Why 30% Recession Odds Are Harder to Trade Than 60%

9 mins ago

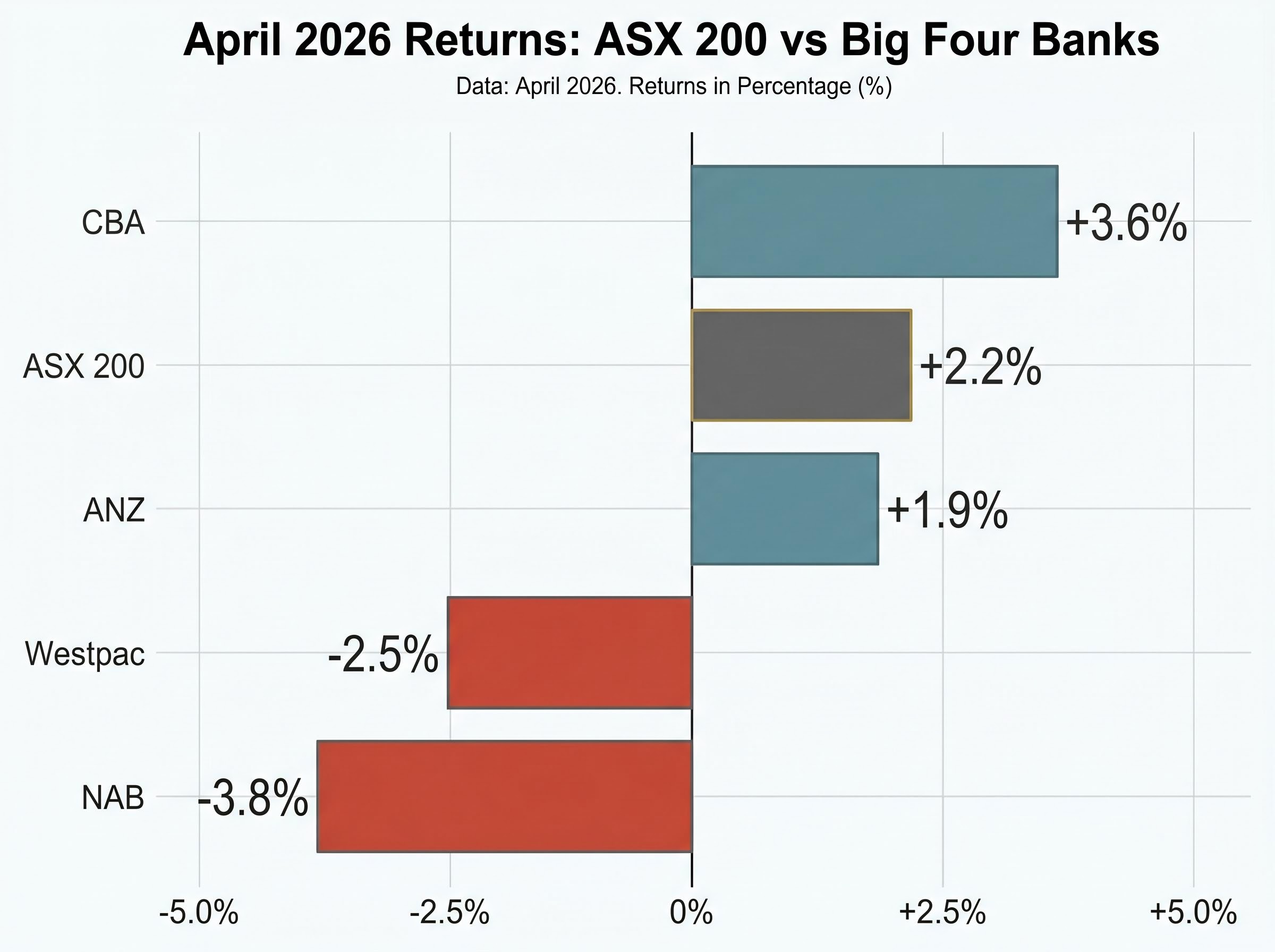

In April 2026, the ASX 200 returned +2.2%. Commonwealth Bank added 3.6%. ANZ gained 1.9%. The big four banks, as a group, appeared to be tracking with the broader market.

Then two of them fell sharply, each on the same day their management chose to speak to investors.

Westpac dropped -2.6% on 14 April, the day it released a pre-results trading update. NAB fell -3.6% on 20 April, after publishing an operational update that flagged a $706 million credit impairment charge. Neither bank had reported a single line of official half-year results. Both finished the month in negative territory while their peers climbed.

With NAB’s results released on 4 May and Westpac’s scheduled for 5 May, the April disclosures represent the clearest available signal about what investors will be scrutinising in those reports. What follows is an analysis of what each disclosure actually said, why markets reacted the way they did, and what the combined picture reveals about reading pre-results communications as forward-looking risk signals for ASX bank stock exposure.

The numbers tell the story before any interpretation is required. Two banks outperformed the ASX 200 in April. Two underperformed it by a wide margin.

| Bank | April 2026 return | Single-day disclosure drop | Closing price (30 April) |

|---|---|---|---|

| CBA | +3.6% | N/A | $173.66 |

| ANZ | +1.9% | N/A | $36.65 |

| Westpac | -2.5% | -2.6% (14 April) | $38.50 |

| NAB | -3.8% | -3.6% (20 April) | $39.88 |

The key divergence facts:

Neither sell-off was driven by a broad market event. Both were triggered by company-specific communications released before official results. That distinction matters: the question is not whether bank stocks fell in April, but why the market responded so differently to what each bank chose to say.

Sector-level momentum and individual stock fundamentals have diverged sharply in 2026, with the 10.5 percentage point spread between CBA’s year-to-date gain and NAB’s year-to-date decline illustrating that broad financials exposure and selective stock positioning have produced very different outcomes.

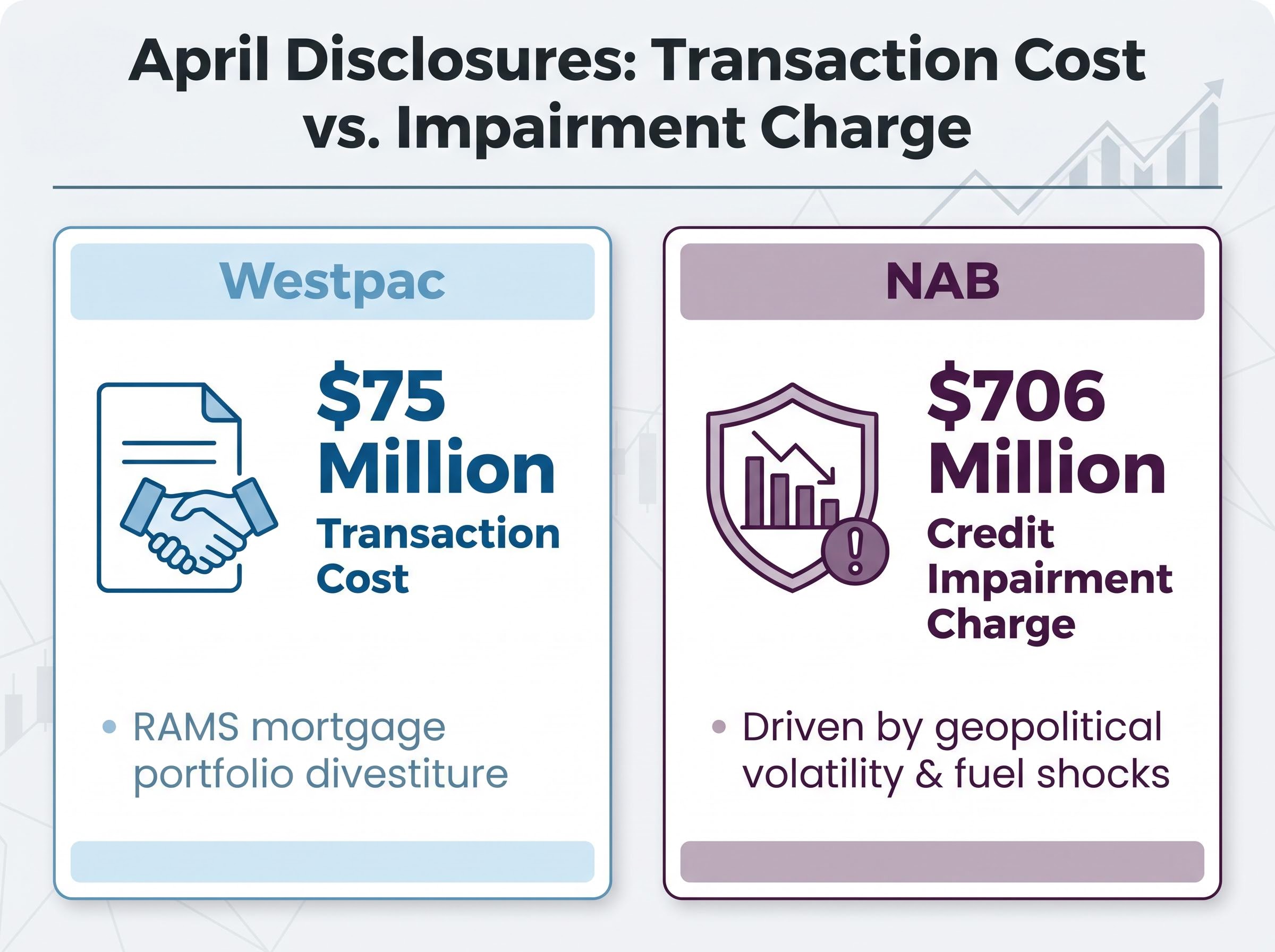

Westpac’s 14 April trading update carried a headline number that hit the share price immediately: a $75 million reduction to net profit after tax from transaction costs associated with the sale of its RAMS mortgage portfolio.

The sale, to a consortium comprising Pepper Money Ltd (ASX: PPM), KKR, and PIMCO, was on track for completion in H2 FY26. The RAMS exit represented a strategic decision to shed a non-core lending brand, not a response to credit stress.

The $75 million NPAT reduction represents transaction costs from the RAMS divestiture. It is a one-off cost of selling an asset, not a write-down of loans or a signal of deteriorating credit quality.

The market’s -2.6% reaction reflected the headline impact on near-term earnings. What the update also contained, and what the single-day sell-off may have initially underweighted, was a set of operational metrics pointing in the opposite direction.

The same trading update included:

The provisions increase is worth noting separately. A bank raising its collective provisions ratio is building a buffer against potential future losses across its loan book, a precautionary step that reflects awareness of macroeconomic uncertainty rather than identification of specific problem loans. Westpac’s build to 1.29% signals macro caution, not portfolio stress.

NIM expansion and transition cost trade-offs at regional banks like Bendigo illustrate how the same financial metrics investors scrutinise in big four disclosures, net interest margin stability, provisions trajectory, and cost discipline, play out differently when a bank is mid-way through a structural transformation rather than operating at scale.

Two banks disclosed earnings headwinds in the same month. The market treated one as a temporary cost and the other as a more serious signal. Understanding why requires separating two categories of disclosure that Australian bank investors encounter regularly.

A credit impairment charge is a bank’s recognition that specific loans or portfolios may not be fully recoverable, requiring capital to be set aside now against expected future losses.

A transaction cost, by contrast, is a one-off outflow tied to a specific event, such as selling an asset or restructuring a business unit. It carries no implication about the quality of the remaining loan book.

| Characteristic | Transaction cost (Westpac) | Credit impairment charge (NAB) |

|---|---|---|

| Definition | One-off cost of completing an asset sale | Capital set aside for loans expected to underperform |

| Trigger | RAMS portfolio divestiture | Geopolitical volatility, fuel shocks, sector stress |

| Balance sheet impact | Reduces NPAT in the period; no ongoing drag | Increases provisions; may recur if conditions worsen |

| Forward-looking signal | Low: reflects a completed strategic decision | High: reflects management’s view of near-term loan risk |

| Investor interpretation | Assess whether core earnings offset the one-off hit | Assess whether the charge is sufficient or may grow |

NAB’s $706 million charge, driven by geopolitical volatility and its spillover into agriculture, transport, and manufacturing, carries forward-looking implications that Westpac’s $75 million divestiture cost does not. The size of NAB’s charge, the largest single provisioning event disclosed by any of the big four during this reporting cycle, compounds the distinction. Conflating the two types of disclosure produces mispriced reactions in either direction.

The abstract concept of credit impairment becomes concrete when traced from its geopolitical origin to its dollar figure on a bank’s books. NAB’s $706 million charge, to be recorded in H1 2026, followed a specific transmission path.

The connection between a geopolitical conflict and an Australian bank’s earnings runs through fuel. When Middle East disruption pushes oil and diesel prices higher, Australian farmers face rising costs for machinery, fertiliser transport, and irrigation. Freight operators absorb higher fuel bills on thin margins. Manufacturers dependent on imported components see both input costs and shipping costs climb.

Banks do not wait for those borrowers to miss payments. Under forward-looking impairment accounting, management assesses the probability that macroeconomic conditions will cause loan losses and sets aside capital now. That is what NAB did on 20 April.

The RBA Financial Stability Review for March 2026 identified elevated geopolitical tensions, particularly Middle East conflict, as a source of severe potential shock through oil and commodity market disruptions, providing the macro-level risk assessment framework that informed NAB’s decision to raise forward-looking provisions across fuel-exposed sectors.

The market’s response was immediate. NAB shares dropped -3.6% on disclosure day and finished the month down -3.8%. For context, CBA’s February results had shown profit rising 5% with improved credit quality, making NAB’s charge stand out further against the sector backdrop.

The Westpac and NAB disclosures illustrate how the same event type, a voluntary pre-results update, can carry fundamentally different implications depending on what is disclosed. Three questions form a useful framework for any investor assessing a big four bank’s mid-period communication:

Voluntary pre-results disclosures are not required. When a bank chooses to speak before it must, the content of that communication reflects management’s own assessment of what investors need to know before the official numbers arrive.

Analyst consensus on big four valuations adds another layer to the April divergence story, with three of the four banks carrying sell ratings and implied 12-month downsides ranging from 13% to more than 50%, a backdrop that makes market sensitivity to any negative disclosure materially higher than it would be at more neutral starting valuations.

The near-term checkpoint arrives within days. NAB reported half-year results on 4 May, and Westpac is scheduled for 5 May. ANZ’s results, released on 1 May, showed statutory profit of $3,650 million and cash profit of $3,780 million (up 70% on the prior second half), providing a constructive data point for the sector heading into the final two reports.

Widening the lens beyond the two underperformers reveals a sector that entered May on broadly stable footing.

No confirmed evidence of a broad sector rotation away from big four bank stocks had emerged as of early May 2026. The combination of dividend appeal, above-market earnings growth from CBA and ANZ, and cost discipline from Westpac appeared to sustain both institutional and retail interest in the sector.

ASX 200 index concentration in the big four means that a provisioning event at a single bank does not stay contained to that stock; it applies downward pressure across the financials sector, which collectively represents around 25% of the entire index by market capitalisation.

The distinction between sector-level resilience and stock-specific risk differentiation is where the analysis sharpens. Westpac’s one-off transaction cost and NAB’s geopolitical provisioning represent meaningfully different risk profiles, even though both produced negative monthly returns.

Investors holding big four bank exposure can verify whether the pre-results signals aligned with confirmed numbers by reviewing NAB’s 4 May and Westpac’s 5 May official ASX filings. ANZ’s strong 1 May result provides a constructive anchor ahead of Westpac’s report. APRA’s quarterly ADI statistics offer the regulatory-level data for tracking sector-wide provisioning trends beyond individual disclosures.

The APRA quarterly ADI statistics track aggregate capital adequacy, asset quality, and provisioning ratios across all authorised deposit-taking institutions, giving investors a sector-wide benchmark against which individual bank collective provisions ratios, including Westpac’s build to 1.29%, can be assessed in context.

April 2026 gave ASX bank investors two templates they will encounter repeatedly across reporting cycles. One bank disclosed a transactional cost associated with a strategic exit; the market absorbed the headline, found the operational detail underneath, and the stock stabilised. Another bank disclosed a credit risk provision driven by geopolitical forces flowing into the domestic loan book; the market re-priced the stock more aggressively and carried that re-pricing into month-end.

The analytical value of these two events lies less in the specific dollar figures and more in the framework they illustrate. Voluntary mid-period disclosures are a management communication choice. Learning to distinguish what each type reveals about risk assessment, and what it does not, is more durable investor knowledge than tracking any single month’s price movement.

Disclosure literacy, the ability to separate noise from signal before results are officially confirmed, is a repeatable analytical edge for investors managing big four bank exposure.

The confirmed results from NAB and Westpac will add the next data layer. APRA’s quarterly ADI statistics will provide the sector-level provisioning context. April’s disclosures provided the questions; May’s numbers will begin to provide the answers.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

A credit impairment charge is capital a bank sets aside for loans it expects may not be fully recoverable, representing a forward-looking assessment of loan book risk. For ASX bank stocks, a large impairment charge like NAB's $706 million signals management concern about near-term loan losses, which can weigh on earnings and the share price.

NAB dropped 3.6% on 20 April after disclosing a $706 million credit impairment charge linked to geopolitical volatility and stress in agriculture, transport, and manufacturing sectors, while Westpac's 2.6% fall on 14 April reflected a one-off $75 million transaction cost from selling its RAMS mortgage portfolio. Markets treated NAB's charge as a higher-risk, potentially recurring signal compared to Westpac's one-off divestiture cost.

Middle East conflict and associated fuel price shocks raise operating costs for Australian borrowers in fuel-exposed sectors such as agriculture, transport, and manufacturing, increasing the probability of loan defaults. Banks like NAB respond by raising credit provisions ahead of actual defaults, which directly reduces reported profit.

Investors should determine whether a disclosed cost is a one-off item or a recurring earnings drag, assess whether it signals loan book stress or a strategic portfolio decision, and examine accompanying operational metrics such as net interest margin, lending growth, and expense trends for context.

CBA gained 3.6% and ANZ rose 1.9% in April 2026, both tracking at or above the ASX 200's 2.2% return, while NAB fell 3.8% and Westpac declined 2.5%, with both underperformers suffering sharp single-day drops on the days they released voluntary pre-results updates.