Why Governance and Communication Drive Post-IPO Value

11 hrs ago

A $10,000 investment that controls $100,000 worth of shares is not fiction. It is the everyday reality of leveraged investing on the ASX, and the mechanics behind it are more accessible than most retail investors assume. With Australian self-managed super funds (SMSFs) holding over $1.05 trillion in assets as at 30 June 2025 and digital platforms continuing to lower the barrier to sophisticated instruments, understanding financial leverage has never been more immediately relevant. Yet the concept remains poorly understood, often conflated with reckless speculation rather than recognised as a structured technique with defined mechanics and manageable risk parameters. What follows explains how leverage works from first principles, walks through the practical ways Australian investors access it via ASX-listed instruments including Exchange-Traded Options and MINI Warrants, and makes the risks concrete so readers can approach the topic with clear-eyed confidence.

The word “leverage” borrows directly from mechanics: a lever allows a small input force to move a much larger output. Financial leverage works on the same principle. A small amount of personal capital, combined with borrowed funds, controls a position far larger than the investor’s own money could achieve alone.

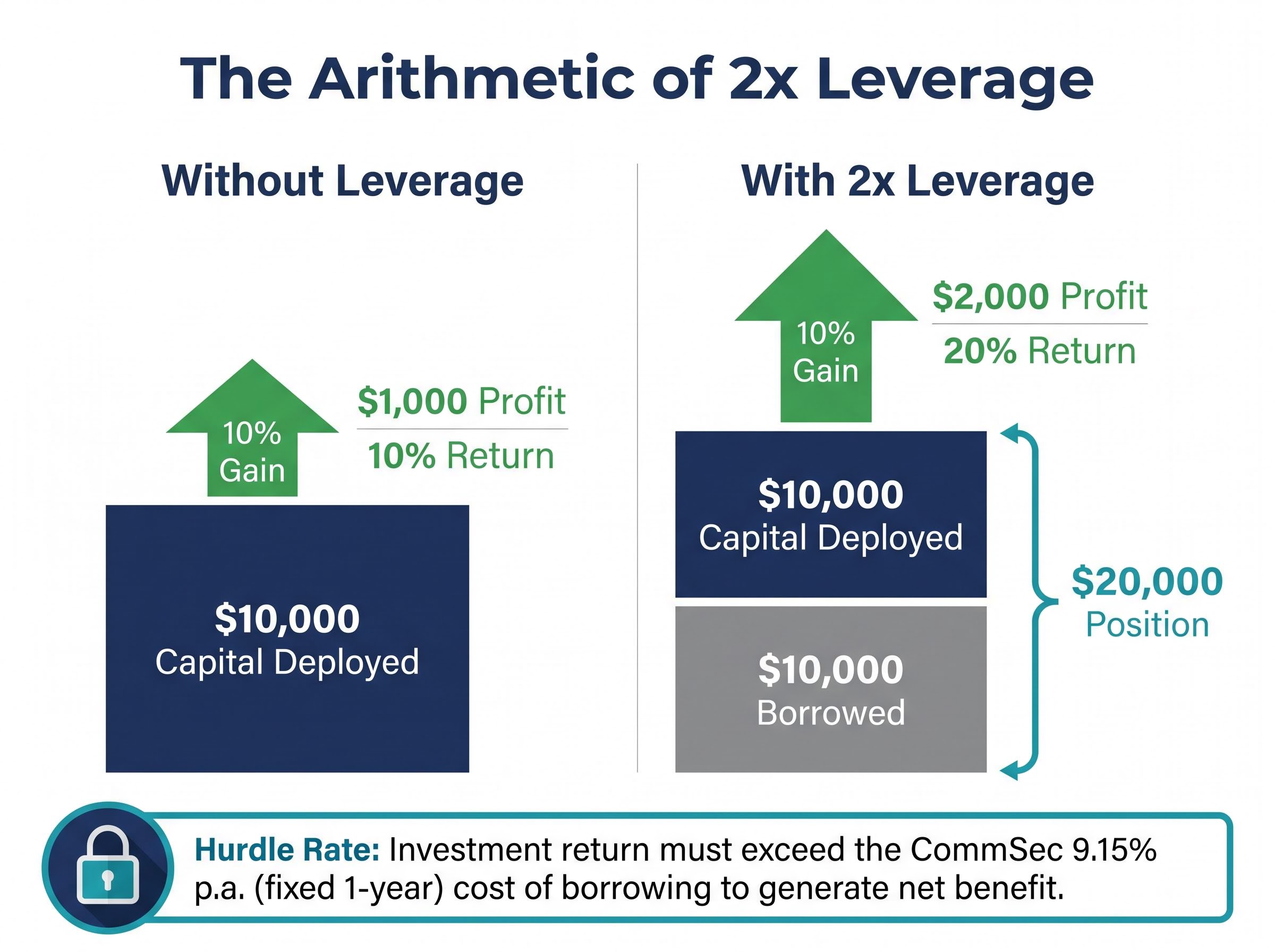

The arithmetic is straightforward. An investor contributes $10,000 of personal capital and borrows another $10,000, creating a $20,000 position. If the underlying asset rises 10%, the position gains $2,000. That $2,000 return on $10,000 of personal capital represents a 20% return, double the 10% the investor would have earned without borrowing.

Without leverage:

With leverage (2x):

The elegance conceals a condition. Leverage only generates net benefit when the investment return exceeds the cost of borrowing. With CommSec currently charging 9.15% p.a. fixed on one-year margin loans, the investment must clear that hurdle before a single dollar of leveraged profit materialises.

Leverage only generates net benefit when the investment return exceeds the borrowing cost.

That cost of capital is not a footnote. It is the variable that determines whether leverage amplifies wealth or quietly erodes it.

For retail investors operating through platforms such as CommSec or SelfWealth, leverage is accessed through three primary channels: margin lending against a share portfolio, exchange-traded derivative instruments, and internally leveraged products such as warrants.

Margin lending is the most familiar form. It involves borrowing against existing share holdings to fund additional positions, with the shares themselves serving as collateral. The current rate environment sets the cost: CommSec charges 9.15% p.a. fixed for one-year terms and 9.20% p.a. for two-year terms, meaning the return hurdle is material in the current cycle.

Loan to Value Ratios determine exactly how much a lender will advance against a given portfolio, ranging from 40% for volatile small-cap holdings to 80% for blue-chip shares, and the specific LVR assigned to each position directly sets the threshold at which a margin call is triggered.

The scale of self-directed investing in Australia adds context. SMSFs held $1.05 trillion in assets as at 30 June 2025, representing a substantial pool of capital where individual investors are making their own allocation decisions. Not all leveraged products carry equivalent consumer protections, however. ASIC’s January 2026 review of contracts-for-difference (CFD) providers found over 50% in breach of regulatory rules, resulting in $26 million returned to retail investors.

The ATO’s SMSF quarterly statistical report for June 2025 confirmed the $1.05 trillion figure, underscoring the scale of self-directed capital in Australia where individual trustees bear full responsibility for allocation and risk decisions.

The following table compares the three primary leverage channels available to Australian retail investors:

| Channel | How leverage is accessed | Approximate cost or premium | ASX-listed? | Key regulatory note |

|---|---|---|---|---|

| Margin Lending | Borrow against existing share portfolio | 9.15%-9.20% p.a. (CommSec fixed rates) | No (facility with broker) | Subject to margin calls if collateral value falls |

| MINI Warrants | Purchase ASX-listed warrant with built-in leverage | Embedded in warrant pricing; varies by product | Yes | Integrated stop-loss mechanism; read PDS before trading |

| Exchange-Traded Options | Pay a premium for the right to buy or sell shares at a set price | Premium varies by strike, expiry, and volatility | Yes | Maximum loss on long positions capped at premium paid |

Understanding which channels exist and what they currently cost helps investors assess whether a return thesis justifies leverage before committing capital.

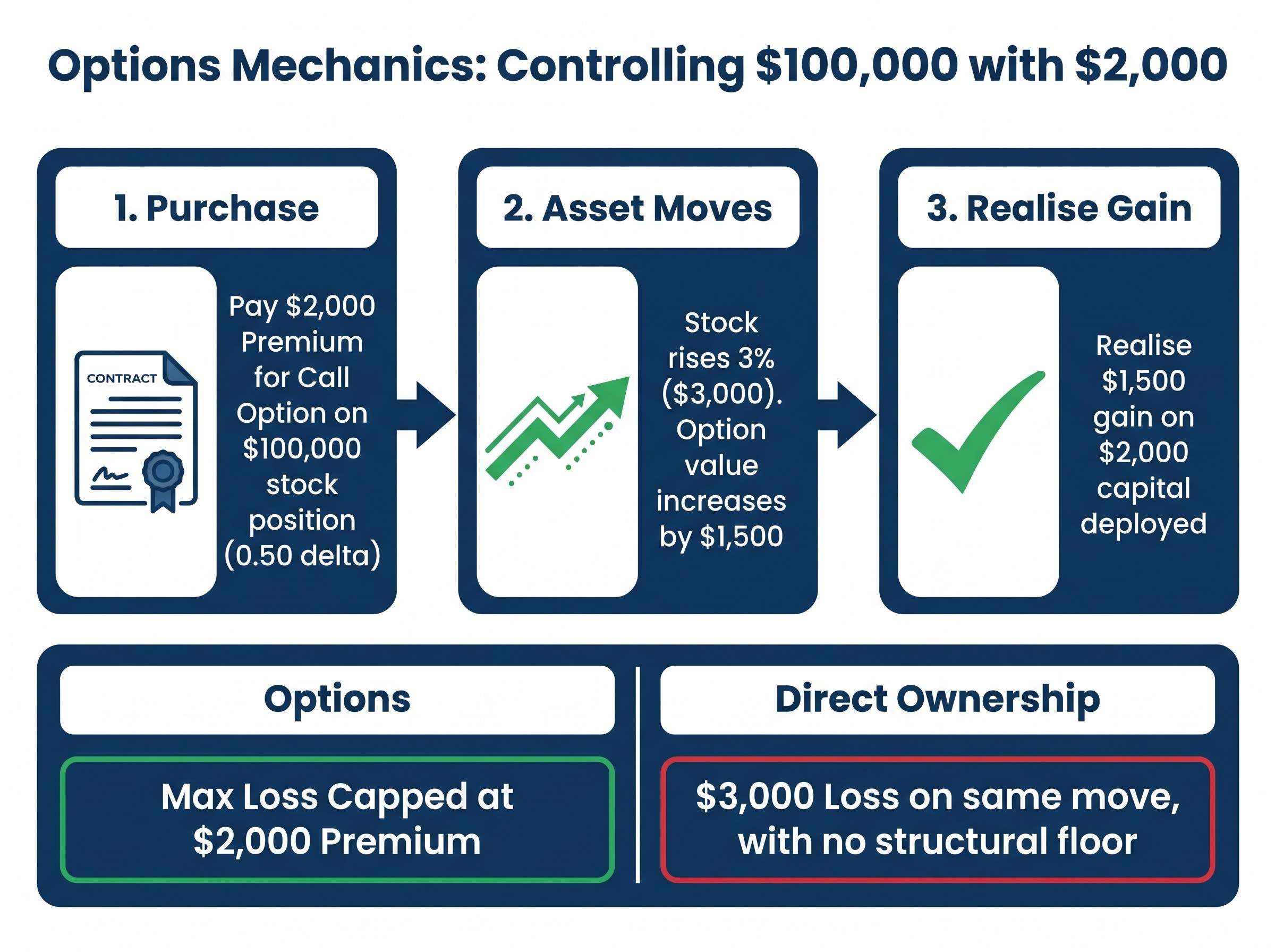

Exchange-Traded Options (ETOs) are contracts that confer the right, without obligation, to buy or sell an underlying ASX-listed asset at a predetermined price before a specified expiry date. A call option grants the right to buy; a put option grants the right to sell. The buyer pays a premium for this right, and that premium is the maximum amount they can lose.

Options create leveraged exposure because a relatively small premium payment controls a much larger parcel of shares. The relationship between the option’s price movement and the underlying asset’s movement is captured by a measure called delta. A delta of 0.50 means the option’s price moves approximately 50 cents for every $1 the underlying asset moves.

The mechanics of a single call option trade follow three steps:

If the stock falls instead, the maximum loss on the long option position is capped at the $2,000 premium paid. Direct ownership of the same position would expose the investor to a $3,000 loss on the same percentage move, with no structural floor.

With a long option position, the most an investor can lose is the premium paid. The leverage potential is magnified, but the floor is defined.

That defined-loss structure distinguishes options from margin lending, where losses can exceed the investor’s initial capital.

MINI Warrants are ASX-listed instruments that offer adjustable leverage across a range of underlying assets, including equities, commodities, index futures, and currencies. They are generally considered more accessible for newer or less experienced investors than standard options, in part because of their defining structural feature: a built-in stop-loss mechanism.

The four defining features of MINI Warrants are:

The leverage arithmetic is direct. On a $100,000 stock position with 5x leverage, the investor deploys $20,000 in capital. A 3% move in the underlying asset produces the same $3,000 dollar gain or loss as holding the shares directly, but with only one-fifth of the capital at risk.

The stop-loss automatically closes the position if the underlying asset’s price falls to the barrier level, preventing losses from extending beyond the capital invested in the warrant. This mechanism provides a structural floor that margin lending does not offer.

There is a caveat. In fast-moving or illiquid markets, the asset’s price can gap through the stop-loss level between trading intervals. When this occurs, the actual closing price may differ from the theoretical stop-loss level, meaning realised losses can occasionally exceed the expected protection. This gap risk is a specific and material consideration when evaluating MINI Warrants.

Leverage amplifies losses with exactly the same force it amplifies gains. A 50% decline in a 2x leveraged position does not halve the investor’s capital; it eliminates it entirely. The $20,000 borrowed must still be repaid, leaving the investor with zero personal capital and an outstanding debt.

The mechanics of a margin call make this worse in practice. When a leveraged position falls below the lender’s required collateral threshold, the investor must deposit additional funds or face forced liquidation of the position. Forced selling typically occurs at the worst possible time, locking in losses that might otherwise have been temporary.

Regulatory evidence confirms these risks are real and ongoing. ASIC’s January 2026 review of CFD providers found more than 50% in breach of regulatory rules, with $26 million returned to retail investors as a result. The RBA’s Financial Stability Review (October 2025) identified high leverage in certain strategies as a notable financial stability risk, extending the concern beyond individual portfolios to systemic exposure.

Leverage does not change the direction of market risk. It multiplies whatever the market does, in both directions, at the same rate.

Understanding the asymmetric timing dimension is equally important: gains accumulate over time, but forced losses can crystallise in hours. Before using any leveraged instrument, every retail investor should be able to answer three questions:

If any answer is unclear, leverage does not yet belong in the portfolio.

Margin lending suitability depends on three structural conditions that the rate environment has made more demanding: consistent after-cost returns that clear a borrowing rate now exceeding 10% per annum at some major providers, liquid reserves sufficient to meet a margin call without forced divestment, and income stability to service ongoing interest obligations across a full market cycle.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Leverage is most safely employed as a targeted, proportionate component of a broader portfolio rather than as a whole-of-portfolio approach. The size of any leveraged position should be scaled to the investor’s genuine capacity to absorb a total loss of the leveraged component without materially affecting their financial position.

Three practical steps for approaching leveraged instruments for the first time:

ASIC Regulatory Guide 240, updated in March 2026, sets out the disclosure expectations that apply to products involving leverage and derivatives, including requirements for issuers to present key risk metrics in a standardised format that retail investors can compare across products.

At a borrowing cost of 9.15% p.a., the investment must return more than 9.15% before leverage adds any net value. That hurdle was materially lower during the near-zero rate period of 2020-2022, meaning strategies that appeared effective then require higher-conviction positions today.

The principle does not change: leverage is a conditional tool, and the condition is that the return exceeds the cost. What changes is how demanding that condition becomes in different rate environments. The ASX and ASIC’s MoneySmart platform both provide educational resources for investors considering leveraged instruments, and reviewing these before allocating capital is a practical first step.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Leverage is a capital-efficiency tool. Its outcome depends entirely on the quality of the underlying investment decision, not on the leverage itself. Two conditions must both be present before it is appropriate: a credible return thesis that exceeds borrowing cost, and personal risk capacity to absorb the amplified downside without forced liquidation.

ASIC’s ongoing oversight, from the RG 240 update in March 2026 to the CFD provider review in January 2026, signals that the regulator expects informed, disciplined engagement from investors who choose these instruments. That expectation aligns with the core argument: leverage rewards preparation and punishes its absence, with equal force.

Investors considering leveraged instruments for the first time can explore the ASX’s Exchange-Traded Options and MINI Warrants educational resources, and review ASIC’s MoneySmart guidance on margin lending and derivatives, before making any leveraged investment decision.

Investors exploring leveraged instruments beyond ASX-listed options and warrants will find our full explainer on CFD leverage and margin covers the mechanics of margin rates, position sizing, and guaranteed stop-loss orders, alongside the ASIC REP 828 data showing nearly 70% of retail CFD traders recorded losses in 2026.

Financial leverage means using borrowed capital alongside your own money to control a larger investment position than your personal funds alone could achieve, amplifying both potential gains and potential losses proportionally.

MINI Warrants are ASX-listed instruments that provide built-in leverage across equities, commodities, indices, and currencies, with an integrated stop-loss mechanism that automatically closes the position at a predetermined barrier to limit losses.

CommSec currently charges 9.15% per annum fixed for one-year margin loans and 9.20% per annum for two-year terms, meaning a leveraged investment must return more than these rates before leverage adds any net value.

Leverage amplifies losses at the same rate it amplifies gains, margin calls can force asset sales at the worst possible time, and ASIC's January 2026 review found over 50% of CFD providers in breach of regulatory rules, resulting in $26 million returned to retail investors.

ASIC's March 2026 update to Regulatory Guide 240 expects retail investors to read the relevant Product Disclosure Statement before trading; experts also recommend paper-trading first and sizing any leveraged position so a total loss would not materially affect the broader portfolio.