmed their commitment to the OPEC+ framework following the departure, keeping alliance supply management partially intact.

World Oil reporting on OPEC+ output and UAE exit confirms that Algeria, Russia, and Kazakhstan reaffirmed alliance commitments following the UAE’s departure, preserving partial supply management discipline even as the bloc’s collective influence over Gulf production narrowed.

Medium-term price modelling must now account for UAE production behaviour as a separate input from both OPEC+ decisions and Strait security conditions. The UAE’s capacity to increase output independently introduces a volume variable that interacts with, but is distinct from, the security situation.

The verdict: a programme that buys time, not resolution

Project Freedom has delivered near-term price relief and modest shipping confidence. It has not altered the structural risk calculus for energy markets.

The historical precedent from Operation Earnest Will and the current escalation evidence, including the Fujairah attack and resumed strikes, both point to persistent volatility until diplomatic resolution, not military logistics, changes the underlying conditions.

Project Freedom buys time. It does not buy resolution. The programme addresses a logistics crisis while the geopolitical conflict that created it continues to widen.

The next four to six weeks of transit data, freight rates, and war risk premiums will determine whether the programme’s initial confidence effect holds. Energy investors who focus purely on headline crude prices will miss those leading indicators, and the leading indicators are where the actionable signal lives.

For investors wanting to build a broader framework for reading energy and equity markets under geopolitical stress, our full explainer on geopolitical risk and market resilience examines the specific conditions under which headline shocks translate into sustained market damage versus temporary dislocations, using the April 2026 Caspian Pipeline attack and multiple historical precedents to map when sentiment repricing becomes fundamental repricing.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.