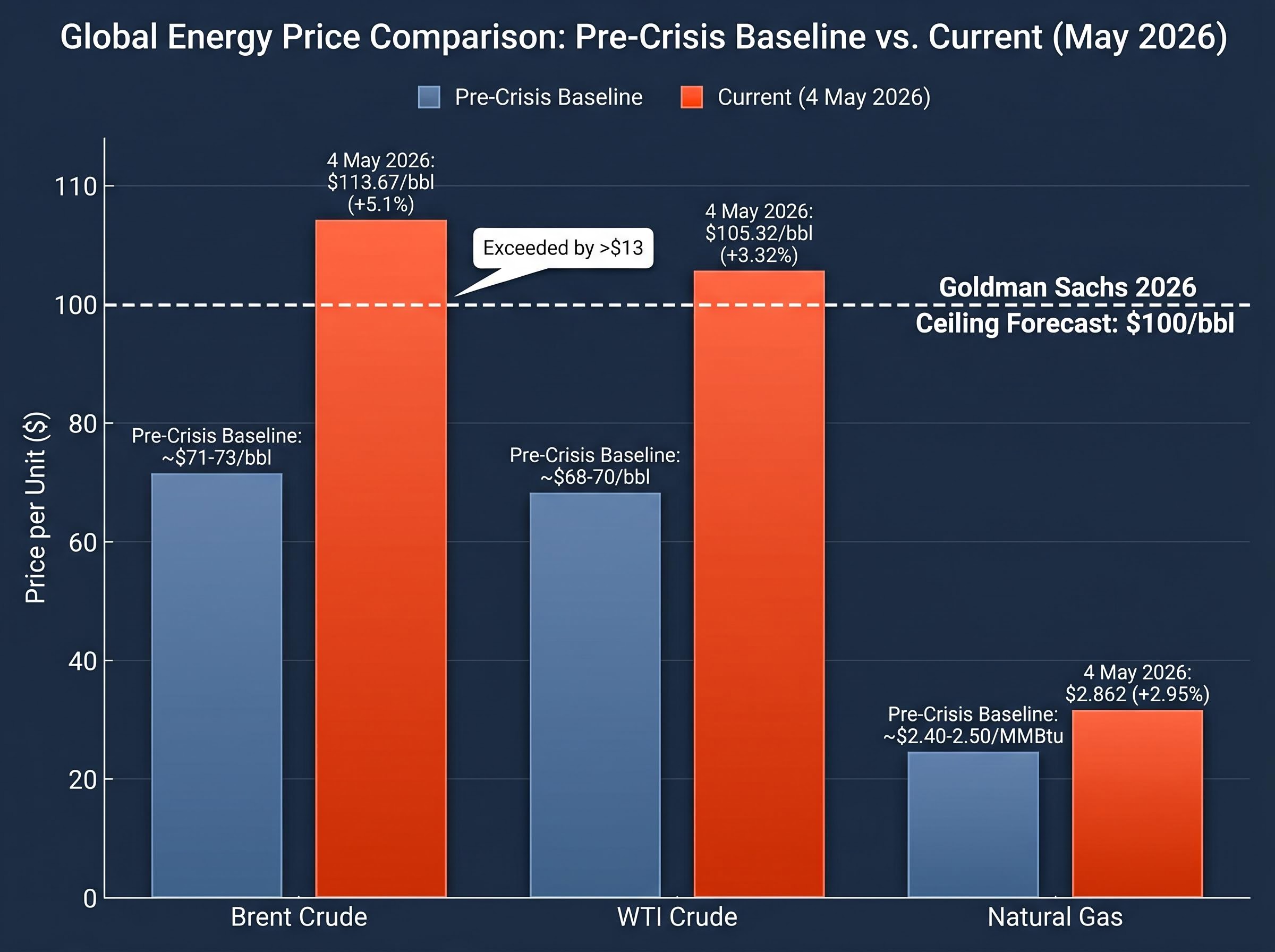

Brent crude surged 5.1% to $113.67 per barrel on 4 May 2026, hours after Iranian missiles and drones struck the Fujairah Oil Industry Zone, one of the Middle East’s largest petroleum storage complexes. WTI crude climbed 3.32% to $105.32. Natural gas futures rose 2.95%. Crude oil prices now sit above the $100 per barrel threshold Goldman Sachs flagged as a worst-case scenario just weeks ago, and every major analyst forecast set at the outset of the Strait of Hormuz crisis has been exceeded.

The strait, a passage carrying roughly one-fifth of the world’s oil supply, has been under competing blockades for nine weeks. The International Energy Agency (IEA) has described the disruption as the greatest global energy security challenge in modern history. What follows explains what is driving crude oil prices to yearly highs today, what the Fujairah attack changes about the supply picture, and what energy analysts and JPMorgan economists say about how long this disruption is likely to last.

Brent crude breaks above every analyst forecast as Fujairah complex takes direct hits

The numbers arrived first. Brent crude at $113.67. WTI at $105.32. Natural gas at $2.862. All posted on a single session, all above every baseline forecast issued when the Hormuz crisis began in early March.

When the strait was first contested, Brent and WTI surged 10-13% to the $80-82 range. Goldman Sachs set a $100 per barrel ceiling forecast for the end of 2026. That figure is now in the rear-view mirror.

Goldman Sachs forecast oil prices could reach $100 per barrel through the end of 2026 if Hormuz flows did not normalise. As of 4 May 2026, Brent has already exceeded that threshold by more than $13.

The Fujairah attack was the catalyst that pushed an already-elevated market into new territory. UAE civil defence confirmed a fire at the petroleum complex following Iranian drone and missile strikes, with UAE air defence systems engaged. Three Indian nationals sustained moderate injuries, according to the Fujairah Media Office. JPMorgan analysts had already flagged Brent and U.S. gasoline at yearly highs during the prior week, making today’s move an acceleration of an existing trend rather than an isolated spike.

The Brent crude spike above $125 on 30 April was the move that set the psychological floor for today’s session, with the prior close at $111.88 already embedding a risk premium that made the Fujairah attack’s 5.1% push to $113.67 a continuation rather than a reversal.

| Commodity | 4 May Price | 4 May Change | Pre-Crisis Baseline |

|---|---|---|---|

| Brent Crude | $113.67/bbl | +5.1% | ~$71-73/bbl |

| WTI Crude | $105.32/bbl | +3.32% | ~$68-70/bbl |

| Natural Gas | $2.862 | +2.95% | ~$2.40-2.50 |

For consumers, prices at this level translate directly into higher fuel costs. JPMorgan’s framing of strong domestic U.S. economic data against surging energy prices captures the tension that now defines the macro outlook.

When big ASX news breaks, our subscribers know first

What the Fujairah Oil Industry Zone is, and why attacking it matters

The Fujairah Oil Industry Zone spans approximately 12.8 million square metres along the UAE’s eastern coast. It is the largest commercial refined oil product storage hub in the Middle East, and it serves as a terminus for a pipeline that allows the UAE to export crude without routing it through the Strait of Hormuz.

That bypass function made Fujairah one of the few active workarounds during nine weeks of competing blockades. Its key strategic functions include:

- Pipeline bypass terminus for Gulf crude exports, avoiding the Strait of Hormuz

- Primary regional refined oil product storage hub

- Oil trading centre for physical and derivatives markets

- Bunkering hub for vessel refuelling operations

The UAE had already quit OPEC on 28 April 2026, making it a geopolitically isolated actor with independently significant infrastructure. The Fujairah attack struck a country that had just broken with the producer bloc while operating one of the few facilities keeping some Gulf crude flowing to global markets.

Why this pipeline bypass mattered so much

While the Strait of Hormuz remained choked, the Fujairah pipeline route functioned as a partial pressure-relief valve, allowing some export volumes to bypass the contested waterway entirely. Damaging it does not simply add to a list of regional grievances. It compounds the broader supply bottleneck by degrading the physical infrastructure that had kept at least a fraction of Gulf exports moving. That degradation explains why oil markets responded so sharply to this specific attack rather than treating it as routine regional noise.

What the Strait of Hormuz closure actually looks like from the water

Two blockades operate simultaneously in the strait. Iran enforces tolls and seizures on vessels transiting what it claims as territorial waters. The United States maintains a naval blockade targeting Iranian-linked vessels, seizing and redirecting tankers under a framework Washington calls “Project Freedom.” The result is a de facto stranglehold on commercial transit.

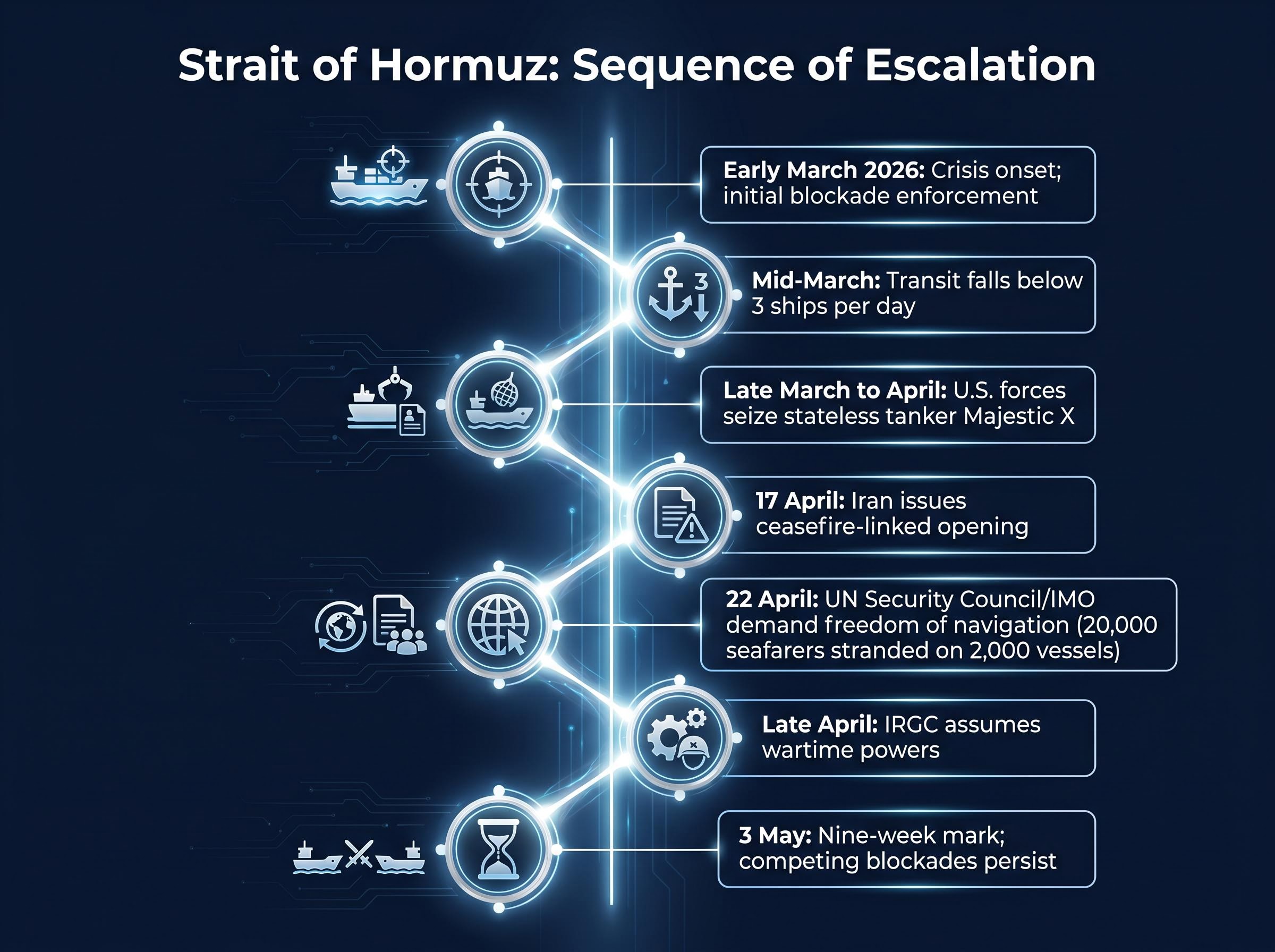

The sequence of escalation has unfolded as follows:

- Early March 2026: Crisis onset; initial blockade enforcement begins, transit volumes collapse

- Mid-March: Commercial transit falls below 3 ships per day at earlier crisis points

- Late March to April: U.S. forces seize stateless tanker Majestic X; at least two additional Iranian seizures confirmed

- 17 April: Iran issues ceasefire-linked opening for commercial vessels on designated routes

- 22 April: UN Security Council and IMO demand freedom of navigation, reporting approximately 20,000 seafarers stranded on approximately 2,000 vessels

- Late April: IRGC assumes wartime powers internally; President Trump claims U.S. forces disabled seven small Iranian watercraft. A South Korean vessel catches fire during Project Freedom operations

- 3 May: Nine-week mark; competing blockades persist with no signs of breaking

The two sides give directly contradictory accounts of what is actually transiting the strait. U.S. Central Command claims Project Freedom has reopened commercial routes. Iran’s IRNA has denied any commercial vessels or oil tankers cleared the strait.

Maritime historian Sal Mercogliano has characterised the operating environment as uniquely complex and dangerous, noting that the combination of competing U.S. and Iranian blockades, resurgent piracy, and stranded seafarers treated as geopolitical leverage creates conditions without a clear modern precedent.

Dark fleet activity, vessels operating with AIS transponders switched off, has compounded monitoring difficulties. That dispute over what is actually moving through the water directly affects how shipping insurers price coverage and whether cargo owners can secure tanker time at any rate, both of which feed into the physical supply dynamics behind today’s price numbers.

The dual blockade’s stranglehold on commercial transit is compounded by a third constraint the headline price numbers do not capture: war risk insurance withdrawal has made securing tanker coverage at any viable premium nearly impossible for cargo owners attempting to route through the strait, a dynamic that persists independently of military and political developments.

Why supply chain normalisation will take months, not days

Iran’s 17 April ceasefire-linked opening for commercial vessels on designated routes generated some diplomatic optimism. Traffic through the strait has not followed. Volumes remain far below pre-crisis levels despite the gesture.

A political agreement, even a durable one, would not translate quickly into restored supply. The physical constraints embedded in the global energy logistics chain do not respond to diplomatic timelines.

The physical lag that no ceasefire can fast-forward

The downstream bottlenecks preventing rapid normalisation include:

- Refinery ramp-up: Facilities that have been running below capacity or shut down require weeks to restart safely

- Tanker repositioning: Vessels rerouted around the Arabian Peninsula are not available for immediate Hormuz transit

- QatarEnergy LNG restart: Force majeure declared on 3 March 2026 means gas liquefaction facilities remain offline, with a restart expected to take weeks

- Inventory rebuild: Kuwait and UAE production shutdowns have depleted stockpiles that cannot be replenished overnight

- Piracy rerouting risk: Twin hijackings off Somalia on 27 April, with at least 3-4 hijackings in late April, add cost and delay to alternative routes

The IEA has described this as the greatest global energy security challenge in modern history, with approximately 20% of global oil supply and significant liquefied natural gas (LNG) volumes affected. Multiple economists and energy analysts have indicated normalisation could take several months even if the strait reopens immediately. Recovery timelines from historical comparators do not apply cleanly here because the dual blockade’s ongoing legal complexity has no precedent.

For investors pricing energy assets or hedging commodity exposure, the lag between a political deal and actual restored supply means a diplomatic headline is unlikely to immediately deflate the oil price premium that has built up over nine weeks.

OPEC+ output increase and why 188,000 barrels per day is not enough

OPEC+ announced on 3 May 2026 a confirmed output increase of 188,000 barrels per day for June 2026. The intention was clear: partially compensate for disrupted Gulf supply.

The scale tells a different story. The Strait of Hormuz carries approximately 20% of global oil supply. An increase of 188,000 barrels per day represents a fraction of the disrupted volumes.

- What OPEC+ announced: 188,000 barrels per day increase for June 2026

- What the disruption removed: Approximately one-fifth of global seaborne oil and significant LNG volumes

- What complicates future responses: The UAE’s exit from OPEC on 28 April fractures producer bloc cohesion

The IEA’s March 2026 estimate of a 0.8% addition to global inflation was calculated under conditions that have since worsened. With Brent above $113, that baseline figure is likely understated.

JPMorgan analysts have framed the central unresolved question for markets: will energy prices climb further and significantly hamper economic growth, or will diplomacy intervene before that threshold is crossed?

The gap between what OPEC+ announced and what the disruption has removed from global supply explains why prices have not responded to the supply-side policy move.

The OPEC+ June output decision was announced in the context of Gulf supplies being prevented from clearing the Strait of Hormuz, with the UAE’s independent capacity factored into assessments of how much the bloc could realistically compensate for disrupted volumes.

The picture taking shape for energy markets and the broader economy

Nine weeks of dual blockade. Brent above $113. Fujairah damaged. OPEC+ response insufficient. Normalisation months away. That is the state of the energy market as of 4 May 2026.

Cross-asset moves on the same session paint a broader picture.

| Asset | Level | Change |

|---|---|---|

| S&P 500 | 7,207.96 | -0.3% |

| NASDAQ | 25,075.23 | -0.2% |

| Dow Jones | 49,106.28 | -0.8% |

| VIX | 18.15 | +6.83% |

| U.S. Dollar Index | 98.315 | +0.32% |

| Gold Futures | $4,532.54 | -2.41% |

Equities falling, volatility rising, the dollar strengthening, gold declining. That pattern is consistent with geopolitical risk repricing rather than fundamental economic deterioration.

Oliver Pursche of Wealthspire Advisors noted that the domestic economy remains resilient and corporate earnings are solid, but geopolitical risk is dominating investor attention.

JPMorgan analysts have framed two scenarios as the decision fork ahead: further price escalation leading to meaningful drag on economic growth, or diplomatic resolution before that threshold is crossed. Economists have flagged worst-case risks including stagflation and recession driven by fuel and fertiliser shortages cascading through global supply chains.

The recession transmission channels activated by sustained high oil prices operate simultaneously rather than sequentially: reduced consumer disposable income, rising business input costs, Federal Reserve rate pressure, and an investment and hiring pullback each compound the others, a pattern that preceded every major US recession since 1973 and that Moody’s Analytics has now assigned a 48.6% probability of repeating in 2026.

What to watch in the days ahead as the crisis enters its tenth week

The specific signals that will determine whether this crisis deepens or finds an off-ramp fall into four categories:

- Military: U.S. Central Command operational updates on Project Freedom; further IRGC statements or actions in the strait

- Diplomatic: Any change in Iran’s ceasefire posture; movement on multilateral negotiations following the UN Security Council’s April demands

- Energy infrastructure: Fujairah Oil Industry Zone damage assessment and restart timeline; QatarEnergy force majeure restart (expected weeks away as of early March declaration)

- Commercial transit: Any measurable change in vessel volumes through the Strait of Hormuz; insurance pricing shifts from major underwriters

- Macroeconomic data: April nonfarm payrolls due Friday (week of 5-9 May 2026), which will be read against the energy price backdrop

- Corporate earnings: AMD, Super Micro Computer, and Disney are scheduled to report the same week, offering a window into how corporate outlooks are adjusting

The UAE’s post-OPEC status and QatarEnergy’s force majeure restart timeline are two under-watched threads that could move energy prices independently of the Hormuz situation. The IRGC’s assumption of wartime powers in late April has produced no near-term diplomatic reversal signals.

A crisis that has already rewritten the energy security playbook

The IEA called this the greatest global energy security challenge in modern history. Nine weeks of competing blockades have tested that assessment and confirmed it. Approximately 20,000 seafarers remain stranded on approximately 2,000 vessels. Normalisation, according to geopolitical analysts and shipping experts, remains months away.

What nine weeks of dual blockade have revealed is the fragility of the routing architecture that moves one-fifth of the world’s oil through a waterway narrow enough to be contested by a single state actor. The IRGC’s wartime powers remain in effect. No substantive diplomatic progress was visible as of 3 May.

Whether the reader is tracking energy exposure in a portfolio, managing a business exposed to fuel costs, or planning summer travel with an eye on petrol prices, the mechanics described in this article are what connect a military confrontation in a narrow waterway to prices paid at the pump. Consumer behaviour shifts are already visible, according to Wealthspire Advisors.

For readers wanting to trace how the blockade has already broken through into specific corporate earnings and industry outcomes, our full explainer on the Iran conflict’s economic cascade covers Spirit Airlines’ permanent closure, ExxonMobil and Chevron’s hedge-loss paradox, and the Federal Reserve’s rate-hold dilemma in detail, with the ISM Prices Paid index at a four-year high of 84.6 as the clearest indicator of where inflation pressure is heading.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.