An Australian investor holding $20,000 in shares can use that portfolio to borrow an additional $30,000 to invest, without selling a single holding. The mechanism that makes this possible is margin lending, a regulated form of borrowing to invest that uses an existing portfolio as security. With total Australian margin lending balances reaching $16.77 billion as of December 2025, the strategy carries real scale and real consequences. This article explains exactly how margin lending works, what determines borrowing capacity, what happens when markets move against a leveraged position, and what any investor needs to understand before considering the approach.

Gearing up: what margin lending actually is

Most Australians understand the logic of a home loan. A bank lends money to buy property, and the property itself serves as security for the loan. Margin lending applies the same structural principle to an investment portfolio.

Instead of property, the borrower pledges financial assets as collateral. A margin lender advances funds against those assets, allowing the investor to gain market exposure larger than their own capital would permit, without needing to liquidate existing holdings.

The types of collateral that margin lenders typically accept include:

- Listed shares on approved securities lists

- Managed funds meeting the lender’s eligibility criteria

- Cash deposits held within the lending facility

$16.77 billion: Total Australian margin lending balances as of December 2025, up from $15.48 billion in September 2025, reflecting meaningful quarterly growth in leveraged investment activity.

Margin lending sits within the broader category of gearing, the practice of borrowing to invest. It is regulated under Chapter 7 of the Corporations Act 2001 as a financial product, which means providers and advisers operate under Australian Securities and Investments Commission (ASIC) oversight. That regulatory framework shapes every aspect of how these loans are structured, disclosed, and managed.

When big ASX news breaks, our subscribers know first

How the Loan to Value Ratio determines your borrowing power

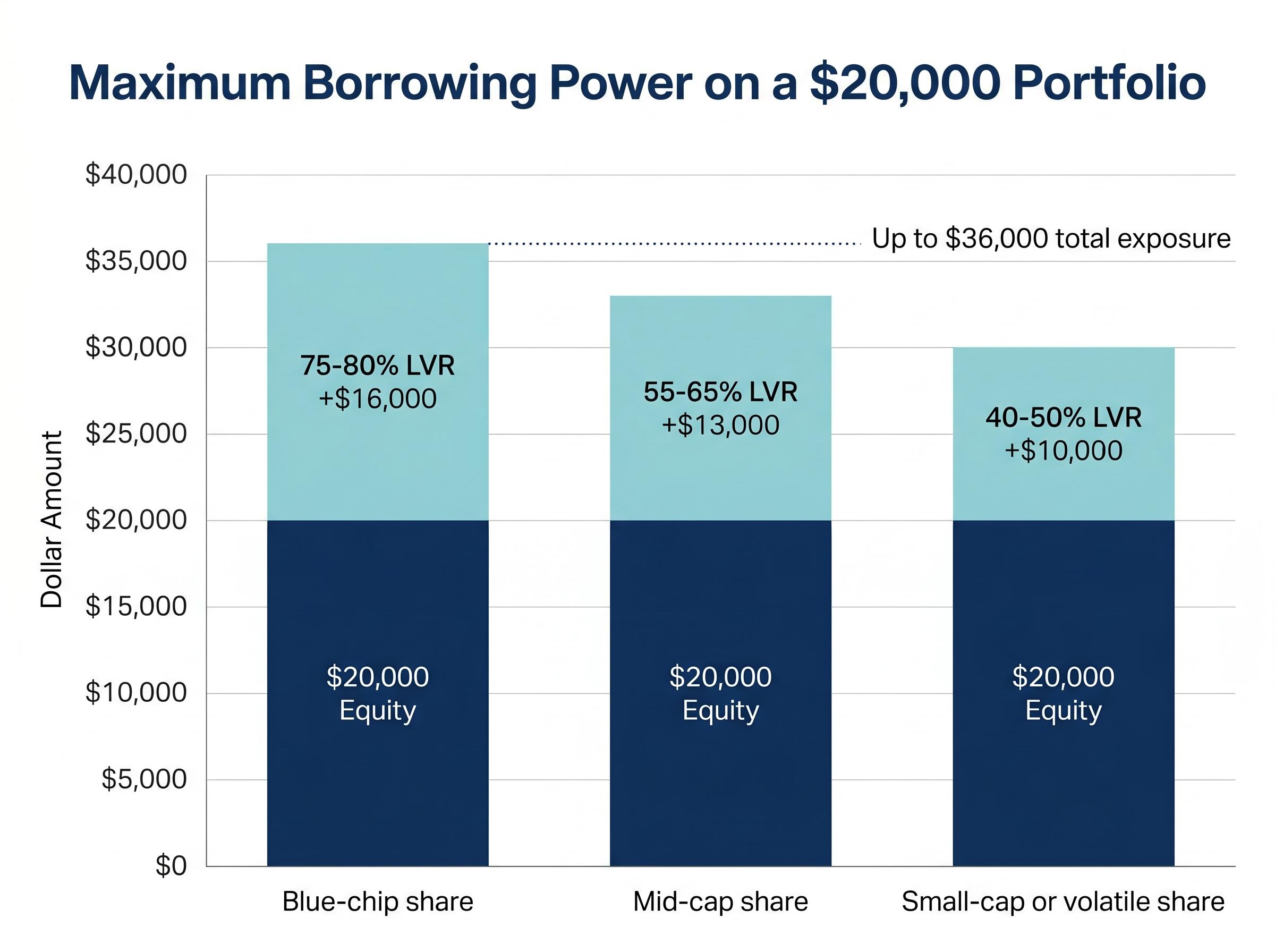

The Loan to Value Ratio (LVR) is the percentage of a portfolio’s value that a lender will advance as a loan. It is calculated by dividing the outstanding loan balance by the current market value of the pledged portfolio. The LVR is the single most important number in any margin lending arrangement because it determines how much an investor can borrow.

Not all securities attract the same LVR. Blue-chip shares, those with large market capitalisations and relatively stable price histories, typically sit at the higher end of the spectrum, with LVRs of 75-80%. Smaller or more volatile securities may attract LVRs as low as 40%, reflecting the greater risk they pose to the lender if the position needs to be liquidated quickly.

A worked example clarifies the mechanic. An investor holding $20,000 in blue-chip shares at an 80% LVR could borrow up to $16,000, giving total investment exposure of $36,000. The same investor holding $20,000 in a volatile small-cap name at 40% LVR would be limited to $8,000 in borrowing.

| Security Type | Indicative LVR | Portfolio Value Example | Maximum Loan Amount |

|---|---|---|---|

| Blue-chip share | 75-80% | $20,000 | $15,000-$16,000 |

| Mid-cap share | 55-65% | $20,000 | $11,000-$13,000 |

| Small-cap or volatile share | 40-50% | $20,000 | $8,000-$10,000 |

Borrowing capacity is also shaped by the borrower’s individual financial circumstances. An LVR determines the ceiling; the lender’s assessment of income, liabilities, and risk tolerance determines whether the borrower reaches it.

ASX bank concentration risk is directly relevant to margin lending because Australian investors who pledge ASX 200-aligned portfolios as collateral are often holding a heavily weighted bet on the four major banks; Morningstar flagged all four as overvalued in April 2026, and a valuation reset in that sector would compress collateral values and trigger LVR breaches simultaneously across many leveraged accounts.

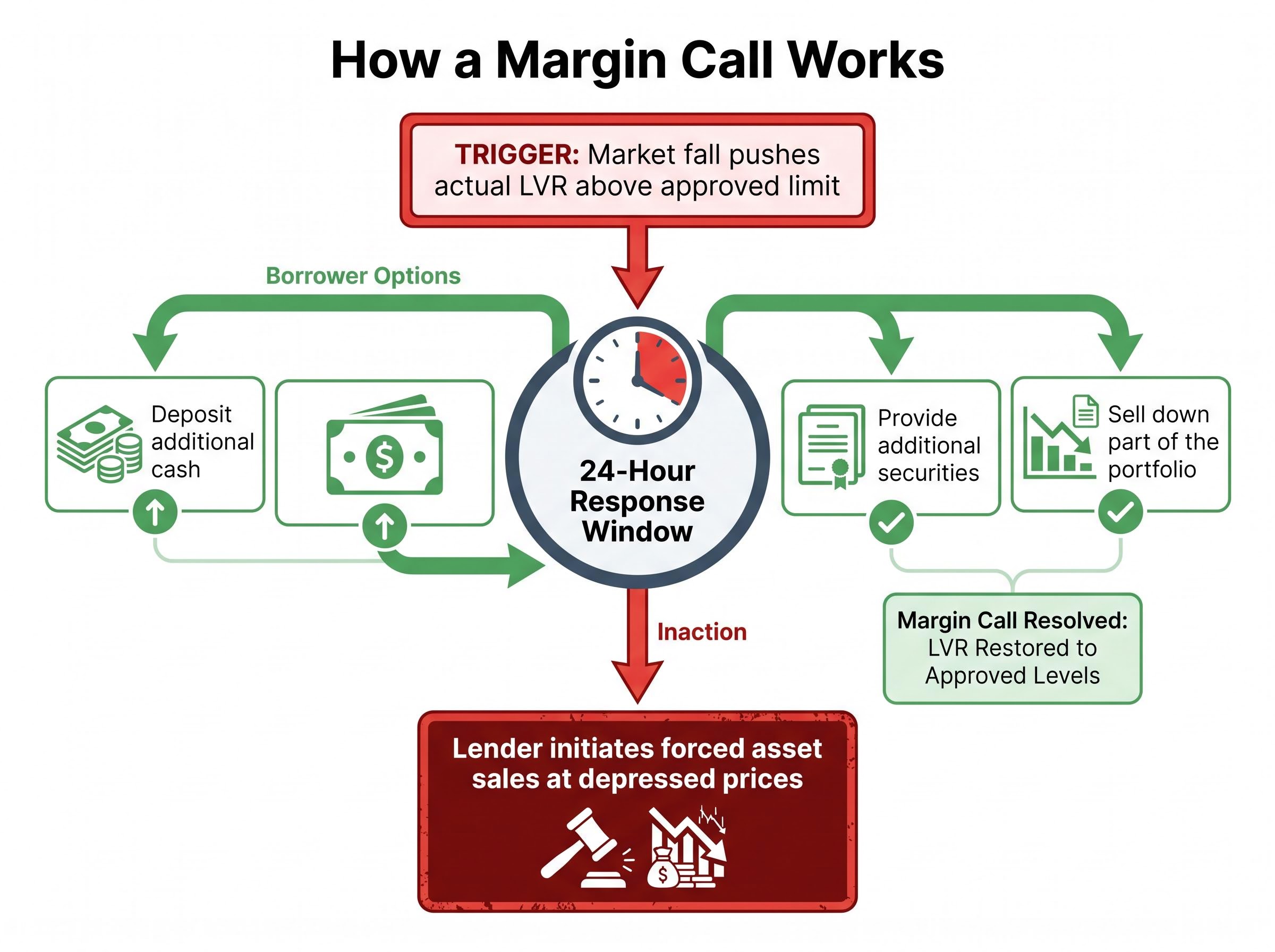

What happens when markets fall: understanding margin calls

A portfolio that sits comfortably within its LVR limit at the point of purchase can breach that limit without any action from the investor. All it takes is a fall in the market value of the pledged securities.

When the portfolio’s declining value pushes the actual LVR above the lender-approved limit, a margin call is triggered. This is the lender’s formal notification that the borrower’s account has moved outside agreed parameters, and corrective action is required.

The urgency is real. Borrowers typically have as little as 24 hours to respond to a margin call. If the borrower fails to act within that window, the lender has the contractual right to sell assets from the portfolio on the borrower’s behalf to bring the LVR back within the approved limit. Those forced sales may occur at depressed prices, crystallising losses the investor might otherwise have chosen to wait out.

ASIC’s 2026 regulatory outlook has identified risk disclosure for high-risk products as a priority area, with margin lending falling within that scope.

Your options when a margin call is triggered

Three corrective responses are available when a margin call is received:

- Deposit additional cash into the margin lending account, reducing the LVR by increasing the equity buffer.

- Provide additional securities as collateral, broadening the asset base the lender holds as security.

- Sell down part of the portfolio to reduce the outstanding loan balance directly.

The choice between these options depends on available liquidity, the tax consequences of selling (particularly whether a sale would crystallise a capital gain or loss), and the investor’s view of whether the market decline is temporary or structural.

The cost of borrowing and the potential tax offset

Interest is charged on the outstanding loan balance for as long as the margin loan remains open. Both variable and fixed-rate margin loans are available in Australia, and the rate directly affects whether the strategy generates a net return or destroys value.

Current rates across major Australian providers reflect the elevated benchmark rate environment of 2026:

| Provider | Variable Rate | 1-Year Fixed Rate | Notes |

|---|---|---|---|

| CommSec | 9.40% p.a. | 9.15-9.20% p.a. | Commonwealth Bank subsidiary |

| NAB Margin Loan | From approx. 8.75% p.a. (effective 1 April 2026) | 9.97% p.a. | Variable rate recently reduced |

| Interactive Brokers Australia | Approx. 6.778% p.a. | N/A | Benchmark rate plus 1.5-2.5%; notably lower than major banks |

Interest paid on a margin loan may be tax-deductible in Australia where the borrowed funds are used to generate assessable income, such as dividends or distributions. This potential offset reduces the effective cost of borrowing, though the benefit varies by individual circumstance and professional tax advice should be sought before relying on it.

The RBA rate hike outlook is material to any margin lending decision made in 2026: a 25 basis point increase to 4.35% would push variable margin loan rates higher still, widening the gap between borrowing costs and investment returns that borrowers are already working against.

Investment returns must exceed the cost of borrowing for the strategy to deliver a net positive outcome. At current Australian rates, that return hurdle sits between approximately 6.8% and 9.4% per annum before the tax treatment is factored in.

The risks every first-time borrower must weigh

Four risks sit at the centre of any margin lending decision, and each carries specific consequences a borrower should be able to visualise before committing:

- Amplified losses from leverage: A 10% fall in a fully leveraged portfolio does not produce a 10% loss on the investor’s equity. It produces a significantly larger percentage loss because the investor’s own capital absorbs the full impact of the decline while the loan obligation remains unchanged.

- Speed and consequences of margin calls: A margin call can arrive within days of a market correction, and the 24-hour response window leaves limited room for deliberation. Inaction triggers forced asset sales.

- Variable interest rate exposure: Borrowers on variable rates face the risk that rate increases will raise their cost of carry, widening the gap between borrowing costs and investment returns.

- Forced asset sales at inopportune prices: If the lender liquidates pledged assets to meet a margin call, sales occur at prevailing market prices, which during a correction may be well below fair value.

Losses from a leveraged position must still be combined with the obligation to repay the loan in full, regardless of market direction. An investor can lose more than their original capital.

Why the current environment raises the stakes

The 2026 environment compounds these structural risks. The Reserve Bank of Australia’s March 2026 Financial Stability Review noted overall financial system resilience but flagged increased risks from non-bank lending growth. ASIC’s 2026 outlook identified high-risk products as a priority concern for consumer losses. Cost-of-living pressures, elevated geopolitical volatility, and higher-for-longer interest rate conditions mean the margin for error on a leveraged strategy is narrower than it was during the low-rate environment of 2020-2021.

The RBA March 2026 Financial Stability Review confirmed overall system resilience while specifically flagging non-bank lending growth as a source of increasing risk, a finding that sits directly alongside the elevated interest rate environment shaping borrowing costs for leveraged investors today.

The regulatory floor underneath Australian margin lending

Margin lending is not an unregulated corner of the market. It is classified as a financial product under Chapter 7 of the Corporations Act 2001, a status established by the Corporations Legislation Amendment (Financial Services Modernisation) Act 2009, which commenced on 1 January 2010. Prior to that date, margin loans were not covered under the Consumer Credit Code, leaving borrowers with fewer formal protections.

Under the current framework, the protections available to borrowers include:

- Product disclosure: Providers must issue a Product Disclosure Statement outlining fees, risks, and terms.

- AFS licence requirement: Both margin lending providers and the advisers who recommend these products must hold an Australian Financial Services licence from ASIC.

- Responsible lending obligations: Lenders are required to assess the suitability of the product for the borrower’s circumstances.

- Dispute resolution access: Borrowers have access to external dispute resolution through ASIC-approved schemes if a complaint cannot be resolved directly with the provider.

ASIC maintains ongoing oversight of compliance within this framework, with recent updates focusing on risk disclosure standards for high-risk products. For a first-time borrower, this regulatory structure means clear entitlements: the right to disclosure, the right to appropriately assessed lending, and the right to recourse if something goes wrong.

Before you borrow, know what you are signing up for

The investor from the opening scenario, holding $20,000 in shares and considering borrowing against them, now has a clearer picture. They understand that an LVR determines how much they can borrow, that a margin call can arrive within 24 hours of a market decline, that interest rates at current levels demand returns north of 6.8-9.4% per annum to break even, and that a regulated framework provides disclosure and dispute resolution but does not eliminate the risk of loss.

Margin lending is a legitimate and regulated strategy that can expand an investor’s market exposure. It is not inherently suitable or unsuitable for any individual. Suitability depends on financial resilience, investment horizon, and the capacity to meet a margin call without being forced to sell at a loss.

Systematic investing strategies such as dollar-cost averaging into diversified index products sit at the opposite end of the risk spectrum from margin lending, and investors weighing the two approaches often find that the discipline required to execute one is structurally incompatible with the reactive decision-making that margin calls can force.

The logical next step for any investor weighing this strategy is a conversation with a licensed financial adviser who can model the approach against their individual circumstances, risk tolerance, and tax position.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.